Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 119.62 Billion |

| Market Size (2031) | USD 152.45 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

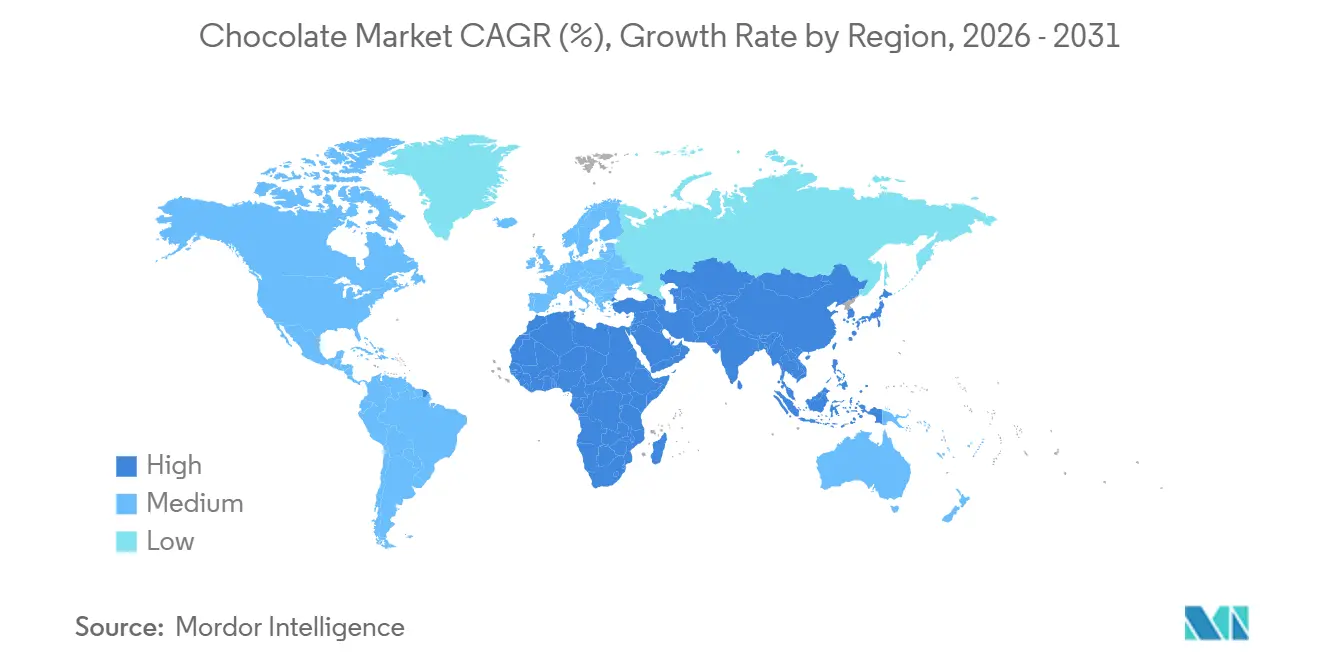

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

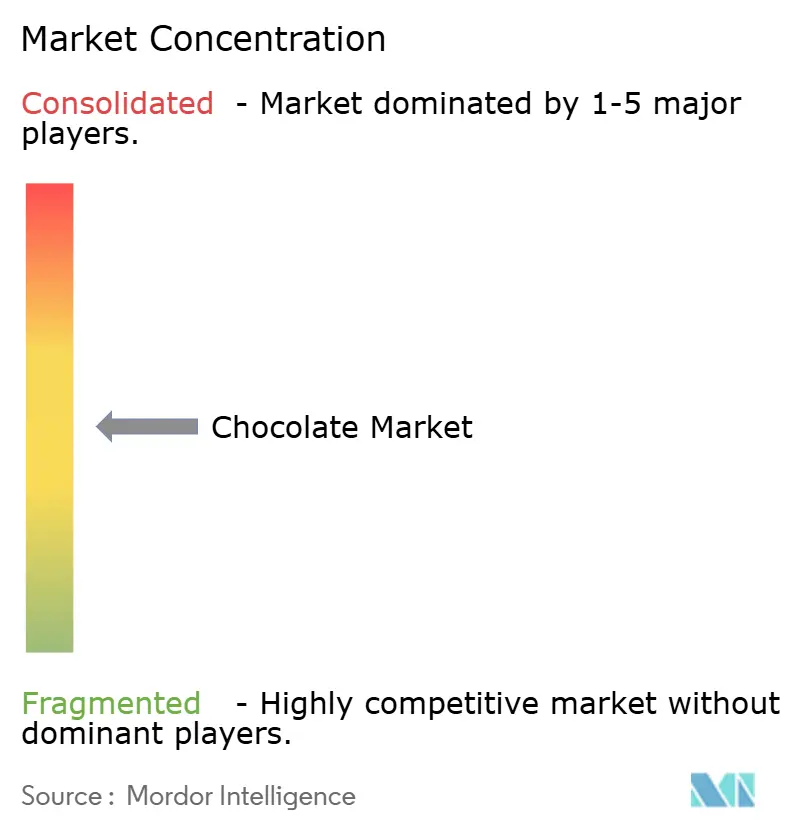

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chocolate Market Analysis by Mordor Intelligence

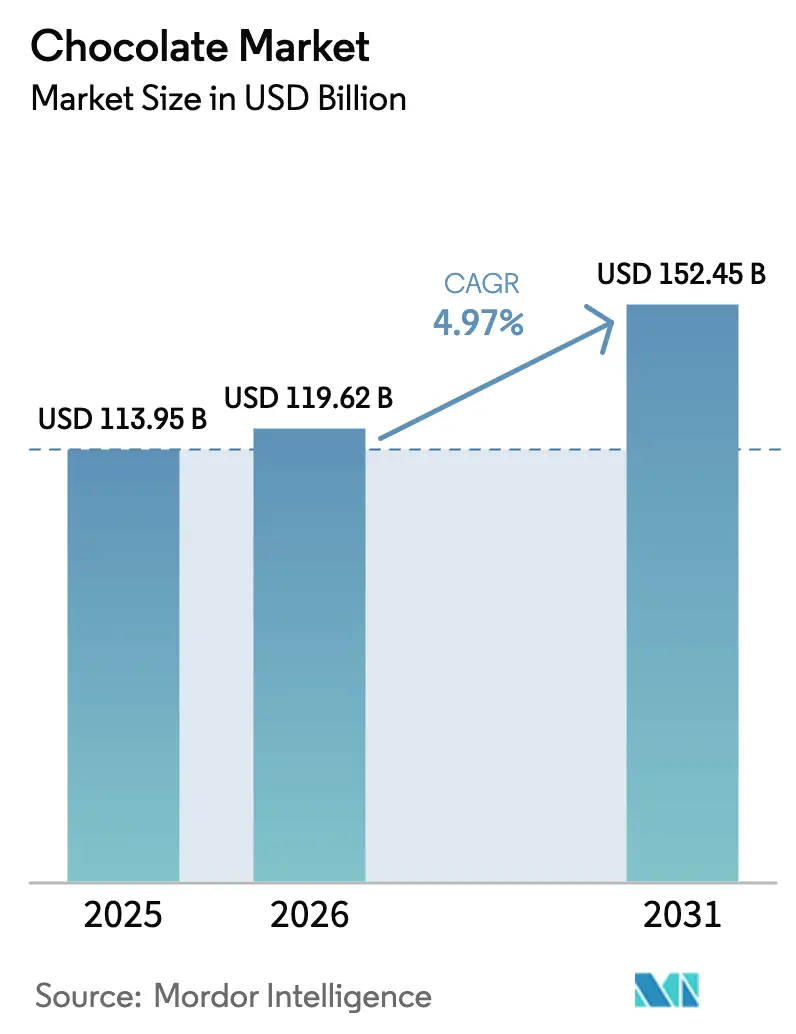

The Chocolate Market size was valued at USD 113.95 billion in 2025 and is estimated to grow to USD 119.62 billion in 2026, reaching USD 152.45 billion by 2031, with a CAGR of 4.97% during the period 2026-2031. The growth of the Chocolate Market is driven by changing consumer preferences, premiumization, and product innovation. The increasing demand for high-quality, artisanal, and ethically sourced chocolates is prompting manufacturers to focus on single-origin, bean-to-bar, and craft products that appeal to consumers seeking authentic and indulgent experiences. Additionally, the market is experiencing growth in functional and health-oriented chocolates, including products with reduced sugar, added nutrients, plant-based ingredients, and wellness-focused components such as probiotics and adaptogens, aligning with broader health-conscious consumption trends. Flavor innovation and global taste exploration are also contributing to market growth, with brands introducing exotic inclusions, culturally inspired flavors, and limited-edition products to enhance consumer engagement and differentiate in a competitive market.

Key Report Takeaways

- By product type, milk and white variants held 64.54% revenue share in 2025; dark chocolate is forecast to expand at a 5.34% CAGR through 2031.

- By form, tablets and bars led with 48.18% revenue share in 2025; pralines and truffles are set to advance at a 4.98% CAGR to 2031.

- By price range, the mass tier accounted for 76.81% of the 2025 value; the premium segment is projected to grow at a 6.34% CAGR through 2031.

- By ingredient type, dairy-based products represented an 81.12% share in 2025; plant-based formulations are poised for a 6.11% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 43.82% share in 2025; online retail is progressing at a 7.07% CAGR through 2031.

- By geography, Europe commanded a 43.56% share in 2025; the Middle East and Africa are expected to post a 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and craft chocolate movement | +1.2% | Global, concentrated in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Flavor innovation and global taste exploration | +0.8% | Global, early adoption in North America and Asia-Pacific | Short term (≤ 2 years) |

| Growth of gifting and seasonal consumption occasions | +0.7% | Global, peak impact in Middle East (Ramadan), Asia-Pacific (Lunar New Year), Western markets (Valentine's, Easter, Christmas) | Short term (≤ 2 years) |

| Rising demand for sustainable and ethical cocoa sourcing | +0.9% | Global, regulatory push in Europe, consumer-led in North America | Long term (≥ 4 years) |

| Clean-label and natural ingredient reformulation | +0.6% | North America and Europe core, spillover to urban Latin America and Asia-Pacific | Medium term (2-4 years) |

| Advancements in chocolate processing | +0.5% | Global, manufacturing hubs in Europe, North America, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization and craft chocolate movement

One of the key drivers of the global chocolate market is the increasing focus on premiumization and the craft chocolate movement. This reflects a growing consumer preference for high-quality, artisanal, and ethically sourced products over mass-produced alternatives. Consumers are increasingly drawn to chocolates with unique flavor profiles, higher cocoa content, and authentic origin stories, enhancing the indulgence experience and fostering a willingness to pay a premium. This trend is particularly prominent in mature markets, where demand for single-origin, bean-to-bar, and limited-edition chocolates is rising, often accompanied by transparent sourcing practices and sustainability credentials. The emotional and experiential appeal of craft chocolates further supports premiumization, as these products are positioned as both personal indulgences and gifting options. Brands differentiate themselves through storytelling, innovative packaging, and curated flavor offerings. For example, in June 2025, Cacao Hunters, a premium chocolate brand known for its award-winning single-origin chocolates and commitment to ethical sourcing, launched in the United States, highlighting the market potential for craft chocolates and the emphasis on premium, ethically focused products.

Flavor innovation and global taste exploration

Flavor innovation and global taste exploration are playing a pivotal role in driving the market as consumers increasingly seek unique, adventurous, and culturally inspired chocolate experiences that transcend traditional milk, dark, and white varieties. Manufacturers are pushing boundaries by incorporating an extensive array of exotic ingredients, such as spices, botanicals, fruits, nuts, and regional delicacies, to cater to evolving consumer preferences and craft distinctive products that stand out in highly competitive markets. This trend is further fueled by the rising demand for experiential consumption, where chocolate transforms into a medium for exploring diverse culinary influences and uncovering stories of origin. For example, in November 2024, Lindt unveiled its limited-edition Dubai-Inspired Pistachio Chocolate Bar in Düsseldorf, seamlessly blending Middle Eastern flavors with premium chocolate to captivate European consumers. This exemplifies how brands are strategically leveraging cultural inspirations to elevate product appeal, foster deeper consumer engagement, and expand their global reach.

Growth of gifting and seasonal consumption occasions

The growth of gifting and seasonal consumption occasions highlights chocolate's continued popularity for celebrations, holidays, and culturally significant events. Consumers increasingly associate chocolate with emotional indulgence, luxury, and thoughtful gifting, making it a preferred choice for occasions such as Valentine’s Day, Christmas, Easter, Diwali, and Ramadan. The demand for premium, visually appealing, and themed chocolates drives manufacturers to introduce limited-edition assortments, decorative packaging, and regionally inspired flavors, enhancing both product value and consumer engagement. For example, Ramadan gifting in Gulf Cooperation Council (GCC) countries is growing rapidly, driven by rising incomes and an expanding expatriate population. This has increased demand for luxury chocolate hampers, often featuring gold-leaf decoration and date-filled pralines that combine local tastes with European craftsmanship. Such culturally tailored offerings strengthen brand relevance, drive seasonal sales spikes, encourage premiumization, and reinforce chocolate’s position as a versatile gift, collectively supporting sustained growth in the global chocolate market.

Rising demand for sustainable and ethical cocoa sourcing

The chocolate market is driven by the growing demand for sustainable and ethical cocoa sourcing, driven by increasing consumer awareness of environmental impact, fair labor practices, and traceability. Consumers today seek not only indulgence but also products that align with their values, favoring chocolates made from responsibly sourced cocoa that supports farmer livelihoods, reduces deforestation, and adheres to ethical labor standards. This shift has led manufacturers to adopt certifications such as Fairtrade, Rainforest Alliance, and UTZ, while also investing in direct sourcing programs and enhancing supply chain transparency to build credibility and maintain consumer trust. According to the International Cocoa Organization (ICCO), Africa produced approximately 3.46 million tons of cocoa beans in 2024/2025, underscoring the continent’s vital role in global cocoa supply and the need for sustainable practices in these key producing regions [1]Source: International Cocoa Organization (ICCO), "Production of cocoa beans worldwide", icco.org. By incorporating sustainability into their sourcing strategies, chocolate manufacturers can mitigate reputational and supply risks while capitalizing on the growing premium segment of ethically conscious consumers, positioning sustainability as a significant growth driver in the global chocolate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising regulatory pressure on sugar and confectionery products | -0.9% | Europe and United Kingdom primary, North America secondary, emerging in Latin America and Asia-Pacific | Medium term (2-4 years) |

| Allergies and rising dietary restrictions | -0.5% | Global, acute in North America and Western Europe | Short term (≤ 2 years) |

| Consumer shift toward low-sugar and low-calorie lifestyles | -0.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Cocoa price volatility and supply-chain disruptions | -1.1% | Global, acute margin pressure in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising regulatory pressure on sugar and confectionery products

The chocolate market faces a significant restraint due to increasing regulatory pressures on sugar and confectionery products. Governments worldwide are implementing stricter measures to address health concerns such as obesity and diabetes. These measures include sugar taxes, front-of-pack nutritional labeling, restrictions on marketing to children, and limits on sugar content. Such regulations compel manufacturers to reformulate products, reduce sugar levels, or use alternative sweeteners, which may affect taste, texture, and consumer acceptance if not managed effectively. Additionally, compliance with these regulations imposes operational and cost challenges, particularly for large-scale producers managing diverse product portfolios across regions with varying regulatory requirements. These challenges are further compounded by the need to balance regulatory compliance with maintaining brand identity and consumer loyalty. Overall, these regulatory pressures constrain product development flexibility, raise production costs, and may reduce sales of traditional high-sugar chocolate products in key markets, potentially driving a shift toward healthier alternatives and innovative product offerings.

Allergies and rising dietary restrictions

Allergies and rising dietary restrictions are significantly impacting the market by shaping consumer purchasing behavior and product formulation. Ingredients such as milk, nuts, soy, gluten, and eggs, which are commonly used in chocolate products, pose allergy risks for a growing number of consumers, thereby reducing the accessibility of conventional offerings. Furthermore, dietary trends such as veganism, lactose intolerance, low-sugar or keto diets, and other health-conscious restrictions are driving demand for alternative formulations. This intensifies the pressure on manufacturers to innovate while ensuring the preservation of taste and texture. These challenges not only increase formulation complexity and production costs but also lead to market fragmentation, as brands are required to cater to diverse niche dietary needs. Consequently, allergies and dietary restrictions act as a significant restraint by narrowing the potential consumer base for traditional chocolate products and necessitating substantial investments in product development, labeling compliance, and meeting evolving consumer expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains on Health Halo

Milk and white chocolate maintained their dominance in the chocolate market in 2025, accounting for approximately 64.54% of total sales. This performance was driven by strong consumer familiarity, broad demographic appeal, and versatility across various consumption occasions. Milk chocolate, in particular, remains the most widely accepted format due to its milder sweetness, creamy texture, and balanced cocoa-dairy profile. These attributes make it especially appealing to children, first-time consumers, and mass-market buyers in both developed and emerging regions. White chocolate, while smaller in market share, complements this segment with its indulgent positioning and flavor adaptability. It is often used as a base for inclusions such as nuts, fruits, caramel, and flavored fillings. Together, milk and white chocolates benefit from significant penetration in everyday snacking, gifting, seasonal assortments, and impulse purchases, particularly within supermarkets, convenience stores, and travel retail channels.

Dark chocolate is projected to grow at a robust CAGR of 5.34% during 2026–2031, reflecting a shift in consumer preferences toward products that combine indulgence with perceived health benefits. Unlike milk and white chocolates, dark chocolate is increasingly positioned as a healthier indulgence due to its higher cocoa content, lower sugar levels, and naturally occurring antioxidants such as flavonoids. These attributes resonate strongly with health-conscious and aging consumer groups. This positioning has allowed dark chocolate to transition from occasional consumption to more regular snacking and functional treat occasions, particularly in developed markets. Additionally, dark chocolate aligns well with clean-label, vegan, and plant-based trends, as many formulations are naturally dairy-free, making it an attractive option for lactose-intolerant and flexitarian consumers.

By Form: Tablets and Bars Lead, Pralines Premiumize

Tablets and bars accounted for approximately 48.18% of chocolate sales in 2025, highlighting their position as the leading and most widely consumed chocolate format. This dominance is primarily attributed to their convenience and ease of consumption, as tablets and bars are portable, mess-free, and suitable for on-the-go snacking across various consumer groups. Their standardized shapes and breakable portions also support portion control, enabling consumers to manage intake while indulging, aligning with the increasing focus on health awareness and mindful snacking habits. Additionally, tablets and bars cater to a wide range of preferences, offering diverse flavors, textures, and cocoa content levels, which appeal to both traditional and adventurous consumers. Their widespread availability in supermarkets, convenience stores, and online platforms further reinforces their accessibility and popularity among global consumers.

Pralines and truffles are projected to grow at a CAGR of 4.98%, driven by their strong positioning as premium, indulgent, and gift-oriented chocolate formats rather than everyday snacks. This growth is closely tied to the rising demand for celebratory and experiential consumption, particularly during festivals, holidays, and special occasions, where consumers prioritize products with higher perceived value and emotional appeal. The segment benefits from artisanal craftsmanship, innovative fillings, and sophisticated flavor profiles, including alcohol-infused, fruit, nut, and single-origin cocoa variants, which enhance differentiation and support premium pricing. Furthermore, luxury packaging, the expansion of specialty chocolate stores, travel retail, and premium online gifting platforms are increasing the visibility and accessibility of pralines and truffles.

By Price Range: Premium Segment Outpaces Mass Market

Mass-market chocolate products accounted for approximately 76.81% of chocolate sales in 2025, highlighting their continued dominance due to affordability, widespread availability, and habitual consumption patterns. These products cater to everyday indulgence and impulse purchases, benefiting from extensive distribution, particularly in emerging and price-sensitive markets. Mass-market chocolates also enjoy strong brand recognition and consumer trust, supported by consistent taste profiles and frequent promotional activities, which drive high purchase frequency and volume-based growth. Manufacturers are maintaining the relevance of this segment through incremental innovations, such as portion-controlled packs, localized flavors, improved packaging, and selective enhancements like reduced sugar, fortified variants, and ethical sourcing claims, all while keeping price points stable.

The premium chocolate segment is growing at a CAGR of 6.34%, indicating a shift in consumer preferences toward quality, authenticity, and elevated indulgence. This growth is fueled by increasing demand for single-origin cocoa, high cocoa-content formulations, artisanal craftsmanship, and ethically sourced ingredients, which enhance perceived value and brand differentiation. Premium chocolates are increasingly associated with self-indulgence, gifting, and experiential consumption, supported by sophisticated packaging and narratives emphasizing provenance and sustainability. Additionally, the segment benefits from the rising popularity of dark chocolate for its perceived health benefits, as well as the growing trend of limited-edition and seasonal offerings that create exclusivity and drive consumer interest. The focus on transparency in ingredient sourcing and the use of clean-label formulations further strengthens consumer trust and loyalty in this segment.

By Ingredient Type: Plant-Based Alternatives Accelerate

Dairy-based chocolate accounted for approximately 81.12% of global ingredient-type sales in 2025, underscoring its strong presence in mainstream chocolate consumption and widespread consumer acceptance. This segment's dominance is attributed to its creamy texture, balanced sweetness, and familiar taste profile, which make milk-based formulations particularly popular in mass-market products, family-oriented consumption, and impulse purchases. Additionally, dairy-based chocolate offers significant formulation versatility, serving as the preferred base for various formats such as bars, tablets, pralines, truffles, and filled chocolates. Its ability to cater to diverse consumer preferences and occasions enhances its relevance for both everyday snacking and gifting, further solidifying its market leadership.

Plant-based chocolate formulations are growing at a CAGR of 6.11%, reflecting a notable shift in ingredient preferences among vegan, flexitarian, and lactose-intolerant consumers. This growth is fueled by increasing demand for dairy-free, allergen-friendly, and clean-label chocolates, alongside heightened awareness of animal welfare and sustainability. Manufacturers are innovating with alternatives such as oat, almond, coconut, and soy-based ingredients, which aim to replicate the creaminess of traditional milk chocolate while offering unique taste profiles and nutritional benefits. The expanding availability of plant-based options across retail channels and their appeal to health-conscious consumers further contribute to the segment's robust growth trajectory.

By Distribution Channel: Online Retail Disrupts Traditional Gatekeepers

Supermarkets and hypermarkets accounted for approximately 43.82% of chocolate sales in 2025, maintaining their position as the leading retail channel. This dominance is attributed to their extensive product assortment, high consumer footfall, and strong visibility for both mass-market and premium brands. These formats serve as the primary point of purchase for everyday chocolate consumption, offering one-stop shopping convenience, competitive pricing, and frequent in-store promotions that drive impulse buying and bulk purchases. Additionally, supermarkets and hypermarkets provide manufacturers with significant shelf space and merchandising flexibility, enabling effective brand differentiation through packaging, seasonal displays, and promotional campaigns. The inclusion of private-label offerings and premium sub-sections further allows retailers to cater to both value-driven and premium-seeking consumers.

Online retail is expanding at a CAGR of 7.07%, emerging as one of the fastest-growing distribution channels for chocolate. This growth is supported by increasing digital penetration and evolving consumer purchasing behavior. According to the International Telecommunication Union (ITU), 5.5 billion people were online in 2024, representing 68% of the global population, up from 65% in the previous year [2]Source: International Telecommunication Union (ITU), "Internet use continues to grow", itu.int. This rise in connectivity has significantly expanded the addressable consumer base for e-commerce. Online platforms, including direct-to-consumer websites, brand-owned portals, marketplaces, and subscription models, offer greater convenience, broader product assortments, and access to premium and niche offerings that may not be available in physical stores. Furthermore, online retail facilitates personalized gifting, customized assortments, seasonal bundles, and premium storytelling, which strongly appeal to younger, urban, and digitally native consumers.

Geography Analysis

Europe accounted for approximately 43.56% of total revenue in the chocolate market in 2025, driven by its deeply rooted chocolate consumption traditions and strong premium heritage. The region benefits from a long-standing cultural acceptance of chocolate as both an everyday indulgence and a popular gifting option, particularly in countries like Belgium, Germany, Switzerland, France, and the United Kingdom. Europe is also recognized globally for its artisanal craftsmanship, single-origin sourcing, and premium formulations, contributing to both volume and value growth. Highlighting this strength, Belgium exported chocolate worth EUR 4.02 billion in 2024, according to the Observatory of Economic Complexity (OEC), emphasizing the region’s role as a major consumption hub and a significant exporter of high-value chocolate products worldwide [3]Source: Observatory of Economic Complexity (OEC), "Chocolate in Belgium", oec.world.

The Middle East and Africa (MEA) is the fastest-growing chocolate market, with a CAGR of 5.96%, driven by a combination of cultural, demographic, and regulatory factors. Chocolate consumption in the region is closely tied to occasions such as Ramadan, Eid, weddings, and hospitality-led gifting, where premium boxed chocolates and assortments are highly favored. Growth is further supported by rising disposable incomes in Gulf Cooperation Council (GCC) economies, increasing demand for premium and imported brands, and the expanding retail presence of luxury and specialty chocolate stores. Additionally, the growing adoption of halal-certified chocolate formulations is enabling brands to cater to mass-market consumers while adhering to regional dietary norms, facilitating growth across both premium and mainstream segments.

North America and the Asia-Pacific exhibit contrasting yet complementary growth patterns in the chocolate market. North America maintains steady value-led growth by balancing high per-capita consumption with trends such as premiumization, increased adoption of dark chocolate, and innovation in plant-based and reduced-sugar formulations, despite the market's maturity. Conversely, Asia-Pacific is experiencing rapid growth, fueled by urbanization, the westernization of diets, and the increasing acceptance of chocolate as a snack and gifting product in countries like China, India, Japan, and Southeast Asia. Smaller pack sizes, localized flavors, and premium gifting assortments are helping brands expand consumption in the region, positioning Asia-Pacific as a key long-term growth driver, even as Europe continues to lead in overall market share.

Competitive Landscape

The chocolate industry is moderately consolidated, with a few multinational companies such as Mars, Incorporated, Mondelēz International Inc., Nestlé S.A., Ferrero International SpA, and The Hershey Company holding a significant share of the market. These companies leverage extensive manufacturing capabilities, global sourcing networks, and strong brand portfolios that cover mass-market, premium, and gifting segments. Their scale allows for cost efficiencies, consistent quality, and widespread retail penetration, supporting their leadership across supermarkets, convenience stores, and travel retail channels worldwide.

Despite the industry's consolidation, opportunities are emerging in high-growth niche segments such as plant-based chocolate formulations, single-origin and traceable cocoa products, and functional chocolates infused with adaptogens, probiotics, or wellness-focused ingredients. In these areas, large companies often face challenges related to agility and credibility, as consumers increasingly prioritize authenticity, transparency, and purpose-driven brands. This shift has created favorable conditions for startups and independent chocolatiers to attract early adopters by focusing on clean labels, ethical sourcing, and artisanal craftsmanship.

In response to these trends, major players are expanding into niche segments through premium sub-brands, limited-edition launches, sustainability certifications, and selective acquisitions. While these strategies help diversify their portfolios, consumer perceptions of authenticity often favor independent artisans over corporate-led innovations, particularly in health, sustainability, and origin-focused categories. Consequently, the competitive landscape is evolving into a dual structure, where large companies maintain dominance in volume, while smaller, specialized players drive trends and influence premium and innovation-focused growth within the global chocolate market.

Chocolate Industry Leaders

-

Mars, Incorporated

-

Mondelēz International Inc.

-

Nestlé S.A.

-

Ferrero International SpA

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Cadbury Dairy Milk has expanded its portfolio in India with the launch of Milkinis, a crème-filled chocolate bar targeting younger, on-the-go consumers. It is available in single and twin packs.

- September 2025: Ferrero Rocher introduced new Ferrero Rocher chocolate squares, offering a modern variation of the brand's iconic gold-wrapped praline. The range includes Milk Hazelnut, Dark Hazelnut, White Hazelnut, Caramel Hazelnut, and an assorted selection.

- July 2025: The Campco introduced three new chocolate products: Dark Delight dark chocolate, Dome Delight premium truffles, and Campco Orange Eclairs. These additions enhance the company's product portfolio, catering to diverse consumer preferences.

- May 2025: Nestle has introduced new chocolate bar flavors such as Aero Strawberry, Milkybar Chokito, and Milkybar Crunch Block. The Milkybar Chokito features caramel nougat combined with cereal balls, while the Milkybar Crunch Block contains crunchy cereal pieces coated in white chocolate.

Global Chocolate Market Report Scope

The chocolate market encompasses the global industry involved in the production, distribution, and sale of chocolate products derived from cocoa beans. The chocolate market is segmented by product type, form, price range, ingredient type, distribution channel, and geography. Based on product type, dark chocolate, milk, and white chocolate. Based on form, the market is segmented into tablets and bars, molded blocks, pralines and truffles, and other forms. Based on price range, the market is segmented into mass and premium. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single Origin |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Store |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dark Chocolate | |

| Milk and White Chocolate | ||

| By Form | Tablets and Bars | |

| Molded Blocks | ||

| Pralines and Truffles | ||

| Other Forms | ||

| By Price Range | Mass | |

| Premium | ||

| By Ingredient Type | Dairy-based | |

| Plant-based | ||

| Single Origin | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Online Retail Stores | ||

| Convenience Store | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms