Pasta Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 59.44 Billion |

| Market Size (2031) | USD 75.66 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

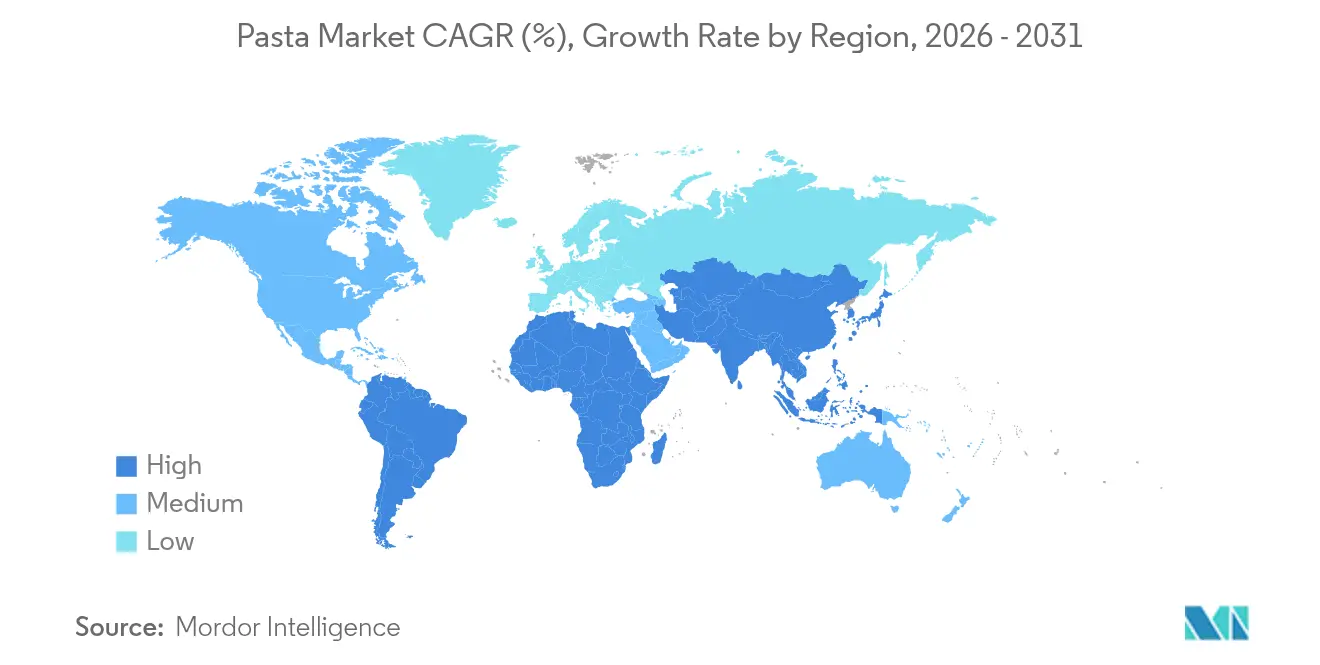

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

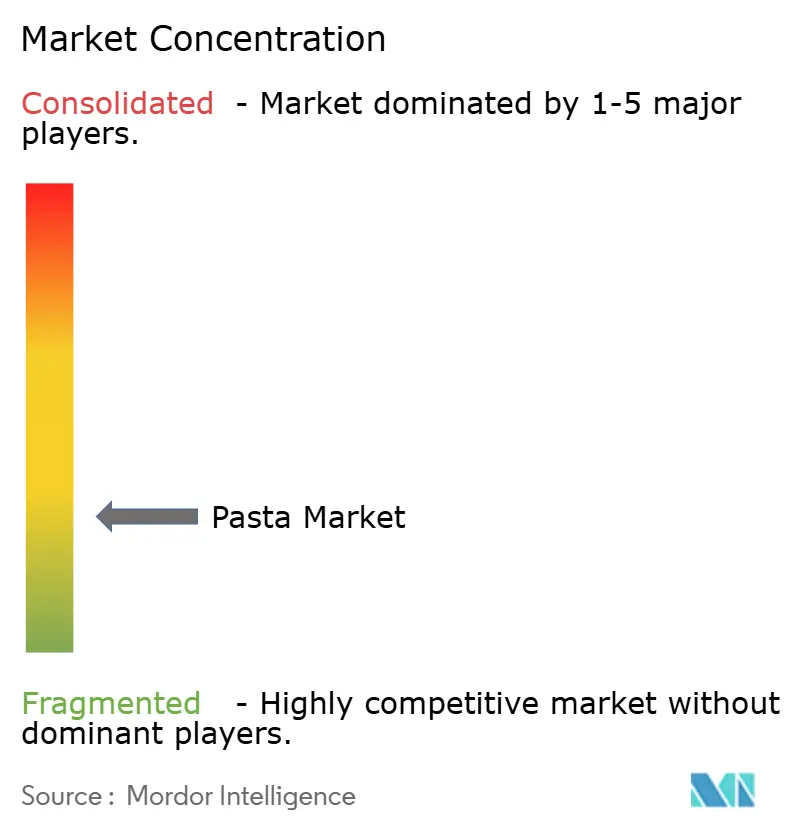

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pasta Market Analysis by Mordor Intelligence

The pasta market size was valued at USD 56.26 billion in 2025 and estimated to grow from USD 59.44 billion in 2026 to reach USD 75.66 billion by 2031, at a CAGR of 4.94% during the forecast period (2026-2031). Consumer demands for convenience, health-conscious formulations, and sustainable production fuel this growth. Pasta's global appeal stems from its affordability, versatility, and adaptability to diverse dietary and cultural preferences. Europe, bolstered by Italy's robust production and export capabilities, leads the market. In contrast, the Asia-Pacific region emerges as the fastest-growing, spurred by urbanization, westernized diets, and increasing disposable incomes. While dried pasta remains the dominant choice, fresh and chilled varieties are gaining popularity, driven by a surge in demand for artisanal and gourmet offerings. Health trends are propelling the growth of free-from and specialty products, with innovations like 3D printing enabling customized pasta shapes. Retail channels dominate distribution, but foodservice is witnessing a robust post-pandemic resurgence. Traditional cardboard packaging still reigns, yet there's a notable shift towards flexible and sustainable formats, prized for their portion control and eco-friendliness.

Key Report Takeaways

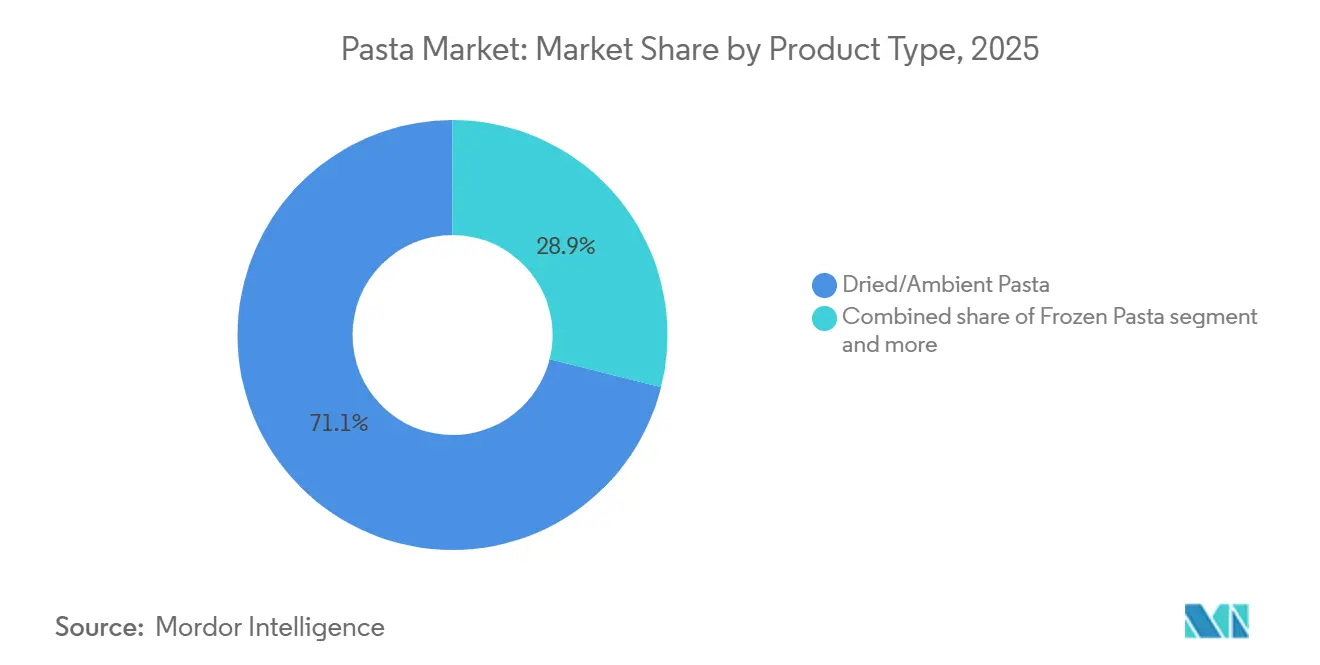

- By product type, dried pasta led with 71.09% of pasta market share in 2025, while frozen pasta is projected to expand at a 7.48% CAGR through 2031.

- By category, conventional offerings captured 90.66% revenue share in 2025; free-form pasta is forecast to grow at a 7.38% CAGR through 2031.

- By filling, plain pasta accounted for 89.66% of the pasta market size in 2025, whereas stuffed/filled variants are advancing at an 7.00% CAGR through 2031.

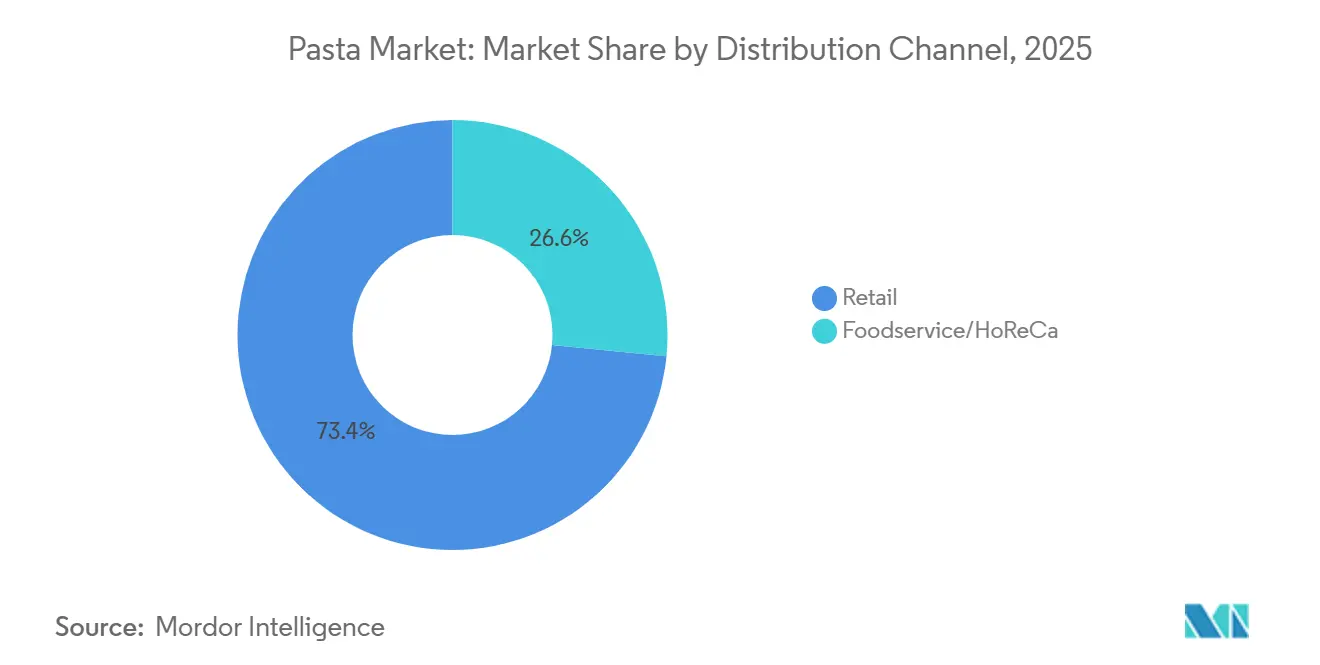

- By distribution channel, retail commanded 73.42% of pasta market share in 2025 and shows the fastest growth with a 5.24% CAGR through 2031.

- By geography, Europe held a 45.84% share of the pasta market size in 2025, while Asia-Pacific is on course for a 7.35% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pasta Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for convenient ready-to-cook options | +1.2% | Global, with strongest adoption in North America and Asia-Pacific | Medium term (2–4 years) |

| Rising demand for functional and health-oriented pasta | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Revitalization of foodservice channels | +0.8% | Global, led by North America and Europe recovery | Short term (≤ 2 years) |

| Emergence of 3d printing for premium pasta customization | +0.3% | Europe and North America, niche premium segments | Long term (≥ 4 years) |

| Sustainability-driven innovation in pasta production | +0.4% | Europe and North America, regulatory compliance focus | Medium term (2–4 years) |

| Surging popularity of ethnic and globally inspired flavors | +0.5% | Global, with Asia-Pacific leading fusion trends | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Convenient Ready-to-Cook Options

Manufacturers are reshaping their priorities, product designs, and retail strategies in response to the rising demand for convenience-driven pasta consumption. As urban lifestyles grow more time-constrained, manufacturers are focusing on quick-prep pasta formats that don't compromise on quality or nutrition. Barilla's Ready Pasta, for instance, offers fully cooked pasta in microwavable pouches, ready in just 60 seconds. Similarly, Primi Pasta employs rapid hydration technology, achieving an al dente texture in a mere 3 minutes. Packaging strategies are also evolving, with increased demand for microwavable, portion-controlled, and shelf-stable formats appealing to single-person households and busy professionals. Structural changes, like increased workforce participation and the rise of smaller households, further amplify this trend. According to the United Nations, in 2024, over 57% of the global population resided in urban areas, with projections suggesting this will surpass 60% by 2030 [1]Source: United Nations, “World Urbanization Prospects 2024,” un.org. Moreover, the International Food Information Council highlights that 64% of younger consumers lean towards quick meal solutions instead of traditional cooking [2]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org. This underscores a significant evolution in pasta consumption, emphasizing speed, simplicity, and the urban lifestyle.

Rising Demand for Functional and Health-Oriented Pasta

As consumers increasingly prioritize health, the packaged pasta segment is witnessing a surge in product innovation and portfolio diversification. Leading this charge is the trend of protein fortification, with brands turning to ingredients like pea protein isolates and flours from lentils, chickpeas, and quinoa to boost nutritional value. Heightened health awareness in the wake of the pandemic has made protein a pivotal factor in purchasing decisions, especially in North America and Europe. Egglife Foods' POWER PASTA, for instance, boasts double the protein and a 90% reduction in carbohydrates compared to traditional fresh pasta, all while being gluten- and dairy-free. Similarly, Barilla Protein+ combines lentils, chickpeas, and peas to offer 17g of protein per serving, targeting mainstream consumers. SpirEat’s innovative pasta, infused with Chlorella vulgaris microalgae, is gaining popularity for its rich protein and fiber content, alongside its environmental advantages. This segment's growth trajectory underscores a notable consumer trend: a readiness to pay a premium for clean-label, nutritionally enhanced products, especially in developed markets where claims of protein content, low carbohydrates, and allergen-free attributes heavily influence pasta purchases.

Sustainability-Driven Innovation in Pasta Production

Sustainability is becoming a competitive imperative in pasta manufacturing, driving innovation across ingredients, processes, and packaging. Producers are adopting low-emission cooking technologies, such as Barilla’s passive cooking method, which cuts CO₂ emissions by up to 80%, aligning with climate targets and operational efficiency. Packaging reformulations like Südpack’s recyclable flowpacks and Barilla’s removal of plastic windows highlight efforts to reduce material waste without compromising visibility or shelf stability. Water and energy usage in production are being optimized through closed-loop systems and heat recovery technologies, particularly in large-scale facilities. Ingredient sourcing is also shifting, with growing interest in regenerative wheat farming and low-input crop alternatives like chickpeas and lentils. Carbon labeling and life cycle assessments are increasingly used to benchmark impact and guide innovation. These shifts resonate with environmentally conscious consumers, strengthen ESG credentials, and help pasta brands stay ahead of tightening EU and FDA sustainability directives.

Surging Popularity of Ethnic and Globally Inspired Pasta Flavors

The growing appetite for ethnic and fusion cuisines is reshaping pasta innovation, with brands increasingly experimenting beyond traditional Italian profiles to reflect regional and cross-cultural influences. Consumers, especially Millennials and Gen Z, are gravitating toward bold, globally inspired flavors such as spicy Korean gochujang penne, Thai basil fettuccine, or Indian-style masala fusilli. Symrise reports a 38% increase in consumer interest for cross-cultural pasta flavors in 2024, particularly in North America and Asia-Pacific, where culinary exploration is tied to lifestyle identity and social media discovery [3]Source: Symrise, “Cross-Cultural Flavor Trends 2024,” symrise.com. Brands like Explore Cuisine have introduced products such as Thai Coconut Chickpea Fusilli, merging Southeast Asian flavors with alternative proteins, appealing to flexitarians and culturally adventurous consumers. The fusion trend is also reflected in flavor-forward ready meals and meal kits, with retail pasta sauces incorporating global ingredients like miso, harissa, and tamarind, signaling pasta's evolution into a globally adaptable culinary base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price instability due to durum wheat supply disruptions | -0.7% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Rising popularity of low-carb and keto diets | -0.5% | North America and Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Consumer perception of pasta as a processed or less-healthy food | -0.3% | North America and Europe, health-conscious segments | Medium term (2–4 years) |

| Stricter regulatory limits on sodium and additives | -0.2% | Global, led by North America and Europe regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Low-Carb and Keto Diets

In North America and Western Europe, traditional pasta consumption is facing a significant challenge due to the rising popularity of low-carb and ketogenic diets. These diets typically limit daily carbohydrate intake to under 50g, aiming to promote weight loss and improve metabolic health. Given that a serving of conventional durum wheat pasta contains about 40g of carbs, many health-conscious consumers find it exceeds their acceptable threshold. In response, brands are introducing low-carb alternatives, such as Immi Eats’ keto ramen. Yet, these alternatives often compromise on texture and flavor, which can restrict their broader appeal. Furthermore, the International Food Information Council (IFIC) highlighted in 2024 that over 47% of U.S. adults were actively cutting back on carbs, a trend that's steadily diminishing the demand for traditional pasta [4]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org. As these low-carb preferences become ingrained in health and wellness lifestyles, they're not only reshaping formulation strategies but also exerting downward pressure on core wheat-based pasta segments.

Price Instability Due to Durum Wheat Supply Disruptions

Durum wheat supply fluctuations are shaking up the pasta value chain, leading to uncertainties in pricing and procurement. Key growing regions in Europe, especially Italy, the heart of premium pasta production, have faced setbacks due to climate-related challenges. Changes in cultivation practices, including shrinking sowing areas and water shortages, have strained producers, leading to diminished yields and inconsistent quality. In response to these shortages, manufacturers are seeking out alternative suppliers like Canada and the U.S. However, this shift brings its own set of hurdles, such as unpredictable import costs, varying delivery schedules, and differences in semolina quality. Such disruptions are particularly significant for upscale pasta brands that prioritize regional authenticity and ingredient traceability. As a result of this ongoing volatility, the industry is rethinking its sourcing strategies, pouring resources into agronomic research, and fine-tuning supply chain logistics. Yet, these adjustments come with cost pressures that could sway retail pricing and profit margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dried Pasta Dominate Pasta Market

In 2025, dried/ambient pasta holds a commanding 71.09% market share, thanks to its affordability, long shelf life, and extensive distribution. Its shelf-stable nature makes it a pantry staple, especially in markets that prioritize price and convenience. These qualities bolster dried pasta's widespread appeal. Brands like Monte’s Fine Foods are elevating the segment's profile by reintroducing traditional techniques like bronze die extrusion and slow drying to enhance texture and differentiate themselves in a crowded market.

While frozen pasta holds a smaller market share, it's the fastest-growing segment, boasting a projected CAGR of 7.48% through 2031. Consumers are increasingly prioritizing convenience in their food choices, supporting demand for frozen meal solutions across developed markets. According to the Frozen in Focus 2025 report published by Nomad Foods, a frozen food company, more than half (52%) of consumers in Italy agree that frozen food helps save time, making it an attractive option for busy individuals and families. This evolving preference is driving product innovation within the frozen pasta category. For instance, Birds Eye offers Steamfresh Mediterranean Vegetable Pasta, which is packaged in a specially designed Steamfresh bag that generates steam during microwave heating, allowing the product to be ready in just one minute. The steam-cooking process helps retain texture, moisture, and flavor while delivering quick and convenient meal solutions. Such innovations continue to strengthen the appeal of frozen pasta during the forecast period.

By Category: Conventional Strength Meets Free-Form Innovation

In 2025, conventional pasta dominated the market with an 90.66% share, buoyed by its familiarity among consumers, ease of cooking, and robust merchandising from global retailers. Leading brands, Barilla and De Cecco, leverage high production efficiency and unwavering quality standards, fostering loyalty across diverse demographics. The category thrives on its price accessibility, straightforward cooking instructions, and deep-rooted presence in traditional cuisines. Its relevance is further cemented by institutional consumption in schools and foodservice outlets.

On the other hand, free-form pasta is on a rapid ascent, boasting a 7.38% CAGR. A growing appetite for customization, artistic presentation, and culinary experimentation fuels this surge. Companies like BluRhapsody harness 3D printing technology to craft intricate pasta shapes, often reserved for gourmet dishes. Meanwhile, innovations from Carnegie Mellon, such as the morphing pasta that changes shape upon cooking, not only minimize packaging but also appeal to eco-conscious consumers. With a strong emphasis on visual allure and upscale dining experiences, free-form pasta has carved a niche, especially among Gen Z and premium clientele, who crave unique meal experiences.

By Filling: Plain Pasta Foundation Supports Stuffed Premiumization

In 2025, plain pasta commands a dominant 89.66% market share, thanks to its versatility in global recipes. Its affordability and adaptability make it a staple in homes, restaurants, and institutions alike. Brands such as Banza, with their chickpea-based spaghetti, showcase the evolution of plain pasta, infusing health-conscious attributes while retaining its traditional charm. Its straightforward storage and cooking methods bolster its popularity, particularly in developing regions with a burgeoning middle class.

On the other hand, stuffed pasta is on the rise, boasting 7.00% CAGR through 2031, driven by a trend towards premiumization and meal solutions. Leading the charge is Pastificio Rana, which markets gourmet ravioli and tortellini in refrigerated sections worldwide. As consumers increasingly gravitate towards globally-inspired fillings, like truffle, spinach-ricotta, and even Thai flavors, stuffed pasta emerges as a quick yet luxurious dining choice. Innovations in packaging, like modified atmosphere packaging (MAP), not only enhance shelf life but also pave the way for growth in both chilled and frozen sections.

By Distribution Channel: Retail Dominate the Paste Market

In 2025, retail channels command a 73.42% share of the market and growing at a 5.24% CAGR through 2031, capitalizing on trends like home cooking, pantry stocking, and the rise of private labels. Brands such as 365 by Whole Foods and Great Value leverage affordability to boost volume, while premium brands enjoy the spotlight with strategic shelf-space allocations. The supermarkets and hypermarkets channel plays a critical role in driving global pasta demand, supported by the expansion of organized retail and the strong presence of large-format grocery chains across developed and emerging markets. Leading pasta manufacturers increasingly leverage strategic in-store partnerships with retailers to enhance visibility and influence consumer purchasing behavior through targeted merchandising, category management, and shelf-space optimization.

The online retail channel has emerged as a major growth engine for global pasta sales, driven by the rapid expansion of e-commerce grocery platforms and evolving consumer buying habits. According to data from the Office for National Statistics (ONS), online retail spending in Great Britain continued to demonstrate strong growth momentum in 2025. Online spending values increased by 2.1% in Quarter 4 (October–December 2025) compared with Quarter 3 (July–September 2025), while year-on-year growth reached 8.4% versus Quarter 4 2024. This sustained expansion highlights the increasing importance of e-commerce channels in food retail and reflects continued consumer adoption of online grocery purchasing. Building on this trend, online retail has become a key demand accelerator for pasta, as consumers increasingly shift toward digital grocery platforms for staple replenishment, price comparison, and promotional purchasing.

Geography Analysis

In 2025, Europe commands a dominant 45.84% share of the market, bolstered by its ingrained pasta consumption habits and robust production infrastructure. Italy, with its rich cultural heritage and artisanal expertise, spearheads this dominance. Renowned brands like De Cecco and Barilla not only underscore Italy's commitment to quality but also cement the region's stature in the global export arena. Italian consumers, valuing authenticity and tradition, gravitate towards origin certifications such as PDO or PGI. While shelf-stable pasta varieties lead the market, fresh and stuffed formats are carving out a niche, particularly in specialty grocers and gourmet retail outlets.

Asia-Pacific, boasting a 7.35% CAGR through 2031, emerges as the region with the most rapid growth in pasta consumption. Factors such as urbanization, a growing affinity for Western cuisine, and the rise of dual-income households are propelling the demand for convenient, fusion-ready pasta options. Brands like Nissin, alongside international chains, are localizing offering like kimchi spaghetti or Thai basil fettuccine, showcasing Asian consumers' knack for blending global flavors with regional nuances. This trend is especially pronounced in urban centers, where casual dining increasingly showcases pasta as a versatile platform for local flavor innovations.

North America sees brands like Banza and Jovial leading the charge, innovating to cater to gluten-free, protein-rich, and plant-based preferences. Amidst rising grocery inflation, the expansion of private labels in grocery chains underscores a value-conscious consumer base. South America, buoyed by a rising middle class and a rekindled interest in home cooking, is making steady strides in the pasta market. Meanwhile, the Middle East and Africa are emerging hotspots, driven by a growing wheat-based diet, youthful culinary explorations, and a surge in modern retail. Here, instant and budget-friendly pasta options are making inroads, often bundled with sauces and condiments for added appeal.

Competitive Landscape

The global pasta market is fragmented. Strategic mergers and vertical integration are intensifying the consolidation of the fragmented global pasta market. A prime example is Post Holdings' USD 880 million acquisition of Ronzoni, which catapults it to the position of the second-largest pasta producer in the U.S. This strategic move aims to bolster Post Holdings' scale within the center-store grocery segment. On the other hand, Barilla, leveraging its vertically integrated operations, robust brand equity, and expansive global export network, continues to hold its ground in regional market shares.

As sustainability and health trends reshape consumer expectations, innovation emerges as a pivotal competitive differentiator. Barilla’s “Passive Cooking” initiative, which advocates turning off the heat midway through boiling to slash CO₂ emissions by up to 80%, underscores the integration of environmental responsibility into product usage. Meanwhile, other industry players are pivoting towards functional innovations, like high-protein, low-carb pasta, catering to the fitness-conscious demographic.

The market is witnessing a split: traditional leaders, driven by scale, and nimble innovators, focused on niche segments. Established players, with their efficient manufacturing and expansive distribution, command mainstream categories like dried or plain pasta. In contrast, specialized brands carve out their space by emphasizing value-added attributes, from organic sourcing and non-GMO certification to unique textures and shapes. This evolving landscape indicates that while legacy players will maintain their share through consolidation and a global footprint, the narrative of pasta is being redefined.

Pasta Industry Leaders

Barilla G. e R. Fratelli S.p.A.

Ebro Foods, S.A.

Nestlé S.A.

F.lli De Cecco di Filippo Fara San Martino S.p.A.

Pastificio Rana S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Post Holdings completed its USD 880 million acquisition of 8th Avenue Food and Provisions, including Ronzoni, becoming the second-largest pasta manufacturer in the United States with anticipated annual synergies of USD 15 million.

- March 2025: Egglife Foods launched POWER PASTA at Expo West, a high-protein, low-carb range featuring twice the protein and 90% fewer carbohydrates than traditional fresh pasta.

- September 2024: Artisan Chef Manufacturing Company acquired Buitoni Food Company North America, enhancing refrigerated pasta production capacity across Massachusetts and Virginia.

- March 2024: Barilla partnered with Marie Kondo to promote pasta-box repurposing on Global Recycling Day, supporting the company’s transition to 99% recyclable packaging.

Global Pasta Market Report Scope

| Dried Pasta |

| Fresh/Chilled Pasta |

| Frozen Pasta |

| Canned/Ready to Eat Pasta |

| Conventional |

| Free- Form |

| Plain |

| Stuffed/Filled Pasta |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dried Pasta | |

| Fresh/Chilled Pasta | ||

| Frozen Pasta | ||

| Canned/Ready to Eat Pasta | ||

| By Category | Conventional | |

| Free- Form | ||

| By Filling | Plain | |

| Stuffed/Filled Pasta | ||

| By Distribution Channel | Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the pasta market?

The pasta market size stood at USD 87.06 billion in 2026 and is projected to reach USD 107.66 billion by 2031 at a 4.33% CAGR.

Which region is growing fastest in the pasta market?

Asia-Pacific leads growth with a 7.51% CAGR, driven by urbanization, rising disposable incomes, and a growing appetite for fusion cuisine.

How much of the pasta market share does dried pasta hold?

Dried formats commanded 70.78% of pasta market share in 2025, reflecting their affordability and long shelf life.

What premium trends are shaping new product development?

High-protein formulations, micro-algae fortification, 3D-printed shapes, and globally inspired flavors such as gochujang or Thai basil are key innovation avenues in the pasta industry.

Page last updated on: