Silicone Surfactant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

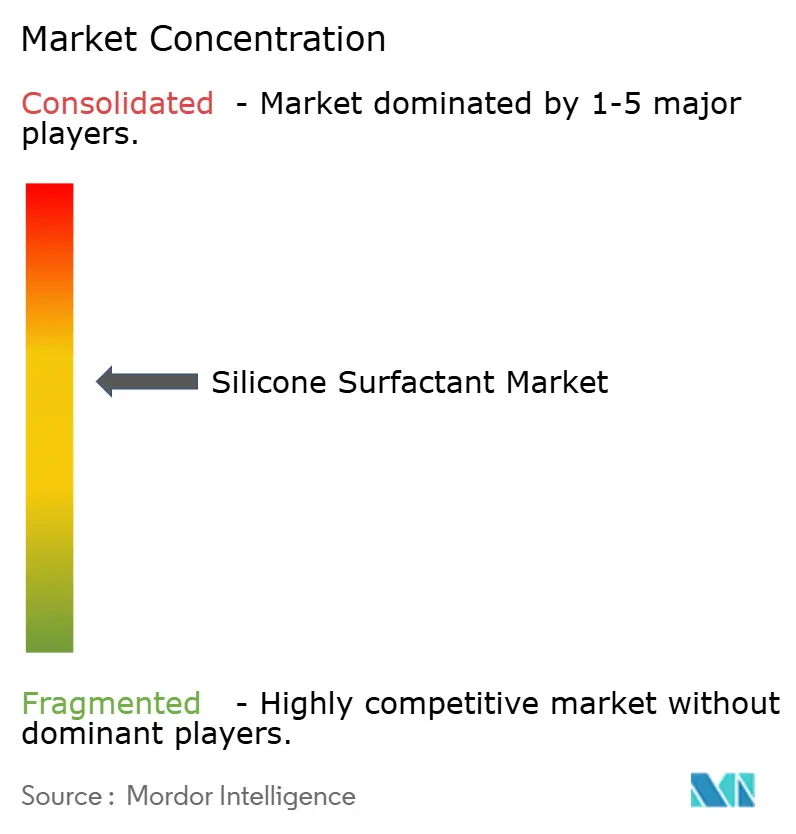

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone Surfactant Market Analysis by Mordor Intelligence

The Silicone Surfactant Market size was valued at USD 2.55 billion in 2025 and estimated to grow from USD 2.65 billion in 2026 to reach USD 3.18 billion by 2031, at a CAGR of 3.76% during the forecast period (2026-2031). Measured growth reflects a maturing landscape in which sustainable formulations, precision agriculture and advanced polyurethane foams become primary demand engines. End-user focus is shifting toward high-value, biodegradable chemistries that satisfy tightening global regulations on cyclosiloxanes and PFAS. Consolidation among vertically integrated producers is accelerating investment in renewable electricity and circular feedstocks, while medium-sized specialty suppliers target drone-ready agricultural adjuvants and PFAS-free textile finishes. Asia-Pacific remains the largest consumption hub thanks to expanding middle-class personal-care spending, growing polyurethane demand in construction and rapid textile wet-processing build-outs. North America and Europe influence the innovation agenda through strict chemical policies that reward bio-based silicone chemistries.

Key Report Takeaways

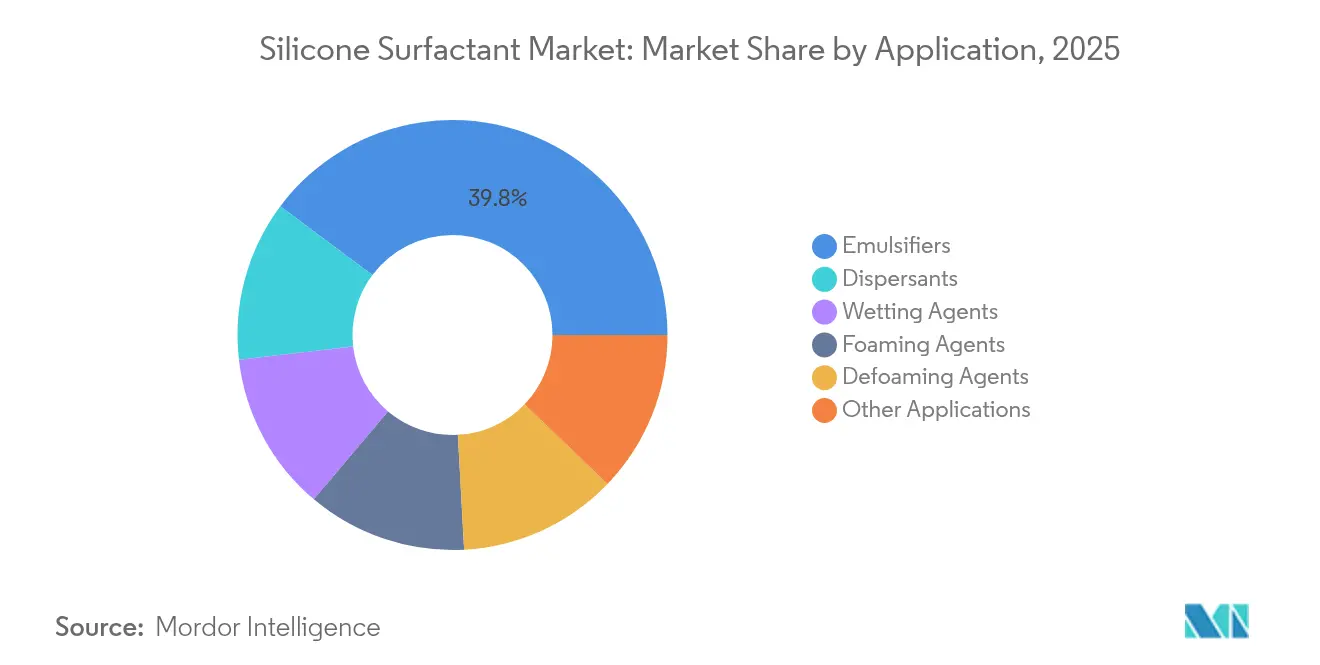

- By application, emulsifiers led with 39.78% of silicone surfactants market share in 2025, while the other-applications cluster is projected to post the fastest 4.55% CAGR through 2031.

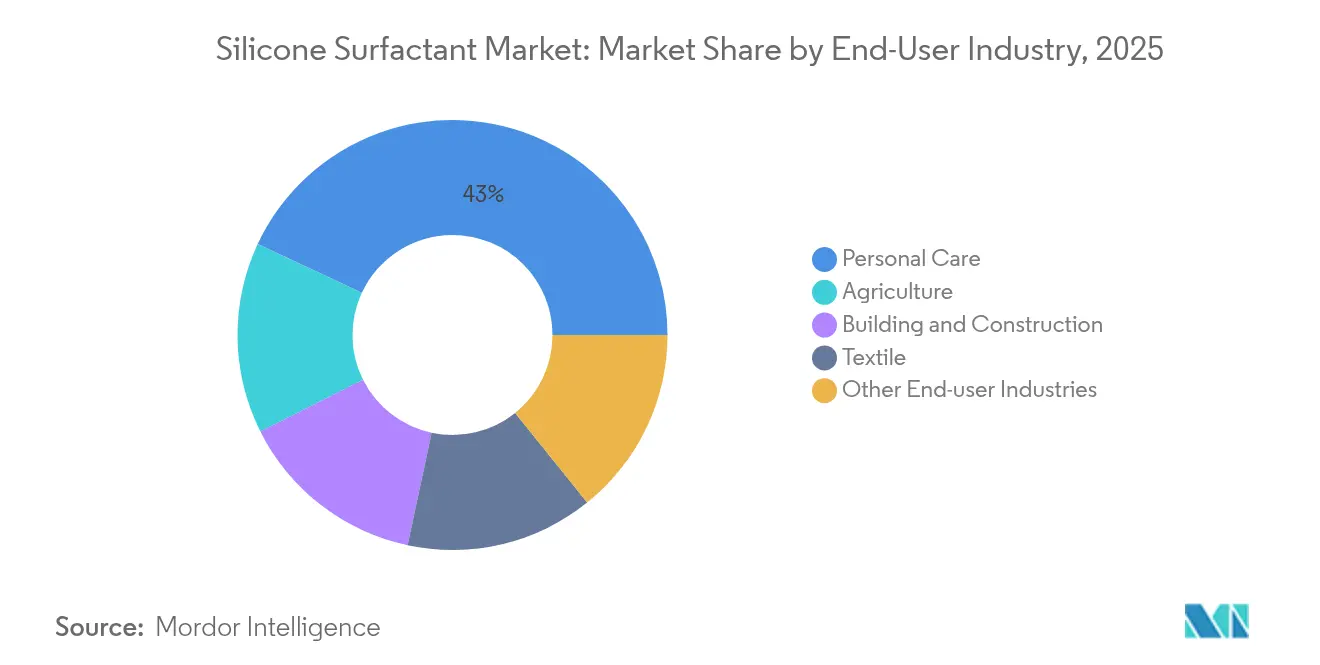

- By end-user industry, personal care accounted for 43.05% share of the silicone surfactants market size in 2025; agriculture is advancing at a 4.35% CAGR to 2031.

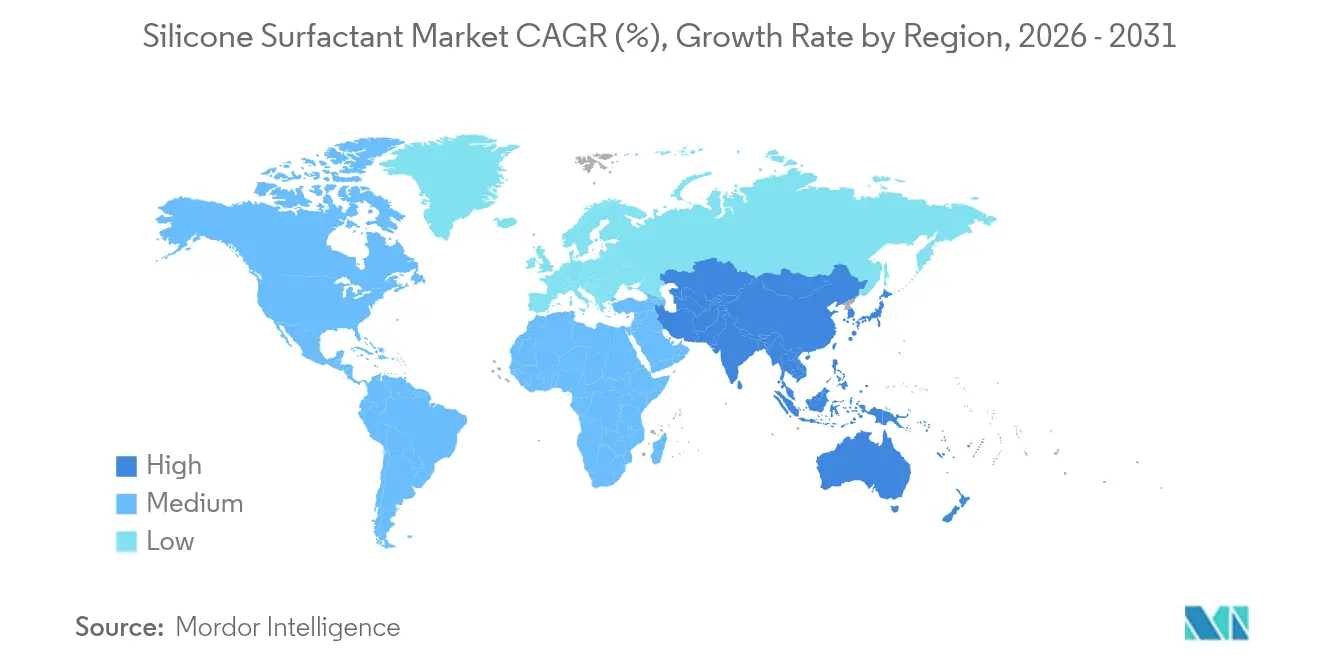

- By geography, Asia-Pacific contributed 45.86% revenue share in 2025, and the region is forecast to register a 4.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicone Surfactant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sensorial silicone‐based personal-care formulations | +1.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid growth of polyurethane foam industry in construction and automotive | +0.80% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Increasing use of super-spreader adjuvants in precision agriculture | +0.60% | Global, with early gains in North America & APAC | Medium term (2-4 years) |

| Expansion of textile wet-processing in emerging economies | +0.40% | APAC emerging markets, particularly Southeast Asia | Long term (≥ 4 years) |

| Sugar-modified, biodegradable silicone surfactants gaining traction | +0.30% | Europe & North America, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sensorial Silicone Formulations in Personal Care

Demand for multisensory skin-care and hair-care products is fueling complex emulsion systems that rely on silicone surfactants to deliver light textures, quick absorption and adaptive moisturization. BASF showcased climate-responsive skin-care prototypes at Cosmet’Agora 2025, highlighting silicone-enabled water-in-oil emulsions that adjust to humidity and temperature shifts[1]BASF, “Cosmet’Agora 2025: BASF Showcases Climate-Adaptive Beauty Routines,” basf.com . CHT Group introduced recycled-content silicone surfactants with 94% reclaimed monomers, merging sensorial performance with circular sourcing. Market migration toward sulfate-free cleansing intensifies the need for gentle yet high-foaming agents that silicone chemistry provides. Premium product positioning and regulatory acceptance of low-cyclic silicone grades underpin stable volume growth in this driver segment.

Polyurethane Foam Growth in Construction and Automotive

Polyurethane foam producers depend on silicone surfactants as cell regulators that stabilize froth and control thermal insulation values. Mexico's polyurethane market is experiencing consistent capacity growth. This growth is driven by nearshoring investments in the automotive sector, which significantly contribute to the nation's GDP. Bio-based polyols from vegetable oils have entered pilot scale, prompting silicone suppliers to tailor surfactants for renewable feedstock compatibility. Wacker’s 2025 expansion of silicone capacity and Dow’s rollout of bio-sourced NORDEL REN EPDM affirm industry commitment to sustainable foam chemistry. Long term, high-performance building codes and electric-vehicle battery insulation requirements underpin robust demand for silicone stabilizers.

Super-Spreader Adjuvants for Precision Agriculture

Drone-based crop protection requires surfactants that lower surface tension to improve canopy penetration while minimizing off-target drift. Evonik launched BREAK-THRU MSO MAX 522 and TEGO XP 11134, polyether-trisiloxane blends engineered for drone delivery that enhance droplet adhesion and pesticide efficacy. Momentive’s Silwet Power combines super-spreading with microbial-compatible chemistry, supporting biological pesticide uptake and soil health. Early field trials in cotton report higher pest-control outcomes with lower spray volumes, driving adoption in Southeast Asia’s rapidly mechanizing farms. These performance gains position agricultural adjuvants as the fastest incremental contributor to the silicone surfactants market through 2030.

Textile Wet-Processing Expansion in Emerging Economies

Foreign direct investment is shifting garment supply chains toward Vietnam and Bangladesh, prompting new wet-processing capacity that relies on silicone surfactants for durable softness, water repellency and color fastness. Shin-Etsu markets antimicrobial finishes that combine polydimethylsiloxane backbones with quaternary ammonium groups to meet performance and hygiene targets. Research into PFAS-free silicone water repellents on polyester blends has confirmed comparable oil repellency without fluorine chemistry[2]ScienceDirect, “Liquid-Repellent PFAS-Free Fabric Coatings,” sciencedirect.com . Adoption is strongest in Southeast Asia, elevating specialty surfactant imports. Long-term infrastructure for effluent treatment and circular dyeing processes will reinforce silicone demand in textile finishing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile siloxane monomer prices | -0.70% | Global, with particular impact on integrated producers | Short term (≤ 2 years) |

| Trisiloxane intermediate supply-chain concentration risks | -0.50% | Global, with highest risk in APAC-dependent supply chains | Medium term (2-4 years) |

| PFAS-style disclosure rules for persistent organosilicons | -0.40% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Siloxane Monomer Prices

Silicon metal and methyl chloride price swings propagate directly into siloxane costs, compressing margins for downstream formulators. Wacker still lifted EBITDA by 47% in 2024 through vertical integration, demonstrating the buffer that captive monomer units provide. Independent blenders, by contrast, face quarterly price passthrough delays that erode competitiveness. Energy-intensive direct synthesis routes expose producers to gas and electricity volatility, an issue most acute in Europe and North America during winter demand peaks. Inventory hedging and long-term offtake contracts partially mitigate risk, yet sustained volatility could shave 0.7 percentage points off the market CAGR until energy markets stabilize.

Trisiloxane Intermediate Supply-Chain Concentration

Global output of critical trisiloxane intermediates resides in a handful of large facilities, many clustered in East Asia. Any operational outage risks constraining specialty surfactant availability worldwide. The European Chemicals Agency will enforce leave-on cosmetic restrictions for D4, D5 and D6 cyclosiloxanes from June 2026, compelling formulators to re-engineer supply chains around alternative intermediates[3]European Chemicals Agency, “Cyclosiloxanes,” echa.europa.eu .EU. Additional regulatory scrutiny on broader siloxane classes could deter capital investment in new capacity. Dow’s collaboration with Circusil on closed-loop silicone recycling aims to cut PDMS carbon footprints by more than 50% and diversify feedstock sources, though commercial scale-up is slated for post-2027. Persistent concentration therefore presents a medium-term drag on the silicone surfactants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Emulsifiers Sustain Leadership as Specialty Uses Accelerate

Emulsifiers retained the largest revenue slice in 2025 with 39.78% of silicone surfactants market share, buoyed by personal-care and industrial formulations that depend on stable oil-in-water systems. The segment’s staying power derives from the ability of silicone chains to orient at interfaces with minimal dosage, thereby enhancing sensory feel and freeze-thaw stability.

Other applications such as electronics cooling fluids, photovoltaic sealants and advanced coatings are forecast to grow at a 4.55% CAGR through 2031, faster than the broader silicone surfactants market. Wetting agents that achieve surface tensions below 20 mN/m enable thinner photoresist layers and efficient agricultural sprays, while novel sulfonate-based defoamers suppress entrapped air in high-shear resin systems. Foaming agents drive density control in polyurethane insulation boards that meet near-zero energy building codes. Collectively, these specialty end-uses diversify revenue streams and reduce dependence on commoditized emulsifier demand.

By End-User Industry: Personal Care Dominates yet Agriculture Advances

Personal care, at 43.05% of 2025 revenue, anchors the silicone surfactants market size through high consumption of shampoos, sunscreens and color cosmetics that rely on mild cleaning, slip and shine performance. Growth within this cohort stems from the migration to sulfate-free and waterless formats in which silicone surfactants maintain foam and tactile cues without harsh detergents.

Agriculture is projected to record the fastest 4.35% CAGR as precision spraying and biological crop-protection agents spread across large farming regions. Super-spreader adjuvants cut water usage and pesticide volumes, satisfying regulatory demands for sustainable intensification. Building and construction consume silicone surfactants through sealants, elastomeric coatings and foamed insulation, leveraging thermal stability for long-lived building envelopes. Textile mills adopt silicone softeners, defoamers and water repellents to achieve premium hand feel and PFAS-free liquid repellency, particularly in Southeast Asia. Electronics and automotive applications complete the portfolio, where silicone surfactants improve dielectric cooling and paint wetting for advanced manufacturing lines.

Geography Analysis

Asia-Pacific’s leadership stems from synchronized growth in consumer spending, industrialization and inward chemical investment. The region’s 4.18% CAGR to 2031 is supported by rising middle-class personal-care demand in India, expanding polyurethane production in China and accelerating drone-assisted agriculture in Southeast Asia. Government incentives for sustainable building materials further reinforce polyurethane foam and sealant uptake. Regional producers leverage economies of scale while global suppliers establish local formulation centers to shorten innovation cycles.

North America commands steady demand driven by automotive and construction applications that incorporate high-specification silicone surfactants. Mexico’s polyurethane boom catalyzed by electric-vehicle production sustains multiyear volume growth. United States regulations phasing out legacy fluorochemicals accelerate adoption of silicone-based water repellents and surface treatments. Canada’s advanced manufacturing and resource sectors maintain baseline consumption, with federal funding promoting bio-based chemical initiatives that intersect with sugar-modified silicone development.

Europe shapes global innovation through forward-leaning regulations that restrict cyclic siloxanes and incentivize renewable electricity in chemical production. Leaders such as Germany and France channel investment toward biodegradable silicone surfactants that comply with the European Green Deal. Northern European countries set procurement specifications that require PFAS-free water repellents in textiles and construction, stimulating market demand. Regional R&D clusters cooperate with multinational suppliers to pilot closed-loop silicone recycling and carbon-negative siloxane production pathways.

Competitive Landscape

Global supply is moderately consolidated, with integrated majors controlling monomer production and downstream specialty lines while niche formulators serve regional or application-specific needs. KCC’s full acquisition of Momentive in 2024 enlarged its silicone toolkit, creating one of the five largest players by revenue. Dow restructured its Dow Corning assets to streamline specialty silicones and accelerate bio-based innovation timelines.

Strategic priorities pivot around sustainability and regional growth. Wacker commissioned a Czech formulation plant capable of 20,000 tpa to satisfy European demand for high-value fluids, elastomer gels and emulsions. Elkem, celebrating 120 years in silicon, accelerates sugar-modified silicone launches to capture natural-origin personal-care demand.

Innovation efforts concentrate on PFAS-free coatings, drone-grade agricultural adjuvants and recyclable silicone networks. Companies expand joint ventures for closed-loop silicone recycling, targeting 50% lifecycle CO₂ cuts. Early movers secure long-term supply agreements with electronics and solar manufacturers that value low-carbon content, providing competitive insulation against raw-material price volatility. Consequently, the silicone surfactants market favors firms with deep R&D budgets, integrated monomer assets and demonstrated ESG performance.

Silicone Surfactant Industry Leaders

Dow

Elkem ASA

Evonik Industries AG

Momentive

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: WACKER has inaugurated a new production complex in China, dedicated to specialty silicones. This facility will produce silicone fluids, emulsions, and elastomer gels. The expansion is expected to strengthen WACKER's position in the silicone surfactant market by enhancing production capacity.

- March 2024: KCC Corporation has finalized an agreement to fully acquire Momentive Performance Materials Group, strengthening its position in the global silicones and specialty solutions industry. This acquisition is expected to significantly influence the silicone surfactant market by enhancing product innovation and expanding market reach.

Global Silicone Surfactant Market Report Scope

The Silicone Surfactant report includes:

| Emulsifiers |

| Foaming Agents |

| Defoaming Agents |

| Wetting Agents |

| Dispersants |

| Other Applications |

| Personal Care |

| Building and Construction |

| Textile |

| Agriculture |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Emulsifiers | |

| Foaming Agents | ||

| Defoaming Agents | ||

| Wetting Agents | ||

| Dispersants | ||

| Other Applications | ||

| By End-user Industry | Personal Care | |

| Building and Construction | ||

| Textile | ||

| Agriculture | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the silicone surfactants market?

The silicone surfactants market size reached USD 2.65 billion in 2026 and is projected to hit USD 3.18 billion by 2031.

Which application segment leads revenue generation?

Emulsifiers hold the top position with 39.78% silicone surfactants market share due to their central role in personal-care and industrial emulsions.

Which end-user industry is expanding the fastest?

Agriculture is set to post a 4.35% CAGR through 2031 as precision spraying and biological crop-protection products scale.

Why is Asia-Pacific the largest regional market?

Asia-Pacific accounts for 45.86% of global demand thanks to robust manufacturing, expanding middle-class consumption and strong investment in textiles, polyurethane foams and agriculture.

What are the main growth drivers for silicone surfactants?

Key drivers include sensorial personal-care innovations, rising polyurethane foam usage in energy-efficient buildings, drone-enabled agriculture and the launch of biodegradable sugar-modified surfactants.

How are regulations shaping product development?

Restrictions on cyclic siloxanes and PFAS push manufacturers toward biodegradable and bio-based silicone chemistries, driving R&D investment and market differentiation.

Page last updated on: