Vodka Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 38.44 Billion |

| Market Size (2031) | USD 47.89 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

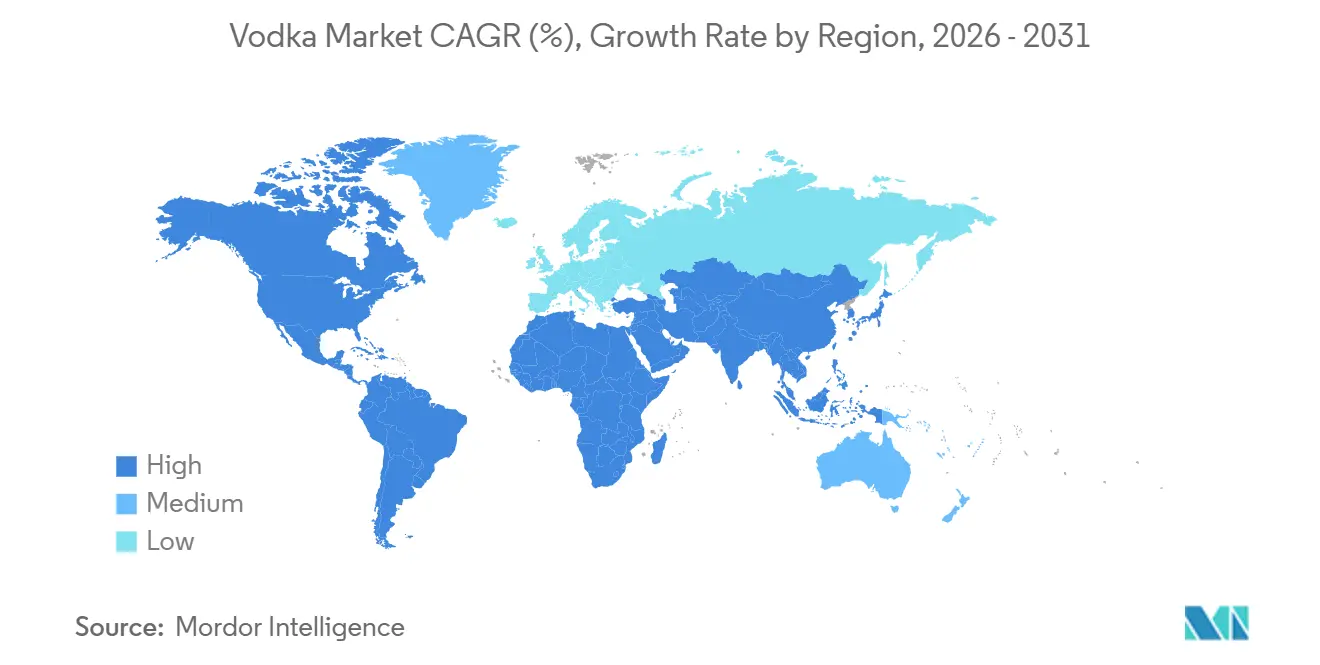

| Fastest Growing Market | South America |

| Largest Market | Europe |

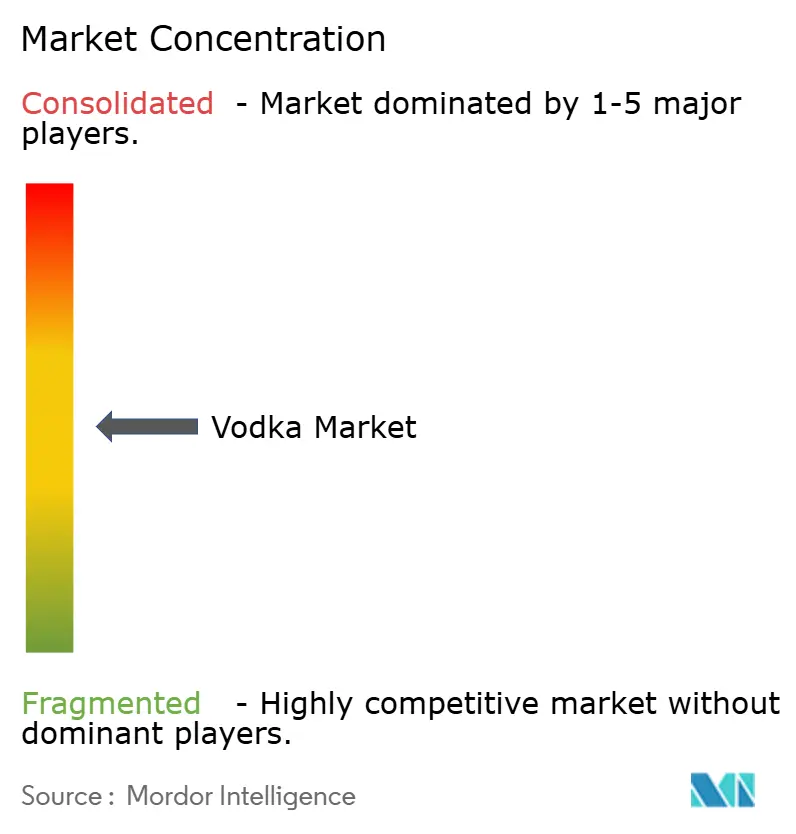

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vodka Market Analysis by Mordor Intelligence

The Vodka Market size is expected to grow from USD 36.78 billion in 2025 to USD 38.44 billion in 2026 and is forecast to reach USD 47.89 billion by 2031 at 4.49% CAGR over 2026-2031. Europe led the market in 2025, contributing 42.74% of the global value. However, demand is gradually shifting toward South America and parts of Asia-Pacific, fueled by the growing cocktail culture, urban tourism, and rising disposable incomes, which are driving the popularity of premium brands. Premiumization has become a critical factor in ensuring margin stability across major regions, as younger consumers increasingly prioritize authenticity, provenance, and sustainability in their purchasing decisions. While off-trade retail continues to dominate in terms of volume, the recovery of on-trade channels and the rising demand for ready-to-drink cocktails are reviving experiential consumption occasions that were disrupted during the pandemic. Meanwhile, regulatory differences, such as Ireland's cancer-warning labels and Scotland's higher minimum unit pricing, are creating margin pressures. These challenges favor producers with economies of scale and flexible compliance systems. In this dynamic market, maintaining a diverse portfolio and a strong omnichannel presence is essential for sustaining competitive resilience.

Key Report Takeaways

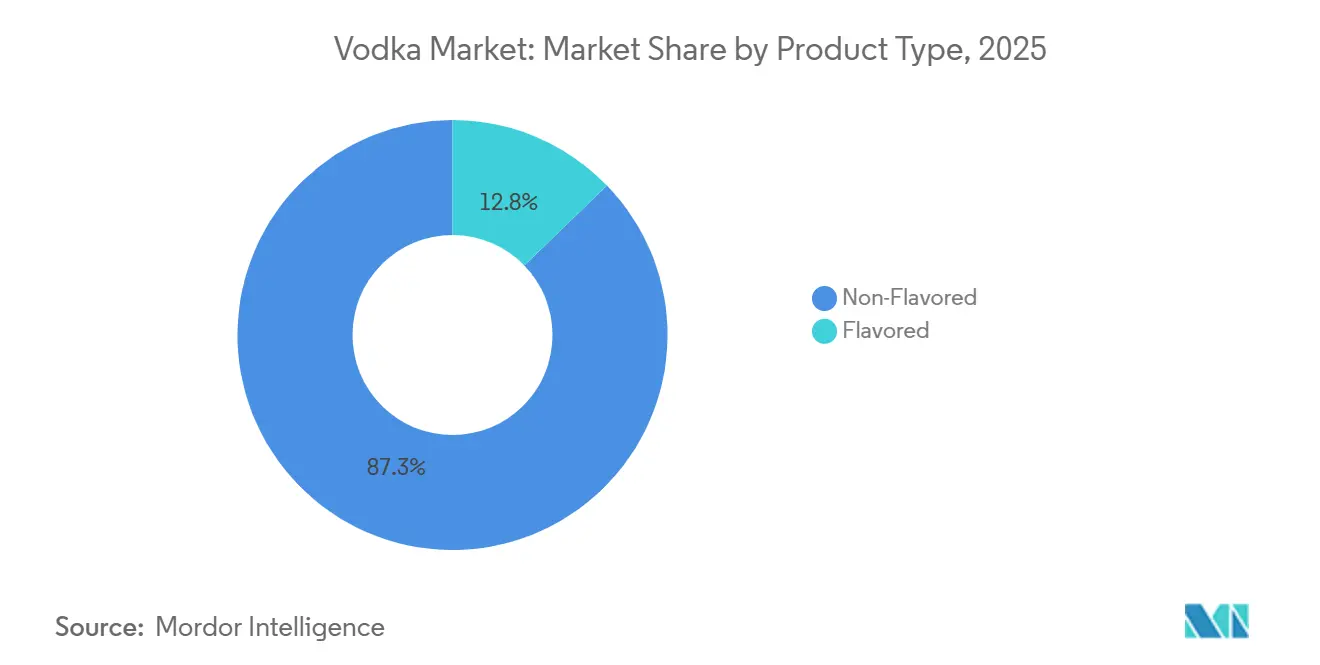

- By product type, non-flavored vodka held 87.25% share in 2025, while flavored offerings are projected to expand at a 5.64% CAGR to 2031.

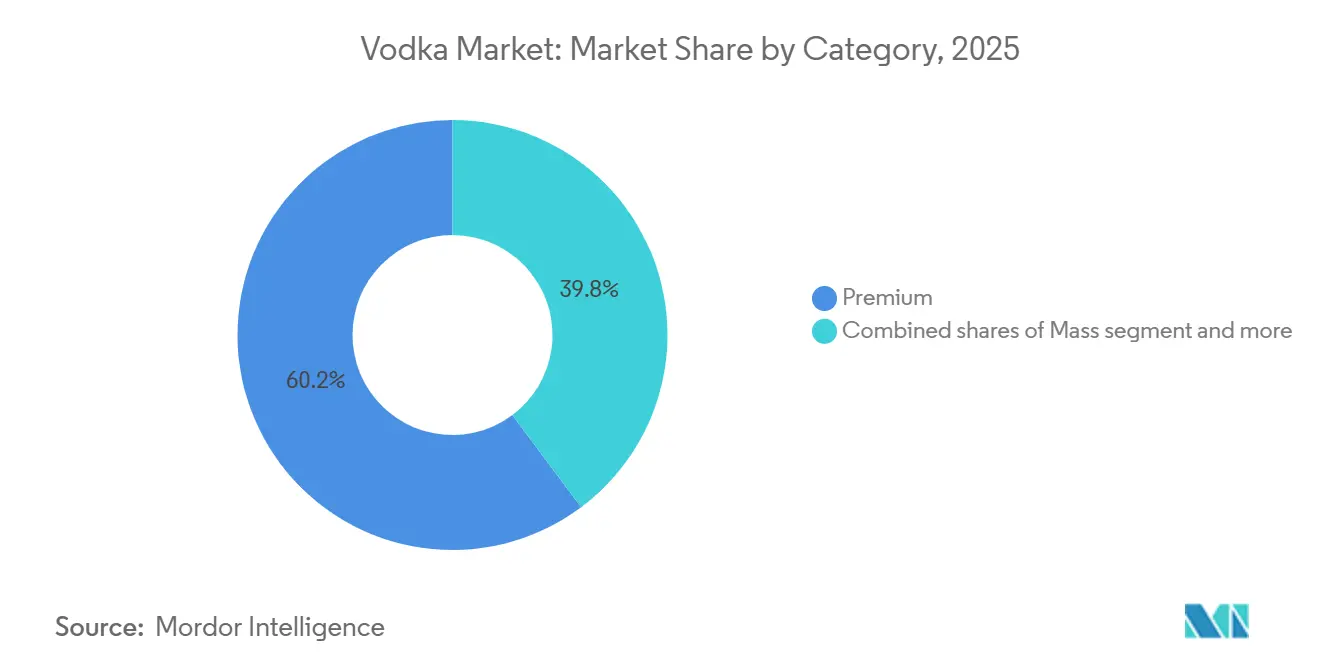

- By category, premium vodka captured 60.21% of sales in 2025, and the super-premium tier is advancing at a 5.74% CAGR through 2031.

- By end user, men accounted for 67.54% of 2025 consumption, whereas women are the fastest-growing segment at a 5.98% CAGR.

- By distribution channel, off-trade outlets delivered 83.54% of volume in 2025, but on-trade venues are rebounding at a 5.66% CAGR.

- By geography, Europe led with 42.74% share in 2025, while South America is forecast to post a 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vodka Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for premium and craft vodkas | +1.2% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising popularity of vodka-based cocktails | +0.9% | Global, particularly North America, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Innovation in flavor and ingredients | +0.8% | North America, Europe, select Asia-Pacific cities (Singapore, Tokyo, Shanghai) | Medium term (2-4 years) |

| Growing tourism and hospitality sector | +0.6% | South America, Middle East and Africa, Asia-Pacific resort destinations | Long term (≥ 4 years) |

| Strategic expansion by pub and bar chains | +0.5% | North America, Europe, urban India and China | Medium term (2-4 years) |

| Sustainability and ethical sourcing | +0.4% | Western Europe, North America, Australia/New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for premium and craft vodkas

Premiumization is transforming value pools as consumers increasingly opt for artisanal and small-batch products that prioritize provenance, distillation techniques, and packaging aesthetics. In 2024, the American Craft Spirits Association recorded sales of 12.7 million 9-liter cases of craft spirits[1]Source: American Craft Spirits Association, "Craft Spirits Sales See Second Year of Decline", americancraftspirits.org . However, this represented a 6.1% year-over-year decline, driven by distribution challenges and capital shortages among smaller producers. Despite this, the contraction has strengthened the position of surviving players: craft distilleries with omnichannel distribution and premium shelf placements captured a larger market share. Direct-to-consumer sales at tasting rooms also contributed significantly to small-craft volumes. Multinational brands have responded to these shifts by introducing super-premium line extensions. For example, Belvedere launched Heritage 176 in September 2024 and Belvedere 10 in July 2024 to protect their high-margin segments from independent competitors. The increasing demand for craft and premium products is pressuring mid-market volume brands, leading to portfolio rationalizations and mergers and acquisitions as companies seek scale economies to mitigate declining per-unit margins.

Rising popularity of vodka-based cocktails

As younger demographics increasingly view mixed drinks as both social currency and experiential moments, cocktail culture is driving more frequent consumption. With fruity and sweet flavor profiles topping consumer preferences, vodka is finding relevance not just in late-night venues but also during happy hours and home mixology. This shift is fueling a 5.66% CAGR forecast for on-trade channels. Bars and restaurants are leveraging signature vodka cocktails to set their menus apart and justify premium pricing. Responding to this trend, ready-to-drink formats are on the rise. For instance, Blake Lively's Betty Booze rolled out its inaugural vodka RTDs in June 2025, and in April 2025, Absolut, in collaboration with Coca-Cola Europacific Partners, debuted Absolut Vodka and SPRITE Watermelon, which garnered an impressive 84% purchase intent in consumer tests. The blend of cocktail culture with convenient formats is driving growth from two fronts: on-premise venues are reaping the rewards of experiential premiums, while off-trade RTD sales are capitalizing on the trend of replicating bar-quality drinks at home.

Innovation in flavor and ingredients

With neutral vodka becoming increasingly commoditized, flavor innovation has taken center stage as the primary differentiator. Producers introduced a series of bold variants between 2024 and 2025: Smirnoff launched Spicy Tamarind in January 2024, Stoli unveiled Halapeño Pepper in January 2026 targeting the Bloody Mary market, and Skyy released Infusions Pineapple in November 2024. These launches align with Bacardi's findings that fruity and adventurous flavors appeal to Gen Z and millennial consumers, who prioritize Instagram-worthy aesthetics and unique taste experiences. Additionally, ingredient transparency and botanical infusions are gaining momentum. Reflecting this trend, Ketel One introduced Botanical Peach and Orange Blossom in February 2024, while Absolut launched Extrakt in June 2024, both emphasizing natural extracts and lower-calorie options. Although the flavored segment's 5.64% CAGR highlights the rapid pace of innovation, it also results in fragmented shelf space and inventory management challenges for retailers. This creates an opportunity for brands skilled in SKU rationalization and data-driven assortment planning.

Growing tourism and hospitality sector

The recovery of tourism post-pandemic has revitalized on-premise spirits consumption, particularly in resort destinations and urban centers where international travelers seek premium beverage experiences. According to UN Tourism, 2025 recorded 1.52 billion international tourists globally, an increase of nearly 60 million compared to 2024[2]Source: UN Tourism, "World Tourism Barometer", untourism.int. South America, with a 7.02% CAGR, attributes part of its growth to the expansion of hospitality infrastructure in Brazil and Argentina. In these countries, a growing middle class and increased inbound tourism are driving higher spirits penetration. In the Middle East, despite regional alcohol restrictions, the UAE is experiencing rising vodka demand in hotel bars and licensed venues catering to expatriates and tourists. On-premise venues are not only significant for volume but also serve as key platforms for brand building. They provide consumers with opportunities to sample premium spirits before purchasing them in off-trade channels. Multinational producers capitalize on this trend through targeted activations and bartender education programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -0.7% | Global, with acute impact in Europe (Ireland, Scotland), select Asia-Pacific markets (India tariffs) | Short term (≤ 2 years) |

| Consumer inclination toward healthy beverages | -0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Health issues over excessive consumption | -0.3% | Global, with emphasis in high per-capita markets (Russia, Poland, Nordics) | Long term (≥ 4 years) |

| Growing demand for low-alcohol products | -0.4% | Western Europe, North America, Australia/New Zealand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations limit the market

Smaller producers, often lacking the necessary legal and lobbying resources, face significant challenges in market expansion due to regulatory complexities and increasing compliance costs. Ireland's Public Health Alcohol Act, which will take effect in May 2026, mandates cancer warning labels on all alcohol products. This regulation not only sets a potential benchmark for other regions but also forces producers to redesign packaging and manage inventory adjustments. In Scotland, the increase in minimum unit pricing to 65 pence in September 2024 will raise retail prices, reducing demand elasticity among price-sensitive consumers. A 2025 report from the World Health Organization revealed that 167 countries impose excise taxes on spirits, with a median rate of 22.5% of the retail price. However, only 23% of these jurisdictions adjust taxes to account for inflation, resulting in unpredictable cost changes when governments revise rates. These overlapping regulations place a disproportionate burden on craft distilleries. Without the infrastructure to handle compliance or the scale to absorb these costs, many smaller players are exiting the market or being acquired by larger companies, driving rapid consolidation in the industry.

Health issues over excessive consumption

Public health campaigns and medical research increasingly associate excessive alcohol consumption with chronic diseases, steadily reducing the social acceptability of heavy drinking, particularly in high per-capita consumption markets. A 2024 report from the World Health Organization (WHO) highlights the severity of the issue, linking 2.6 million annual deaths to alcohol consumption[3]Source: World Health Organization (WHO), "Over 3 million annual deaths due to alcohol and drug use", who.int. In Russia and Poland, where average monthly vodka consumption is 17 and 14 shots, respectively, significant public health challenges could prompt stricter policy measures. These may include advertising restrictions, limited retail hours, or increased excise taxes. The long-term effects, spanning four years or more, reflect the slow pace of behavioral shifts and policy implementation. However, the trend is evident: governments are prioritizing harm reduction over industry expansion. Producers must adapt by investing in responsible-drinking campaigns and developing innovative products (such as lower-ABV options and smaller packaging) to mitigate the risk of punitive regulations. Failure to self-regulate could lead to tobacco-style restrictions, including plain packaging and point-of-sale display bans, which would severely impact brand equity and promotional strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavor Innovation Drives Differentiation

In 2025, non-flavored offerings held a dominant 87.25% share of the vodka market. Bartenders and traditional consumers heavily relied on these neutral spirits for their core cocktail creations. While stable demand supports volume, value growth trails behind category averages due to increased promotional activities and the growing presence of private-label brands. Regulatory definitions, requiring a minimum 37.5% ABV, play a vital role in preserving the traditional vodka segment's identity, ensuring a clear distinction from newer flavored variants. Incumbent players benefit from supply efficiencies: large-volume distilleries utilize continuous stills and multi-region bottling to achieve consistent taste at lower costs, helping them maintain a strong presence on grocery and convenience store shelves.

Flavored variants are projected to drive the vodka market's growth at a 5.64% CAGR through 2031. This expansion is driven by social media-friendly launches that emphasize novelty and visual appeal. Younger consumers, who view spirits as a medium for self-expression, are drawn to spicy, botanical, and dessert-inspired profiles. Additionally, ready-to-drink variations are increasing flavor acceptance, positioning vodka as a versatile choice for any occasion. However, retailers remain cautious, requiring proof of sales velocity before allocating shelf space. This scrutiny encourages producers to refine their offerings, focusing on standout flavors that can sustain consistent demand throughout the year. Brands that skillfully balance innovation with a selective approach to their product range are well-positioned to secure premium shelf placements and protect their profit margins.

By End User: Women Reshape Consumption Patterns

In 2025, men represented 67.54% of the global volume, attracted to heritage cues and value pricing, especially in Eastern Europe and parts of Latin America. Mature male segments are increasingly opting for whisky and craft beer, diverting market share from mainstream vodka labels, while younger men are showing a preference for experiential brands in brown spirits. As gender norms evolve and purchasing power diversifies, marketing strategies rooted in traditional masculinity tropes risk becoming outdated.

Conversely, women are actively contributing to the growth of the vodka market. They are driving expansion in higher-margin flavored and ready-to-drink (RTD) sub-categories, which are growing at a strong 5.98% CAGR. Current product development focuses on zero-sugar claims, convenient single-serve formats, and visually appealing labels designed for social media sharing. Retail strategies are also evolving: research shows that female shoppers are more likely to respond to chilled displays near store entrances, prompting adjustments in modern trade merchandising. Additionally, effective branding now positions women as confident tastemakers, ensuring they are recognized as primary audiences and reinforcing brand relevance throughout the purchasing journey.

By Category: Super-Premium Captures Margin Expansion

In 2025, premium expressions led sales, accounting for 60.21% of the market. This segment not only anchored the vodka market's volume but also managed cost inflation effectively through measured price increases. Mainstream premium brands rely on extensive distribution and consistent flavor to build brand loyalty, while craft producers highlight local stories to support their pricing. However, with growth slowing in mature markets, brands face heightened shelf competition. If mid-range SKUs fail to revitalize their branding, they risk merging indistinctly with other tiers.

Super-premium labels are expected to outperform all other tiers, with a projected 5.74% CAGR. Their growth is driven by gifting occasions, a recovery in travel retail, and connoisseurs seeking exclusive editions. These labels benefit from higher gross margins, which help mitigate commodity price fluctuations and compensate for volume declines in other segments. To sustain growth, producers focus on storytelling that emphasizes terroir, grain types, and artisanal techniques, creating a luxury appeal for affluent urban consumers. However, inflation may push some consumers toward the core premium segment, highlighting the importance of diversified portfolios that address evolving consumer trading behaviors in the vodka market.

By Distribution Channel: Off-Trade Dominance Meets On-Premise Revival

In 2025, off-trade outlets represented 83.54% of the volume, influenced by shifting home mixology trends, increased price sensitivity, and growing e-commerce adoption. Large liquor chains and specialized stores, equipped with knowledgeable staff and extensive assortments, are capitalizing on these changes, often steering consumers toward premium options. The digital landscape is advancing rapidly: collaborations like Au Vodka’s partnership with Huboo are reducing delivery times and expanding geographic coverage. However, regulatory barriers in the U.S. – particularly those restricting interstate direct-to-consumer spirits shipping – continue to limit the broader potential of the online market, maintaining the importance of brick-and-mortar stores.

On-trade channels, anticipated to grow at a 5.66% CAGR, are regaining their social importance as bars, clubs, and festival venues resume operations at scale. Signature serves and theatrical bartending enhance perceived value, often supporting price premiums that mitigate inflationary pressures. While chain pubs bring operational efficiency to cocktail rollouts, independent bars leverage local craft collaborations to deliver authenticity. By implementing balanced channel strategies and utilizing data across multiple touchpoints, producers can effectively track consumer journeys and tailor promotions, maximizing their share of the vodka market across various retail formats.

Geography Analysis

In 2025, Europe captured 42.74% of global sales, supported by strong cultural consumption in Russia, Poland, and the Nordic region, despite tightening regulations that are compressing margins. Western European consumers are shifting towards premium and craft options, prioritizing quality over quantity. However, health-conscious trends are limiting overall growth. The European Union's strict definition and labeling standards ensure product authenticity but restrict innovation, particularly for beverages below the 37.5% ABV threshold. This creates obstacles for developing lighter drinks. Consequently, market players are focusing on storytelling, especially around provenance and sustainability, to stay relevant while adhering to legal requirements.

South America is experiencing rapid growth, with a projected 7.02% CAGR through 2031. This growth is driven by a recovery in tourism, increased investments in nightlife, and the expansion of the middle class. Brazil and Argentina are leading the demand, with urban areas increasingly adopting global cocktail trends. However, challenges such as import tariffs and complex tax systems persist. Producers are addressing these issues by partnering with local distributors, customizing marketing strategies to suit regional preferences, and introducing ready-to-drink formats that align with outdoor social customs.

North America remains the largest single-country market by value, led by the United States. Here, premium and super-premium products are offsetting declines in mid-tier sales. While e-commerce liberalization in some states is breaking down traditional distribution barriers, inconsistencies in interstate regulations are driving up segmentation costs. The Asia-Pacific region offers diverse opportunities: In India, a tariff reduction under a trade agreement with the U.K. is expected to cut landed costs for imported vodka by 50%, expanding consumer access. Meanwhile, although baijiu dominates the market, China's urban centers are fostering cocktail experimentation. In the Middle East and Africa, growth is still in its early stages. The UAE and South Africa, both popular tourist destinations, are seeing increased demand, particularly from expatriates, despite stricter alcohol regulations. Understanding local cultures and forming strategic partnerships are essential for successful vodka market penetration.

Competitive Landscape

The vodka market is moderately fragmented. Major players scale advantages in sourcing, multi-channel distribution, and marketing spend. The major players in the vodka industry, including Diageo PLC, Pernod Ricard S.A., LVMH Moët Hennessy Louis Vuitton, Bacardi Ltd, and Radico Khaitan Ltd., collectively drive industry innovation and market development. Their distribution breadth mitigates localized compliance shocks and ensures prime back-bar placements. Sazerac's 2024 acquisition of Stoli Group signaled a strategic effort to streamline its portfolio, focusing on mid-tier offerings and achieving cost synergies. Despite this consolidation, approximately 2,282 active craft distilleries in the U.S. continue to drive innovation, prompting legacy giants to accelerate flavor cycles.

Flavor and format innovations are key drivers of current competition. Belvedere's lower-ABV Dirty Brew and Stoli's Halapeño Pepper highlight how established brands strengthen loyalty through limited-time releases and seasonal bundles. At the same time, private-label growth in supermarket chains pressures branded suppliers to justify price premiums through experiential marketing, ESG initiatives, and enhanced product quality.

Technology adoption prioritizes market routes and authenticity assurance over production overhauls. Blockchain provenance pilots in boutique distilleries and data-driven merchandising tools in multinational portfolios share the goal of building consumer trust and optimizing channel performance. Companies that combine compliance agility, omnichannel visibility, and compelling storytelling will gain a competitive edge in the evolving vodka market.

Vodka Industry Leaders

-

Diageo PLC

-

LVMH Moët Hennessy Louis Vuitton

-

Pernod Ricard S.A

-

Bacardi Ltd.

-

Radico Khaitan Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Absolut Vodka has collaborated with TABASCO Brand to introduce 'Absolut TABASCO', a spicy creation that combines Absolut's smooth winter-wheat vodka with the bold flavor of fermented, aged red pepper mash.

- May 2025: Piccadily Agro Industries has unveiled 'Cashmir', marking India's debut in the realm of small-batch luxury vodka. Crafted from heritage organic winter wheat and pristine glacial water, 'Cashmir' draws its essence from the picturesque Kashmir Valley.

- February 2025: Sazerac Company completed acquisition of SVEDKA vodka brand from Constellation Brands, marking significant consolidation in the premium vodka segment as distributors seek portfolio diversification to address changing consumer preferences and market dynamics.

- February 2025: ZigZag Vodka has officially launched in Bangalore, marking its entry into one of India's most dynamic markets. Renowned for its exceptionally smooth, clear, and crisp vodka, the brand aims to revolutionize Bangalore's thriving nightlife scene. With a commitment to excellence in vodka craftsmanship

Global Vodka Market Report Scope

Vodka is a clear, alcoholic beverage made most commonly from grains, such as rye, rice, wheat, and vegetables like corn and potatoes. However, modern distilleries have started experimenting with fruits like grapes and apples to produce the spirit. The global vodka market is segmented by product type, category, distribution channel, and geography. By product type, the market is segmented into flavored and non-flavored. Based on category, the market is segmented into mass, premium, and super-premium. Based on the distribution channel, the market studied is segmented into on-trade and off-trade. By off-trade, the market is further segmented into supermarkets/hypermarkets, specialty stores, online retailers, and other distribution channels. The report analyzes emerging and established economies worldwide, comprising North America, Europe, South America, Asia-Pacific, Middle-East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Flavored |

| Non-Flavored |

| Men |

| Women |

| Mass |

| Premium |

| Super Premium |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Flavored | |

| Non-Flavored | ||

| By End User | Men | |

| Women | ||

| By Category | Mass | |

| Premium | ||

| Super Premium | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the vodka market expected to be by 2031?

The vodka market is projected to reach USD 47.89 billion by 2031, advancing at a 4.49% CAGR from 2026 to 2031.

Which product type is growing fastest within global vodka sales?

Flavored variants are forecast to grow at 5.64% CAGR through 2031, driven by bold taste innovation and ready-to-drink formats.

What region offers the highest growth outlook for vodka brands?

South America leads with a 7.02% CAGR, benefiting from hospitality expansion and growing middle-class spending power.

Why are super-premium vodkas gaining traction?

Affluent consumers seek provenance, limited editions, and gifting appeal, pushing super-premium labels to a 5.74% CAGR.

Page last updated on: