Silicone Coating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.43 Billion |

| Market Size (2031) | USD 9.27 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

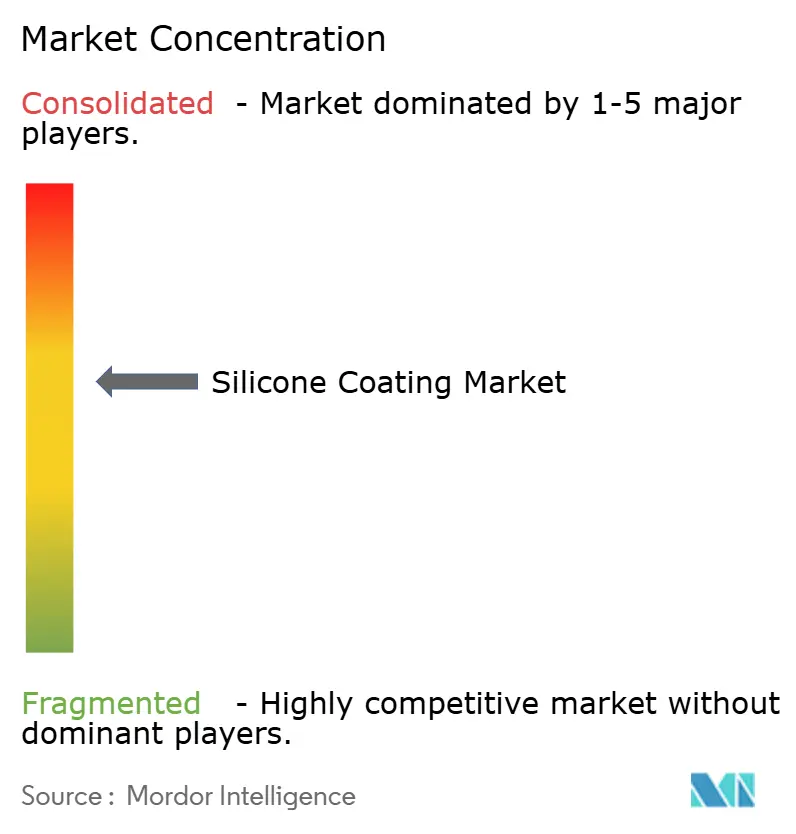

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone Coating Market Analysis by Mordor Intelligence

The Silicone Coating Market size was valued at USD 7.11 billion in 2025 and estimated to grow from USD 7.43 billion in 2026 to reach USD 9.27 billion by 2031, at a CAGR of 4.52% during the forecast period (2026-2031). Ongoing energy-efficiency mandates in commercial roofing, accelerating electronics miniaturization, and the proven thermal stability of silicone polymers continue to move the Silicone coatings market from niche status toward a broadly adopted protective-materials segment. Structural durability, UV resistance, and moisture impermeability position silicone coatings as preferred solutions in climates that impose high thermal shock and solar exposure. Asia-Pacific’s construction boom and its electronics manufacturing dominance anchor global demand, while policy shifts that phase out PFAS-based chemistries further tilt customer selection toward silicone systems. On the supply side, producers with vertically integrated siloxane chains and strong application-engineering support capture higher margins even when feedstock prices fluctuate.

Key Report Takeaways

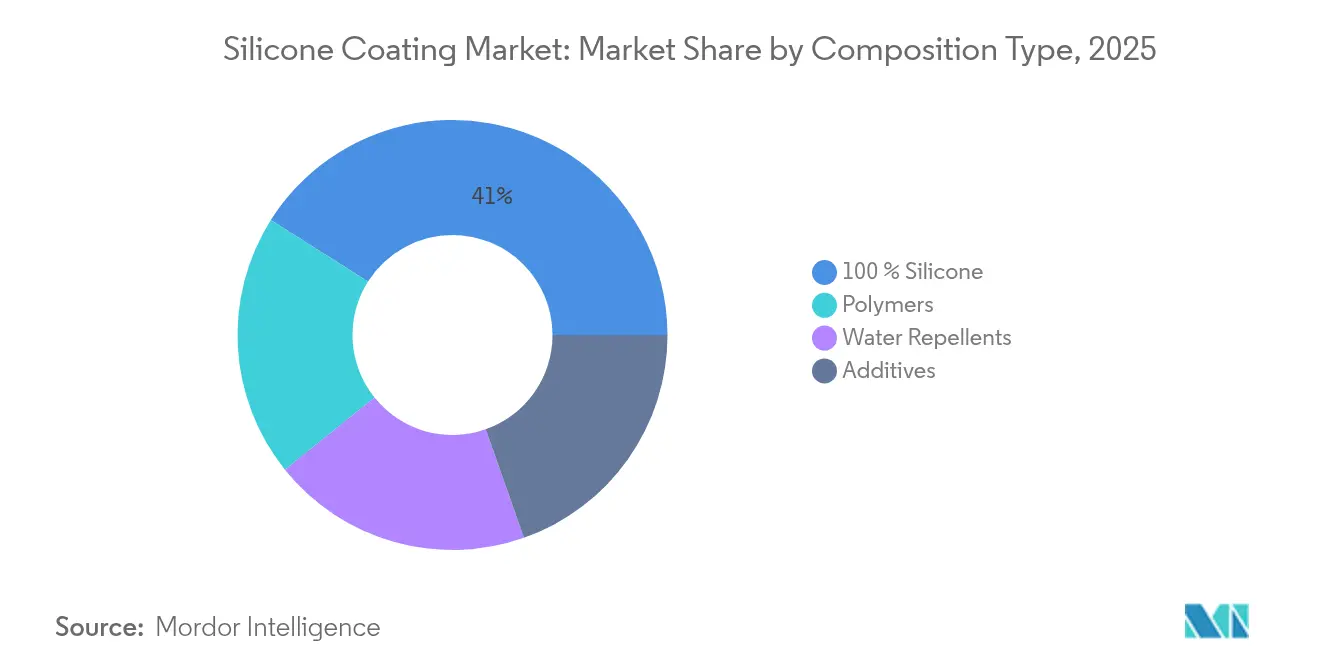

- By composition type, 100% silicone elastomeric coatings held 41.02% of the Silicone coatings market share in 2025; water-repellent systems are forecast to deliver a 5.28% CAGR to 2031.

- By technology, solvent-less platforms led with a 37.85% revenue share in 2025, while UV-cured chemistries are poised for the fastest 5.33% CAGR between 2026 and 2031.

- By substrate, metal surfaces commanded 54.62% of the overall revenue in 2025; concrete and masonry applications are projected to expand at 5.25% CAGR through 2031.

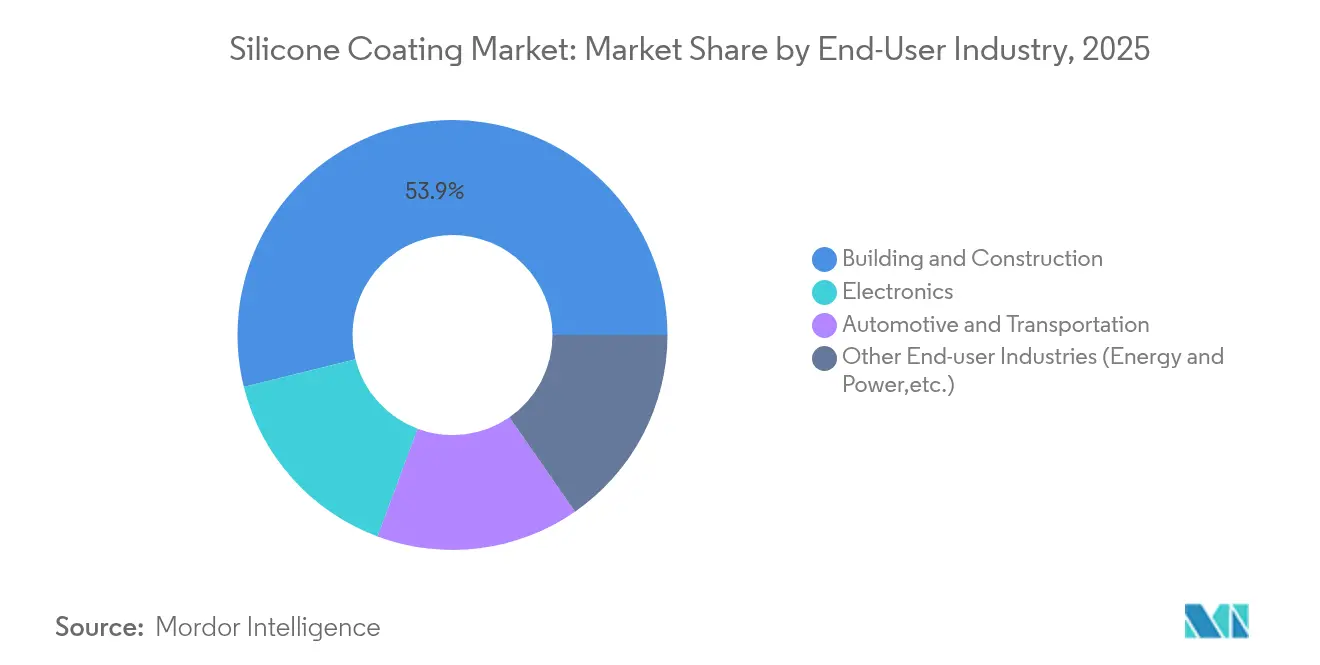

- By end-user industry, building and construction dominated with a 53.88% revenue share in 2025, whereas electronics is expected to register the highest 5.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicone Coating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cool-roof refurbishments for energy-efficient buildings | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Growing demand from building and construction industry | +1.0% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Rapid adoption in consumer and industrial electronics conformal coatings | +0.8% | Global, led by APAC electronics hubs | Short term (≤ 2 years) |

| Increasing demand for silicone coatings from the automotive industry | +0.7% | Global, with EV concentration in China, EU, North America | Medium term (2-4 years) |

| Urban-heat-island mitigation programs driving reflective silicone roofs | +0.5% | Urban centers globally, priority in Asia-Pacific megacities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Cool-Roof Refurbishments for Energy-Efficient Buildings

California’s Title 24 code enforces a minimum aged solar reflectance of 0.63 and thermal emittance of 0.75 on low-slope commercial roofs, converting regulatory language into immediate demand for high-reflectance silicone membranes[1]Technical Committee, “Roof Rating Specifications,” Cool Roof Rating Council, coolroofs.org. Building owners frequently choose silicone restoration rather than full reroofing, trimming capital expenditure by as much as 40% while extending service life. Field studies from the California Energy Commission indicate that cool roofs cut annual energy use by up to 15% in hot climates[2]Research Division, “Tile 24 Compliance Guide,” California Energy Commission, energy.ca.gov. Similar performance-based codes now appear across Europe and fast-growing Asian megacities, embedding silicone solutions in long-range retrofit budgets. As electricity tariffs continue to rise, the payback period for silicone cool-roof systems shortens, reinforcing a durable demand driver in the Silicone coatings market.

Growing Demand from the Building and Construction Industry

The construction sector is shifting from reactive repairs toward proactive envelope protection, and silicone chemistry sits at that strategic pivot point. Moisture ingress remains the dominant degradation mechanism in concrete, yet vapor-permeable silicone barriers extend structural life by two to three decades while allowing substrates to breathe. Nanotitanium-modified silane coatings tested on long-span bridges have demonstrated potential lifetimes exceeding 70 years. Warranty frameworks in public-infrastructure procurement increasingly specify minimum service intervals that silicone technology uniquely satisfies, anchoring the long-term influence of this driver. Emerging government incentives for “whole-life-carbon” accounting further lift specification rates for high-durability silicone membranes, amplifying growth momentum in the Silicone coatings market.

Rapid Adoption in Consumer and Industrial Electronics Conformal Coatings

Component miniaturization raises power densities and moisture-sensitivity, prompting electronics suppliers to migrate toward PFAS-free silicone conformal coatings with superior dielectric performance. Momentive’s thermally conductive encapsulants operate reliably from −50 °C to +200 °C, meeting the envelope required for 5G base-station modules. Atomic-layer-deposition research now proves uniform silicone coverage inside 60:1 aspect-ratio vias without impairing signal integrity. Global roll-outs of IoT sensors add billions of boards that demand corrosion-resistant, low-modulus coatings. Consequently, electronics OEMs view silicone coatings less as optional insurance and more as an enabling design element, reinforcing a robust short-term pull on the Silicone coatings market.

Increasing Demand from the Automotive Industry

The shift from internal-combustion engines to battery-electric platforms multiplies thermal-management challenges, elevating silicone interface materials from ancillary to critical components. Dow’s DOWSIL TC-3080 gel delivers uniform heat spread at pack level while allowing automated dispensing speeds required for gigafactory scale. Parker’s CoolTherm systems combine moisture sealing with 2 W/m·K conductivity, protecting control boards from dust and vibration. Original equipment manufacturers increasingly bake coating specifications into advanced product quality planning, pushing silicone suppliers toward IATF 16949 accreditation for process rigor. Advanced driver-assistance and high-voltage inverters further widen the scope of silicone use, translating automotive electrification trends into medium-term growth for the Silicone coatings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices (siloxanes, fumed silica) | -0.9% | Global, with concentration in silicone manufacturing regions | Short term (≤ 2 years) |

| Supply-chain concentration of silane monomer feedstocks | -0.6% | Global, with vulnerability in APAC supply chains | Medium term (2-4 years) |

| Stricter indoor-air fire-safety codes limiting interior silicone use | -0.4% | North America & EU regulatory jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices for Siloxanes and Fumed Silica

Silicon-metal price swings cascade through to siloxane and fumed-silica intermediates, undermining cost predictability for coating formulators. Concentrated smelting capacity in energy-intensive provinces means that local power curtailments or environmental shutdowns in China can spike global raw-material indices within weeks. Coating producers respond through supply-contract hedging and greater recycle content, with emerging depolymerization technologies converting post-consumer silicone back into monomeric feedstock. Capital-intensive backward integration shelters margins yet favors only a handful of multinational players. Short-term volatility therefore translates into cautious inventory strategies among downstream users, mildly dampening expansion in the Silicone coatings market.

Supply-Chain Concentration of Silane Monomer Feedstocks

High-purity silane plants operate in fewer than ten global locations, leaving the value chain exposed to single-point disruptions. Specialty silanes tune adhesion and water repellency, and qualification cycles for replacements can exceed one year, discouraging rapid supplier substitution. Capacity expansions underway in the United States and the Middle East will not come online before 2026, prolonging supply-tight conditions. Construction firms with liquidated-damages clauses incur cost overruns when key silanes are delayed, eroding confidence in just-in-time procurement. The resulting risk premium tempers otherwise robust growth in the Silicone coatings market during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Composition Type: Elastomeric Dominance Faces Water-Repellent Innovation

In 2025, 100% silicone grades generated 41.02% of total revenue, reflecting their unrivaled durability under severe UV and thermal cycling. These products anchor industrial-maintenance budgets in petrochemical, marine, and roofing markets where downtime costs exceed material premiums. Water-repellent chemistries, although smaller in volume, post the highest 5.28% CAGR to 2031 as architects increasingly specify breathable yet moisture-blocking façades for net-zero buildings. Advancements in super-hydrophobic silicone resins have achieved static contact angles above 160°, opening façade panels, monuments, and even solar modules to new protective paradigms.

Research pipelines now blend bio-based alkyl-polysiloxanes that retain high contact angles while cutting carbon intensity, answering sustainability tenders in public infrastructure. Concurrently, additive packages containing silsesquioxanes and nano-zirconia enable abrasion resistance without raising VOC levels, a benefit in emission-regulated spray booths. Competitive differentiation therefore migrates from basic polymer conversion to proprietary surface-energy control, locking in customer loyalty and supporting pricing power across the Silicone coatings market.

By Technology: Solvent-less Leadership Challenged by UV-Cured Innovation

Solvent-less systems captured 37.85% revenue in 2025, propelled by environmental regulations that cap VOC content in architectural and OEM facilities. Absence of flammable carrier solvents also simplifies plant-safety audits, lowering insurance premiums for applicators. Yet UV-cured platforms, forecast to grow at 5.33% CAGR, are rapidly closing the gap as production lines chase sub-minute tack-free times and lower energy footprints. Breakthroughs in near-infrared photoinitiators achieve cure depths exceeding 25 mm, unlocking structural adhesives and thick-section potting that previously defaulted to thermal bakeouts.

Water-borne hybrids edge into schools and hospitals where indoor-air regulations restrict solvent exposure, while radiation-cured epoxies protect mini-LED backplanes against flux-solder processing. Collectively, these technology options expand the addressable footprint of the Silicone coatings market, supplying specifiers with an increasingly granular toolkit aligned to both throughput and sustainability metrics.

By Substrate: Metal Applications Drive Volume while Concrete Gains Momentum

Metal substrates ruled 2025 sales with 54.62%, anchored by process-plant piping, offshore structures, and locomotive exhaust systems that demand thermal shock tolerance and corrosion inhibition. Electrical utilities also coat aluminum bus-bars to damp corona discharge in humid climates. Concrete-and-masonry coatings, however, will post a 5.25% CAGR as megacity transit tunnels, bridges, and parking decks seek breathable waterproofing. Bifunctional siloxane primers now couple chemically to calcium silicate hydrate, raising freeze-thaw durability and slashing algae colonization by over 70%.

Plastics and composites represent niche but strategic deployments in aerospace fairings and wind-turbine blades, where low surface energy combats ice accretion. For glass façades, one-component silicone clear coats deliver self-cleaning performance and curb particulate adhesion—attributes valued in dense urban corridors. The diversified substrate landscape demonstrates that formulation science, rather than raw volume, underpins value creation in the Silicone coatings market.

By End-User Industry: Construction Stability Meets Electronics Acceleration

Building and construction retained a stalwart 53.88% revenue share in 2025, its dominance secured by roof restoration, façade hydrophobization, and joint sealing. Government retrofit subsidies funnel expenditure into reflective coatings that both curb peak-load energy demand and stretch maintenance cycles beyond 20 years. Electronics, benefiting from a 5.55% CAGR through 2031, embraces silicone’s dual role as dielectric barrier and thermal spreader. Conformal coatings featuring low-modulus organosilicon networks protect high-density boards against capillary condensation without inducing solder-joint stress.

In automotive, lightweight battery enclosures now integrate silicone potting to offset vibration and prevent thermal runaway propagation. Power-grid assets, meanwhile, employ high-creepage-distance silicone housings that repel pollution flashovers, illustrating ecosystem cross-pollination. Collectively, these trends underscore how end-user innovation continues to re-shape opportunity contours inside the Silicone coatings market.

Geography Analysis

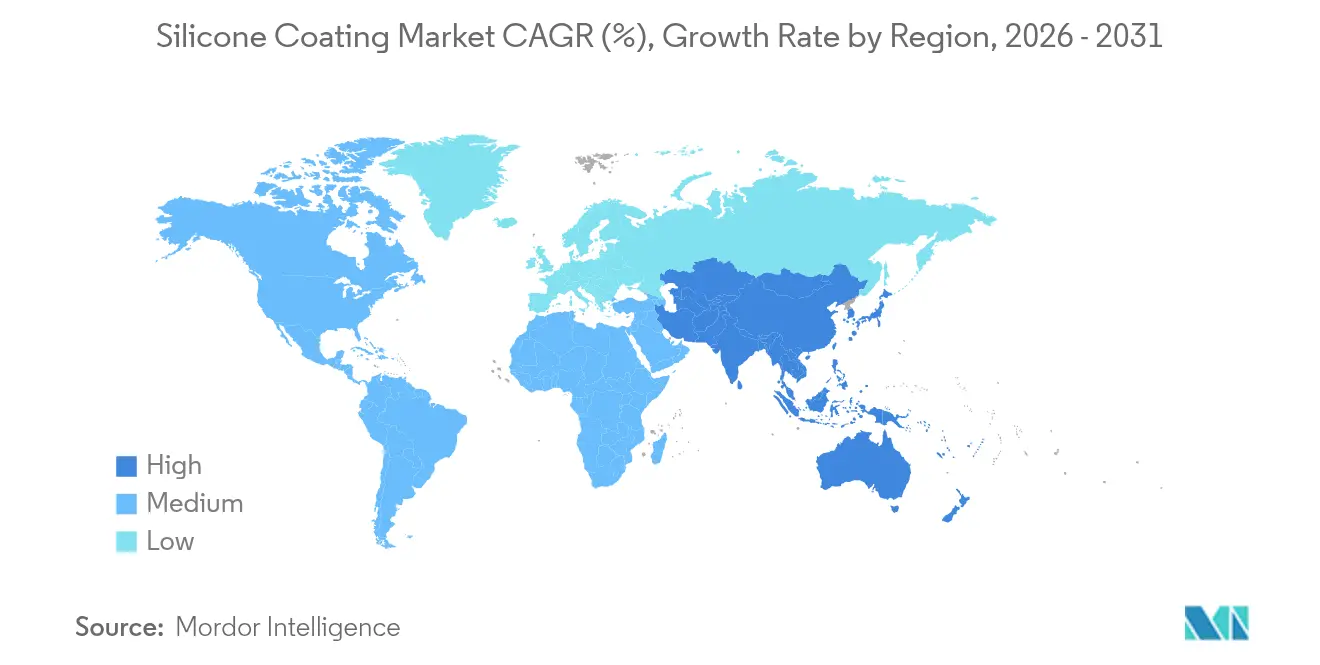

Asia-Pacific accounted for 45.70% of global revenue in 2025 and is projected to register a 4.92% CAGR to 2031, reflecting concerted infrastructure investment in China, India, and Vietnam alongside electronics manufacturing saturation in South Korea and Taiwan. Local firms increasingly channel R&D into EV thermal-management and semiconductor encapsulation, broadening regional value capture beyond basic volume. Multinational producers deepen joint ventures to secure proximity to end-users and buffer logistics exposure, thereby sustaining leadership within the Silicone coatings market.

North America remains a technologically mature arena where energy codes, such as California’s Title 24, institutionalize cool-roof demand. Roofing contractors leverage silicone restoration systems to sidestep landfill disposal fees, boosting adoption in sun-belt states. In Canada, federal green-building standards elevate vapor-permeable façade coatings, while Mexico’s automotive clusters generate steady pull for thermal-interface silicones. These dynamics anchor steady value growth, even as overall unit volumes plateau.

Europe’s market pursues circular-economy goals that reward long-life, low-maintenance chemistries, positioning silicone as the default for bridge refurbishment and offshore wind monopiles. Germany and the Nordics pioneer in-process recycling of silicone liner waste, reinforcing local supply resilience. Elsewhere, Southern Europe’s renovation wave channels stimulus funds toward roof-reflective coatings to mitigate urban heat islands. Emerging economies in South America and the Middle East & Africa add incremental demand through port expansions and energy projects, though currency volatility and limited applicator expertise moderate uptake in these regions.

Competitive Landscape

The Silicone coatings market reflects moderate consolidation. Dow, WACKER, and Momentive headline the tier-one roster, each operating integrated siloxane chains, global technical-service footprints, and application labs that shorten customer adoption cycles. KCC Corporation’s 2024 acquisition of Momentive consolidates R&D assets and grants the Korean conglomerate greater access to premium automotive and semiconductor accounts.

Evonik’s 2025 reorganization of its Silica and Silanes businesses under the “Smart Effects” banner illustrates portfolio streamlining designed to focus capital on high-growth EV and medical-device coatings. Meanwhile, Siltech stakes out sustainability leadership through bio-alkyl polysiloxane additives that cut fossil-carbon input yet maintain hydrophobic performance, appealing to European eco-label schemes. Smaller regional formulators thrive in regulated niches—such as low-smoke cloister coatings specified by Japanese rail operators—by tailoring chemistries to local codes and offering rapid field-service response.

Silicone Coating Industry Leaders

Shin-Etsu Chemical Co., Ltd

Momentive

Wacker Chemie AG

Dow

Elkem ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Evonik Coating Additives has expanded its TEGO Rad range with a new silicone acrylate additive for radiation-curing coatings and inks. Offering excellent wetting, slip, and low foaming, it is suitable for inks, varnishes, and clear or pigmented wood coatings.

- June 2025: Hempel has launched Hempaguard NB, a high-performance silicone hull coating for newbuild vessels. Part of the Hempaguard range, it provides fuel savings and fouling protection during construction.

Global Silicone Coating Market Report Scope

The silicone coating market report includes:

| Polymers |

| 100 % Silicone |

| Water Repellents |

| Additives |

| Solvent-less |

| Solvent-based |

| Water-borne |

| Radiation/UV-cured |

| Metal |

| Concrete and Masonry |

| Plastics and Composites |

| Glass and Ceramics |

| Building and Construction |

| Electronics |

| Automotive and Transportation |

| Other End-user Industries (Energy and Power,etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Composition Type | Polymers | |

| 100 % Silicone | ||

| Water Repellents | ||

| Additives | ||

| By Technology | Solvent-less | |

| Solvent-based | ||

| Water-borne | ||

| Radiation/UV-cured | ||

| By Substrate | Metal | |

| Concrete and Masonry | ||

| Plastics and Composites | ||

| Glass and Ceramics | ||

| By End-user Industry | Building and Construction | |

| Electronics | ||

| Automotive and Transportation | ||

| Other End-user Industries (Energy and Power,etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Silicone Coating Market size?

The Silicone coatings market size stands at USD 7.43 billion in 2026 and is forecast to reach USD 9.27 billion by 2031.

Which end-user sector holds the largest revenue share?

Building and construction applications account for 53.88% of 2025 revenues, making them the dominant sector.

Which segment is expanding fastest by technology?

UV-cured silicone coatings lead growth with a projected 5.33% CAGR between 2026 and 2031.

Why are silicone coatings increasingly used in electronics?

Miniaturization, PFAS phase-outs, and high thermal-management requirements make silicone materials the preferred conformal-coating choice.

Page last updated on: