Pentachlorophenol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

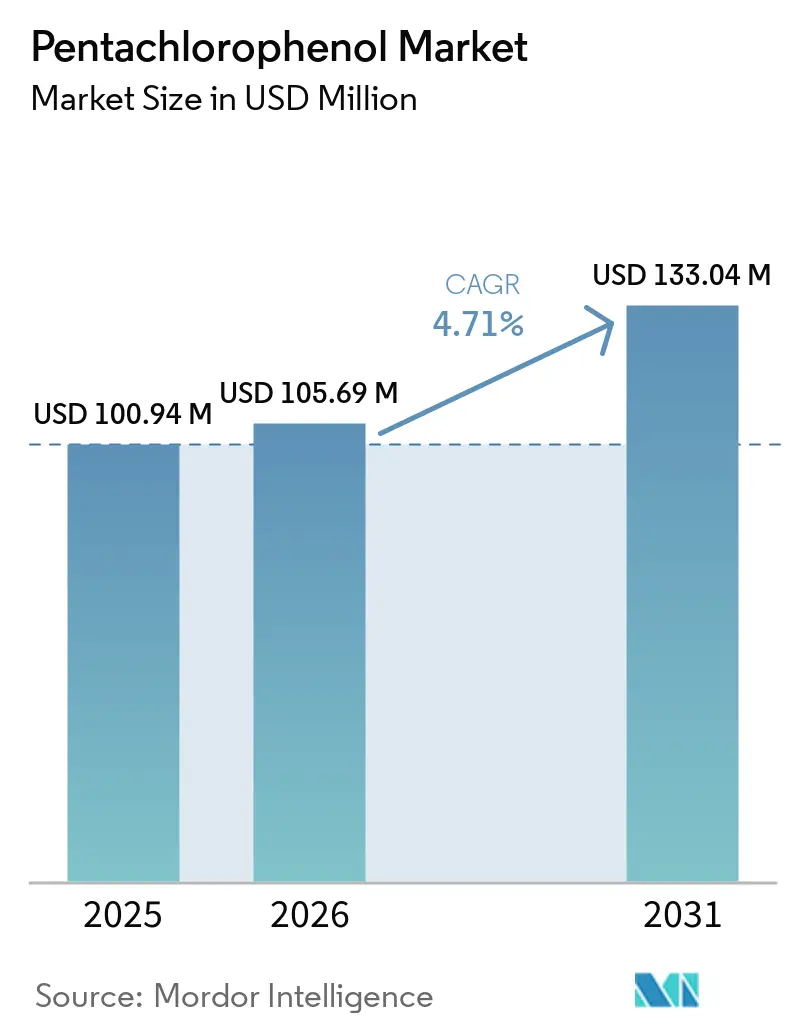

| Market Size (2026) | USD 105.69 Million |

| Market Size (2031) | USD 133.04 Million |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pentachlorophenol Market Analysis by Mordor Intelligence

The Pentachlorophenol Market size is projected to expand from USD 100.94 million in 2025 and USD 105.69 million in 2026 to USD 133.04 million by 2031, registering a CAGR of 4.71% between 2026 to 2031. Pentachlorophenol remains deeply entrenched in legacy wood-treatment infrastructure, especially in utility poles and heavy timber, yet a phased regulatory sunset in the United States and rising global ESG scrutiny are reshaping demand patterns. Capital-intensive infrastructure projects in emerging Asia continue to specify oil-borne preservatives because they outperform aqueous alternatives in humid or saline environments, sustaining baseline volume even as copper-based systems gain traction in developed regions. Competitive dynamics increasingly favor vertically integrated suppliers that already own solvent-recovery and waste-handling assets, allowing them to internalize disposal costs that smaller treaters cannot absorb. The interplay of compliance deadlines, infrastructure roll-outs, and substitution economics underpins a pentachlorophenol market that is simultaneously contracting in North America and Western Europe while expanding in South and Southeast Asia.

Key Report Takeaways

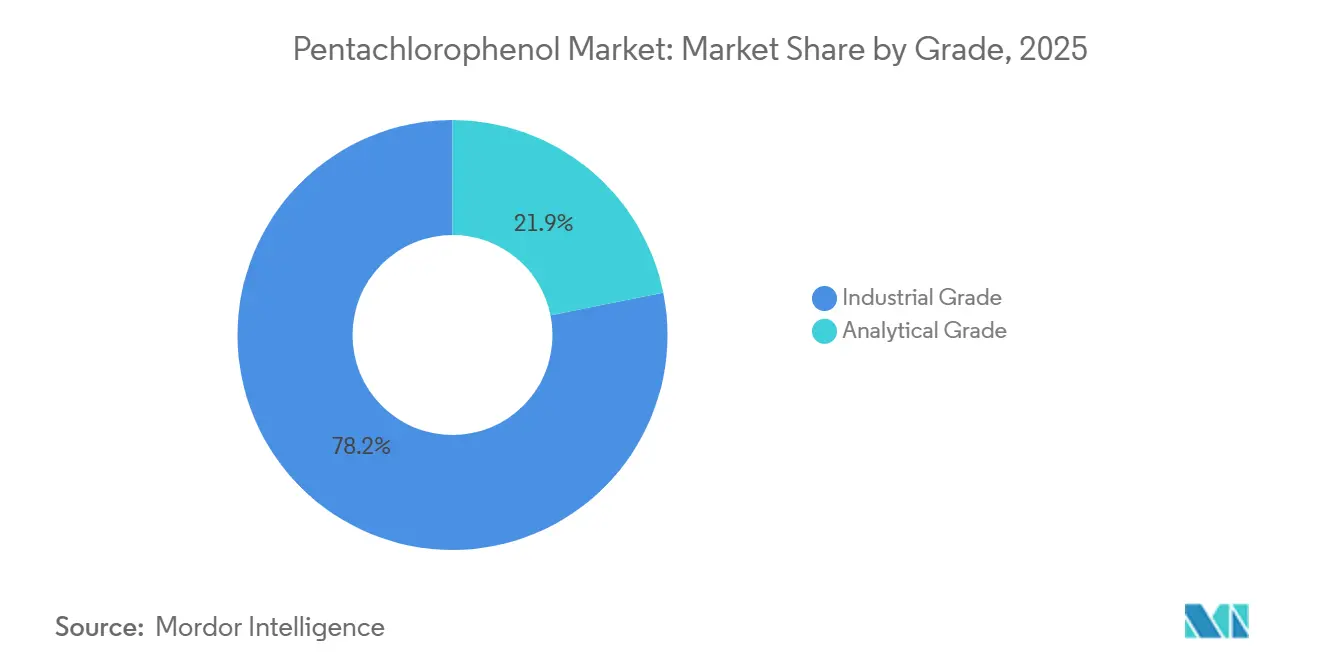

- By grade, industrial grade captured 78.15% of the pentachlorophenol market share in 2025, whereas analytical grade is forecast to expand at a 4.88% CAGR through 2031.

- By application, wood preservatives held 60.22% of the pentachlorophenol market share in 2025, while industrial biocides are projected to record the fastest 4.82% CAGR through 2031.

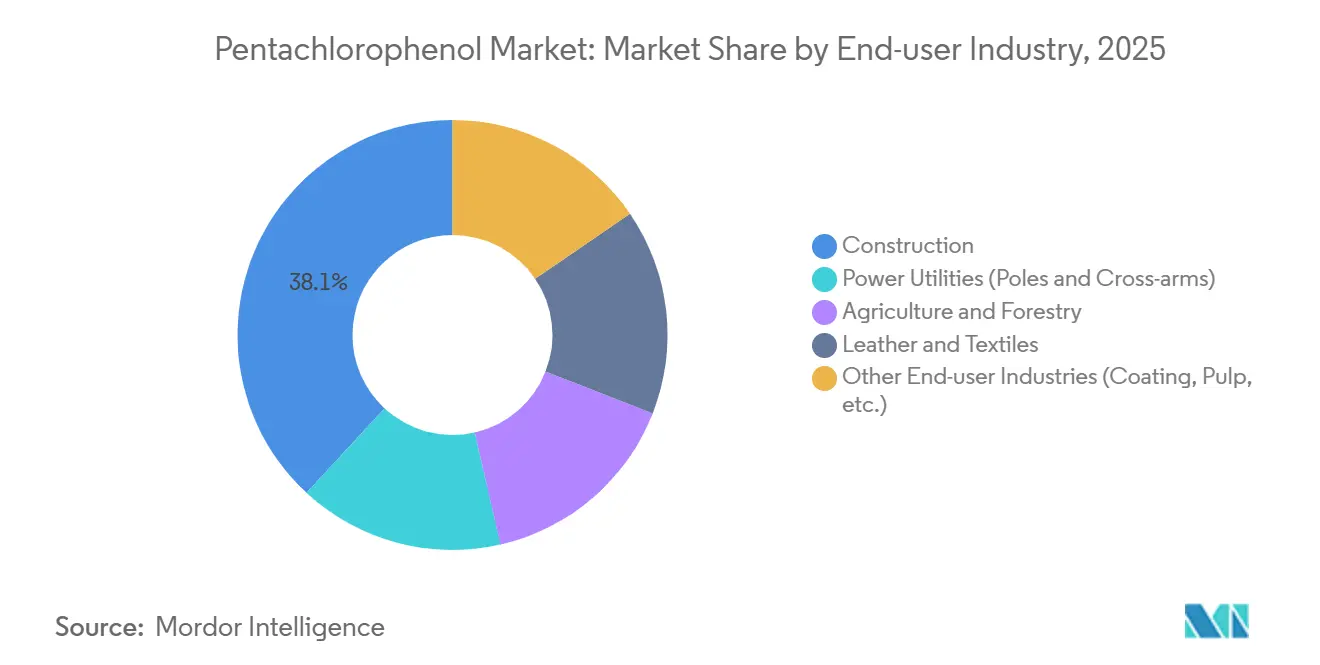

- By end-user industry, Construction accounted for 38.12% of the pentachlorophenol market share in 2025 and is expected to advance at a 5.23% CAGR through 2031.

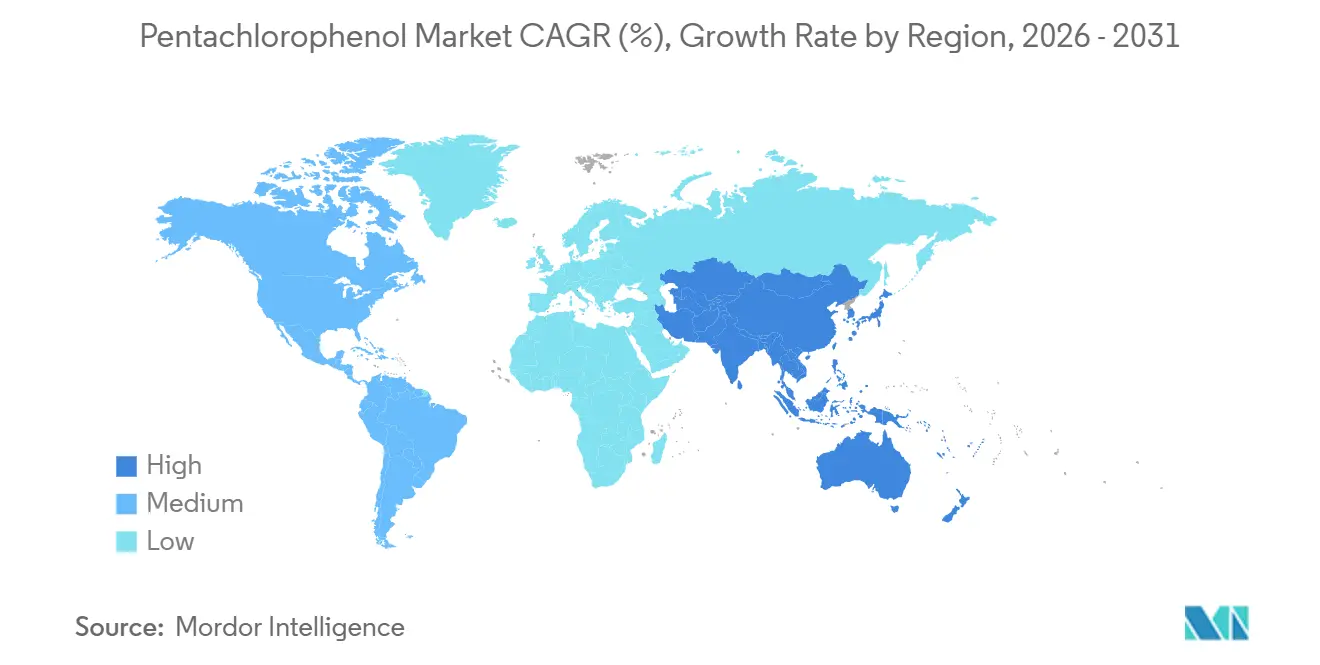

- By geography, Asia-Pacific commanded 39.22% of the pentachlorophenol market share in 2025 and is advancing at a 5.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pentachlorophenol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding infrastructure in emerging economies | +1.2% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Continued use in industrial pesticides and herbicides | +0.8% | Global, with concentration in Asia-Pacific and South America | Long term (≥ 4 years) |

| Creosote withdrawal driving substitution | +0.6% | Europe and United Kingdom | Short term (≤ 2 years) |

| CLT structural panels requiring deep-penetration preservatives | +0.7% | North America and Europe | Medium term (2-4 years) |

| Rural broadband roll-outs using timber masts | +0.5% | Asia-Pacific (India, Philippines, Indonesia) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Infrastructure in Emerging Economies

Hundreds of road, rail, and utility mega-projects in Asia are unlocking sustained demand for deep-penetration preservatives that outperform water-borne chemistries in termite-prone climates. China’s 14th Five-Year Plan channels USD 4.2 trillion into transportation corridors and industrial parks, a pipeline that continues to specify industrial-grade pentachlorophenol where environmental enforcement remains patchy. India’s USD 3.4 billion strategic railway build-out near its northern border similarly leans on treated sleepers that resist fungal decay under monsoon exposure. Across ASEAN, prefab timber housing valued at USD 36.6 billion in 2024 relies on long-life preservatives to satisfy 50-year structural warranties in humid coastal markets. Because copper-naphthenate systems cost about 50% more on a delivered basis, price-sensitive contractors continue to order pentachlorophenol, propping up pentachlorophenol market demand even as regulatory sunsets loom in the West.

Continued Use in Industrial Pesticides and Herbicides

Industrial biocides remain a niche but resilient outlet for pentachlorophenol, especially in high-temperature cooling systems at power plants and refineries where isothiazolinone alternatives break down rapidly. Leather tanneries in South America and parts of Southeast Asia also employ the chemical to prevent microbial attack on hides during storage when chromium-free processes are unavailable. Although global agricultural volumes have fallen sharply post-2024, jurisdictions outside the Stockholm Convention still allow pentachlorophenol herbicide formulations for woody weed control. The segment anchors a predictable if modest revenue stream that tempers overall market volatility.

Creosote Withdrawal Driving Substitution

The United Kingdom’s February 2025 sunset for creosote and the European Union’s consumer-use ban are diverting orders toward pentachlorophenol for treaters that already own compatible oil-borne cylinders. European rail operators must replace roughly 40 million sleepers in secondary lines where concrete alternatives remain uneconomic, and pentachlorophenol offers a familiar drop-in solution until copper naphthenate or DCOI retrofits are completed. Viance has positioned its DCOI technology as a future-proof successor, yet adoption lags because pressure-treatment cycles and solvent-recovery equipment require recalibration. The substitution window boosts short-term pentachlorophenol market revenue but is expected to taper beyond 2027.

Rural Broadband Roll-Outs Using Timber Masts

Government-sponsored broadband drives utility-pole demand in rural India, the Philippines, and Indonesia, where timber poles can be installed at one-third the cost of steel. India’s 250,000-village BharatNet expansion alone ordered an estimated 2 million treated poles in 2025, directly uplifting the pentachlorophenol market size tied to construction end-users[1]Department of Telecommunications India, “BharatNet Phase-II Update,” dot.gov.in. Coastal deployment areas with salt spray and monsoonal moisture require deep-penetration preservatives to guarantee 40-year service life, reinforcing the chemical’s value proposition. Yet regulators in California and other U.S. states are drafting 2028 bans, underscoring a bifurcating demand profile: robust in emerging Asia, shrinking in advanced economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of eco-friendly alternatives | -0.9% | North America and Europe | Medium term (2-4 years) |

| ESG-driven insurer and investor restrictions on utilities | -0.6% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Rising disposal costs for hazardous treated wood | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Eco-Friendly Alternatives

Copper azole, alkaline copper quaternary, micronized copper azole, and DCOI have captured more than 70% of North American residential-lumber demand since the 2024 EPA manufacturing cutoff. Silicate-based systems such as SiooX, acquired by Russwood in 2025, mineralize the wood surface and generate no hazardous waste, aligning with LEED credits and lowering life-cycle costs once tracking fees are considered. As large Chinese formulators scale copper naphthenate, price premiums shrink, accelerating substitution. This eco-pivot slices into the pentachlorophenol market share in regions where regulations and green-finance criteria converge.

Rising Disposal Costs for Hazardous Treated Wood

Hazardous-waste landfills charge an average of USD 292 per ton to accept pentachlorophenol-treated wood, almost five times the cost for non-hazardous alternatives. California’s Alternative Management Standards offer a partial reprieve, yet compliance audits cost up to USD 150,000 per year for a mid-size treater[2]CalRecycle, “Alternative Management Standards for Treated Wood Waste,” calrecycle.ca.gov. Across the EU, waste containing more than 5 ppm pentachlorophenol must be incinerated, adding EUR 250-400 per ton (USD 270-430) to life-cycle cost. The economics push smaller operators to exit, reinforcing consolidation and trimming long-term pentachlorophenol market demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Industrial Formulations Anchor Utility and Heavy Timber

Industrial grade generated 78.15% of 2025 revenue, underscoring its role in high-load applications like utility poles and marine pilings that demand 6-12 lb/ft³ retention rates. The pentachlorophenol segment’s advantage stems from legacy pressure cylinders and solvent-recovery loops that would require USD 1-3 million in retrofits to handle aqueous copper systems. Analytical grade is rising at a 4.88% CAGR through 2031 as laboratories, regulators, and consultants expand site assessments using EPA Method 8540 kits and sub-ppm detection technologies. Certified reference materials from Merck KGaA and Biosynth support this compliance boom, positioning the sub-segment for steady growth through 2031.

Despite EPA phase-out deadlines, emerging Asia keeps ordering industrial grade for infrastructure corridors, cushioning global volume declines. However, price parity between copper naphthenate and industrial pentachlorophenol is approaching in India and China, pressuring margins. Analytical grade benefits from that very regulatory churn; as phase-outs bite, demand for monitoring reagents intensifies, expanding its pentachlorophenol industry share within total revenue.

By Application: Wood Preservatives Dominate Amid Substitution Pressures

Wood preservatives held 60.22% of 2025 revenue, reflecting pentachlorophenol’s unmatched penetration and leach resistance in utility poles, railway sleepers, and marine timbers. The EPA’s February 2027 use-up cliff has sparked a near-term substitution surge in North America, yet replacement sleepers across Europe’s secondary rail lines sustain interim demand. Cross-laminated timber projects further buoy sales where solvent depth is critical. Industrial biocides, the fastest-growing slice at a 4.82% CAGR through 2031, satisfy cost-sensitive cooling-tower operators in warm, saline geographies. Pesticides and herbicides continue only in regulatory gray zones but shrink annually as more countries adopt Stockholm Convention standards.

Longer term, copper-based and silicate-based systems are eroding pentachlorophenol market share, particularly in residential and light-commercial sectors. Yet pockets of entrenched industrial demand and the sunk-cost inertia of pressure-treating infrastructure ensure wood preservatives remain the largest application through 2031, albeit at a diminished percentage of the overall market size.

By End-user Industry: Construction Leads Share and Growth

Construction delivered 38.12% of 2025 revenue and is forecast to climb at a 5.23% CAGR tgrough 2031, fueled by rural broadband roll-outs and mass-timber architecture. India’s BharatNet, for example, specified 2 million treated poles in 2025, propelling local pentachlorophenol market demand. Power utilities face steeper substitution headwinds as insurers and state commissions mandate copper naphthenate or composite alternatives by 2028. Agriculture and forestry sustain niche demand in South America for vineyard posts, while leather and textiles remain marginal yet persistent where chromium-free tanning agents are scarce.

The pentachlorophenol market size tied to construction is poised to plateau around 2028 if ISO 21887 adopts depth-of-penetration thresholds disfavoring solvent-borne chemistries. Conversely, a lenient standard could lock the preservative into CLT supply chains for another decade, sustaining its largest end-user share.

Geography Analysis

Asia-Pacific accounted for 39.22% of 2025 revenue and is advancing at a 5.16% CAGR through 2031, underpinned by China’s USD 4.2 trillion transport build-out and India’s strategic rail and broadband projects. Treaters in Vietnam, Indonesia, and the Philippines benefit from abundant local timber and lower compliance costs, locking in pentachlorophenol’s price edge over copper azole. North America is in structural decline; the EPA manufacturing ban, effective 2024, halts new supply, and only stockpiles may be used until February 2027. California’s Public Utilities Commission is set to ban new pentachlorophenol poles by 2028, accelerating contraction.

Europe exhibits a mixed profile: creosote withdrawal temporarily lifts demand as treaters switch to pentachlorophenol while upgrading for copper naphthenate, but REACH limits of 5 ppm in consumer articles cap long-term growth. South America and the Middle-East and Africa offer fragmented yet resilient demand thanks to lax enforcement and cost sensitivity; however, rising green-finance criteria may curtail exports of treated wood, narrowing the market in these regions post-2030.

Competitive Landscape

The market is moderately fragmented. Koppers commands a prominent share via vertically integrated operations, but its February 2026 idling of two U.S. plants illustrates the pressure to consolidate its footprint ahead of the 2027 use-up deadline. Viance leverages DCOI approvals to cross-sell replacement chemistries, positioning itself as a transition partner for treaters with stranded oil-borne assets. Russwood’s 2025 acquisition of SiooX signals a strategic realignment toward silicate technologies that skirt hazardous-waste liabilities. Regional specialists, notably in Southeast Asia, maintain a share through localized supply chains and lower environmental oversight, yet they face scale disadvantages as disposal and audit costs rise.

Strategic moves in 2024-2026 underscore rationalization: Culpeper Wood Preservers bought two southeastern U.S. rivals to spread compliance overhead, while Koppers shifted Australian output toward higher-margin carbon-pitch derivatives to offset falling pentachlorophenol volumes. White-space opportunities cluster in analytical-grade materials and hybrid preservative systems that marry solvent-borne depth with eco-friendly surface protection. Overall, the top five producers collectively hold roughly 58% of global revenue in 2025, indicating mid-level concentration.

Pentachlorophenol Industry Leaders

Albemarle Corporation

Santa Cruz Biotechnology Inc.

AccuStandard

KANTO KAGAKU

Viance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Koppers Inc. announced the closure of its wood-treating facilities located in Vance, Alabama, and Florence, South Carolina. The closures significantly impacted the pentachlorophenol market, as these facilities were key contributors to its supply chain.

- October 2023: Canada had phased out the use of pentachlorophenol (PCP) for wood treatment. However, Canadian electrical firms were allowed to import PCP-treated poles from the U.S. strictly for disposal purposes until October 4, 2026.

Global Pentachlorophenol Market Report Scope

Pentachlorophenol (PCP) is a highly toxic organochlorine compound primarily utilized as a heavy-duty wood preservative for utility poles and railroad ties. However, its use is heavily restricted due to significant environmental and health risks, including potential carcinogenicity.

The Pentachlorophenol Market is segmented by grade, application, end-user industry, and geography. By grade, the market is segmented into industrial grade and analytical grade. By application, the market is segmented into wood preservatives, pesticides and herbicides, leather preservation, industrial biocides, and other applications (e.g., antimicrobial agents). By end-user industry, the market is segmented into construction, power utilities (poles and cross-arms), agriculture and forestry, leather and textiles, and other end-user industries (coating, pulp, etc.). The report also covers the market size and forecasts for pentachlorophenol in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Industrial Grade |

| Analytical Grade |

| Wood Preservatives |

| Pesticides and Herbicides |

| Leather Preservation |

| Industrial Biocides |

| Other Applications (e.g., Antimicrobial Agents) |

| Construction |

| Power Utilities (Poles and Cross-arms) |

| Agriculture and Forestry |

| Leather and Textiles |

| Other End-user Industries (Coating, Pulp, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Industrial Grade | |

| Analytical Grade | ||

| By Application | Wood Preservatives | |

| Pesticides and Herbicides | ||

| Leather Preservation | ||

| Industrial Biocides | ||

| Other Applications (e.g., Antimicrobial Agents) | ||

| By End-user Industry | Construction | |

| Power Utilities (Poles and Cross-arms) | ||

| Agriculture and Forestry | ||

| Leather and Textiles | ||

| Other End-user Industries (Coating, Pulp, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the pentachlorophenol market?

The pentachlorophenol market size stands at USD 105.69 million in 2026 and is forecast to reach USD 133.04 million by 2031.

Which region drives growth through 2031?

Asia-Pacific leads, with a 5.16% CAGR through 2031 as China, India, and ASEAN nations continue specifying legacy oil-borne preservatives in infrastructure projects.

What segment accounts for the biggest pentachlorophenol market share in 2025?

Wood preservatives remain dominant, representing 60.22% of 2025 revenue even amid substitution pressures.

How are regulations influencing supplier strategies?

Major producers are idling U.S. capacity, acquiring eco-friendly technologies, and consolidating to manage hazardous-waste liabilities ahead of the 2027 use-up deadline.

Page last updated on: