Silicon Metal Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 3.66 Million tons |

| Market Volume (2031) | 4.74 Million tons |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

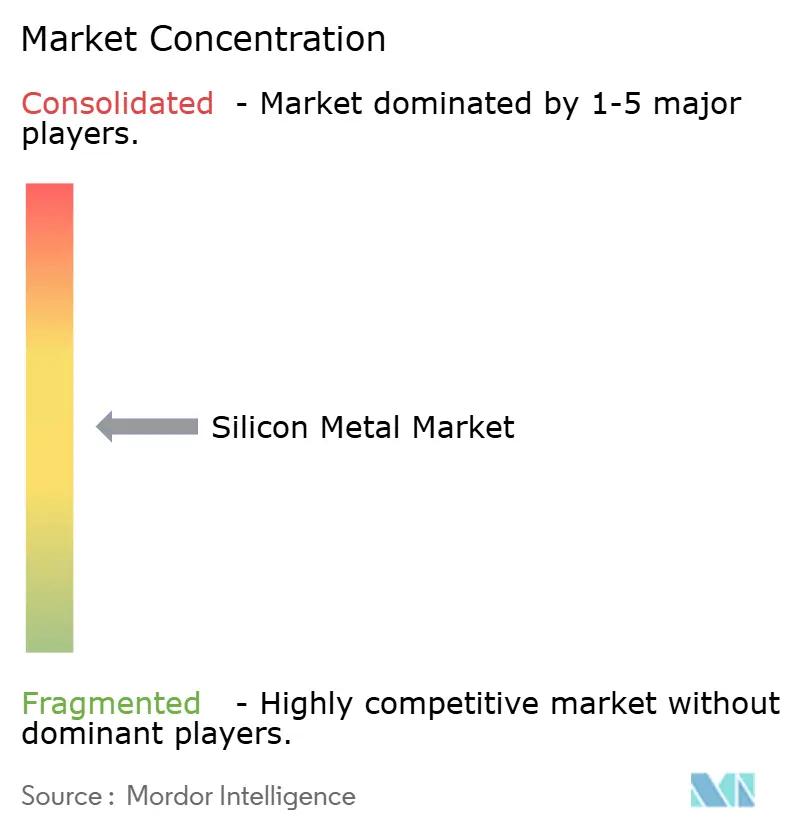

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicon Metal Market Analysis by Mordor Intelligence

Silicon Metal Market size in 2026 is estimated at 3.66 million tons, growing from 2025 value of 3.47 million tons with 2031 projections showing 4.74 million tons, growing at 5.35% CAGR over 2026-2031. The upward trajectory reflects the material’s pivotal role in aluminum lightweighting, solar-PV modules, and silicon-anode batteries. Production cuts announced by Chinese smelters in April 2025 sharpened global supply awareness even as demand from automotive gigacasting, photovoltaic expansions, and semiconductor recovery stayed firm. Trade policy actions, including new U.S. antidumping petitions and existing tariffs on several Asian origins, have widened regional price spreads, elevating North American premiums but allowing Asian buyers to capitalize on lower spot values. Energy-intensive production economics and tightening carbon regulations continue to shift procurement toward low-emission suppliers. Parallel progress in silicon-anode technology, supported by sizable federal grants and private capital rounds, offers a nascent yet strategically important outlet that could cushion the silicon metal market against future cyclic downturns.

Key Report Takeaways

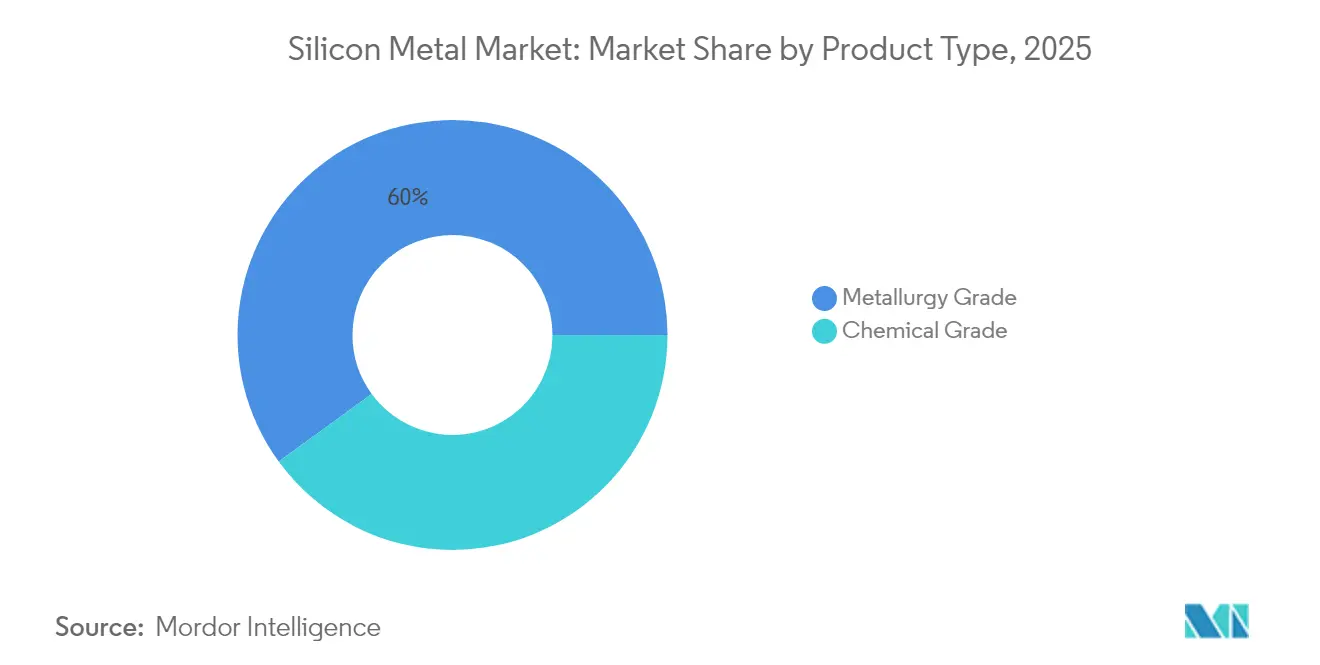

- By product type, metallurgy grade led with 60.02% of silicon metal market share in 2025 and posted the fastest 5.83% CAGR through 2031.

- By form, lump accounted for 44.62% share of the silicon metal market size in 2025 whereas powder registered a 6.25% CAGR forecast to 2031.

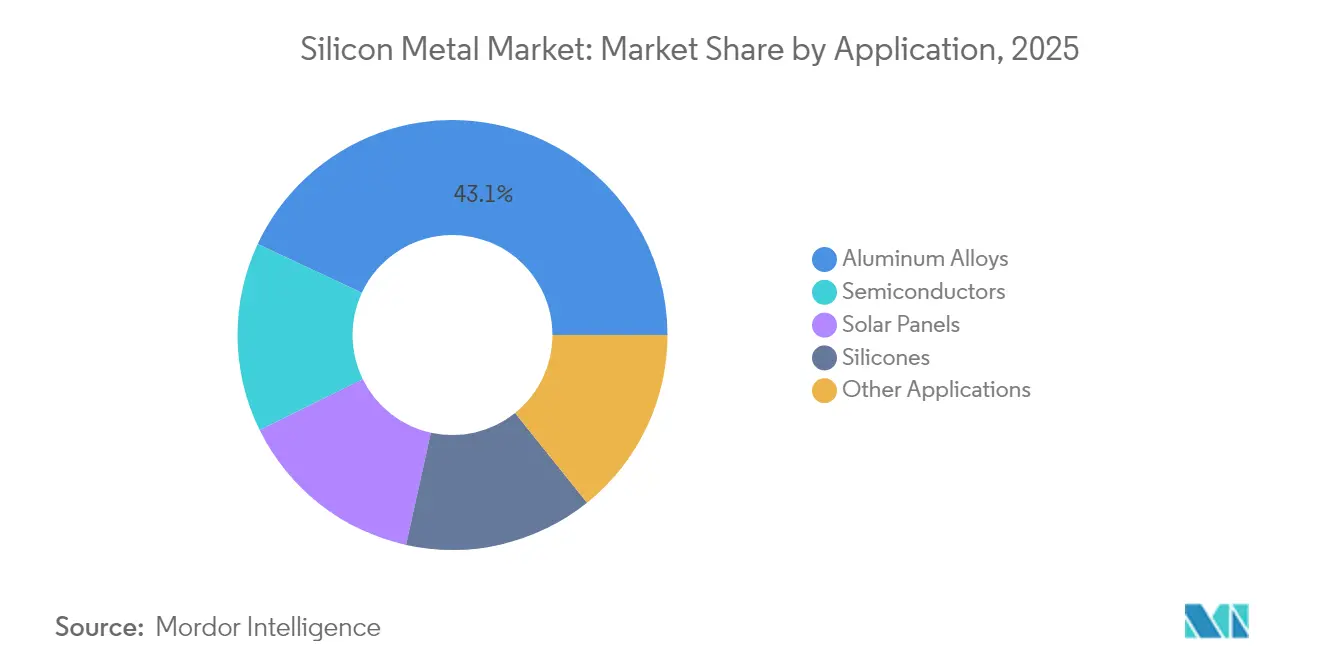

- By application, aluminum alloys captured 43.05% of the silicon metal market share in 2025; solar panels are projected to expand at 6.92% CAGR to 2031.

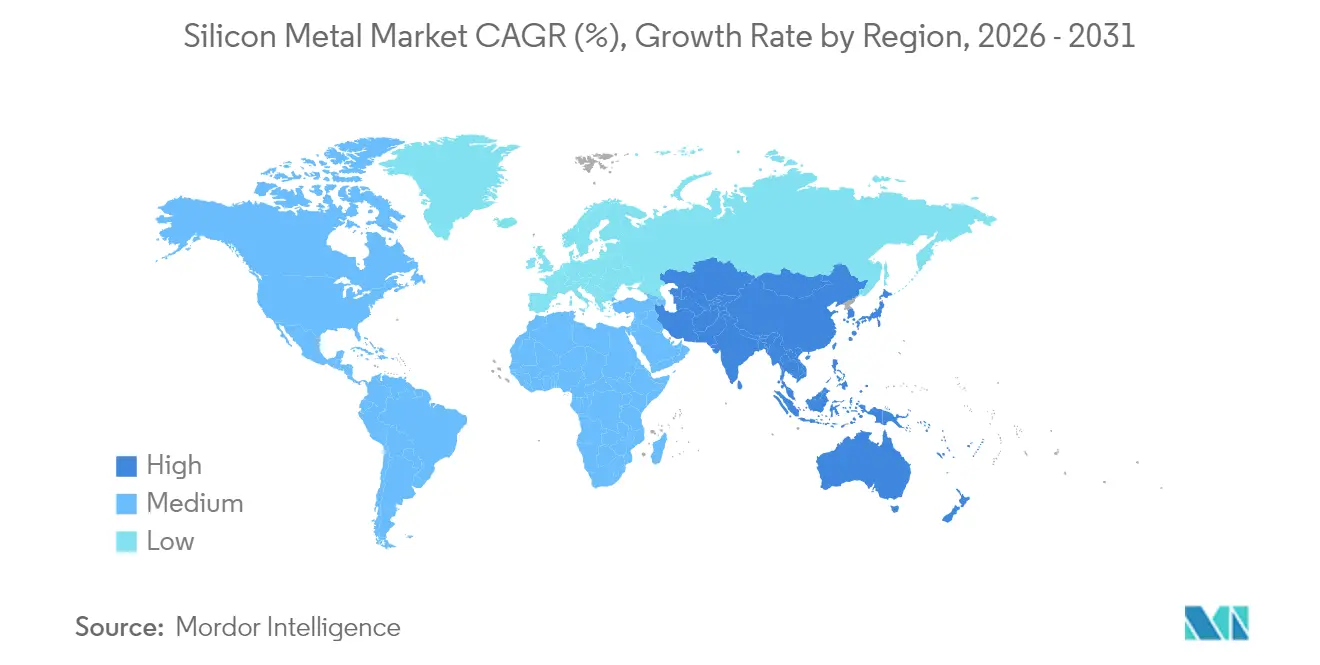

- By geography, Asia-Pacific commanded 67.74% share of the silicon metal market in 2025 and is advancing at a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicon Metal Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight Al-Alloy demand boom | +1.2% | APAC and North America | Medium term (2-4 years) |

| Solar-PV capacity additions accelerating | +1.8% | Global, led by APAC and emerging markets | Short term (≤ 2 years) |

| Expanding global silicones capacity | +1.1% | North America, Europe, APAC | Medium term (2-4 years) |

| Semiconductor content growth per device | +0.9% | Global, concentrated in APAC hubs | Long term (≥ 4 years) |

| Silicon-anode batteries commercialising | +0.4% | North America and APAC early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweight Al-Alloy Demand Boom (Automotive and EV)

Automotive OEMs are raising aluminum content per vehicle because lighter structures extend driving range without enlarging battery packs. Tesla’s gigacasting adoption spurred other EV start-ups in China to replicate large aluminum body sections that need high-purity metallurgy-grade silicon additives. Aluminum foundries in the United States and Europe have announced capacity expansions that secure local alloy grades yet intensify demand for stable silicon inputs. Chinese alloy producers keep price leadership thanks to scale, though higher freight and tariff barriers erode some of that edge for buyers west of the Pacific. As more battery enclosures move from cast iron to aluminum, silicon metal purchases from automotive tier-ones rise in tandem with every new EV platform rollout. The driver therefore underpins steady baseline growth in the silicon metal market even when cyclical sectors fluctuate.

Solar-PV Capacity Additions Accelerating

China shipped 499 gigawatts of PV modules in 2024 and targets more than 580 gigawatts in 2025. Polysilicon oversupply forced leading Chinese producers to cut furnace utilization below 40% yet the government’s clean-energy mandate keeps greenlighting new downstream capacity. India, Brazil, and the Middle East accelerate solar flotillas that lean on imported ingots, adding breadth to global demand. Although polysilicon margins compressed severely, silicon metal consumption for rod reactors remains tied to long-term installation curves, not quarterly price swings. As modules become more efficient, wafer makers compensate by using higher quality feedstock, indirectly lifting purity requirements for chemical-grade silicon. Even with short-term volatility, the multi-year solar buildout reinforces a strong positive contribution to the overall silicon metal market.

Expanding Global Silicones Capacity

Dow, Wacker Chemie, and Shin-Etsu each approved multi-year debottlenecks that lift silicone elastomer volumes for construction and automotive sealants. Unlike solar or semiconductors, silicones tap many end-markets, buffering demand across economic cycles. New architectural codes that mandate weather-resistant façades fuel the adoption of silicone-based coatings, especially in Southeast Asia’s tropical climates. Electronics OEMs specify thermal interface materials made from specialty silicones that dissipate heat in high-power servers, adding premium pull on high-purity silicon metal feedstock. North American converters pursue domestic sourcing to hedge logistical risk, supporting new smelter feasibility studies in Canada. The diversified consumption pattern supplies a stable tailwind for the silicon metal market, limiting exposure to single-sector swings.

Semiconductor Content Growth per Device

Wafer shipments are projected to rise between 11% and 19% in 2025 as AI servers and edge devices proliferate[1]SEMI, “Quarterly Wafer Shipment Forecast,” semi.org. Advanced packaging requires a larger die per package as well as through-silicon vias, lifting raw silicon intensity. Taiwan’s TSMC and South Korea’s Samsung both run multibillion-dollar fabs that backstop bulk polysilicon demand. While memory downturns can dent near-term offtake, the secular trend toward higher transistor counts sustains a positive slope. Emerging silicon-on-insulator substrates impose stricter impurity specifications, favoring suppliers with upgraded refining lines. The geographically concentrated node ecosystem in East Asia underlines the need for secure feedstock, reinforcing a long-term, albeit moderate, boost to the silicon metal market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy-cost and CO₂-intensive production | -1.5% | Europe and North America | Short term (≤ 2 years) |

| China-centric supply-chain price volatility | -0.8% | Global, acute in import-dependent regions | Medium term (2-4 years) |

| Forced-labor trade restrictions risk | -0.6% | Global, concentrated on Xinjiang-sourced materials | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy-Cost and CO₂-Intensive Production

Producing 1 ton of silicon metal consumes near 12 megawatt-hours of electricity, exposing smelters to volatile power tariffs across Europe and parts of North America. EU carbon prices above EUR 80 per ton CO₂ further burden Western players that already pay twice the grid rates typical in Yunnan or Sichuan. Elkem’s Norwegian pilot to capture furnace off-gas and recycle it as a reductant demonstrates proactive mitigation yet demands heavy capex. Absent such low-carbon upgrades, cost gaps can exceed USD 650 per ton, eroding regional competitiveness. Buyers with ESG mandates favor greener supply but balk at paying steep premiums, leading some European fabricators to import Asian material despite tariff exposure. The restraint suppresses expansion plans in high-cost geographies and drags on the global silicon metal market growth momentum.

Forced-Labor Trade Restrictions Risk

The Uyghur Forced Labor Prevention Act presumes all Xinjiang-origin silicon is tainted unless proven otherwise, obliging importers to produce rigorous traceability records[2]U.S. Department of Commerce, “Uyghur Forced Labor Prevention Act Entity List,” commerce.gov . Hoshine Silicon Industry’s inclusion on U.S. entity lists in 2024 exemplifies reputational exposure. Customs detentions delay shipments for months, forcing buyers to split supply lots and raise working capital buffers. Global brands issue supplier codes requiring independent audits, prompting some smelters to exit the region entirely. Compliance technology such as blockchain tracing raises overhead for smaller players, indirectly consolidating the market. While the restriction chiefly affects chemical-grade flows into polysilicon, spillover sentiment squeezes metallurgy-grade sales linked to suspect mines, dampening the silicon metal market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metallurgy Grade Maintains Volume Leadership

Metallurgy grade contributed 60.02% to 2025 shipments and is forecast to grow 5.83% annually on the back of sturdy aluminum alloy demand in automotive and aerospace. This portion of the silicon metal market size equated to just over 2.08 million tons and scales in near lockstep with aluminum casting output in China, the United States, and Mexico. Gigacasting adoption multiplies alloy ingot pull per vehicle, embedding silicon at roughly 7% weight in key alloy series. Asian smelters leverage hydro-power and large submerged-arc furnaces to deliver low-cost feedstock, helping the silicon metal market maintain competitive pricing despite energy hikes elsewhere. Looking ahead, 3D-printed aluminum structures could modestly reduce melt volumes yet raise purity requirements, supporting premium niches.

Chemical grade covers the balance and supports polysilicon, silicones, and semiconductor raw material flows that swing with technology cycles. Silicon metal market share for chemical grade fell marginally in 2025 as polysilicon oversupply pressed volumes, but replacement demand from electronics and EV battery supply chains caps the downside. Vertical integrators aligned with wafer and chemical plants hedge price risk by self-consuming, shielding margins when external orders soften. Over the forecast, modest recovery in solar investment and stable silicones end-markets keeps chemical-grade CAGR in the 4% zone, slower than metallurgy yet integral to the silicon metal market’s resilience.

By Form: Powder Segment Rises on Advanced Applications

Lump still dominated at 44.62% in 2025 due to ease of charging submerged-arc furnaces and lower processing cost. Nevertheless, powder shipments are climbing 6.25% per year, and the share of the silicon metal market size tied to powders could top 29.00% by 2031. Fine powders under 10 microns supply lithium-ion battery anodes, thermal interface pastes, and metal additive manufacturing. Producers invest in inert-gas atomizers to achieve spherical morphology that improves flowability in laser sintering systems, thereby carving out high-margin channels. Granules remain important for chemical reactions that rely on surface-area control, but growth is moderate.

Powder’s ascent attracts newcomers specializing in chemical vapor deposition coatings and composite matrix fillers. Prices hover 15-18% above lump on an equivalent silicon basis, cushioning margins against energy inflation. Regulatory scrutiny over dust hazards spurs the adoption of encapsulated handling systems that raise barriers to entry. Over time, inter-material competition from nano-silica and silicon carbide may temper absolute growth, but the powder form’s flexibility locks it in as the fastest contributor to incremental demand across the silicon metal market.

By Application: Solar Panels Outpace Long-Time Alloy Leader

Aluminum alloys absorbed 43.05% of global consumption in 2025 and continue as the cornerstone of the silicon metal market. Every metric ton of AlSi castings requires 70–100 kilograms of silicon, and the automotive transition to lightweight frames anchors a durable baseline. Construction extrusions in the Middle East and Southeast Asia add further volume, extending geographic spread. Yet solar panels now hold the highest growth slot at 6.92% CAGR to 2031, primed by ambitious climate targets and falling module costs.

Polysilicon’s current glut reduced furnace run-rates, but module shipment momentum remains intact, ensuring that chemical grade uptake resumes once destocking concludes. Semiconductor and silicones applications share roughly equal slices near 10% each, giving the silicon metal market diverse income streams. Niche emerging uses range from high-entropy alloys for aerospace to porous silicon in next-gen sensors. Some of these pathways could unlock step-change demand if commercial hurdles fall, but the core application mix remains stable throughout the outlook.

Geography Analysis

Asia-Pacific delivered 67.74% of 2025 tonnage and is tracking a 5.78% CAGR to 2031, making it the leading region in the silicon metal industry. The region is supported by China’s integrated mine-to-module clusters that shorten lead times and compress cost. Yunnan’s hydro-rich grid lowers power tariffs, maintaining smelter breakevens even with carbon fees. Japan and South Korea add refined demand via cutting-edge semiconductors and EV platforms. Indonesia channels USD 45.74 billion into silica downstreaming to hatch regional alternatives that hedge against Chinese dominance.

North America logged premium spot prices as antidumping probes steered imports away, magnifying supply tightness. The Inflation Reduction Act’s domestic content rules encourage fresh furnace projects in the Pacific Northwest, where hydro-power can partially neutralize energy cost headwinds. Canada positions its low-carbon grid as a magnet for OEMs seeking ESG-compliant alloys. Europe faced similar cost challenges with electricity tariffs, yet, embraced innovation grants to advance CO₂-free process pilots, keeping capacity viable through technology differentiation.

Brazil leverages abundant quartzite and existing metallurgical know-how, while Gulf Cooperation Council members channel cheap natural gas and solar power into aluminum complexes that require silicon alloying. Africa focuses on solar-PV buildouts in high-insolation corridors, promising a future lift in polysilicon-related demand. The mosaic underscores how regional energy economics and policy filters govern the silicon metal market’s evolving geography.

Value Chain Analysis

The silicon metal value chain starts with quartz and quartzite mining and beneficiation, along with reductants (notably carbon sources) and electrodes consumed in submerged-arc furnaces. Smelting is the main value-add step and is structurally tied to electricity availability and price, with power typically accounting for a large share of total production cost. This concentrates competitive capacity in low-cost power regions. Output then splits into metallurgy-grade shipments for aluminum alloying (including automotive casting and extrusion supply chains) and chemical-grade material routed to polysilicon and silicones producers, where additional refining and granulation or powdering steps may be required depending on end-use purity and handling needs.

Midstream and downstream logistics and compliance increasingly influence flows. The United States remains a net importer and, per USGS, domestic silicon metal and ferrosilicon production in 2025 occurred at five facilities located east of the Mississippi River, making import channels and distributor inventories important for alloy makers and chemical customers. Trade actions have become a bottleneck and a rerouting trigger: the April 2025 antidumping and countervailing duty petitions filed by Ferroglobe and Mississippi Silicon, and the European Commission safeguard actions finalized via Regulation (EU) 2025/2351 in November 2025, added policy-driven friction that can shift volumes between regions and increase the value of traceable, lower-risk supply for downstream buyers.

Competitive Landscape

The global industry is moderately fragmented, with leading silicon metal manufacturers such as Elkem, Ferroglobe, Wacker Chemie, GCL Technology, and Hoshine leverage scale and integrated supply. Chinese producers trimmed output in April 2025 to stabilize domestic margins, signaling coordinated supply stewardship. Trade policies reshape the playing field. The April 2025 U.S. petitions applied pressure on Australian, Laotian, Norwegian, and Thai exporters, prompting some to reroute volumes to Europe and Japan. Technology investment represents another front: companies pair submerged-arc furnaces with photovoltaic power arrays to mitigate electricity volatility, while powder specialists build proprietary surface treatments to secure battery OEM approvals.

Silicon Metal Industry Leaders

Elkem ASA

Ferroglobe

Hoshine Silicon Industry Co., Ltd.

Rusal

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Low-carbon and traceable supply is a clear whitespace as buyers face higher scrutiny on emissions and origin, while silicon metal production remains energy intensive. That shows up in Western producer and policymaker efforts to upgrade processes and use protection measures, including Elkem's CO2-mitigation work in Norway and the EU's safeguard measures finalized on certain ferro-alloying elements in November 2025 (Regulation (EU) 2025/2351). Together, these actions change the relative attractiveness of sourcing inside versus outside the bloc. Projects and financing that align production with energy strategy also create room for differentiation, such as Ferroglobe securing financing in 2025 to support silicon metal production expansion in South Africa aimed at renewable energy and semiconductor supply chains.

On the supply side, capacity additions and operating-model modernization in China create an opportunity for scale players to compete on unit costs and delivery reliability, while non-China investments focus more on resilience and compliance. East Hope Group reported progress at its Lanzhou Silicon Project in Northwest China in March 2026, with 10 of 28 planned furnaces operational toward a 400,000-ton annual design and a 5G-enabled factory approach, highlighting automation and digital operations as levers to lower conversion costs. On the demand side, upgrades in solar cell technology (TOPCon, HJT) and the push toward higher purity inputs create openings for refiners and powder producers that can meet tighter specs for chemical-grade and advanced-material applications, including silicon-anode battery pathways where qualification cycles favor consistent particle engineering and impurity control.

Recent Industry Developments

- March 2026: Hoshine Silicon Industry Co., Ltd. announced a private placement plan to raise up to RMB 5.8 billion to fund energy-linked infrastructure at its Shanshan Silicon-based New Materials Industrial Base, including a coal-electricity integration project, and to supplement working capital. The plan targets a structurally lower and more controllable power cost base, a key lever in silicon metal competitiveness.

- April 2025: U.S. producers Ferroglobe and Mississippi Silicon filed antidumping and countervailing duty petitions covering silicon metal imports from Australia, Laos, Norway, and Thailand. The action elevated trade-policy risk in procurement strategies and contributed to wider regional price spreads and supply rebalancing.

- November 2024: Elkem secured EU Innovation Fund support to pilot carbon-capture reuse at Norwegian plants with the objective of producing CO2-free silicon metal. The project highlighted how decarbonization-linked funding is being used to support high-cost regions and build differentiated supply for ESG-sensitive downstream customers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the silicon metal market covers the production and consumption of silicon metal sold as a raw material across major producing and consuming regions, tracked by volume along the supply chain from smelters to downstream users.

Scope exclusions: We exclude downstream finished goods value, such as aluminum parts, silicones, solar modules, and semiconductor devices, even though silicon metal is used in making them.

Segmentation Overview

- By Product Type

- Metallurgy Grade

- Chemical Grade

- By Form

- Lump

- Powder

- Granules

- By Application

- Aluminum Alloys

- Semiconductors

- Solar Panels

- Silicones

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Turkey

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- Nigeria

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a starting point for silicon metal supply, trade, and use-case context before any sizing assumptions were locked. We referred to public and official sources such as USGS mineral statistics, UN Comtrade trade flows, World Bank macro indicators, and IEA energy and industrial datasets, since power availability and costs are closely linked to smelting output.

Along with these, we reviewed company annual reports and investor presentations to track capacity changes, maintenance cycles, and end-use exposure. Technical papers and patents were also reviewed to understand purity requirements and application shifts, including routes tied to chemical uses and polysilicon. Where needed, paid subscriptions for company financials and a shipment-level import-export database were used to cross-check trade intensity and flag abnormal movements in specific years. These examples are not exhaustive, and additional public and paid sources were checked to complete coverage, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on expert interviews and structured surveys with participants across the value chain, including producers, distributors, and downstream buyers tied to aluminum alloying, silicones, solar, and semiconductor-adjacent uses. Because output and pricing can change with energy constraints and regional policy settings, we used conversations across APAC, EMEA, and the Americas to confirm the drivers behind volume moves and the points where substitution appears in practice.

Inputs from these respondents were then used to refine the practical boundaries of the market, validate utilization and trade assumptions, and stress-test forecast inputs so the model stayed grounded in operational expectations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | APAC: 48% |

| Mid tier: 48% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 19% | Managers: 55% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where production, trade, and apparent consumption signals were reconstructed by region, then mapped to silicon metal use in key downstream demand pools. The model was subsequently checked using selective bottom-up approximations, such as sampled supplier volumes, channel checks on import mixes, and sanity checks using typical consumption intensity in aluminum alloying and chemical uses.

A few practical inputs kept the model anchored, including smelter capacity and utilization ranges, import-export balance by major corridors, application mix shifts between metallurgy and chemical pathways, energy availability markers that influence operating rates, and regional policy or environmental constraints that can temporarily remove supply. For forecasting, scenario analysis was used so demand growth and supply restarts were not assumed to be smooth, and scenarios were aligned to what interviewees expected for ramp-ups, restarts, and demand normalization. Where bottom-up signals were incomplete for smaller producers or for fragmented trade routes, gaps were handled by applying region-specific coverage ratios, cross-checked with trade intensity and utilization feedback.

Data Validation & Update Cycle

Validation was done in layers so that clear errors were caught early and smaller drifts were corrected before sign-off. We compared market totals against independent indicators such as trade directionality, utilization narratives, and application-level demand markers, then investigated large variances by revisiting assumptions and rechecking the underlying source data.

Before finalization, the model and key assumptions went through an internal multi-step review, and respondents were re-contacted when outputs did not match operational reality, for example where reported supply cuts or restarts did not align with observed trade movements. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest view available at the time of publication.

Mordor Intelligence's Silicon Metal Market Sizing Compared With Other Published Estimates

Published market sizes for silicon metal often do not match because the boundary of what is being counted can shift, and because the unit of measurement can change between value and volume. Differences also show up when pricing assumptions are applied without clearly stating the grade mix, trade timing, or currency treatment.

By tracking production and trade indicators and then converting them into a demand-led volume view, Mordor Intelligence keeps the estimate aligned to the physical silicon metal market, while some sources blend in price-led revenue totals that move quickly with energy cost swings and regional shortages.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.47 M (2025) | |

| Global Consultancy A | USD 8.00 B (2025) | Uses a revenue-based definition that depends heavily on assumed average prices and grade mix, which can inflate totals when spot prices rise even if physical volumes stay similar. |

| Industry Publisher B | USD 8.51 B (2025) | Counts value across application chains and applies regional share assumptions, which can shift the market upward when downstream pricing or regional mix is treated inconsistently year to year. |

The spread in the table mainly comes from whether the market is expressed as physical volume or as revenue that is sensitive to price cycles and grade definitions. With clearer boundaries, traceable inputs, and repeatable checks against trade and utilization signals, the final number stays easier to interpret and to update when conditions change.

Key Questions Answered in the Report

How fast is global demand for silicon metal expected to grow through 2031?

Volume expands from 3.66 million tons in 2026 to 4.74 million tons in 2031 at a 5.35% CAGR.

Which region commands the largest share of silicon metal consumption?

Asia-Pacific accounted for 67.74% in 2025, driven by integrated supply chains and lower power costs.

What application will add the most incremental tons by 2031?

Solar panels lead growth at a 6.92% CAGR as global PV installations rise despite current polysilicon oversupply.

Why are Western smelters investing in carbon-capture technology?

High energy prices and EU carbon charges threaten cost competitiveness, so low-carbon upgrades help secure market access and price premiums.

How are trade policies influencing regional silicon prices?

U.S. antidumping actions and existing tariffs widen spreads, lifting North American prices to USD 2,751 per ton versus USD 1,459 in Asia-Pacific.

Page last updated on: