Silanes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

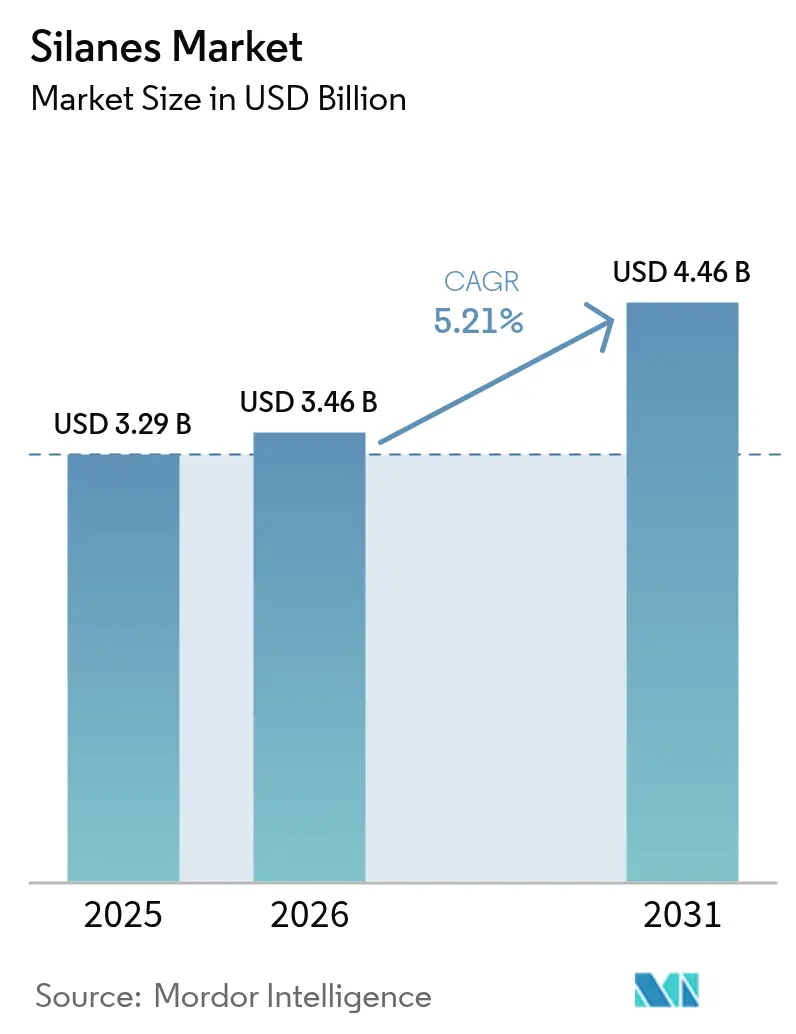

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 4.46 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

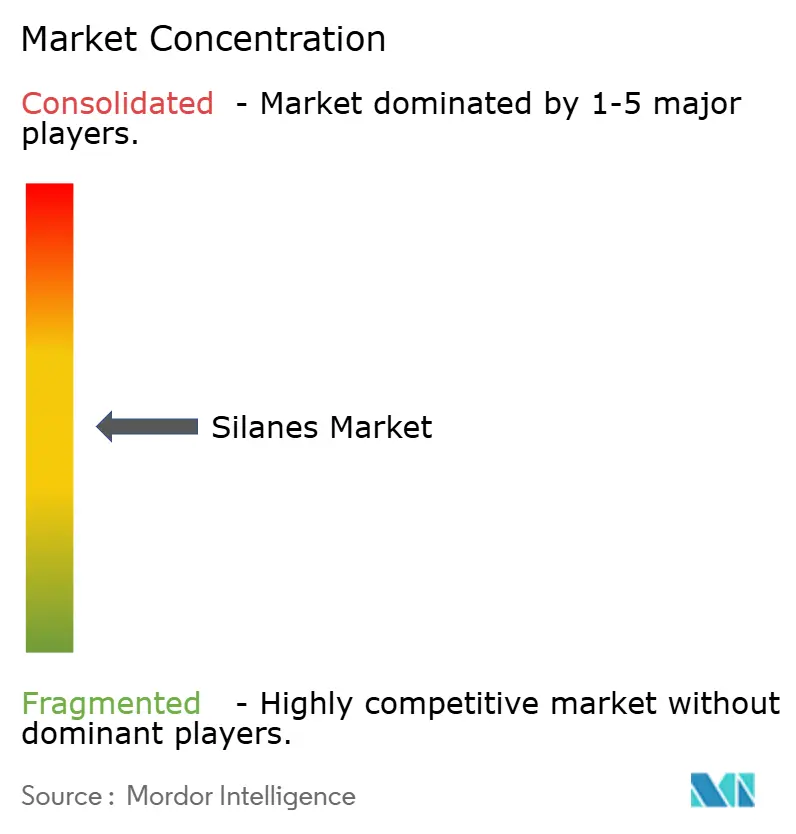

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silanes Market Analysis by Mordor Intelligence

The Silanes Market size was valued at USD 3.29 billion in 2025 and estimated to grow from USD 3.46 billion in 2026 to reach USD 4.46 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031). Rising penetration of silane-modified solutions in semiconductor packaging, green tire manufacturing, and waterborne coatings underscores the steady growth trajectory. The material’s ability to chemically bridge organic polymers with inorganic substrates continues to unlock design flexibility in electronics, mobility, and construction. Asia-Pacific’s advanced manufacturing base, sustained infrastructure activity, and supportive policy framework collectively anchor the region’s demand. Parallel R&D programs led by integrated producers such as Dow, Wacker, Evonik, and Shin-Etsu augment application breadth while buffering supply-side risks through backward integration.

Key Report Takeaways

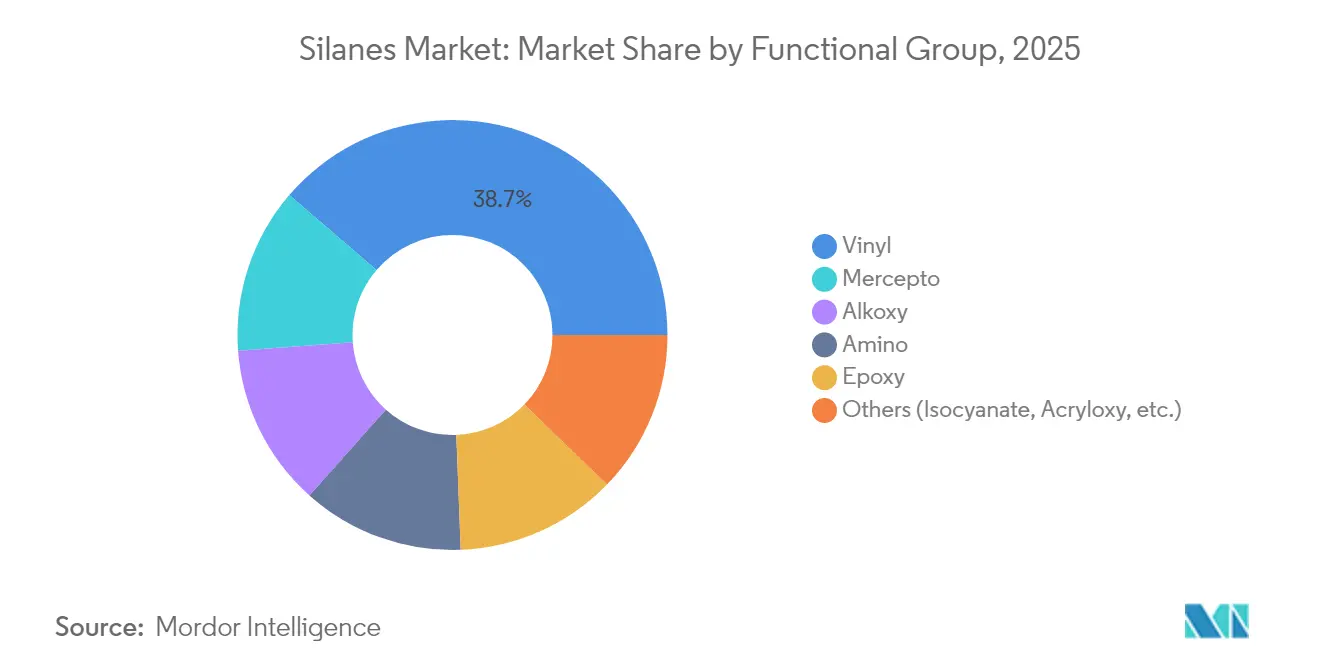

- By functional group, vinyl silanes led with 38.72% revenue share in 2025, whereas mercapto types are projected to expand at a 6.65% CAGR to 2031.

- By application, coupling agents captured 34.62% of the silanes market share in 2025; anti-corrosion treatments are poised for the highest 6.41% CAGR through 2031.

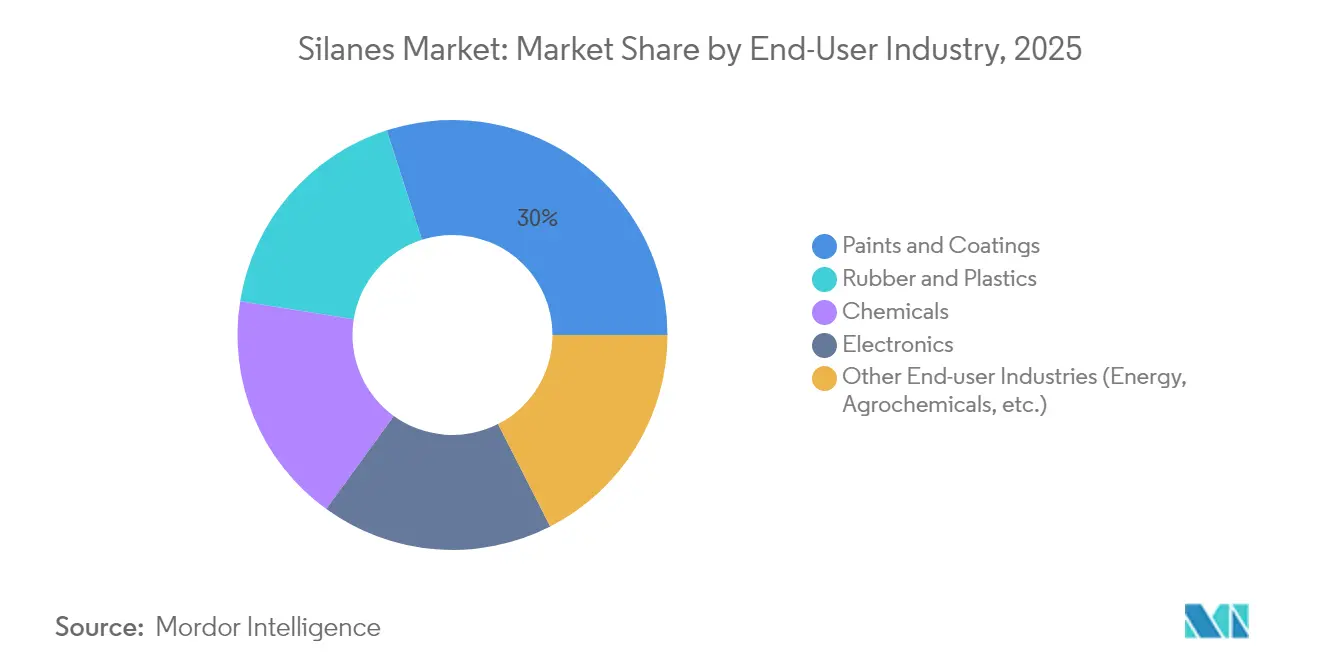

- By end-user industry, paints and coatings accounted for 29.95% share of the silanes market size in 2025, while the “Others” segment—covering energy storage and agrochemicals—advances at a 6.78% CAGR.

- By geography, Asia-Pacific commanded 46.10% of global demand in 2025 and is on track for a 6.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silanes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging paints and industrial coatings demand | +1.20% | Global, with APAC leading growth | Medium term (2-4 years) |

| Electronics miniaturisation and 5G semiconductor packaging | +0.90% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Light-weighting in electric vehicles tyres and green tires | +0.80% | Global, with early gains in China, Europe, North America | Medium term (2-4 years) |

| Water-borne adhesive adoption in construction | +0.60% | Europe & North America regulatory driven, APAC volume growth | Long term (≥ 4 years) |

| Organofunctional silanes in green hydrogen electrolyser seals | +0.40% | Europe & North America leading, APAC manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Paints and Industrial Coatings Demand

Paints and coatings represented 30.22% of the silanes market demand in 2024, a share that reflects infrastructure projects across emerging economies and stricter rules on volatile organic compounds. Water-borne formulations increasingly rely on silane coupling agents for strong adhesion between organic binders and inorganic substrates, a need magnified in marine and heavy-duty environments. California’s architectural-coatings proposal to tighten VOC limits has accelerated reformulation cycles, prompting coating formulators worldwide to adopt low-methanol silane grades[1]California Air Resources Board, “2025 Suggested Control Measure for Architectural Coatings,” arb.ca.gov . Advanced silane chemistries thus preserve coating durability while helping producers comply with evolving regulations. The resulting pull-through effect fortifies long-range demand visibility for the silanes market.

Electronics Miniaturisation and 5G Semiconductor Packaging

Logic and memory nodes below 7 nm have shifted chip-package interaction stresses, raising the bar for ultra-thin diffusion barriers. Organosilane adhesion promoters safeguard copper interconnects and passivation layers, enabling higher I/O density in fan-out wafer-level packaging. Semiconductor-grade material volumes are climbing in tandem with Asia-Pacific’s foundry expansions, while North American device makers increase local sourcing to mitigate geopolitical risk. This technical dependence embeds electronics as a durable growth locomotive for the silanes market.

Light-weighting in Electric-Vehicle Tires and Green Tires

Global electric-vehicle penetration has stimulated silica–silane coupling systems that lower rolling resistance and curb energy consumption. Bis(triethoxysilylpropyl)-tetrasulfide dominated formulations in 2024, yet new mercapto-sulfur hybrid grades are gaining traction for faster cure cycles and reduced VOC output. Green-tire programs by leading OEMs in China and Europe underpin a tangible mid-term consumption surge, reinforcing automotive as a high-value channel for the silanes market.

Water-borne Adhesive Adoption in Construction

Builders across Europe and North America continue switching from solvent-borne to water-borne sealants to satisfy stringent indoor-air-quality mandates. Silanes bridge polarity gaps between disparate substrates and elevate moisture resistance, traits that translate into longer service life for structural joints. Field trials on concrete surfaces show over 90% reduction in chloride ingress once silane treatments are applied, underscoring their protective credentials. As retrofits and resilient-building standards spread, construction adhesives remain an expanding revenue stream within the silanes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent REACH limits on VOC and methanol content | -0.70% | Europe primary, global secondary impact | Short term (≤ 2 years) |

| Tetrachlorosilane handling hazards and logistics costs | -0.50% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Semiconductor-grade silane price volatility | -0.30% | APAC manufacturing hubs, global supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent REACH Limits on VOC and Methanol Content

The European Chemicals Agency has classified cyclic siloxanes D4, D5, and D6 as persistent and bioaccumulative, compelling suppliers to overhaul product lines ahead of the June 2026 enforcement date[2]European Chemicals Agency, “Restriction of D4, D5, and D6 under REACH,” echa.europa.eu . Manufacturers must invest in analytical validation, updated safety-data-sheet management, and plant upgrades, elevating compliance costs across the value chain. Although larger incumbents can absorb these expenses, smaller formulators may curtail operations, thereby moderating short-term capacity additions to the silanes market.

Tetrachlorosilane Handling Hazards and Logistics Costs

Tetrachlorosilane reacts violently with moisture to emit hydrogen chloride, necessitating double-walled tankers and nitrogen-blanketed storage. Insurance premiums and carrier surcharges inflate landed costs, particularly in regions with limited hazardous-material infrastructure. Integrated producers with captive chlorosilane loops retain a cost advantage, while merchant buyers face margin compression. These operational realities weigh on the silanes market’s expansion pace in certain geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functional Group: Vinyl Dominance Faces Mercapto Disruption

Vinyl silanes captured 38.72% of global demand in 2025, owing to their pivotal role in silica-reinforced tires and glass-fibre composites. Their ability to graft onto filler surfaces while polymerising with rubber matrices ensures low rolling resistance and high wet-grip performance. The silanes market size attributed to vinyl chemistry is projected to advance steadily as mainstream tire producers uphold silica-based tread formulations. In parallel, mercapto silanes are forecast to post the highest 6.65% CAGR through 2031 as electronics and anti-corrosion sectors seek elevated reactivity under mild conditions. Research on dual-silane pre-modified fillers reveals superior crosslink density, indicating that hybrid chemistries could reshape future demand. Amino, epoxy, and alkoxy families continue to secure niche volumes across composites and adhesion-promotion uses, underpinning functional diversity in the silanes market.

Growing environmental focus is driving R&D into low-VOC and methanol-free grades across all functional groups. Vinyl technology benefits from incremental catalyst refinements that cut residual chlorine, while mercapto routes explore sulfur optimization for cleaner curing by-products. Suppliers also advance pre-hydrolysed concentrates that shorten mixing cycles and minimise solvent exposure. Such process innovations elevate customer productivity and tighten performance spreads, ensuring that each functional family retains relevance as the silanes market matures.

By Application: Anti-corrosion Gains Momentum Against Coupling Agents

Coupling agents represented 34.62% of overall revenue in 2025, cementing their status as the backbone of composite and adhesive interfaces. The silanes market share linked to coupling use remains sizeable, given the ubiquity of hybrid materials across automotive, construction, and electronics. However, demand for silane-based anti-corrosion systems is accelerating at a 6.41% CAGR, benefiting from regulatory bans on hexavalent-chromium pre-treatments. Multilayer metal-protection stacks now incorporate silane primers for enhanced barrier properties and paint adhesion, a trend that will amplify volume pull-through. Adhesion-promotion, moisture-scavenging, dispersant, and hydrophobing functions together extend the breadth of silane consumption, reinforcing the silanes industry value proposition across disparate end uses.

Strategic product launches, such as Evonik’s modular Dynasylan SIVO portfolio, underscore a pivot toward customisable anti-corrosion blends that accommodate wide metal substrates while respecting VOC caps. Coatings formulators adopting these systems report shorter process times and lower bake temperatures, attributes that translate into energy savings for manufacturing facilities. These operational advantages resonate strongly in sustainability-driven sectors, maintaining robust growth prospects for anti-corrosion applications within the silanes market.

By End-user Industry: Diversification Beyond Paints and Coatings

In 2025, paints and coatings commanded 29.95% of global volume, driven by infrastructure upgrades and the rapid shift to water-borne systems. The silanes market size accrued from this industry will continue expanding as protective-coatings specifications become stricter in marine, offshore, and industrial segments. Conversely, the “Others” category—spanning energy storage, agrochemicals, and hydrogen technology—is projected to grow fastest at a 6.78% CAGR. Silicon-rich anodes for lithium-ion batteries rely on tailored silane binders to mitigate volume-expansion stress, an emerging value stream poised to influence future consumption.

Rubber and plastics follow closely, underpinned by green-tire and lightweight-composite adoption in mobility applications. The electronics sector leverages ultra-pure silanes for barrier and dielectric layers, while chemical intermediates supply niche synthesis routes in pharmaceuticals and performance fluids. As each end-use explores decarbonisation and circularity, formulators increasingly prefer multi-functional silanes that deliver performance and regulatory compliance simultaneously, broadening the silanes market footprint across industries.

Geography Analysis

Asia-Pacific held 46.10% of global demand in 2025, reflecting China’s extensive electronics, automotive, and construction value chains. The silanes market size in the region is projected to compound at 6.48% CAGR through 2031 as capacity additions align with regional policy incentives for advanced manufacturing. Wacker’s multi-site footprint in Nanjing, Zhangjiagang, and Shanghai underscores the need for local production, logistics, and application-development support. India’s building-materials expansion and renewable-energy targets add further upside, while Japan and South Korea sustain premium-grade uptake for semiconductor and EV battery components.

North America remains a mature yet strategically important hub. Federal funding of USD 200 million to Group14 for a 7,200 metric-ton silane plant in Washington illustrates government efforts to strengthen domestic supply chains. Automotive electrification, aerospace composites, and resilient-infrastructure mandates collectively nurture specialized silane demand. The region’s regulatory rigor regarding VOC and toxic-substance control also rewards suppliers of low-emission formulations, fostering product differentiation in the silanes market.

Europe exhibits moderate growth as REACH compliance reshapes product portfolios and spurs adoption of chrome-free and methanol-reduced grades. Producers with integrated R&D and manufacturing, such as Evonik and Momentive, leverage site upgrades to secure market access under stricter rules. South America and the Middle East & Africa present nascent opportunities as infrastructure and industrialisation advance. Sika’s 2024 network of new plants and technology centers in India and China provide a roadmap for regional platforms that can mirror local performance norms while leveraging global process know-how. Import dependence and logistics complexity could nevertheless temper adoption rates until local manufacturing matures, creating segmented expansion profiles within the silanes market.

Competitive Landscape

The silanes market is moderately fragmented. Five leading companies—Dow, Wacker, Evonik, Momentive, and Shin-Etsu—control a sizeable share through vertically integrated silicon value chains, proprietary process technologies, and global technical-service networks. Product breadth lets these incumbents address coupling, adhesion, barrier, and surface-modification needs with tailored grades. Technical support remains a key purchasing criterion as customers prioritise application performance over pure commodity cost.

Strategic consolidation has reshaped competitive dynamics. Evonik’s January 2025 merger of its Silica and Silanes businesses into the Smart Effects platform combines filler and coupling expertise to accelerate compound-specific solutions. KCC Corporation’s 2024 acquisition of Momentive added specialty silane assets, broadening reach across electronics and industrial-coatings customers. Meanwhile, energy-storage entrants such as Group14 and Sila Nanotechnologies command investor attention for high-capacity silicon-anode innovations, signalling adjacent-industry convergence with the silanes market.

Supply-chain resilience has become a strategic imperative following pandemic-era disruptions and geopolitical tensions. Dow’s Gulf Coast chlorosilane expansion fortifies feedstock integration, while Wacker’s Charleston, Tennessee, debottleneck supports regional redundancy. Producers also intensify ESG commitments by lowering carbon footprints and phasing out high-hazard solvents, a trend expected to influence competitive positioning in forthcoming tenders.

Silanes Industry Leaders

Dow

Evonik Industries AG

Momentive

Shin-Etsu Chemical Co., Ltd.

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Evonik Industries launched Smart Effects, a strategic merger of its Silica and Silanes business lines, targeting enhanced customer solutions and operational synergies across automotive, electronics, and consumer health markets. The integration combines silane chemistry and silica technology expertise to deliver sustainable, circular solutions.

- September 2024: WACKER has introduced a new precursor silane to expand its specialty portfolio for the semiconductor industry, targeting the production of advanced memory chips and microprocessors. This development strengthens WACKER's silane market position by addressing rising demand.

Global Silanes Market Report Scope

The scope of the silanes market report includes:

| Vinyl |

| Amino |

| Epoxy |

| Mercepto |

| Alkoxy |

| Others (Isocyanate, Acryloxy, etc.) |

| Coupling Agents |

| Adhesion Promoters |

| Moisture Scavengers |

| Hydrophobing and Dispersing Agents |

| Silicate Stabilizers |

| Anti-corrosion and Surface Treatments |

| Paints and Coatings |

| Rubber and Plastics |

| Electronics |

| Chemicals |

| Other End-user Industries (Energy, Agrochemicals, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Functional Group | Vinyl | |

| Amino | ||

| Epoxy | ||

| Mercepto | ||

| Alkoxy | ||

| Others (Isocyanate, Acryloxy, etc.) | ||

| By Application | Coupling Agents | |

| Adhesion Promoters | ||

| Moisture Scavengers | ||

| Hydrophobing and Dispersing Agents | ||

| Silicate Stabilizers | ||

| Anti-corrosion and Surface Treatments | ||

| By End-user Industry | Paints and Coatings | |

| Rubber and Plastics | ||

| Electronics | ||

| Chemicals | ||

| Other End-user Industries (Energy, Agrochemicals, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the silanes market?

The silanes market size is USD 3.46 billion in 2026 and is projected to reach USD 4.46 billion by 2031.

Which region dominates global demand for silanes?

Asia-Pacific leads with 46.10% share in 2025 and is forecast for the fastest 6.48% CAGR through 2031 due to its strong manufacturing base.

Which functional group holds the largest revenue share?

Vinyl silanes account for 38.72% of demand in 2025, driven by their use in tire and composite applications.

What is the highest-growth application area?

Anti-corrosion treatments are expanding at a 6.41% CAGR as industries replace chromium-based systems with silane alternatives.

How are regulations influencing silane formulations in Europe?

REACH restrictions on VOCs and cyclosiloxanes are steering suppliers toward methanol-reduced and chrome-free grades, reshaping product portfolios in the region.

What recent strategic move signals consolidation in the industry?

Evonik merged its Silica and Silanes businesses into the Smart Effects platform in 2025 to deliver integrated performance solutions.

Page last updated on: