Hot Dogs And Sausages Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

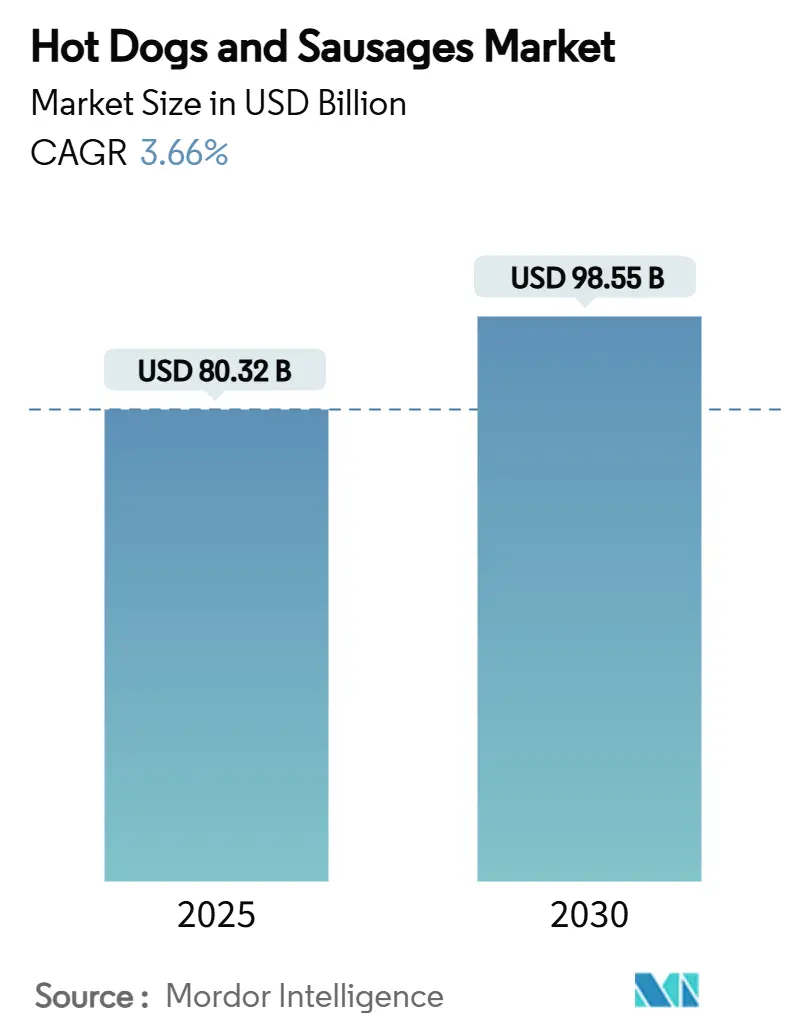

| Market Size (2025) | USD 82.32 Billion |

| Market Size (2030) | USD 98.55 Billion |

| Growth Rate (2025 - 2030) | 3.66% CAGR |

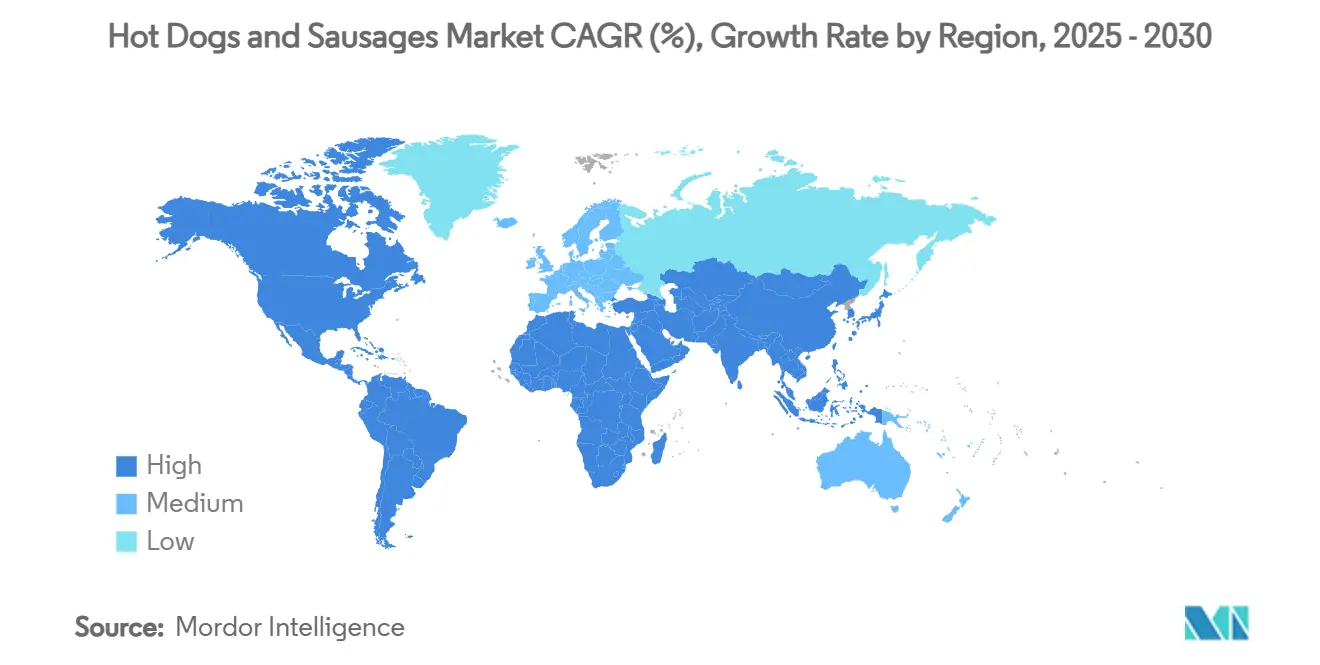

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hot Dogs And Sausages Market Analysis by Mordor Intelligence

The global hot dogs and sausages market size is USD 82.32 billion in 2025 and is projected to reach USD 98.55 billion by 2030, exhibiting a CAGR of 3.66% during the forecast period. In the U.S., hot dogs are more than just food; they're a cultural staple. The National Hot Dog and Sausage Council highlights this sentiment: Americans consumed around 7 billion hot dogs between Memorial Day and Labor Day 2025 [1]Source: National Hot Dog & Sausage Council, “Summer Hot Dog Statistics 2025,” nhdsc.com. This underscores not only the strong seasonal appeal but also the deep-rooted presence of hot dogs in American cuisine. Quick-service and fast-casual chains are diversifying their menus, introducing regional and gourmet varieties. Urban food scenes are buzzing with offerings like Portillo’s Chicago-style hot dogs and Korean-inspired cheese-filled sausages. The trend of premiumization is evident, with brands such as Applegate and Johnsonville leading the charge. They're rolling out clean-label, flavored options crafted from high-quality meat cuts and natural casings. The Asia-Pacific region is emerging as the fastest-growing market, with Western-style meat snacks, particularly ready-to-eat sausage formats, gaining traction. The market's resilience can be attributed to a blend of cultural significance, convenience, innovative products, and a broadening distribution network.

Key Report Takeaways

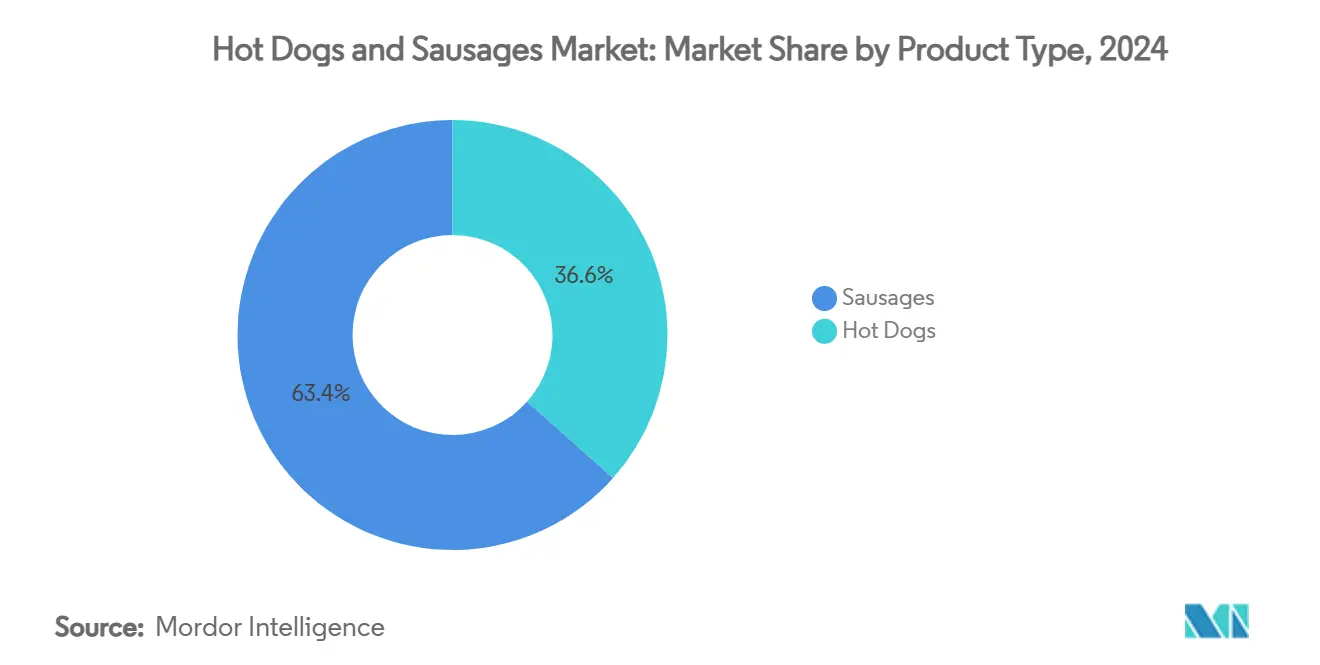

- By product type, sausages held 63.54% of the hot dogs and sausages market share in 2024, while hot dogs are forecast to post the fastest 4.51% CAGR through 2030.

- By meat/protein source, pork dominated with 54.67% share of the hot dogs and sausages market size in 2024; chicken is projected to grow at a 5.12% CAGR to 2030.

- By flavor, salted-classic variants captured 74.43% share in 2024, whereas flavored options are advancing at a 6.23% CAGR during the same horizon.

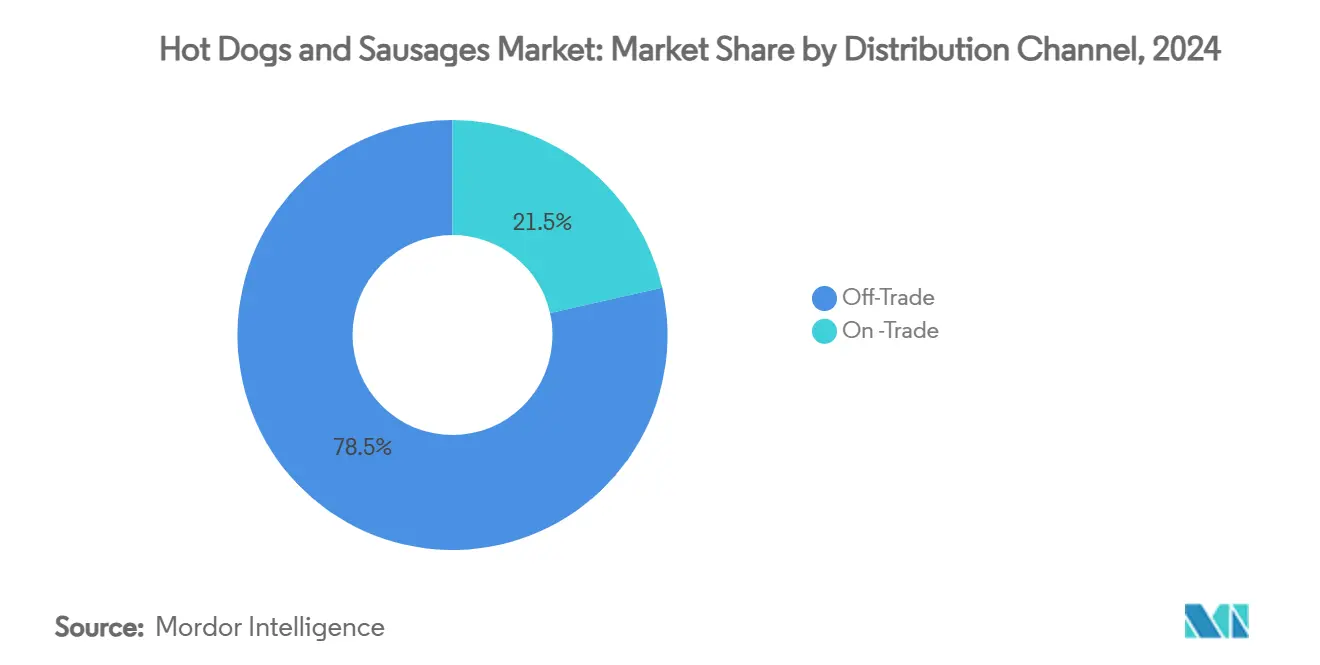

- By distribution channel, off-trade channels commanded 78.53% of the hot dogs and sausages market size in 2024; on-trade is expanding at a 5.41% CAGR through 2030.

- By packaging form, chilled lines accounted for 59.94% share in 2024, and frozen SKUs are set to register a 4.93% CAGR up to 2030.

- By geography, North America accounted for a share of 39.43% in 2024, and Asia-Pacific is set to register a CAGR of 6.44% by 2030.

Global Hot Dogs And Sausages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and evolving lifestyles | +0.8% | Global (Asia-Pacific lead) | Long term (≥ 4 years) |

| Growth in foodservice and casual dining | +0.6% | North America and Europe | Medium term (2-4 years) |

| Demand for gourmet and flavored meats | +0.5% | North America and Europe | Medium term (2-4 years) |

| Expansion of supermarket and retail channels | +0.4% | Global (developing markets) | Long term (≥ 4 years) |

| Strategic investments by key players | +0.3% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Cross-cultural popularity of meat products | +0.2% | Global urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanization and Evolving Lifestyles Spurring Convenience Food Demand

Urbanization and changing lifestyles are driving the hot dogs and sausages market, aligning with new consumer eating habits. According to the 2024 IFIC Food & Health Survey, 56% of Americans opted for snacks or smaller meals over traditional meals in 2023 [2]Source: IFIC Foundation, “2024 Food & Health Survey,” ificfoundation.org. This trend towards on-the-go eating favors hot dogs and sausages, which are seen as quick, protein-rich, portable meal alternatives. In response, retailers are rolling out single-serve sausage packs and heat-and-eat trays, catering to smaller households and solo diners. Convenience stores, like 7‑Eleven, have revamped their hot dog counters to cater to commuters. Meanwhile, quick-service chains, Nathan’s Famous and Checkers Drive-In, launched sausage-based grab-and-go items in 2023, tapping into the snack-time trend. Additionally, manufacturers are innovating with healthier formulations, such as low-fat and plant-based sausages, to attract health-conscious consumers. The growing popularity of food delivery services is also contributing to the market's expansion, as these products are increasingly featured in online meal kits and delivery menus. These industry moves underscore the shift towards snack-like consumption, broadening the appeal of hot dogs and sausages and fueling market growth.

Growth in Foodservice and Casual Dining Preferences

As dining out becomes a staple for many Americans, the appetite for hot dogs and sausages in restaurants and eateries is surging. Data from the USDA ERS highlights a notable trend: in 2023, Americans dedicated 55.7% of their food budget to dining out, amounting to a hefty USD 1.5 trillion, while groceries took up the remaining 44.3%, or USD 1.1 trillion [3]Source: USDA Economic Research Service, “Food Expenditure Series,” ers.usda.gov . This pivot in spending underscores a growing consumer preference for convenience and on-the-go dining, arenas where hot dogs and sausages shine. In response to this trend, 2023 saw fast-casual giants like Nathan’s Famous and Checkers Drive-In roll out sausage-centric menu items, targeting snack enthusiasts and late-night diners. The popularity of drive-throughs and takeout has surged, with many operators opting for menu items that maintain their quality during delivery. This trend favors sausages, celebrated for their heat retention and versatility in wraps, bowls, or buns. Additionally, the increasing influence of social media on food trends has amplified the visibility of hot dogs and sausages, with many brands leveraging platforms to showcase innovative recipes and pairings. By catering to the modern consumer's desire for comfort, convenience, and flavor, these evolving dining habits are propelling the market growth for hot dogs and sausages in both retail and foodservice arenas.

Increasing Demand for Gourmet and Flavored Meat Products

As consumers increasingly gravitate towards premium, globally-inspired, and flavor-rich meat options, the hot dog and sausage categories are witnessing notable growth. Boldly flavored sausages, such as those infused with bourbon whiskey, Korean BBQ, or chipotle cheddar, are particularly resonating with millennials and Gen Z shoppers. These younger demographics are on the lookout for heightened taste experiences and a touch of novelty in their daily meals. Brands are responding to this demand with innovations like Wright Brand’s gourmet sausage links, featuring indulgent varieties such as bacon, cheddar & jalapeño, marrying taste with protein-rich nutrition. This surge in interest dovetails with the burgeoning charcuterie culture, where consumers are increasingly splurging on artisanal meats, valuing craftsmanship, texture, and regional authenticity. Furthermore, a focus on “clean-label” attributes like nitrate-free options, heritage pork, and responsibly sourced ingredients bolsters trust and loyalty among health-conscious and ethically-minded consumers. These shifting preferences are not only broadening product offerings but also elevating sausages and hot dogs to the status of premium protein choices, moving them beyond their traditional perception as budget staples.

Cultural Influence and Cross-Cultural Popularity of Meat-Based Products

As global flavors increasingly permeate mainstream menus, adventurous younger consumers are gravitating towards hot dogs and sausages. The National Restaurant Association’s 2024 report underscores a rising consumer appetite for bold, regional tastes, spotlighting Southeast Asian cuisines, especially Korean-style dishes, as leading food trends [4]Source: National Restaurant Association, “2024 What’s Hot Culinary Forecast,” Restaurant.org, restaurant.org. In tune with these trends, both restaurants and quick-service restaurants (QSRs) are infusing these flavors into their meat offerings. Urban gourmet hot dog joints, for instance, now feature Korean-inspired cheese dogs drizzled with gochujang glaze and sausage burritos packed with bulgogi-style meats. Grocery delis and foodservice venues are also highlighting a range of ethnic sausage varieties, from Jamaican jerk and Portuguese linguiça to South African boerewors. By embedding these culturally inspired offerings into the familiar formats of hot dogs and sausages, businesses are not only satisfying consumers' cravings for novelty and authenticity but also driving both trial and premiumization in retail and foodservice channels. Moreover, these global meat flavors are making waves in limited-time offerings across U.S. chains, allowing brands to gauge regional appeal and draw in multicultural Gen Z and millennial audiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed meat health concerns | -0.9% | Global (Developed markets) | Long term (≥ 4 years) |

| Volatility in pork and beef prices | -0.7% | Global (Major producing regions) | Short term (≤ 2 years) |

| Competition and saturation in mature areas | -0.4% | North America and Europe | Medium term (2-4 years) |

| Stringent food safety regulations | -0.3% | Global (Variable by jurisdiction) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns and Negative Public Perception due to Processed Meat Risks

As younger consumers gravitate towards cleaner labels and healthier protein choices, hot dog and sausage manufacturers face mounting pressures from health concerns tied to processed meat. High-profile health advisories and cancer risk classifications have intensified negative perceptions, compelling brands to reformulate or reposition their products, often at a heightened operational cost. Regulatory momentum is gaining traction; for instance, food policy reviews in the EU and UK are shaping discussions in U.S. advocacy circles, leading several brands to make preemptive labeling changes. Additionally, the growing popularity of plant-based alternatives is further challenging traditional meat products, pushing manufacturers to diversify their portfolios. Moreover, advancements in food technology are enabling the development of innovative solutions, such as fermentation-based preservation methods, which can enhance product appeal. While these challenges loom large, they simultaneously unveil avenues for growth through innovations like cleaner formulations, sodium reductions, and natural preservatives strategies that resonate with health-conscious consumers. By tackling these issues head-on, manufacturers not only safeguard their reputation but also align with the surging demand for healthier meat alternatives.

Volatility in Pork and Beef Raw Material Prices

In 2024, processors in the hot dog and sausage industry grappled with rising input costs as live cattle and lean hog futures surged. While pork prices are set to ease slightly in 2025, beef prices are on an upward trajectory, complicating cost planning. Weather-related disruptions have not only strained supply chains but also curtailed pork processing capacity. This has been felt at retail, with hot dog prices jumping over in five years, underscoring the challenge of affordability. Manufacturers, already contending with declining cattle inventories and the cyclical nature of livestock production, face intensified forecasting hurdles. Yet, amidst these challenges, there's a silver lining: the industry is leaning towards strategic maneuvers like vertical integration, hedging, and automation investments. These moves aim to rein in processing costs and bolster long-term resilience and competitiveness. Additionally, companies are exploring alternative protein sources to diversify product offerings and mitigate risks associated with traditional livestock. Furthermore, advancements in cold chain logistics are being adopted to enhance supply chain efficiency and reduce wastage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sausages Dominate Despite Hot Dog Growth

In 2024, sausages dominate the hot dog and sausage market, capturing a 63.54% share, owing to their versatility and cultural integration. This lead is bolstered by a consumer shift towards customizable, flavorful options, with a surge in globally-inspired varieties like chorizo, merguez, and longganisa in both retail and foodservice. The rising trend of charcuterie boards and protein-rich meals has made sausages a favored choice for convenience and indulgence, especially among millennials and Gen Z, who are on the hunt for premium meat experiences.

Hot dogs, though a smaller segment, are outpacing sausages with a projected CAGR of 4.51% through 2030. Quick-service restaurants and gourmet food trucks are elevating hot dogs with upscale toppings and global flavors like gochujang mayo, kimchi relish, and truffle aioli, drawing in younger, adventurous diners. Health-driven innovations, including nitrate-free and organic grass-fed options, are also giving hot dogs a premium makeover. On another front, sausage producers are venturing into plant-based and hybrid meat solutions, capitalizing on the rising flexitarian trend and driving growth in both segments.

By Meat Type: Pork Leadership Challenged by Chicken Growth

In 2024, pork commands the hot dog and sausage market with a 54.67% share. Its stronghold is largely due to consumers gravitating towards familiar flavors, especially in regional and ethnic forms like chorizo, bratwurst, and Italian sausage. Beyond just being a breakfast staple, pork sausages shine during grilling sessions, seamlessly fitting into daily routines. Offerings such as spicy smoked sausages and maple breakfast links cater to those indulgent cravings, solidifying their appeal. Additionally, the affordability and widespread availability of pork-based products further contribute to their dominance in the market.

Chicken is carving out a niche as the market's fastest-growing protein, boasting a 5.12% CAGR projected through 2030. This surge underscores a broader trend towards leaner, health-conscious choices. Shoppers are now gravitating towards products like grilled chicken sausages and hot dogs, especially those boasting reduced sodium and fat. Brands such as Applegate and Aidells are capitalizing on this shift, rolling out chicken-centric products that spotlight clean-label ingredients and a protein punch. Furthermore, the versatility of chicken as a protein source allows manufacturers to experiment with innovative flavors and formats, appealing to a broader consumer base.

By Flavor: Traditional Dominance with Premium Growth

In 2024, classic flavors, particularly salted ones, dominate the hot dog and sausage flavor segment, holding a commanding 74.43% market share. This dominance underscores a widespread consumer preference for traditional, nostalgic profiles, especially during routine consumption times like breakfast and grilling. These familiar flavors enjoy a robust shelf presence, due to consistent demand across demographics. They're often packaged in multi-packs for family consumption, bolstering volume-driven sales in both retail and foodservice channels.

On the other hand, flavored varieties are rapidly gaining ground, with a projected 6.23% CAGR growth rate through 2030. This surge is fueled by a trend towards premiumization and shifting taste preferences. Global and ethnic influences are spurring innovation, with flavors like Korean BBQ, Mexican chipotle, and Mediterranean herb-infused sausages becoming increasingly popular. Brands such as Aidells and Niman Ranch are introducing bold flavors like pineapple bacon and habanero cheddar sausages, targeting younger consumers with a penchant for adventurous tastes. Additionally, limited-edition seasonal flavors and clean-label claims resonate with health-conscious and novelty-seeking buyers, boosting brand visibility and enabling manufacturers to set premium prices on shelves.

By Distribution Channel: Off-Trade Dominance with On-Trade Opportunity

In 2024, off-trade channels dominate the hot dog and sausage market, commanding a 78.53% share. This trend is largely attributed to inflation-conscious consumers prioritizing value, convenience, and meal versatility at home. Retail giants Walmart and Kroger have noted a surge in sales of bulk-packaged sausages and multipack hot dogs, particularly under their private labels, Great Value and Simple Truth. Convenience stores, with 7-Eleven leading the charge, are expanding their hot hold units, offering grab-and-go sausages to cater to busy urban commuters. E-commerce platforms, notably Amazon Fresh and Instacart, are witnessing a spike in demand for chilled meat bundles and subscription boxes.

On-trade channels are projected to grow at a 5.41% CAGR through 2030. This growth is driven by foodservice players who are transforming sausages and hot dogs into premium, flavor-centric offerings. Quick-service chains, such as Wienerschnitzel, are capitalizing on this trend by introducing limited-time flavors like BBQ Luau Dogs and Korean BBQ Sausages, appealing to consumers' desire for novelty. Similarly, Shake Shack and Portillo’s are enhancing the hot dog experience with artisanal buns and chef-selected toppings. Innovations tailored for delivery, such as Pret A Manger's pre-wrapped gourmet sausage rolls and offerings from ghost kitchens, are meeting the rising demand for high-quality, portable meat meals.

By Packaging Form: Chilled Products Lead with Frozen Growth

In 2024, chilled hot dogs and sausages dominate the market, capturing 59.94% share, highlighting a robust consumer inclination towards freshness, clean-label ingredients, and the convenience of ready-to-cook options. Brands such as Applegate and Johnsonville have adeptly tapped into this consumer trend, presenting chilled sausages that are not only minimally processed and antibiotic-free but also come with transparent labeling. Shoppers increasingly link chilled formats to premium quality and reduced preservatives. This perception fuels consistent growth in both supermarket deli sections and refrigerated meat aisles. Furthermore, the popularity of grab-and-go chilled sausage rolls in convenience stores and grocery delis underscores this segment's leadership, particularly among urban, health-conscious consumers.

Meanwhile, the frozen products segment is on the rise, boasting a 4.93% CAGR growth rate projected through 2030. This surge is attributed to innovations in freezing and packaging technologies, which ensure product integrity and flavor preservation. Brands like Beyond Meat and Tyson are at the forefront, utilizing flash-freezing and steam-bag formats to introduce protein-rich sausage patties tailored for the busy consumer. These brands are also tapping into the trend of portion-controlled, resealable frozen packs, which are particularly appealing to smaller households and flexitarian consumers prioritizing convenience and minimizing food waste. Brands like Armour cater to this demand, providing long-lasting canned sausages ideal for pantry stocking.

Geography Analysis

In 2024, North America commands a 39.43% share of the global hot dogs and sausages market, bolstered by robust foodservice integration, high per-capita consumption, and a deep-seated cultural significance. U.S. brands such as Ball Park, Nathan’s Famous, and Oscar Mayer lead the pack, due to their ubiquitous presence and nostalgic resonance. These brands are venturing into premium and clean-label territories, with Oscar Mayer debuting uncured, nitrate-free offerings to cater to shifting consumer tastes. The entrenched presence of hot dogs in venues like stadiums, convenience stores, and quick-service restaurants, exemplified by Sonic Drive-In's gourmet hot dog menu, reinforces the region's supremacy.

Asia-Pacific emerges as the fastest-growing region, boasting a CAGR of 6.44% through 2030, fueled by rising incomes, urbanization, and an increasing Western culinary influence. Industry giants like JBS are making significant strides in Southeast Asia, exemplified by their USD 100 million investment in processing facilities in Vietnam, aiming to capitalize on the surging demand. In China, brands like Shuanghui (affiliated with WH Group) are infusing Western flavor profiles into traditional sausage formats. Concurrently, Korean entities such as CJ CheilJedang are witnessing heightened global interest in their hot dogs and sausage-centric snacks, due to exports and fusion products resonating with K-cuisine trends.

Europe and Latin America showcase more established or moderately expanding markets, influenced by traditional consumption habits and regulatory frameworks. European stalwarts like Herta (under Nestlé's umbrella) and Wiesbauer lead the charge, offering artisanal and regionally-protected sausages like bratwurst and frankfurters. In Latin America, brands such as Sadia (part of BRF S.A.) and San Rafael are rolling out value-added sausage products tailored to local tastes, especially targeting urban centers in Brazil and Mexico, where there's a burgeoning appetite for protein-rich convenience foods, undeterred by wider economic challenges.

Competitive Landscape

The market exhibits a moderate fragmented structure, with companies in the hot dogs and sausages market differentiating themselves through brand positioning, product innovation, and targeted marketing. Brands such as Tyson's Hillshire Farm, Hormel's Applegate, and Johnsonville boast diversified portfolios, featuring clean-label, organic, and gourmet products. Their marketing increasingly targets health-conscious and younger demographics, emphasizing attributes like being nitrate-free and antibiotic-free. For instance, Applegate’s commitment to “natural and organic” resonates with wellness-focused shoppers, while Johnsonville's emphasis on bold flavors and heritage storytelling strikes a chord with traditional consumers.

Technology plays a pivotal role in enhancing operational efficiency and ensuring product consistency among industry leaders. Companies such as Hormel are turning to advanced automation and AI systems to counteract labor shortages and escalating production costs. Robotic cutting machines now handle tasks previously done by manual workers, boosting yield accuracy and minimizing waste. Additionally, AI-driven predictive maintenance and real-time analytics optimize inventory management and uphold food safety standards.

In a bid to bolster market share and adapt to evolving consumer preferences, firms are consolidating and ramping up production capabilities. JBS’s USD 135 million investment in expanding Iowa's sausage production and Johnsonville’s acquisition of Salm Partners underscore a trend towards vertical integration and bolstered ready-to-eat offerings. Collaborations with local retailers and QSR chains further expedite their entry into off-trade and on-the-go markets. This strategy aligns with health and sustainability movements, setting them up for promising growth.

Hot Dogs And Sausages Industry Leaders

Tyson Foods, Inc.

Hormel Foods Corporation

Maple Leaf Foods, Inc.

Johnsonville, LLC

WH Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JBS USA unveiled a USD 135 million greenfield plant in Perry, Iowa, that will create 500 jobs and add 130 million lbs of sausage capacity, with first production slated for late 2026.

- June 2025: Tyson Foods released Wright Brand Premium Sausage Links in three flavors delivering 12-13 grams protein per serving, targeting national rollout by fall 2025

- March 2025: JBS committed USD 100 million to two new Vietnamese meat facilities focusing on multi-protein lines using Brazilian raw materials

- July 2024: Smithfield Foods completed the takeover of Cargill’s Nashville dry-sausage plant, boosting annual output by 50 million lbs

Global Hot Dogs And Sausages Market Report Scope

| Hot Dogs |

| Sausages |

| Pork |

| Beef |

| Chicken |

| Others |

| Flavored |

| Salted/Classic |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience and Grocery Stores | |

| Online Retail Stores | |

| Other Channel |

| Chilled |

| Frozen |

| Shelf-stable/Canned |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hot Dogs | |

| Sausages | ||

| By Meat Type | Pork | |

| Beef | ||

| Chicken | ||

| Others | ||

| By Flavor | Flavored | |

| Salted/Classic | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Other Channel | ||

| By Packaging Form | Chilled | |

| Frozen | ||

| Shelf-stable/Canned | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hot dogs and sausages market?

The hot dogs and sausages market size stands at USD 82.32 billion in 2025 and is forecast to reach USD 98.55 billion by 2030.

Which segment leads the market by product type?

Sausages lead with 63.54% share in 2024, although hot dogs are set to grow faster at a 4.51% CAGR.

Why is chicken gaining traction as a protein source?

Chicken offers lower saturated fat and competitive pricing, driving a 5.12% CAGR that challenges pork dominance.

Which region is growing the fastest?

Asia-Pacific posts the highest regional CAGR of 6.44% through 2030, propelled by urbanization and rising disposable incomes.

Page last updated on: