Shilajit Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

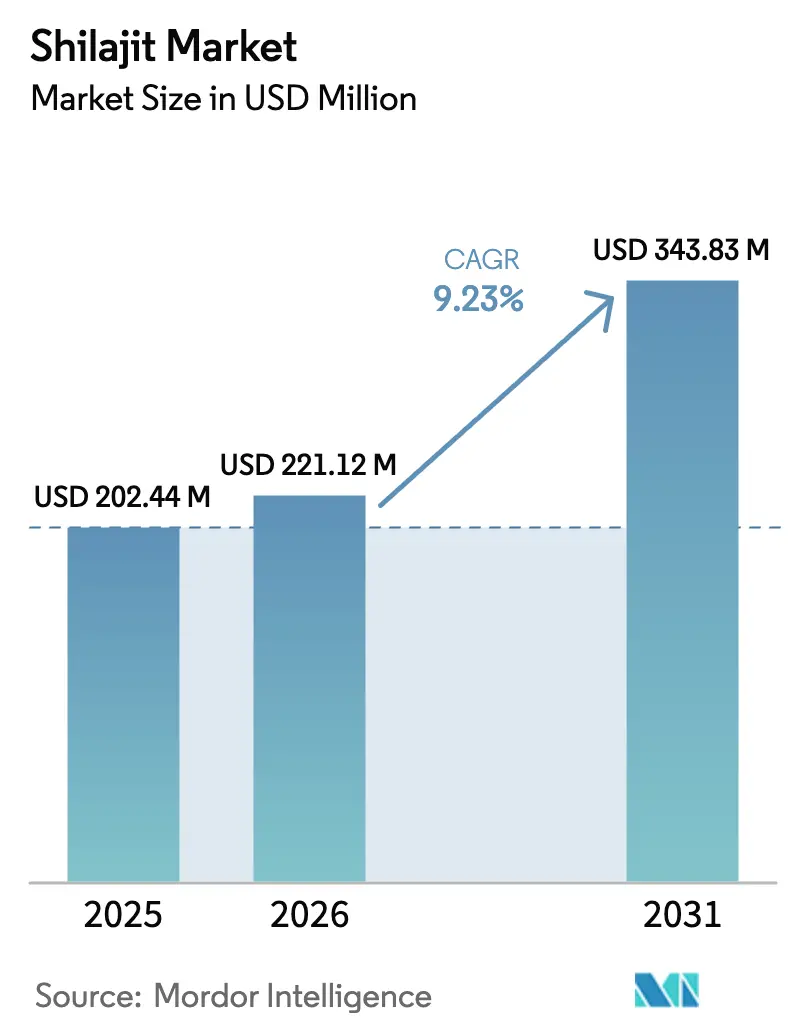

| Market Size (2026) | USD 221.12 Million |

| Market Size (2031) | USD 343.83 Million |

| Growth Rate (2026 - 2031) | 9.23% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Shilajit Market Analysis by Mordor Intelligence

The Shilajit Market is projected to grow significantly, increasing from USD 202.44 million in 2025 to USD 221.12 million in 2026 and reaching USD 343.83 million by 2031, with a CAGR of 9.13% during 2026-2031. This growth is fueled by rising demand for plant-based adaptogens, clearer regulatory frameworks for fulvic-acid-standardized formulas, and growing consumer interest in healthy aging. Heritage positioning continues to drive growth in the Asia-Pacific region, while clinical validation and clean-label claims are key factors influencing adoption in North America. Furthermore, innovations such as water-soluble powders and gummies have broadened the appeal of shilajit beyond its traditional resin form. Despite these advancements, the market faces quality-control challenges, highlighting the critical need for third-party testing and traceable sourcing to help brands secure a competitive advantage.

Key Report Takeaways

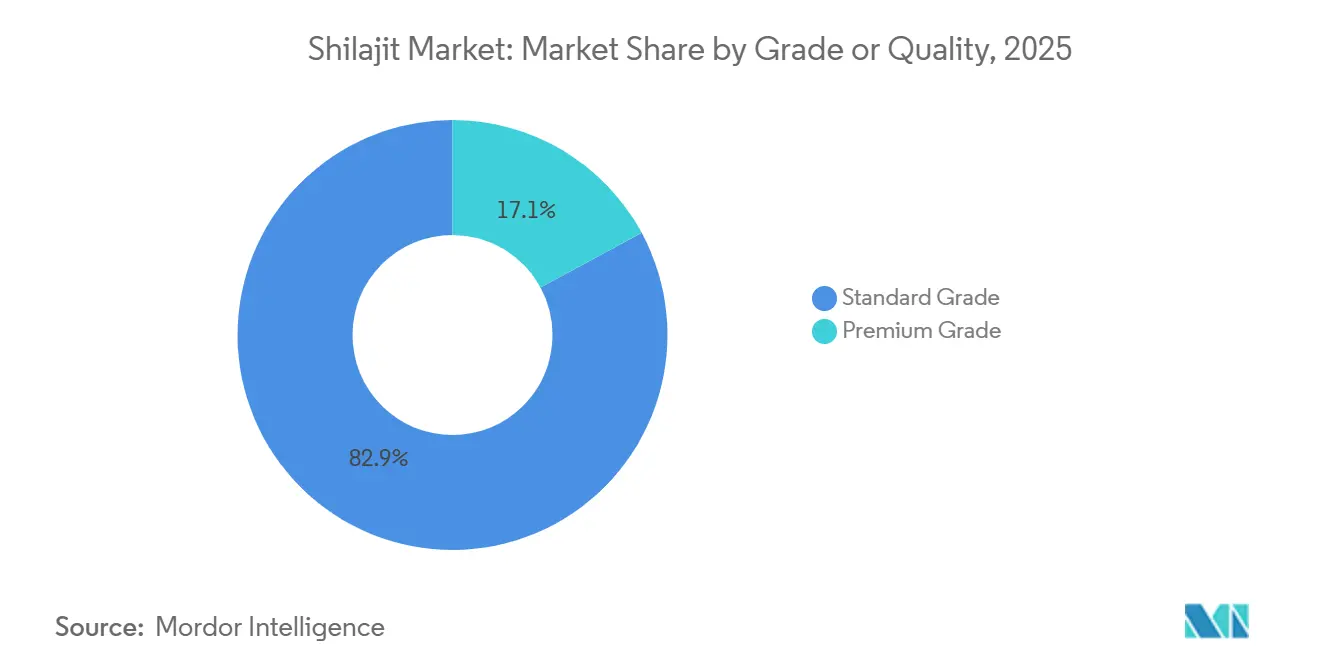

- By grade, Standard Grade held 45.32% of the Shilajit market share in 2025, while Premium Grade is on track to grow at a 9.51% CAGR through 2031.

- By form, resin advanced at a 10.56% CAGR between 2026 and 2031, outpacing capsules, which maintained 25.43% of the Shilajit market size in 2025.

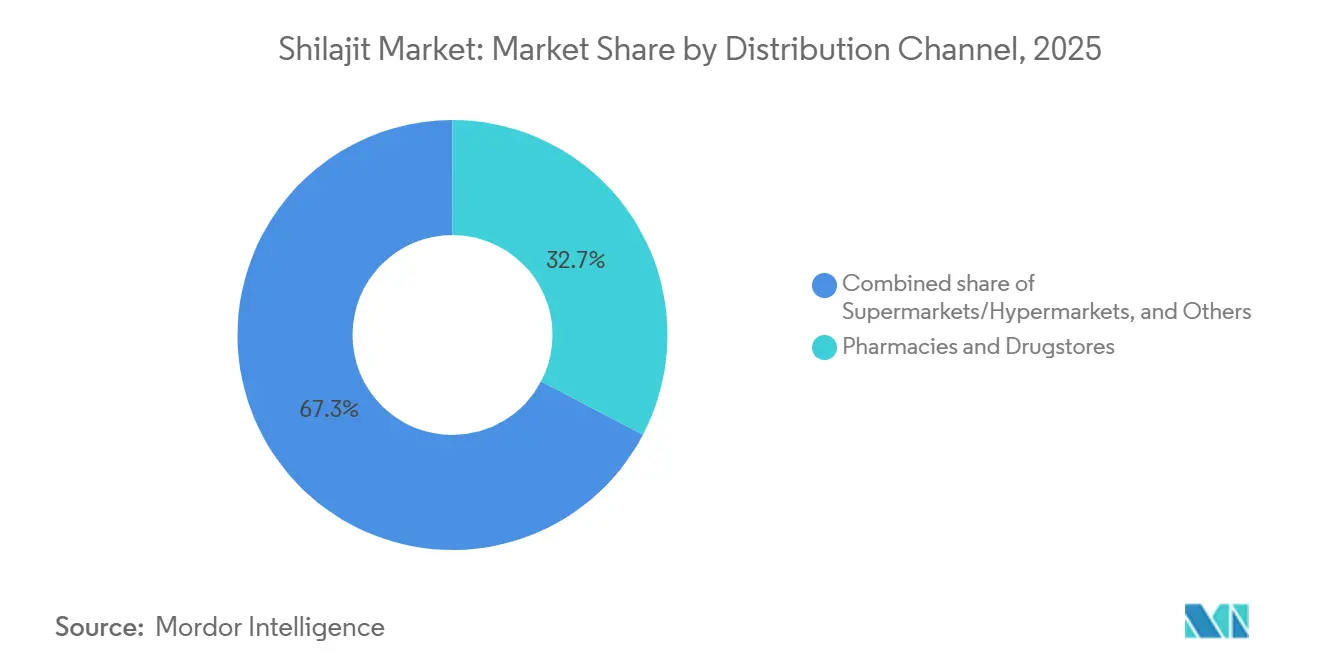

- By distribution channel, pharmacies commanded 32.67% revenue in 2025, but online retail is projected to rise at a 10.21% CAGR to 2031.

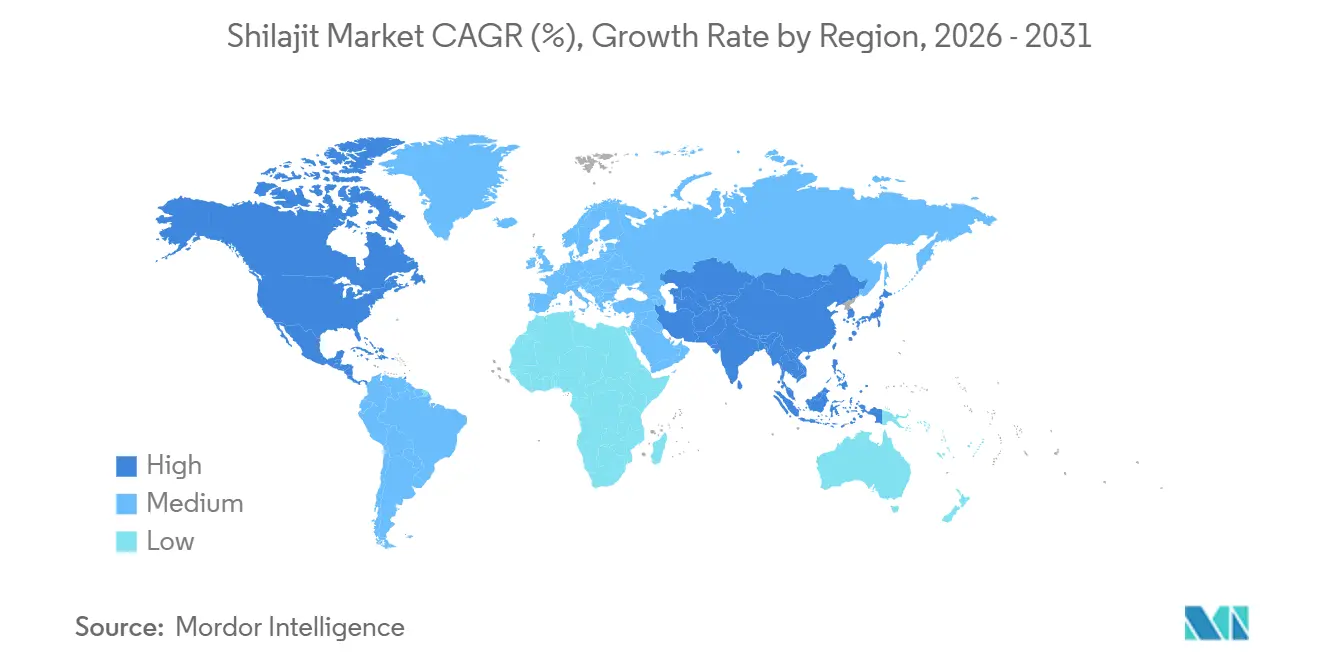

- By geography, Asia Pacific captured 61.02% revenue in 2025, yet Europe is projected to accelerate at 11.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shilajit Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of plant-based and vegan supplements positions Shilajit as a natural alternative | +1.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Innovation in product formulations and formats | +1.5% | Global, led by North America and Asia Pacific | Short term (≤ 2 years) |

| Social-media driven awareness in Gen-Z male wellness | +2.1% | North America, Europe, urban Asia Pacific | Short term (≤ 2 years) |

| Expansion of e-commerce channels | +1.9% | Global, accelerated in Asia Pacific and North America | Medium term (2-4 years) |

| Rising demand for clean-label, ethically sourced Himalayan resins | +1.2% | Europe, North America, urban India | Long term (≥ 4 years) |

| Surge in holistic wellness practices and yoga/Ayurveda adoption worldwide | +1.4% | Global, fastest in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing popularity of plant-based and vegan supplements positions Shilajit as a natural alternative

Plant-based supplements are transforming the wellness industry as consumers increasingly prioritize transparency in ingredient sourcing, manufacturing processes, and product authenticity. Shilajit, a mineral-pitch resin naturally formed over centuries from decomposed plant matter, has gained prominence as a preferred option for vegan and vegetarian diets, offering a plant-based alternative to animal-derived supplements like collagen or fish oil. Packed with fulvic acid, trace minerals, and antioxidants, Shilajit supports energy production, immune function, and overall health, delivering benefits comparable to synthetic multivitamins. Its Ayurvedic heritage further enhances its appeal in markets where traditional and "natural" remedies are highly valued and often command a premium price. However, ensuring product purity is crucial, as adulteration with fillers or synthetic fulvic acid can undermine consumer trust and compromise its clean-label promise. To address these challenges and differentiate in a competitive market, third-party testing and certifications such as USDA Organic or Non-GMO Project Verified are becoming indispensable for building consumer confidence and trust.

Innovation in product formulations and formats

Shilajit is gaining popularity through innovative formats like gummies, liquid drops, and functional beverages, appealing to Gen-Z's preference for convenience, taste, and compatibility with their specialty diets. In 2024, brands such as Blisque and Angel Gummies launched Shilajit-infused gummies, masking the resin's bitterness with natural sweeteners and fruit extracts, while Purblack introduced its Research Grade Shilajit Resin in October 2025, standardized to ≥60% fulvic acid and ≥50% dibenzo-α-pyrones, targeting biohackers and performance athletes. Combination formulations are also gaining traction: Shilajit paired with ashwagandha addresses stress and energy in a single SKU, while Shilajit-turmeric blends target inflammation and joint health. Natreon's PrimaVie—a clinically studied, patented Shilajit extract—has become the ingredient of choice for premium brands seeking to substantiate efficacy claims with human trials, a move that aligns with the European Food Safety Authority's stringent health-claim regulations under Regulation (EC) 1924/2006[1]Source: EUR-Lex, "European Union Food and Health Regulations", eur-lex.europa.eu. Advanced encapsulation technologies like liposomal and nanotechnology are improving bioavailability, though high costs limit their use to premium products. This evolution positions Shilajit as a versatile wellness platform, but brands must balance innovation with authenticity to retain traditional consumers who prefer resin as the authentic form.

Social-media driven awareness in Gen-Z male wellness

Shilajit, a once-obscure Ayurvedic resin, has gained significant traction as a wellness ingredient, thanks to TikTok and Instagram, particularly among Gen-Z males seeking natural testosterone support and cognitive benefits. Viral short-form videos demonstrating the resin dissolving in water, combined with testimonials highlighting its impact on energy and libido, have garnered millions of views and driven impulsive purchases. However, this rapid growth has also attracted counterfeit products and low-quality competitors. In 2024, the Philippine Food and Drug Administration issued a warning about unregistered Shilajit products sold online, emphasizing the challenges regulators face in keeping up with the fast-paced e-commerce environment[2]Source: FDA Philippines. "Philippine Food and Drug Administration Public Warnings", fda.gov.ph/. Gen-Z consumers, many of whom report experiencing anxiety or stress, prioritize transparency and actively research ingredient sourcing and third-party testing. This has created a divided market where premium brands that provide certificates of analysis and heavy-metal testing results build customer loyalty, while opaque sellers struggle with customer retention. The long-term success of Shilajit’s social-media-driven popularity depends on whether brands can convert viral interest into repeat purchases by demonstrating efficacy and fostering trust through measures like batch-level traceability and transparent practices.

Expansion of e-commerce channels

In 2024, e-commerce revolutionized the Shilajit market within the vitamins, minerals, and supplements category, driving significant growth on platforms like Amazon, where Shilajit products expanded across resin, capsule, and powder formats. Smaller brands, such as India-based ACTIZEET, leveraged this shift, reporting a 160% surge in online sales and reaching over 90,000 customers by late 2024 through Amazon and their own website. E-commerce enabled targeted marketing, with premium brands appealing to biohackers through high-fulvic-acid resin and value brands catering to price-sensitive consumers with standard-grade capsules. However, counterfeit and adulterated products flooded the market, exploiting consumers' difficulty in assessing quality. ConsumerLab's 2024 testing revealed a 32,000% variation in fulvic acid content across brands, with some products lacking active compounds. Regulatory frameworks, such as India's FSSAI requirements for seller license verification, remain inconsistently enforced, while cross-border sales from Nepal and Bhutan often evade scrutiny. Brands investing in direct-to-consumer models, subscription services, and educational content, like dosage guides and sourcing videos, can enhance customer lifetime value but must also address the gap in consumer education traditionally filled by pharmacists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit resin proliferation on online marketplaces | -1.6% | Global, most acute in North America and Europe e-commerce | Short term (≤ 2 years) |

| Adulteration and unregulated market players | -1.3% | Asia Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Raw material scarcity and geographic dependence | -0.9% | Global, supply concentrated in India, Nepal, Bhutan | Long term (≥ 4 years) |

| Heavy metal and mycotoxin contamination risks | -1.1% | Global, heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy metal and mycotoxin contamination risks

Regulatory agencies are intensifying their scrutiny of heavy metal levels in botanical supplements, spotlighting contamination concerns as a significant barrier to market growth. Recent studies have identified thallium concentrations of up to 0.5 µg/g in certain shilajit supplements. Extended exposure to these levels can lead to severe health repercussions, including potential neurological harm. The FDA's "Closer to Zero" initiative, designed to reduce heavy metals in food products, has introduced stringent enforcement benchmarks. Many manufacturers of shilajit grapple with consistent compliance. Research indicates that shilajit contains approximately 65 heavy metals, with dangerous ones like lead, arsenic, cadmium, and mercury present. Alarmingly, some of these metals exceed the permissible limits established by the WHO and the FDA. The contamination challenge is further complicated by geographic variability, as the quality of raw materials and their heavy metal profiles differ markedly across regions. This escalating regulatory scrutiny is pushing consolidation towards manufacturers with advanced testing capabilities and superior sourcing networks. Meanwhile, smaller players, often devoid of a robust quality control framework, encounter significant challenges.

Adulteration and unregulated market players

Counterfeit and adulterated shilajit products are eroding consumer trust and prompting regulatory pushback, stifling the growth of legitimate markets. Investigations show that a staggering 99% of shilajit sold through unauthorized channels is either substandard or outright fraudulent, often reduced to mere rice flour laced with minimal pharmaceutical traces. Testing by NOW Foods unveiled counterfeit supplements on Amazon, revealing a mix of white rice flour and sildenafil. This discovery ignited investigations by the FDA and spurred congressional inquiries into the oversight of e-commerce platforms. Online marketplaces are grappling with a severe adulteration issue, as their verification systems often falter against sophisticated counterfeits that closely resemble genuine product packaging and labeling. This dilemma fosters a negative feedback loop: as consumer skepticism grows, their willingness to pay premium prices for authentic products diminishes. Concurrently, legitimate manufacturers are burdened with heightened costs for anti-counterfeiting measures and quality verification systems. In response to these adulteration challenges, regulators are poised to enforce stricter accountability on platforms and impose heftier penalties on fraudulent sellers. Such measures, while aimed at curbing malpractices, could impose compliance costs that weigh heavily on smaller market players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade/Quality: Organic Certification Drives Premium Growth

In 2025, Standard Grade Shilajit captured a 45.32% market share, underscoring its stronghold in price-sensitive regions like India, Southeast Asia, and the Middle East. Here, consumers lean towards affordability over clinical validation. Typically, Standard-grade products, containing 20-30% fulvic acid and undergoing minimal purification, retail between USD 15-25 for a 30-day supply. In contrast, the Premium Grade is set to grow at a 9.51% CAGR through 2031. This surge is fueled by Western consumers and affluent urban Asians seeking standardized potency, heavy-metal testing, and clinical backing. Natreon's PrimaVie—a patented Shilajit extract boasting ≥60% fulvic acid and ≥50% dibenzo-α-pyrones—has emerged as the gold standard for premium formulations. Esteemed brands like Nootropics Depot and Purblack have integrated PrimaVie into their flagship offerings. Furthermore, PrimaVie's clinical trials, showcasing boosts in mitochondrial ATP production and exercise performance, align with the evidence premium consumers demand, meeting the European Food Safety Authority's health-claim standards under Regulation (EC) 1924/2006.

As counterfeit products proliferate, the premium segment's growth is a strategic countermeasure. By securing third-party certifications (like NSF, USP, and ISO 17025), ensuring transparent sourcing, and adopting tamper-evident packaging, premium brands carve out a niche that justifies prices 2-3 times higher than standard grades. Purblack's October 2025 debut of Research Grade Shilajit Resin, featuring batch-specific ICP-MS test results and GPS coordinates of collection sites, underscores this trust-centric strategy. Europe's expansion is notable, with the Traditional Herbal Medicinal Product (THR) pathway granting 178 registrations in the UK by 2024. North America mirrors this trend, as California's Proposition 65 lead limits (set at 0.5 micrograms per day) effectively necessitate premium-grade purification. While Standard grade will continue to lead in volume across Asia Pacific—thanks to Ayurvedic traditions and word-of-mouth endorsements—its market share is poised to dwindle. This shift is driven by rising incomes and heightened health awareness, steering consumers towards premium options.

By Form: Resin Authenticity Challenges Capsule Convenience

In 2025, capsules and tablets command a 25.43% market share, reaping benefits from standardized dosing, extended shelf life, and a consumer base familiar with these traditional supplement formats. Convenience plays a pivotal role in mainstream market penetration; capsule formats sidestep taste barriers and dosing uncertainties, challenges that resin formats grapple with. While powder forms cater to those desiring versatile consumption methods, the "Others" category showcases emerging formats like gummies and liquid concentrates, tailored to specific consumer tastes.

Resin forms, though holding a smaller market share, are witnessing the fastest growth at a 10.56% CAGR. This surge is fueled by authenticity-driven consumers gravitating towards minimally processed alternatives and traditional consumption methods. The upward trajectory of resin growth underscores a more discerning consumer base, one that values processing methods and bioavailability. Educated consumers are increasingly aware that resin forms boast higher concentrations of bioactive compounds than their processed counterparts. Yet, the journey isn't without hurdles; resin formats grapple with issues of adulteration and the challenge of quality verification. Many consumers find themselves at a disadvantage, lacking reliable methods to gauge authenticity without resorting to laboratory tests.

By Distribution Channel: E-commerce Disrupts Traditional Retail

In 2025, professional endorsements and a strong consumer trust in traditional healthcare avenues empower pharmacies and drugstores to capture a 32.67% market share. These established channels not only enhance the credibility of shilajit products but also provide consultations, advising consumers on appropriate usage and potential interactions. Supermarkets and hypermarkets, on the other hand, serve price-sensitive shoppers who prioritize convenience. Specialty health stores and direct-to-consumer platforms further diversify the retail landscape.

Online retail is witnessing a robust ascent, registering a commendable 10.21% CAGR. This growth underscores a significant shift in consumer buying habits, accelerated by digital advancements and a surge in e-commerce during the pandemic. The online boom is predominantly driven by a younger demographic, who are increasingly comfortable purchasing supplements digitally. However, this digital growth faces challenges, notably the proliferation of counterfeit products on major e-commerce platforms, raising quality control concerns. In response, genuine manufacturers are intensifying brand protection measures and enhancing consumer education. Moreover, the rise of online channels is facilitating direct-to-consumer strategies, which not only boost profit margins but also provide manufacturers with critical consumer insights, aiding in product development and marketing refinement.

Geography Analysis

In 2025, the Asia Pacific held a 61.02% market share, driven by India's role as the largest consumer and sourcing hub for Himalayan Shilajit. The Food Safety and Standards Authority of India's "Ayurveda Aahara" licensing category, introduced on September 1, 2025, reclassified Shilajit as a food supplement, enabling broader distribution through supermarkets and e-commerce. A National Sample Survey revealed that 96% of urban and 95% of rural respondents were aware of AYUSH systems, with nearly 50% spending at least INR 100 annually on AYUSH products[3]Source: Government of India. "Press Information Bureau - AYUSH Sector Growth", pib.gov.in. China is emerging as a key market, with traditional Chinese medicine practitioners incorporating Shilajit into kidney health formulations, though regulatory hurdles with the National Medical Products Administration persist. Japan's nascent market is growing as urban professionals seek nootropics and adaptogens like Shilajit to manage stress.

Europe is projected to grow at an 11.01% CAGR through 2031, driven by yoga's mainstreaming, Ayurveda's acceptance, and the Traditional Herbal Medicinal Product (THR) pathway, which enabled 178 registrations in the UK by 2024. Germany and the UK lead adoption, with consumers favoring certified organic, fair-trade Shilajit that meets EU heavy-metal limits under Regulation (EC) 1881/2006. The 2026 India-EU trade agreement reduced tariffs on Ayurvedic exports, allowing Indian brands like Dabur and Baidyanath to compete with European incumbents. Italy's market benefits from integrative medicine practitioners prescribing Shilajit, while France's BELFRIT list creates entry barriers but reduces competition for compliant products. Post-Brexit, the UK’s MHRA independently regulates herbal-medicine registrations, adding complexity for brands navigating dual compliance.

North America, led by the U.S. and Canada, is expanding as adaptogens and nootropics gain popularity. The U.S. FDA's DSHEA framework treats Shilajit as a supplement, lowering entry barriers but enabling counterfeit proliferation, while California's Proposition 65 lead limits favor premium-grade products. Canada’s NNHPD requires pre-market notification and safety evidence, slowing entry but enhancing trust. South America and the Middle East & Africa remain nascent markets, with growing interest in natural wellness solutions and e-commerce platforms like Mercado Libre and Jumia driving demand. Brazil’s ANVISA classifies Shilajit as a novel food requiring pre-market authorization, while the UAE’s Ministry of Health and Prevention has approved select products for pharmacy distribution in Dubai and Abu Dhabi.

Competitive Landscape

The shilajit market is highly fragmented, with the top five players holding only a small share, creating opportunities for consolidation and challenges for competition. This fragmentation stems from low entry barriers, diverse consumer preferences for quality and format, and the absence of dominant brands, unlike more established supplement categories. Companies with strong quality control and verified supply chains hold a competitive edge, particularly as regulatory scrutiny increases due to concerns over heavy metal contamination and product authenticity.

Strategic trends show a divide between heritage-based positioning by traditional Ayurvedic firms like Dabur and Baidyanath, which emphasize cultural authenticity, and newer players focusing on standardized formulations supported by clinical research. Innovation is evident in patent filings for nutraceutical compositions, particularly in combining shilajit with other botanicals to enhance safety and bioavailability, as noted by Justia Patents.

Leading manufacturers are leveraging technology, such as blockchain tracking and third-party testing, to ensure quality and differentiate their products from counterfeits. This fragmented market offers significant opportunities for companies to build trusted brands by maintaining consistent quality and educating consumers about shilajit's health benefits, especially when backed by scientific research. Collaborations with health professionals for endorsements can further enhance brand credibility and foster trust among consumers.

Shilajit Industry Leaders

-

Pürblack

-

Pure Himalayan Shilajit

-

Dabur

-

Baidyanath

-

Nootropics Depot

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dabur India launched its nutraceutical brand "Siens by Dabur," focusing on beauty, daily wellness, and gut health products, utilizing Japanese technology and marine collagen formulations. This strategic diversification represents Dabur's entry into the global nutraceuticals market beyond traditional Ayurvedic products, targeting science-backed ingredients to meet evolving consumer expectations.

- May 2025: Baidyanath introduced 27 nutraceutical products under the Siddhayu brand at Vitafoods Europe 2025, targeting men's and women's health, healthy aging, and kids' nutrition with scientifically backed ingredients.

- May 2025: Pharmavite celebrated the grand opening of its new USD 200 million gummy manufacturing facility in New Albany, Ohio, featuring a "Gummies Innovation Center of Excellence" for R&D of new gummy products.

- April 2025: Steadfast Nutrition launched SteadShilajit Gold, a multifunctional supplement featuring shilajit, 24K gold (Swarna Vark), and Ayurvedic herbs like ashwagandha. The product targets enhanced vitality, fatigue combat, and cognitive health with high fulvic acid concentration, available in over 500 retail stores and online platforms.

Global Shilajit Market Report Scope

Shilajit is a natural, mineral-rich substance that oozes from rocks in high mountain ranges, especially the Himalayas, formed over centuries from the decomposition of plant and microbial matter.

The Shilajit Market Report is Segmented by Grade/Quality into Standard Grade and Premium Grade. By Form into Resin, Capsules/Tablets, Powder, and Others. By Distribution Channel, the market is segmented into Supermarkets/Hypermarkets, Pharmacies and Drugstores, Online Retail, and Other Retail Distributors. By Geography (North America, Europe, Asia Pacific, South America, the Middle East, and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Standard Grade |

| Premium Grade |

| Resin |

| Capsules/Tablets |

| Powder |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies and Drugstores |

| Online Retail |

| Other Retail Distributors |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Grade/Quality | Standard Grade | |

| Premium Grade | ||

| By Form | Resin | |

| Capsules/Tablets | ||

| Powder | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies and Drugstores | ||

| Online Retail | ||

| Other Retail Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for Shilajit through 2031?

The category is projected to grow at 9.23% annually from 2026-2031.

Which region currently leads demand?

Asia Pacific captured 61.02% revenue in 2025, driven by India’s domestic appetite.

Why are consumers shifting to resin over capsules?

Social-media demonstrations of resin purity and “clean-label” preferences are driving a 10.56% CAGR for the format.

What channel is expanding fastest?

Online retail is advancing at a 10.21% CAGR due to Amazon and TikTok Shop adoption.

Page last updated on: