Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.73 Billion |

| Market Size (2026) | USD 5.87 Billion |

| Market Size (2031) | USD 6.59 Billion |

| Growth Rate (2026 - 2031) | 2.38% CAGR |

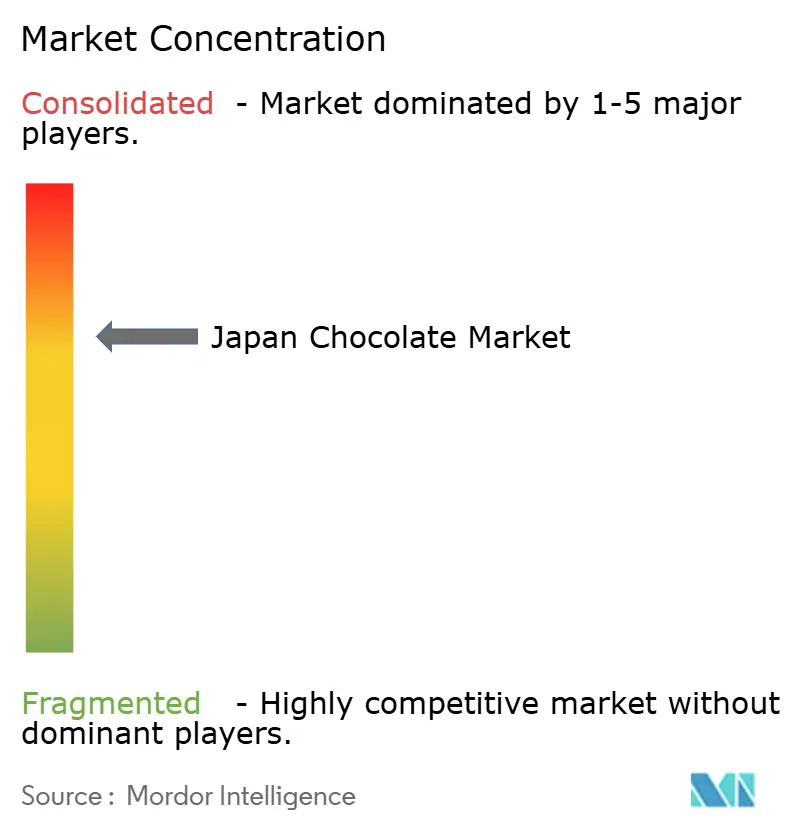

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Chocolate Market Analysis by Mordor Intelligence

The Japan chocolate market size is expected to grow from USD 5.73 billion in 2025 to USD 5.87 billion in 2026 and is forecast to reach USD 6.59 billion by 2031 at 2.38% CAGR over 2026-2031. In 2024, cocoa prices tripled, prompting major manufacturers such as Meiji, Morinaga, and Lotte to raise their product prices. Despite these price hikes, companies managed to maintain sales volumes by introducing limited-edition product lines, aligning launches with popular cultural trends, and discontinuing less profitable product ranges. Retail chocolate prices are rising, and this price increase has temporarily reduced demand for high-cacao chocolates, while encouraging the growth of premium and gifting segments. Functional chocolates gained popularity after Japanese studies highlighted the health benefits of high-polyphenol dark chocolate, such as improved cognitive function and gut health. This trend particularly appealed to active seniors and office workers. The market remains moderately consolidated, with key players driving innovation and adapting to changing consumer preferences.

Key Report Takeaways

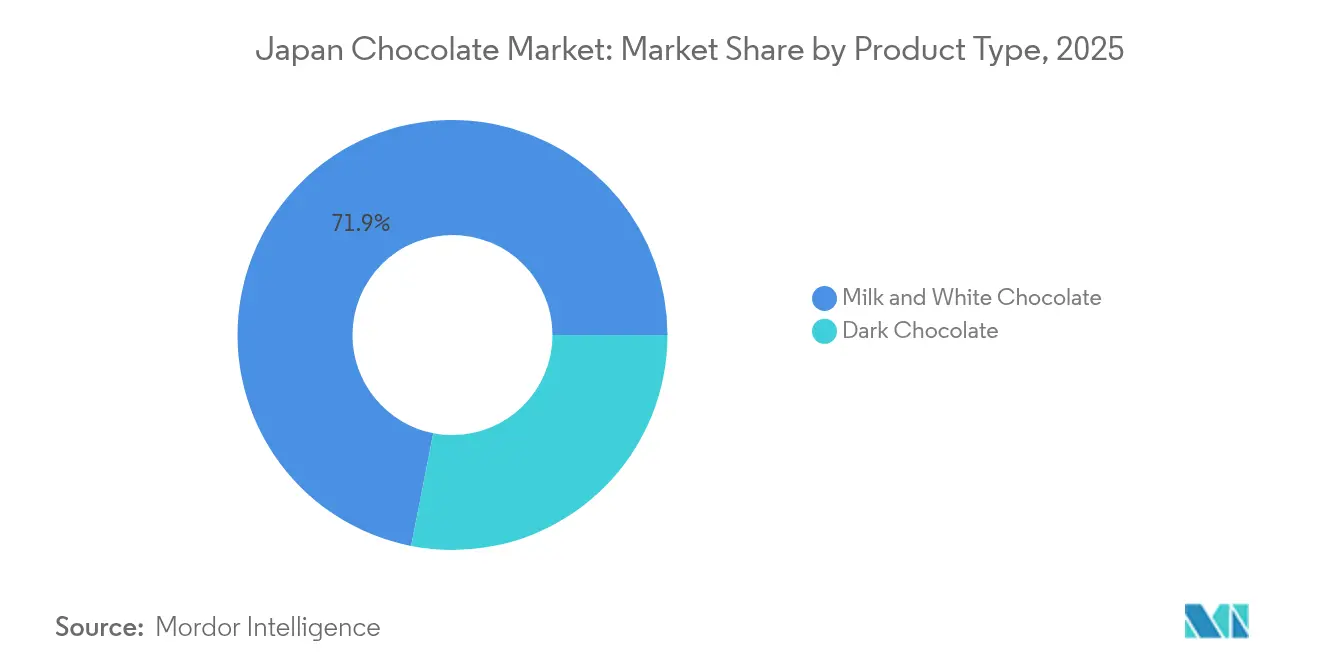

- By product type, milk and white chocolate accounted for 71.92% of Japan's chocolate market share in 2025, while dark chocolate is expected to advance at a 3.44% CAGR through 2031.

- By form, tablets and bars captured a 64.88% share of the Japanese chocolate market size in 2025; pralines and truffles are forecast to expand at a 3.48% CAGR through 2031.

- By price range, the mass tier dominated with a 74.62% share in 2025, whereas the premium chocolate segment is growing at a 5.66% CAGR between 2026 and 2031.

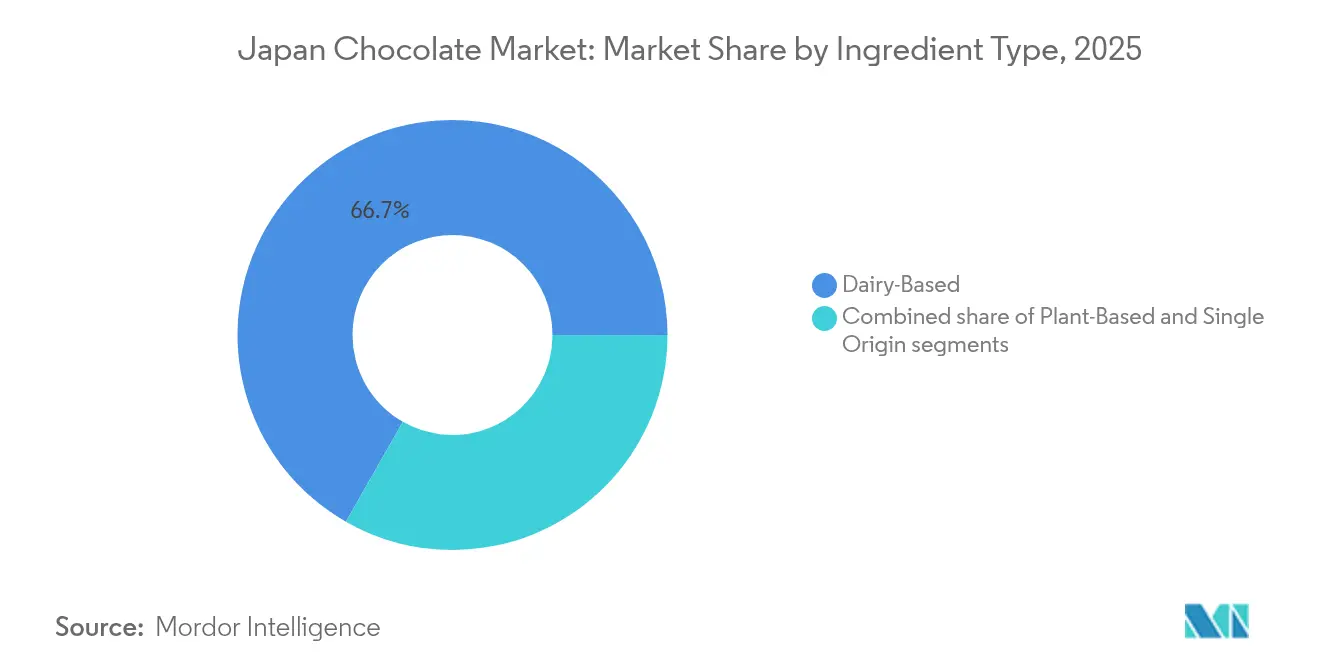

- By ingredient type, dairy-based products accounted for 66.74% of Japan's chocolate market size in 2025, and plant-based alternatives are projected to grow at a 4.26% CAGR.

- By distribution channel, convenience stores secured 38.12% of Japan's chocolate market share in 2025; however, online retail is expected to grow at a 3.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for seasonal and limited-edition products | +0.6% | National, concentrated in Tokyo, Osaka, Nagoya metro areas | Medium term (2-4 years) |

| Growth of convenience snacking among office workers | +0.5% | National, peak in Tokyo, Osaka business districts | Short term (≤ 2 years) |

| Preference for health-oriented and functional chocolates | +0.4% | National, early adoption in Tokyo, Kanagawa | Medium term (2-4 years) |

| Premiumisation and gifting culture | +0.7% | National, strongest in Tokyo, Osaka, Kyoto department stores | Long term (≥ 4 years) |

| Influence of anime, pop culture and character branding | +0.3% | National, spill-over to Southeast Asian via tourism and exports | Short term (≤ 2 years) |

| Rise of sustainability and ethical-sourcing preferences | +0.2% | National, early gains in Tokyo, Yokohama, Kobe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of convenience snacking among office workers

Japan’s chocolate market is heavily influenced by the growing demand for convenient snacking, particularly among the country’s highly employed urban population. As of May 2024, Japan had an employment rate of 97.4%, according to the Organisation for Economic Co-operation and Development, resulting in consistent commuter activity[1]Source: Organisation for Economic Co-operation and Development, "OECD Employment Outlook 2024 - Country Notes: Japan", oecd.org. This has increased the popularity of quick stops at convenience stores, locally known as konbini, where busy individuals often pick up small treats to fit into their hectic schedules. Leading brands such as Lotte Corporation, Morinaga Co., Ltd., and Nestlé SA have capitalized on this trend by offering compact, portable, and diverse chocolate options that cater to on-the-go consumption. Retailers are also playing a significant role in promoting these products through digital marketing campaigns and introducing premium high-cacao chocolate ranges.

Preference for health-oriented and functional chocolates

Japan’s chocolate market is being shaped by a growing preference for healthier and functional products, as more people focus on improving their overall well-being. The World Health Organization predicts that by 2025, an additional 6.5 million people in Japan will achieve better health, leading to a rising demand for chocolates that offer both enjoyment and health benefits[2]Source: World Health Organization, "Population, Japan", data.who.int. To cater to this trend, Meiji introduced a new chocolate line in July 2024, which uses fructooligosaccharides (FOS) instead of regular sugar. FOS is a prebiotic ingredient that supports gut health, making the product appealing to health-conscious consumers. This move highlights a shift in the market, where leading brands are redefining chocolate as more than just a sweet indulgence. By incorporating functional ingredients, companies are aligning their products with the growing interest in healthier lifestyles, while also expanding their appeal to a broader audience.

Influence of anime, pop culture and character branding

Japan’s chocolate market is heavily influenced by anime, pop culture, and character-based branding, which are deeply ingrained in the country’s consumer habits. In 2024, Japan scored 24 on the Anime Popularity Index, according to the World Population Review, highlighting the strong connection between fandom culture and purchasing behavior[3]Source: World Population Review, "Anime Popularity by Country 2025", worldpopulationreview.com. Chocolate brands often collaborate with popular franchises, such as Pokémon, Demon Slayer, and One Piece, to create limited-edition products. These include chocolates with collectible wrappers, exclusive designs for convenience stores, and seasonal packs. Companies such as Lotte and Morinaga also incorporate innovative features like augmented reality (AR) designs to enhance the appeal of their products. These strategies make chocolates a nostalgic and shareable item, appealing to both younger audiences and adults who enjoy pop culture.

Premiumisation and gifting culture

Japan’s chocolate market is experiencing significant growth in premium products and a shift toward more personalized gifting practices, while traditional obligation gifting is becoming less popular. Consumers are increasingly opting for high-quality, artisanal, and single-origin chocolates, particularly for honmei gifting (a form of romantic or special gifting) and personal indulgence. This trend is driving value growth in the market. Brands like La Maison du Chocolat are focusing on offering boutique-style chocolates tailored for corporate events and milestone celebrations. Similarly, Laederach emphasizes its Swiss artisanal heritage to attract premium buyers. Dandelion Chocolate leverages the appeal of single-origin chocolates, highlighting the unique characteristics of cocoa from specific regions, which resonates well with Japanese consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward low-sugar and low-calorie lifestyles | -0.4% | National, concentrated in Tokyo, Kanagawa, Osaka | Medium term (2-4 years) |

| Allergies and rising dietary restrictions | -0.2% | National, early adoption in urban centers | Long term (≥ 4 years) |

| Strong competition from healthier snack alternatives | -0.3% | National, strongest in Tokyo, Osaka, Fukuoka | Short term (≤ 2 years) |

| Cocoa price volatility and supply-chain disruptions | -0.5% | National, with spillover to Southeast Asia export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer shift toward low-sugar and low-calorie lifestyles

Japan’s chocolate market is facing challenges as more consumers adopt low-sugar and low-calorie diets due to growing health concerns. In 2024, the International Diabetes Federation reported that 8.1% of adults in Japan are living with diabetes, which has further encouraged the population to reduce sugar consumption[4]Source: International Diabetes Federation, "Diabetes in Japan (2024)", idf.org. This shift in consumer behavior has led to a decline in demand for traditional chocolate products. Even high-cacao chocolate, which is often marketed as a healthier option, has seen lower sales volumes as its higher price deters many consumers. To address these changes, manufacturers are introducing lighter and reduced-sugar chocolate options. However, consumer adoption of these products has been slow. Additionally, new allergen-labeling regulations set to take effect in 2025 are creating added compliance challenges, particularly for smaller chocolate companies.

Competition from healthier snacks

Japan’s chocolate market is facing challenges due to the rising popularity of healthier snack options. Consumers are increasingly choosing snacks that are low in sugar, high in fiber, and offer additional health benefits. Products like protein bars, nut mixes, yogurt bites, and portion-controlled snack packs are becoming more popular, especially among office workers and younger consumers who value these options for their ability to provide better satiety and cleaner ingredient labels. Convenience stores are responding to this trend by giving more shelf space to these healthier snacks, making them more accessible and visible to shoppers. This shift is reducing the frequency of impulse chocolate purchases. Chocolate manufacturers need to adapt by reformulating their products to include healthier ingredients, highlighting functional benefits, or positioning their offerings as premium indulgences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains on Health Evidence

Milk and white chocolate are the most preferred types in Japan’s chocolate market, together making up 71.92% of the market share in 2025. Their popularity stems from well-known products like Meiji Milk Chocolate and Morinaga Milk Chocolate, which have become staples in Japanese snacking and gifting culture. These chocolates are easily found in convenience stores, supermarkets, and seasonal gift packs, ensuring they remain accessible to consumers. Their timeless flavors and wide appeal make them a favorite for both casual treats and special occasions, maintaining their strong presence in the market.

Dark chocolate is rapidly gaining popularity as the fastest-growing segment, with an expected CAGR of 3.44% from 2026 to 2031. This growth is driven by increasing consumer interest in healthier options, especially among older individuals who are more conscious of their health benefits. To cater to this demand, manufacturers are launching more high-cacao and functional dark chocolate products, promoting them as both healthy and enjoyable. As more people become aware of the benefits of polyphenols and flavanols in dark chocolate, it is shifting from a niche product to a significant part of Japan’s chocolate market.

By Form: Pralines and Truffles Capture Gifting Premiums

Tablets and bars remained the leading chocolate formats in Japan’s market in 2025, capturing a 64.88% share of the total market. Their widespread popularity stems from their convenience and availability in single-serve and multi-pack options, which are perfect for quick and easy purchases at convenience stores. These formats are portable and cater to busy lifestyles, making them a go-to choice for consumers. Manufacturers rely on efficient production methods to ensure consistent quality and affordable pricing, which in turn enhances their appeal across various consumer groups.

Pralines and truffles are anticipated to grow at a CAGR of 3.48% through 2031, making them one of the fastest-growing segments in the market. This growth is driven by increasing demand for premium and indulgent chocolate options, particularly for gifting and special occasions. These products stand out due to their unique flavors, artisanal craftsmanship, and elegant packaging, which attract consumers in specialty and department stores. As more people seek high-quality and luxurious chocolate experiences, pralines and truffles are expected to make a significant contribution to the market's value growth in the coming years.

By Price Range: Premium Segment Outpaces Mass Market

In 2025, the mass tier accounted for 74.62% of Japan’s chocolate market, making it the largest segment. This dominance is attributed to the popularity of well-known brands, their affordable prices, and widespread availability in convenience stores, supermarkets, and pharmacies. These chocolates are a popular choice for everyday snacking, due to frequent discounts, seasonal promotions, and consistent stock availability. While premium chocolates are gaining attention, the mass tier continues to lead because it offers affordability and convenience, making it a reliable option for most consumers.

Meanwhile, premium chocolate is expected to grow at a compound annual growth rate (CAGR) of 5.66% through 2031, becoming the fastest-growing segment of the chocolate market. Consumers are increasingly interested in high-quality options such as artisanal chocolates, single-origin cacao, and elegant gift packaging. This shift is driven by trends like self-gifting and a willingness to pay more for superior products. Boutique chocolatiers, specialty imports, and craft chocolate makers are benefiting from this growing demand. As premium chocolates gain popularity, they are expected to make a significant contribution to the market’s value growth in the years to come.

By Ingredient Type: Plant-Based Alternatives Gain Traction

Dairy-based chocolate accounted for 66.74% of Japan’s market in 2025, supported by the country’s strong milk supply chain and the preference for its creamy and smooth texture. These chocolates are a popular choice for people of all ages and are a staple in daily snacking habits. They are widely available in convenience stores, supermarkets, and seasonal assortments, making them an easy and familiar option for consumers. The consistent quality and traditional flavors of dairy-based chocolate ensure its steady demand and continued market dominance.

Plant-based chocolate is projected to grow at a 4.26% CAGR through 2031, as more Japanese consumers shift towards vegan or flexitarian diets. Companies are focusing on creating alternatives using ingredients like oat, almond, and rice to replicate the creamy texture of milk chocolate. These products appeal to consumers seeking healthier, allergen-free, or environmentally friendly options. With increasing availability in specialty stores and mainstream retail outlets, plant-based chocolate is gradually transitioning from a niche product to a significant driver of market growth in Japan.

By Distribution Channel: Online Retail Gains as Konbini Dominates

In 2025, convenience stores accounted for 38.12% of Japan’s chocolate market, largely due to their round-the-clock operations and convenient locations near railway stations. These stores are a go-to option for commuters, especially during busy hours, leading to frequent impulse purchases. The wide availability of single-serve chocolate bars, seasonal products, and limited-edition offerings ensures quick sales and high turnover. With consistent customer traffic and strategically placed displays, convenience stores remain a vital channel for everyday chocolate consumption in Japan.

Online channels are expected to grow at a 3.73% CAGR through 2031, making them the fastest-growing distribution method for chocolate. E-commerce platforms offer features such as personalized recommendations, subscription services, and targeted promotions, which enhance the overall shopping experience. For instance, Tirol’s direct-to-consumer website and FamilyMart’s in-app campaigns have successfully boosted customer engagement and sales. As consumers increasingly prefer the convenience of online shopping, particularly for premium or unique chocolate products, digital platforms are poised to play a more significant role in driving market growth in the years to come.

Geography Analysis

Japan’s chocolate market is heavily concentrated in major cities like Tokyo, Osaka, and Nagoya, which are the country’s key economic hubs. These cities drive demand for premium chocolate imports and gifting, especially through department stores, due to higher disposable incomes and well-established retail networks. Tokyo, in particular, stands out with its extensive network of convenience stores, providing brands with consistent visibility and access to consumers. This setup encourages frequent, impulse-driven purchases, making these cities critical for shaping market trends and driving sales.

Regional preferences significantly influence chocolate consumption patterns across Japan. Hokkaido, known for its high-quality dairy products, sees local brands emphasizing rich milk flavors to differentiate their offerings. In Fukuoka, the demand for omiyage (souvenirs) during peak tourism seasons, particularly from cruise travelers, drives up chocolate sales. Kansai consumers tend to prefer sweeter milk chocolates, while Kanto residents show a stronger inclination toward dark chocolate. Despite these regional differences, manufacturers are increasingly standardizing product assortments nationwide to streamline operations, while still offering limited-edition products to highlight regional flavors and attract local buyers.

Global supply chain strategies are becoming more important for Japanese chocolate manufacturers to remain competitive. Companies like Lotte are aligning their sourcing operations between Japan and Korea to improve efficiency and expand their global reach. Similarly, brands such as Chateraise and Glico have set up production facilities in Southeast Asia to reduce manufacturing costs and comply with local content requirements. These strategies not only help in expanding exports but also ensure competitive pricing in Japan’s domestic market, supporting steady demand and profitability in the chocolate sector.

Competitive Landscape

Japan’s chocolate market is moderately consolidated, with major players such as Meiji, Morinaga, and Lotte. These companies benefit from extensive distribution networks, in-house production capabilities, and significant marketing budgets, making it difficult for new competitors to enter the market. Sustainability has become a key focus for these brands. For instance, Meiji is working toward sourcing 100% sustainable cocoa, Morinaga is pursuing certifications through Cocoa Horizons, and Glico is enhancing its child-labor-free sourcing standards. These efforts underscore the growing importance of environmental, social, and governance (ESG) practices in differentiating companies in the market.

Instead of focusing solely on increasing sales volumes, companies are now prioritizing profitability and efficiency. Morinaga, for example, has outlined a medium-term plan that emphasizes improving return on invested capital (ROIC) by discontinuing low-performing product lines. Meanwhile, Meiji and Glico are launching premium products, such as chocolates sweetened with functional oligosaccharides (FOS) or made using cold-extraction techniques, to target higher-value segments. Smaller brands like Minimal are also gaining traction by offering artisanal, award-winning chocolates primarily through online channels, appealing to consumers who value unique, high-quality products.

Technology is playing an increasingly important role in giving companies a competitive edge. For instance, Lawson uses predictive analytics to minimize waste at its stores, while FamilyMart is experimenting with AI-driven flavor development to create new products. On a global scale, mergers and acquisitions, such as Mars’ acquisition of Kellanova, could influence strategies and investments in Japan’s chocolate market. Companies like Ezaki Glico are better positioned to handle challenges like fluctuating cocoa prices due to their strong financial stability, which allows them to remain competitive even during periods of cost volatility.

Japan Chocolate Industry Leaders

-

Meiji Holdings Co. Ltd

-

Lotte Corporation

-

Morinaga & Co. Ltd

-

Nestlé SA

-

Mars Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Meiji, a prominent Japanese confectionery company, introduced two new limited-edition chocolate products to its portfolio. These new offerings, Almond Chocolate Crunch Okinawa Salt and Milk and Macadamia Chocolate Okinawa Salt and Premium Vanilla, highlighted Okinawa salt as a distinctive ingredient.

- July 2024: Meiji introduced new chocolate products that utilized fructooligosaccharides (FOS) as a substitute for traditional sugar. This innovation reflected the company's commitment to catering to health-conscious consumers seeking lower-sugar alternatives without compromising on taste.

- August 2023: Kaneka Foods Corporation announced plans to launch the first store of the Belgian chocolate brand Benoit Nihant in Japan. The store, named Benoit Nihant Ginza, was located in Ginza, Chuo-ku, Tokyo.

Japan Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Product Type. Tablets and Bars, Molded Blocks, Pralines and Truffles, and Other Forms are covered as segments by Form. Mass and Premium are covered as segments by Price Range. Dairy-Based, Plant-Based, and Single Origin are covered as segments by Ingredient Type. Convenience Stores, Online Retail Stores, Supermarkets/Hypermarkets, and Other Channels are covered as segments by Distribution Channel.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-Based |

| Plant-Based |

| Single Origin |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Stores |

| Other Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-Based |

| Plant-Based | |

| Single Origin | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Stores | |

| Other Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms