Silicon Tetrachloride Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

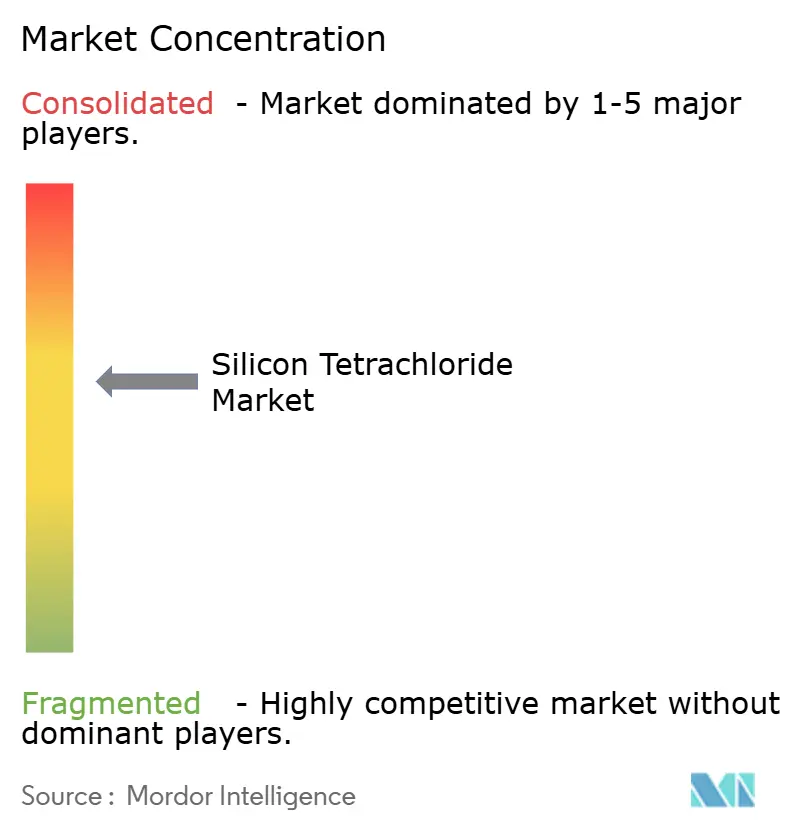

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicon Tetrachloride Market Analysis by Mordor Intelligence

The Silicon Tetrachloride Market size is projected to be USD 2.71 billion in 2025, USD 2.82 billion in 2026, and reach USD 3.45 billion by 2031, growing at a CAGR of 4.12% from 2026 to 2031. An aggressive push toward closed-loop chlorosilane recycling in Chinese polysilicon plants, rising 5G back-haul fiber demand, and semiconductor capacity expansions in North America and Southeast Asia are reshaping every tier of the value chain. Electronic-grade material is gaining prominence as 7N-9N purity becomes standard for advanced nodes, while on-site gas production strategies adopted by leading specialty-gas suppliers diminish long-haul ISO-tank shipments. Integrated producers are consolidating lower-quality capacity, raising the floor for technical-grade purity and tightening feedstock availability. Simultaneously, emerging Middle-Eastern polysilicon projects powered by low-cost renewables signal the arrival of new regional demand nodes for silicon tetrachloride market participants.

Key Report Takeaways

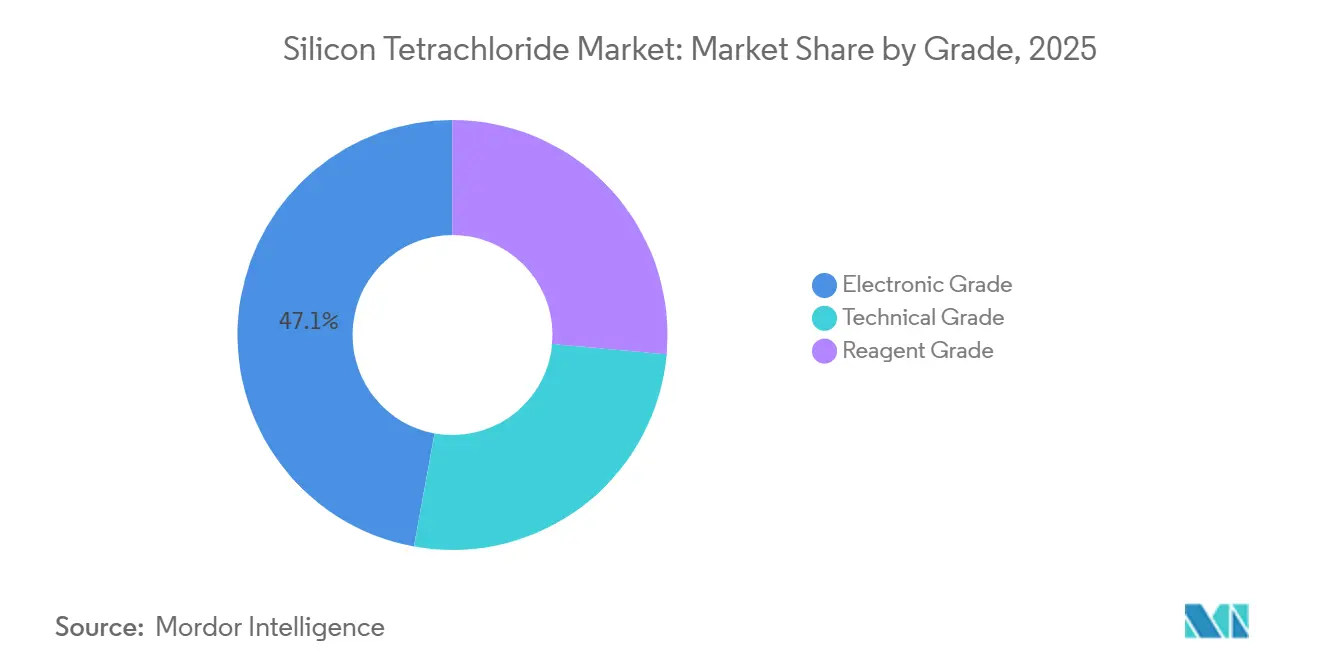

- By grade, electronic grade led with 47.13% of the silicon tetrachloride market share in 2025 and is expected to progress at a 4.61% CAGR during the forecast period (2026-2031).

- By application, electronics and semiconductors commanded 35.22% share of the silicon tetrachloride market size in 2025, while optical-fiber preforms are advancing at a 4.95% CAGR to 2031.

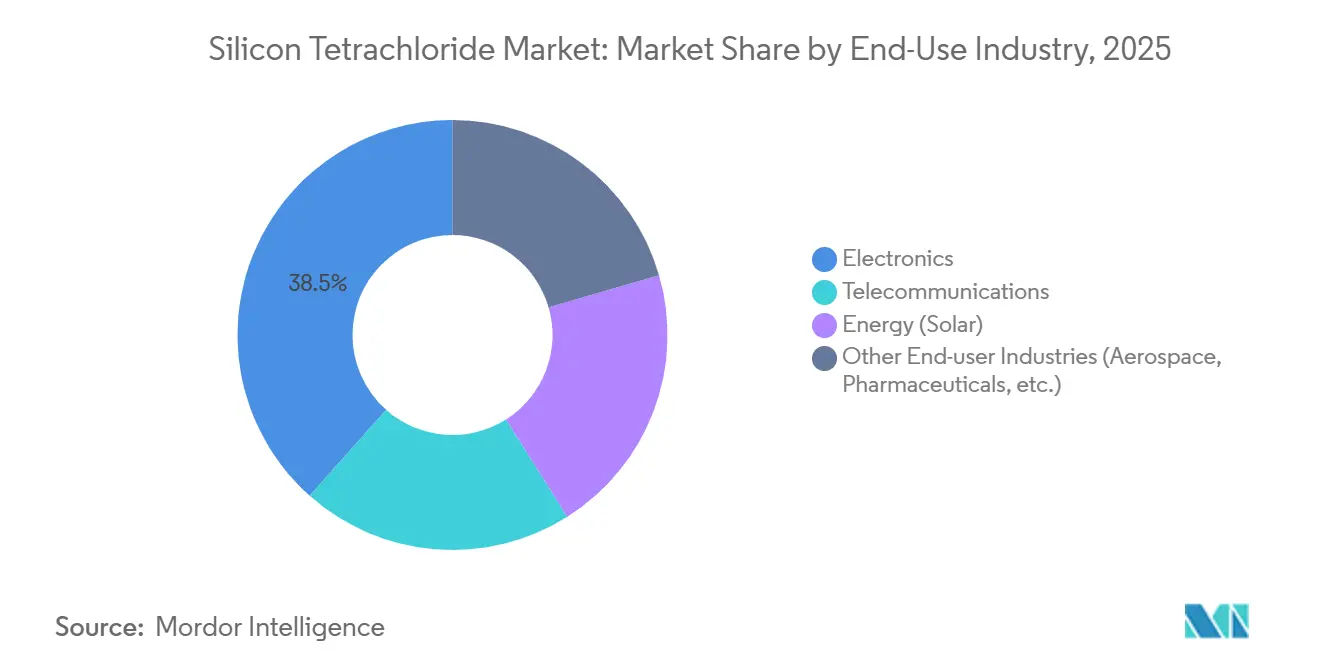

- By end-use industry, electronics accounted for 38.45% revenue in 2025; the telecommunications industry is expected to record the fastest 4.89% CAGR to 2031.

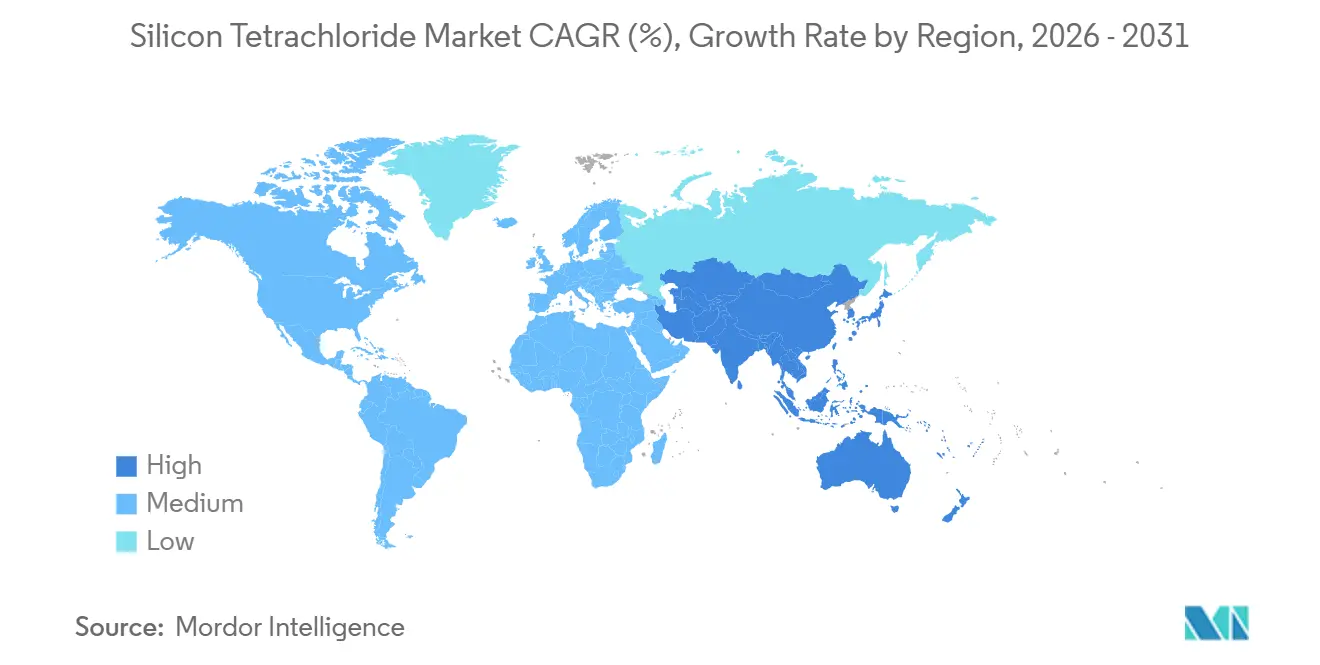

- By geography, Asia-Pacific held 57.45% revenue in 2025 and is expanding at a 4.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silicon Tetrachloride Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for optical fibres in telecommunications | +1.2% | Global, with concentration in APAC (China, India) and North America (5G/FTTH buildout) | Medium term (2-4 years) |

| Expanding use in polysilicon for solar photovoltaics | +1.5% | APAC core (China, India, ASEAN), spill-over to Middle East (Oman, Saudi Arabia) | Long term (≥ 4 years) |

| Rising investments in semiconductor manufacturing | +0.9% | North America (CHIPS Act), Europe (Dresden), APAC (South Korea, Japan, Malaysia) | Medium term (2-4 years) |

| Expanding adoption in fumed silica and silane chains | +0.7% | Global, with APAC (China 45% share) and North America (automotive/EV silicones) | Long term (≥ 4 years) |

| Ultra-low-loss hollow-core fibre and metamaterial R&D needing 7N-plus SiCl₄ | +0.3% | North America, Europe (research institutions), Japan (Tokuyama) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Optical Fibres in Telecommunications

Global telecom build-outs are tightening demand for high-purity SiCl₄ because MCVD (Modified Chemical Vapor Deposition), PCVD (Plasma Chemical Vapor Deposition), OVD (Outside Vapor Deposition), and VAD (Vapor Axial Deposition) preform routes all rely on the reaction of SiCl₄ and oxygen to form silica soot that is later consolidated into glass. VAD and OVD deliver the highest throughput, producing preforms that yield up to 250 km of fiber each, while PCVD offers 100% precursor conversion but drives purity specifications to 6N-7N[1]Fiberoptix Ltd., “Advancements in VAD and OVD Preform Manufacturing,” fiberoptix.com. Active 5G macro- and small-cell densification in China and accelerating FTTH (Fiber to the Home) roll-outs in India underpin the Asia-Pacific pull on the silicon tetrachloride market. North American and European data-center operators moving to 400G/800G coherent optics are also contributing, especially for ultra-low-loss fibers that require 7N-plus feedstock. Specialized research into hollow-core and metamaterial fibers further elevates purity requirements and sustains premium pricing on electronic-grade supplies.

Expanding Use in Polysilicon for Solar Photovoltaics

Polysilicon remains the largest single consumer of SiCl₄, yet oversupply and price pressure have forced widespread consolidation inside China. The top six producers collectively raised more than CNY 50 billion (USD 6.96 billion) in 2025 to acquire and idle roughly 1 million tons of obsolete capacity, a move that tightened technical-grade availability and helped stabilize prices. At the same time, fluidized bed reactor technology is gaining share because it cuts energy consumption by about 25% and generates less SiCl₄ per kilogram of polysilicon, slightly tempering absolute volume growth. N-type solar cells captured half of the global market share in 2023 and demand polysilicon purity of 9N-11N, indirectly pushing SiCl₄ purification technology to new limits. Emerging Middle-Eastern production, such as the 100 kilotons-per-year Sohar plant in Oman, will diversify the silicon tetrachloride market geographically while preserving long-term demand momentum.

Rising Investments in Semiconductor Manufacturing

The CHIPS Act in the United States and comparable incentive schemes in the European Union and Malaysia are catalyzing a wave of new 300 mm fabs. Each site consumes 25-1,000 kg of SiCl₄ annually for CVD (Chemical Vapor Deposition) processes, a modest tonnage but demanding 7N-9N grades[2]Semiconductor Industry Association & OECD, “Emission Scenario Document for Chemical Vapor Deposition,” sia.org. Specialty-gas giants are countering logistics bottlenecks by constructing on-site generation plants, as exemplified by multibillion-dollar projects in Dresden and Singapore, trimming ISO-tank dependence and lowering residual emissions. Malaysia’s 10 kilotons semiconductor-grade polysilicon joint venture, powered by renewable hydropower, positions Southeast Asia as a reliable hub for extreme-purity feedstock and strengthens regional resilience against geopolitical supply shocks.

Expanding Adoption in Fumed Silica and Silane Chains

Fumed silica production via flame hydrolysis of SiCl₄ is expanding at 5.85% CAGR to 2035, riding on EV-driven green-tire formulations and high-performance construction sealants. Asia-Pacific holds roughly 45% of fumed silica revenue, with China dominating capacity and large integrated players controlling both SiCl₄ and downstream silicas. Plant expansions in Michigan, South Carolina, Japan, and South Korea illustrate a deliberate tilt toward regional self-sufficiency in the silicon tetrachloride market, ensuring secure feedstock for critical industries and shielding margins from freight volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasingly stringent chlorine-emission regulations (e.g., PRC greater than or equal to 98.5 % recycle rule) | -0.80% | China (primary), with spillover to ASEAN and India as domestic polysilicon capacity scales | Short term (≤ 2 years) |

| High logistics costs for ISO-tank transport of 6N-9N grades | -0.50% | Global, particularly cross-border shipments (China→North America/Europe; ASEAN→US) | Medium term (2-4 years) |

| Supply-chain exposure to silicon-metal price volatility | -0.60% | APAC core (China 90% of global silicon metal capacity), cascading to all SiCl4 derivative markets globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasingly Stringent Chlorine-Emission Regulations

China’s T/CCSAS 052-2025 standard requires more than or equal to 98.5% chlorosilane recycling, forcing legacy polysilicon lines to invest tens of millions of dollars in distillation and scrubbing upgrades or exit the market. Parallel ESG (Environmental, Social, and Governance) frameworks emerging in India and the European Union further tighten emission ceilings and carbon accounting, effectively raising the cost floor for small or technologically outdated producers. Vertically integrated majors already operating more than 99% recycling enjoy a compliance cost advantage, reinforcing consolidation trends in the silicon tetrachloride market.

High Logistics Costs for ISO-Tank Transport of 6N-9N Grades

Ultra-high-purity SiCl₄ must ship in specially cleaned stainless-steel ISO tanks, and each round-trip cycle includes rigorous residual testing, cleaning, and certification that add 15-25% to baseline freight rates. Cross-border movements from Asia to North America can lift delivered costs by 8-12% versus domestic supply, eroding supplier margins and incentivizing regional production hubs. On-site generation strategies adopted by gas majors bypass transport altogether, tightening merchant logistics capacity and compelling smaller buyers to commit to long-term offtake agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Electronic Grade Commands Premium as Purity Arms Race Intensifies

Electronic Grade held a commanding 47.13% of the silicon tetrachloride market share in 2025 and is projected to grow at a 4.61% CAGR through 2031. The quest for 3 nm logic, 3D DRAM, and 11-nines polysilicon is propelling investment in multi-stage distillation columns, trace-boron removal, and closed-loop recovery systems. Consequently, the historical price gap between electronic and technical grades is narrowing, especially as China’s recycle mandates press even solar-grade producers to adopt higher-purity processes. Tokuyama, Wacker, and Hemlock Semiconductor now bundle SiCl₄, silane, and hyper-pure polysilicon in integrated offerings, reinforcing switching costs for downstream fabs.

Technical Grade, while still indispensable to solar PV, faces margin pressure from overcapacity; utilization rates dipped to 33-40% in early 2025, and spot polysilicon prices crashed more than 50% year-over-year, squeezing cash costs industry-wide. Reagent Grade remains a niche for laboratories and specialty synthesis, with volumes and pricing largely insulated from solar market swings. Across all grades, the silicon tetrachloride market size for electronic-grade material is expected to outpace aggregate growth, illustrating the enduring benefit of purity-driven differentiation.

By Application: Optical-Fiber Preforms Surge on 5G and Data-Center Demand

Electronics & Semiconductors dominated applications with 35.22% share in 2025, yet Optical-Fiber Preforms is the fastest-growing use case at 4.95% CAGR to 2031, reflecting telecom operators’ upgrade cycles. Every preform fabrication route taps SiCl₄ as the preferred silica precursor, and higher throughput from VAD and OVD lines elevates absolute consumption even as conversion efficiencies improve. PCVD’s flawless precursor utilization shifts the focus from volume to purity, driving sellers to guarantee 6N-7N standards consistently and opening premium micro-niches within the broader silicon tetrachloride market.

Chemical Intermediates, such as fumed silica and silane coupling agents, provide a steady demand floor linked to automotive EV growth and green-construction adoption. Meanwhile, Electronics and Semiconductors bifurcate into low-purity bulk CVD needs and minuscule but lucrative 9N demands for advanced wafer nodes. Smaller segments, including specialty coatings and elastomers, benefit from product innovation but do not materially sway total volume trajectories.

By End-Use Industry: Telecommunications Outpaces Electronics as Fiber Appetite Accelerates

Electronics captured 38.45% of the silicon tetrachloride market share in 2025; however, Telecommunications is predicted to log the highest 4.89% CAGR through 2031. Massive fiber plant expansions in China, India, and the United States, paired with submarine-cable upgrades, amplify VAD and OVD line capacity utilization and thereby SiCl₄ pull. Integrated fiber producers increasingly co-locate SiCl₄ distillation units to minimize logistics overhead and meet quick-turn demand, a trend that cements their bargaining power.

Energy (Solar) demand eases as granular FBR technology spreads and per-watt polysilicon intensity falls, but the segment remains large enough to anchor baseline consumption. Automotive and construction users of fumed silica, organofunctional silanes, and specialty sealants show consistent growth aligned with electrification and infrastructure spending packages worldwide, supporting a diversified silicon tetrachloride market demand portfolio.

Geography Analysis

Asia-Pacific retained 57.45% of global share in 2025 and is forecast to expand at a 4.66% CAGR during the forecast period (2026-2031), driven by China’s dominance in polysilicon, optical-fiber preforms, and specialty silica. Capacity rationalization in China shifted the supply curve upward, allowing well-capitalized leaders to capture spread while older assets shuttered. Japan and South Korea are bolstering extreme-purity output, and Malaysia’s hydropower-backed semiconductor-grade venture positions ASEAN as an important redundancy node for the silicon tetrachloride market.

North America is re-emerging as a strategic production base. The CHIPS Act funding for Hemlock Semiconductor and REC Silicon’s Moses Lake restart underscores policy-driven reshoring of hyper-pure materials. Specialty-gas majors are layering on regional on-site generation plants to slash ISO-tank logistics costs. Europe’s high electricity tariffs curb the economics of polysilicon but not of value-added electronic-grade SiCl₄, prompting investments concentrated around fab clusters in Germany and Ireland.

The Middle East debuts with Oman’s 100 kiloton polysilicon facility using low-cost solar and wind power, creating anchor demand for 300-400 kilotons of SiCl₄ annually once steady-state operations begin. Africa and South America remain import-dependent, accounting for a minimal share but offering incremental volume for suppliers seeking geographic diversification in the silicon tetrachloride market.

Competitive Landscape

The Silicon Tetrachloride market is moderately concentrated. Patent race dynamics favor incumbents with decades of process know-how; yet, open-source process intensification data circulating in academic literature lowers knowledge barriers for fast followers. Environmental regulations that enforce greater than or equal to 98.5% recycling blunt low-tech competitive strategies and align sustainability with profitability, a landscape in which compliant integrated giants secure long-term supply contracts with solar and semiconductor heavyweights.

Silicon Tetrachloride Industry Leaders

Wacker Chemie AG

Tokuyama Corporation

OCI Company Ltd.

Evonik Industries AG

Linde plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: South Korean chemical manufacturer OCI Holdings announced that its Malaysian subsidiary, OCI TerraSus, secured a USD 125 million investment from the International Finance Corp to build and operate a polysilicon factory. This advancement in polysilicon production can drive up the demand for silicon tetrachloride, which is pivotal as an intermediate in polysilicon manufacturing.

- January 2026: United Solar Polysilicon (FZC) SPC secured financing from IFC to establish a greenfield polysilicon plant in Oman’s Sohar Freezone. This advancement in polysilicon production can drive up the demand for silicon tetrachloride.

Global Silicon Tetrachloride Market Report Scope

Silicon tetrachloride is a colorless, highly volatile, and corrosive fuming liquid with a pungent odor, used primarily to produce high-purity silicon, optical fibers, and silica-based materials. It reacts violently with water to produce hydrochloric acid. It is essential in the semiconductor industry for etching and chemical vapor deposition.

The silicon tetrachloride market is segmented by grade, application, end-use industry, and geography. By grade, the market is segmented into electronic grade, technical grade, and reagent grade. By application, the market is segmented into electronics and semiconductor, optical fibre preforms, chemical intermediates, and other applications (silicon rubber, etc.). By end-use industry, the market is segmented into electronics, telecommunications, energy (solar), and other end-user industries (aerospace, pharmaceuticals, etc.). The report also covers the market size and forecasts for silicon tetrachloride in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Electronic Grade |

| Technical Grade |

| Reagent Grade |

| Electronics and Semiconductors |

| Optical Fibre Preforms |

| Chemical Intermediates |

| Other Applications (Silicon Rubber, etc.) |

| Electronics |

| Telecommunications |

| Energy (Solar) |

| Other End-user Industries (Aerospace, Pharmaceuticals, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Electronic Grade | |

| Technical Grade | ||

| Reagent Grade | ||

| By Application | Electronics and Semiconductors | |

| Optical Fibre Preforms | ||

| Chemical Intermediates | ||

| Other Applications (Silicon Rubber, etc.) | ||

| By End-Use Industry | Electronics | |

| Telecommunications | ||

| Energy (Solar) | ||

| Other End-user Industries (Aerospace, Pharmaceuticals, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for silicon tetrachloride be by 2031?

The silicon tetrachloride market size is projected to reach USD 3.45 billion by 2031, growing at a 4.12% CAGR from 2026.

Which segment grows fastest over 2026-2031?

Optical-Fiber Preforms top the growth chart with a 4.95% CAGR, outpacing electronics and solar applications.

Why is electronic-grade SiCl₄ gaining share?

Advanced semiconductor and telecom applications require 7N-9N purity, pushing electronic-grade material to 47.13% market share in 2025 and lifting it at a 4.61% CAGR.

Which region leads consumption today?

Asia-Pacific dominates, holding 57.45% share in 2025, thanks to China’s polysilicon and optical-fiber preform clusters and is set for the highest regional CAGR of 4.66%.

Page last updated on: