Market Overview

| Study Period | 2021 - 2031 |

|---|---|

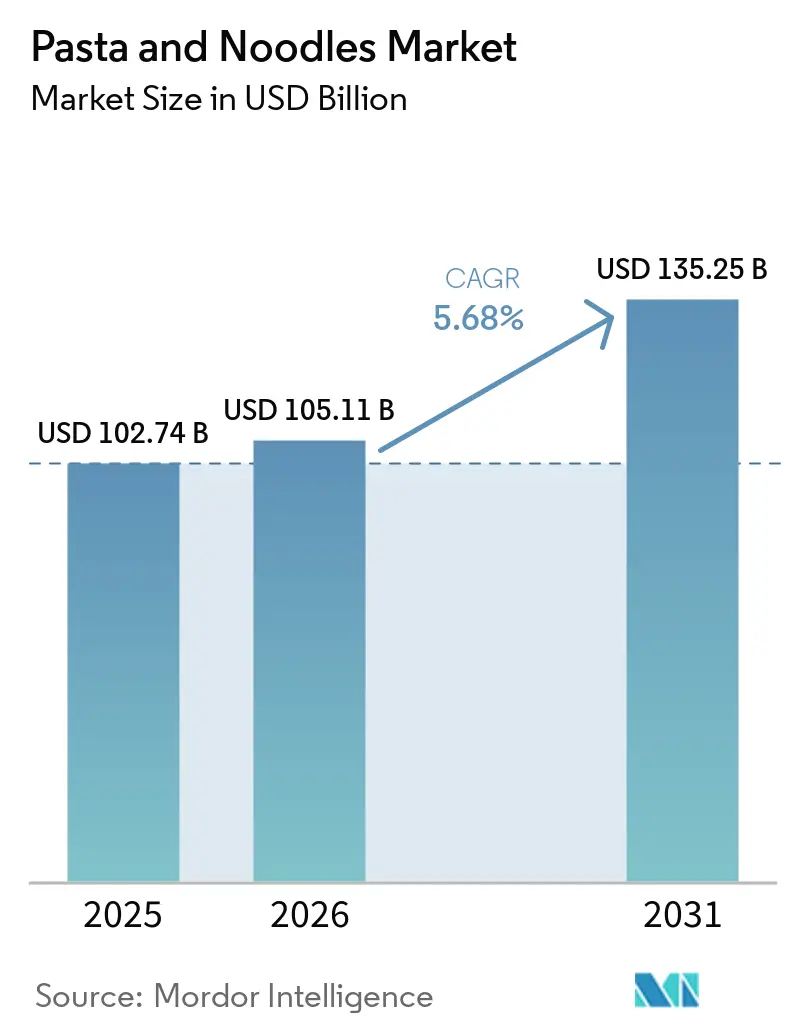

| Market Size (2026) | USD 105.11 Billion |

| Market Size (2031) | USD 135.25 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

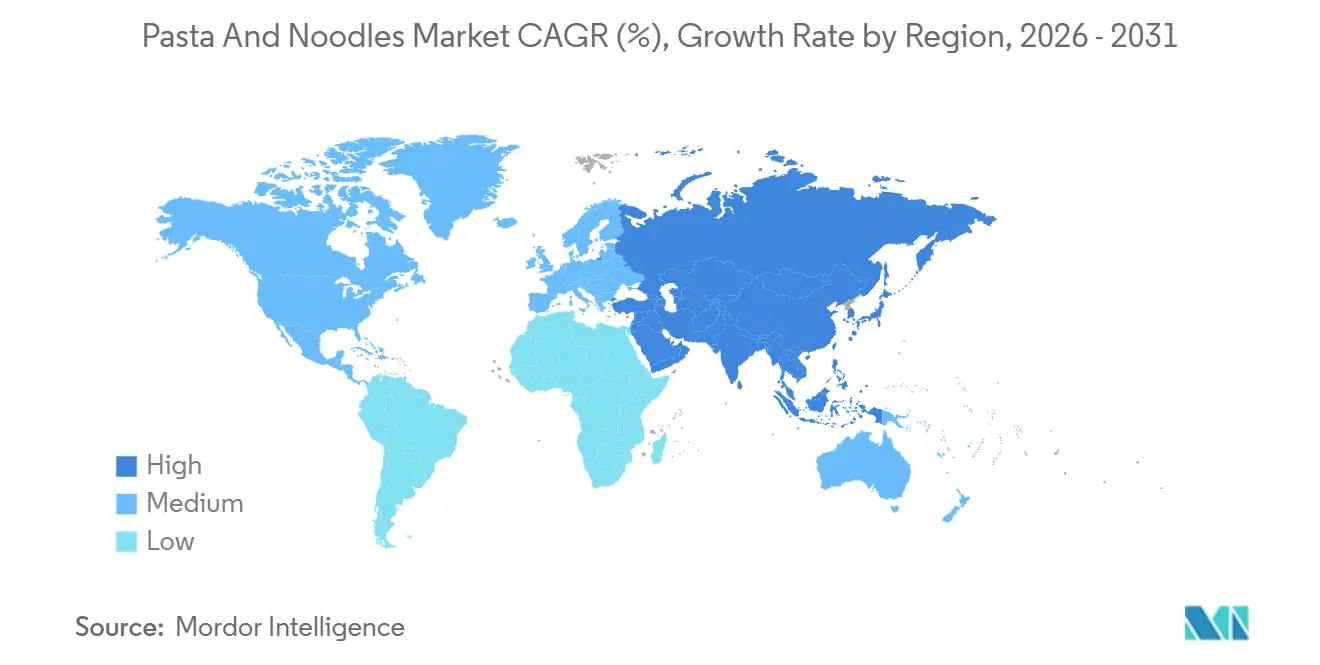

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pasta And Noodles Market Analysis by Mordor Intelligence

The pasta and noodles market size is valued at USD 105.11 billion in 2026, growing from the 2025 value of USD 102.74 billion, and is forecast to climb to USD 135.25 billion by 2031, advancing at a 5.68% CAGR during the forecast period. Consumer demand is widening from classic wheat pasta toward gluten-free, protein-fortified, and ancient-grain variants as households juggle convenience with wellness. Technological improvements in extrusion and drying are enhancing texture and shelf life, allowing premium and value propositions to coexist. Supply-chain investments in Asia-Pacific and South America are shortening delivery times, spurring regional challengers to contest multinational incumbents. Meanwhile, tighter front-of-pack rules in North America and Europe are accelerating low-sodium reformulations and ingredient transparency, creating entry points for agile brands. Currency volatility and rising input costs, however, threaten margins for players lacking hedging strategies.

Key Report Takeaways

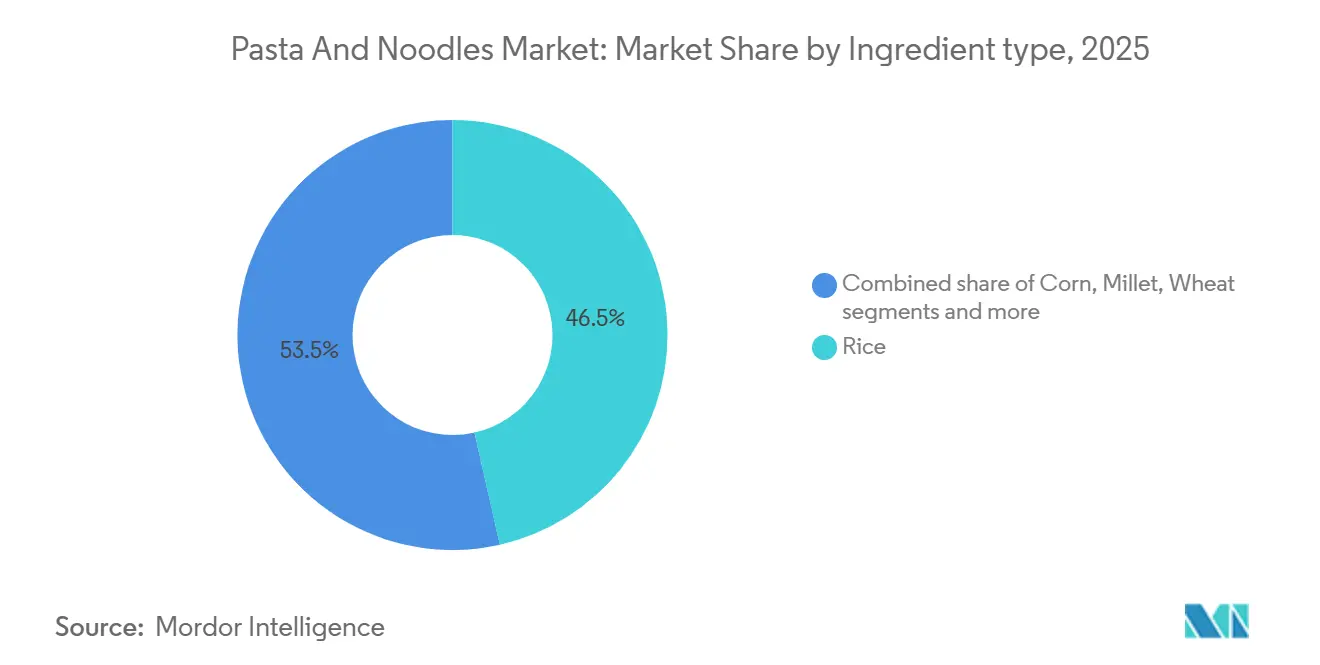

- By ingredient type, rice captured 46.48% of the 2025 value share, while millet is set to climb at a 7.21% CAGR through 2031.

- By product type, dried formats led with 70.11% share in 2025; instant options are projected to grow at a 6.88% CAGR to 2031.

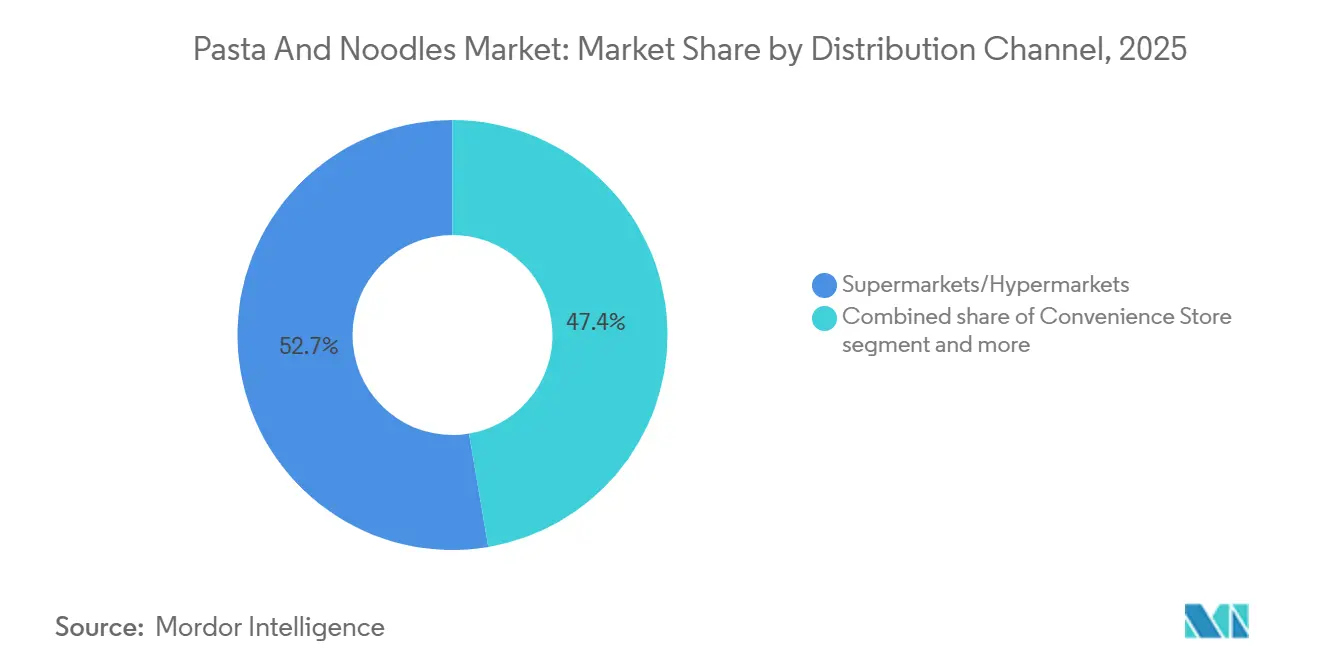

- By distribution channel, supermarkets and hypermarkets accounted for 52.65% of 2025 sales, while online channels showed the fastest trajectory, growing at a 7.55% CAGR to 2031.

- By geography, Europe accounted for 40.25% of 2025 revenue; the Asia-Pacific is poised for the quickest regional expansion, with an 8.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pasta And Noodles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising influence of Asian cuisines | +1.2% | Global, with strongest uptake in North America, Europe, and urban centers across Latin America | Medium term (2-4 years) |

| Growing demand for shelf-stable products | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa, particularly in Nigeria, Egypt, and Kenya | Short term (≤ 2 years) |

| Health trends boosting protein-fortified, gluten-free, and whole-grain variants | +1.0% | North America and Europe lead, with emerging adoption in Australia and urban India | Long term (≥ 4 years) |

| Technological advances in production for better texture and shelf stability | +0.7% | Global, with capital-intensive adoption concentrated in Japan, South Korea, Italy, and United States | Medium term (2-4 years) |

| Rising disposable income in developing markets | +1.1% | Asia-Pacific (India, Indonesia, Vietnam), Sub-Saharan Africa (Nigeria, Kenya), and South America (Brazil, Colombia) | Long term (≥ 4 years) |

| Strategic advertising initiatives by major market players | +0.5% | Global, with highest media spend in China, United States, and Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Influence of Asian Cuisine Globally

The mainstreaming of ramen, pho, and pad thai in Western markets has transformed noodles from ethnic novelties into everyday meal options, with restaurant chains and food-service operators incorporating Asian formats into core menus. In 2025, the United States Department of Agriculture reported a 23% increase in rice noodle imports compared to 2024, reflecting heightened consumer familiarity driven by social media recipe trends and celebrity chef endorsements [1]Source: United States Department of Agriculture, “Rice Noodle Import Statistics 2025,” USDA Foreign Agricultural Service, usda.gov. This culinary diffusion extends beyond restaurants; retail data indicates that Korean instant noodle brands achieved double-digit growth in European supermarkets during 2025, with German and French consumers gravitating toward spicy and umami-rich flavor profiles previously confined to specialty stores. The shift is not merely aesthetic, it signals a willingness to experiment with texture and seasoning paradigms that differ markedly from traditional pasta, creating entry points for Asian manufacturers to establish distribution in markets historically dominated by Italian and American brands.

Growing Demand for Shelf-Stable Products

Urbanization and the growth of nuclear households across Asia-Pacific and Africa are significantly increasing the importance of shelf-stable food formats that require minimal refrigeration and preparation time. In Nigeria, where the power grid remains unreliable, instant noodles have become a vital food choice for low-income urban workers. According to the National Bureau of Statistics, consumption of instant noodles is projected to rise by 18% year-on-year in 2025, highlighting their growing role as a convenient and affordable meal option[2]Source: National Bureau of Statistics Nigeria, “Consumer Goods Consumption Report 2025,” Nigerianstat, nigerianstat.gov.ng. Similarly, in Indonesia, government-driven infrastructure development programs have enhanced last-mile distribution networks, enabling packaged noodles to reach rural areas that previously relied on fresh or wet markets. This shift is further supported by the growing influence of e-commerce platforms, which offer bulk discounts that lower per-unit costs. These discounts not only make packaged noodles more accessible but also encourage stockpiling among price-sensitive consumers, further driving demand in these regions.

Health Trends Boosting Protein-Fortified, Gluten-Free, and Whole-Grain Variants

Consumer awareness of refined carbohydrate risks has catalyzed a reformulation wave, with manufacturers introducing lentil-based, chickpea-enriched, and quinoa-blended noodles to capture health-conscious demographics. In 2025, the European Food Safety Authority updated its front-of-pack labeling guidelines to mandate clearer disclosure of fiber and protein content, prompting Italian pasta producers to launch whole-wheat lines that retain traditional texture while meeting nutritional benchmarks. Concurrently, gluten-free variants are expanding beyond celiac sufferers to include consumers perceiving gluten as inflammatory, with sales in North America growing 14% in 2025 per Nielsen retail tracking data. Protein fortification achieved through egg white, pea protein, or spirulina additives addresses the needs of fitness enthusiasts and aging populations seeking convenient protein sources, a trend particularly pronounced in Australia and Scandinavia. However, these premium products command 30-50% price premiums over conventional offerings, limiting penetration in cost-sensitive markets and creating a bifurcated landscape where innovation clusters in high-income geographies.

Technological Advances in Production for Better Texture and Shelf Stability

Extrusion technology improvements have enabled manufacturers to replicate traditional hand-pulled noodle textures at an industrial scale, while vacuum drying and modified atmosphere packaging extend shelf life without preservatives. Japanese equipment manufacturers such as Toyo Suisan have licensed advanced drying systems to Chinese and Indian producers, reducing moisture content to below 10% while preserving elasticity, a critical quality parameter for premium instant noodles. In Italy, Barilla's 2024 investment in high-pressure processing equipment allows pasta to retain al dente texture after extended storage, addressing export market demands where transit times exceed 60 days. These technological leaps also facilitate clean-label formulations by eliminating the need for chemical preservatives, aligning with regulatory pressures in the European Union and North America. However, capital intensity remains a barrier for small and medium enterprises, concentrating innovation among multinational corporations and widening the quality gap between premium and value segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising raw material costs like wheat and supply chain disruptions | -0.9% | Global, with acute pressure in North Africa, Middle East, and South Asia reliant on wheat imports | Short term (≤ 2 years) |

| Health concerns over high carbohydrates, sodium, and calorie content | -0.6% | North America and Europe lead concerns, with emerging awareness in urban China and Brazil | Medium term (2-4 years) |

| Stringent food safety, labeling, and regulatory compliance requirements | -0.4% | European Union, United States, and Canada, with spillover to export-oriented producers in Asia | Long term (≥ 4 years) |

| Cultural preferences and dietary habits in certain regions limit market penetration | -0.3% | Sub-Saharan Africa, Middle East, and parts of South America where traditional staples dominate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Raw Material Costs and Supply Chain Disruptions

Wheat prices surged 22% between January 2024 and December 2025, driven by drought conditions in Australia and export restrictions imposed by Russia and Ukraine, according to the Food and Agriculture Organization's price index [3]Source: Food and Agriculture Organization, “Food Price Index December 2025,” FAO, fao.org. This volatility disproportionately impacts manufacturers in import-dependent regions such as Egypt and Morocco, where wheat constitutes 60-70% of noodle production costs. Rice prices exhibited similar instability, with India's 2024 export ban on non-basmati rice triggering supply shortages across Southeast Asia and East Africa, forcing producers to source from Thailand and Vietnam at elevated premiums. Supply chain disruptions extend beyond commodities; packaging material costs rose 15% in 2025 due to polyethylene shortages linked to petrochemical plant maintenance shutdowns in the Middle East. Smaller regional brands lacking hedging mechanisms or vertical integration face acute margin compression, with several Nigerian and Kenyan producers reducing SKU portfolios to focus on high-velocity items. These cost pressures are partially mitigated by forward contracting and diversification into alternative grains such as millet and sorghum, though consumer acceptance of non-traditional ingredients remains uneven.

Health Concerns Over High Carbohydrates, Sodium, and Calorie Content

Public health campaigns targeting obesity and hypertension have intensified scrutiny of instant noodles, which typically contain 1,500-2,000 milligrams of sodium per serving—exceeding World Health Organization daily intake recommendations. In 2025, the United Kingdom's National Health Service launched a "Rethink Your Noodles" initiative highlighting links between high-sodium diets and cardiovascular disease, prompting major retailers to delist products exceeding 1,200 milligrams per serving. South Korea's Ministry of Food and Drug Safety mandated front-of-pack sodium warnings on instant noodles in 2024, correlating with a 9% decline in domestic instant noodle consumption during 2025 as consumers shifted toward fresh or refrigerated alternatives. Refined carbohydrate concerns are equally salient, with nutritionists advocating for whole-grain substitutes to mitigate glycemic spikes associated with white flour noodles. These headwinds are most pronounced in affluent markets where health literacy is high and consumers possess purchasing power to trade up to premium alternatives, while price-sensitive segments in developing markets prioritize affordability over nutritional optimization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Millet Gains as Gluten-Free Demand Accelerates

Rice-based noodles held 46.48% of ingredient-type value share in 2025, anchored by entrenched consumption in Vietnam, Thailand, and southern China, where rice noodles are culinary staples. However, millet variants are expanding at 7.21% annually through 2031, the fastest growth among all ingredient categories, driven by gluten-free positioning and micronutrient density that appeals to health-conscious consumers in North America and Europe. Wheat remains the volumetric leader despite slower growth, supported by pasta's dominance in Mediterranean diets and instant noodle ubiquity across Asia. Corn-based noodles occupy a niche, primarily serving Latin American markets where maize is culturally preferred, though adoption remains constrained by texture challenges that manufacturers are addressing through blended formulations combining corn with wheat or rice flours.

Millet's ascent reflects broader ancient-grain trends, with the United Nations declaring 2023 the International Year of Millets, catalyzing awareness campaigns that elevated the grain's profile among Western consumers. Indian producers such as ITC Limited have launched millet noodle lines targeting export markets, leveraging India's position as the world's largest millet producer to offer cost-competitive alternatives to quinoa and amaranth-based products. Regulatory support is evident in India's 2024 inclusion of millet noodles in its Public Distribution System, subsidizing access for low-income households and normalizing consumption. Wheat-based segments face headwinds from gluten-avoidance trends, though durum wheat pasta retains premiumization potential through protected designation of origin certifications in Italy and artisanal production methods that command 40-60% price premiums over mass-market offerings.

By Product Type: Instant Formats Capitalize on Urbanization

Dried noodles and pasta commanded 70.11% of product-type revenue in 2025, reflecting their versatility across culinary applications and extended shelf life that suits both retail and food-service channels. Instant noodles, however, are growing at 6.88% through 2031, outpacing all other formats as urbanization in Asia-Pacific and Africa drives demand for single-serve, rapid-preparation meals. Canned and frozen variants occupy a smaller share, concentrated in North American and European markets where convenience trumps fresh preparation, while chilled or refrigerated noodles cater to premium segments seeking restaurant-quality texture at home. The instant category's momentum is particularly striking in India, where per-capita consumption doubled between 2020 and 2025, supported by aggressive pricing strategies that position instant noodles below USD 0.30 per serving—competitive with street food alternatives.

Technological enhancements are blurring lines between instant and premium segments, with air-dried and non-fried instant noodles emerging as healthier alternatives that retain rapid preparation while reducing fat content by 30-40%. Nissin Foods' 2025 launch of its "Cup Noodle Pro" line in Japan, featuring 15 grams of protein per serving and reduced sodium, exemplifies this convergence, targeting fitness-oriented consumers willing to pay 25% premiums for functional benefits. Dried pasta's resilience stems from its versatility and cultural embeddedness in Italian and Mediterranean cuisines, though growth is decelerating in mature markets as household sizes shrink and single-person households gravitate toward portion-controlled instant formats. Frozen noodle segments are benefiting from meal-kit proliferation, with companies such as HelloFresh incorporating pre-cooked noodles into subscription boxes, though this channel remains nascent outside North America and Western Europe.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets retained 52.65% of distribution share in 2025, leveraging shelf space dominance and promotional muscle to drive volume sales, yet online retail channels are expanding at 7.55% through 2031, the fastest growth among all distribution modes. This shift is most pronounced in China, where platforms such as Alibaba's Tmall and JD.com account for 35% of noodle sales, enabling direct-to-consumer models that bypass traditional wholesalers and reduce distribution costs by 15-20%. Convenience stores remain critical in Japan and South Korea, where 24-hour formats and dense urban footprints facilitate impulse purchases, though their share is eroding as e-commerce offers bulk discounts and subscription services that lower per-unit costs. Other distribution channels, including food-service operators and vending machines, serve niche roles, with vending particularly relevant in Japan, where automated retail infrastructure is mature.

E-commerce's ascent is reshaping competitive dynamics, as smaller brands leverage digital marketing and influencer partnerships to build awareness without incurring traditional retail slotting fees. In India, regional noodle brands have achieved national distribution through Amazon and Flipkart, circumventing the need for physical retail networks that favor established players. Subscription models are gaining traction in North America, where companies such as Thrive Market offer organic and specialty noodles at discounted rates, appealing to health-conscious consumers seeking convenience and value. However, last-mile logistics challenges in rural areas and consumer preferences for tactile product inspection limit e-commerce penetration in parts of Africa and Latin America, where supermarkets and open-air markets remain dominant. The channel's growth trajectory suggests that omnichannel strategies—integrating physical retail with digital fulfillment—will become table stakes for brands seeking to maintain relevance across diverse consumer segments.

Geography Analysis

Europe commanded 40.25% of the noodles and pasta market revenue in 2025, underpinned by Italy's pasta exports, which totaled EUR 3.2 billion (USD 3.5 billion) in 2025 according to the Italian Trade Agency, and Germany's robust retail infrastructure that prioritizes premium and organic variants. However, the region's growth is decelerating as population stagnation and dietary diversification toward plant-based proteins erode per-capita consumption. France and Spain are witnessing modest gains driven by North African immigrant communities that favor couscous and semolina-based noodles, while Eastern European markets such as Poland and Romania are expanding due to rising incomes and Westernization of dietary habits. The United Kingdom's post-Brexit trade realignments have introduced tariff complexities for Italian pasta imports, prompting some UK retailers to source from Turkey and Egypt, where production costs are 20-30% lower. Regulatory compliance remains stringent, with the European Food Safety Authority enforcing rigorous pesticide residue limits on wheat imports, which elevates costs for non-EU suppliers seeking market access.

Asia-Pacific is expanding at 8.87% through 2031, the fastest regional growth rate, propelled by India's instant noodle consumption surge, which reached 8 billion servings in 2025, and China's premiumization trends where consumers are trading up from value brands to Japanese and Korean imports priced 50-80% higher (India Brand Equity Foundation). Japan's domestic market is mature, with per-capita consumption plateauing, yet exports of premium ramen and udon to North America and Europe grew 19% in 2025, driven by culinary tourism and anime-fueled cultural affinity among younger demographics. Australia's noodle market is benefiting from Asian immigration, with Vietnamese and Thai communities sustaining demand for rice noodles and driving retail assortment expansion. Southeast Asian markets- particularly Indonesia, Vietnam, and the Philippines- are witnessing intense competition as local players such as Indofood and global entrants like Nestlé vie for share in price-sensitive segments where brand loyalty is fluid and promotional intensity is high.

North America and South America exhibit divergent trajectories, with the United States and Canada experiencing modest growth constrained by health concerns over sodium and refined carbohydrates, while Brazil, Colombia, and Peru are expanding due to urbanization and rising female labor force participation that elevates demand for convenient meal solutions. Mexico's noodle market is heavily influenced by proximity to the United States, with cross-border trade facilitating access to American brands, though local producers such as Herdez are gaining share through culturally tailored flavors incorporating chili and lime. The Middle East and Africa remain nascent markets, with the United Arab Emirates and South Africa leading consumption due to expatriate populations and Westernized retail formats, while Nigeria's instant noodle market is the continent's largest, driven by affordability and aggressive distribution by local manufacturers. Turkey's strategic position as a production hub for Europe and the Middle East is strengthening, with exports to neighboring markets growing 12% in 2025, supported by competitive labor costs and preferential trade agreements.

Competitive Landscape

Major companies dominate the global pasta and noodles market, which is moderately fragmented. Regional manufacturers and new entrants compete with established multinational companies like Nestlé S.A., Nissin Foods Holdings Co. Ltd., Unilever PLC, Barilla Group, and The Campbell Soup Company. These companies focus on expanding their product portfolios, developing premium products, entering new geographical markets, and offering value-based products to maintain their market positions.

Growth opportunities exist in emerging markets where pasta consumption is increasing but brand preferences remain flexible. The market also shows potential in specialized segments, particularly functional and fortified products targeting specific nutritional requirements. Regional manufacturers maintain competitive positions by emphasizing local ingredients and cultural authenticity.

Manufacturing technology has become a significant differentiator, as advanced processes improve product quality, consistency, and preservation. This competitive environment promotes innovation and market diversification, resulting in broader product selection and enhanced quality for consumers.

Pasta And Noodles Industry Leaders

Nestlé S.A.

Nissin Foods Holdings Co. Ltd.

Barilla Group

The Campbell Soup Company

Ebro Foods, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Maggi expanded its United States portfolio with a new noodle line. The product features three flavors: Indian Classic Masala, Chinese Spicy Garlic, and Korean Spicy BBQ.

- March 2025: General Mills introduced ramen noodles under its Old El Paso and Totino's brands. The new product line includes Old El Paso Ramen Noodles in Fajita and Beef Birria flavors, and Totino's Ramen Noodles in Cheese Pizza and Buffalo-Style Chicken Pizza varieties.

- October 2024: WokTok by Veeba expanded its product portfolio with new Chinese sauces and instant noodles. The company introduced instant cup noodles in five variants: Chowmein, Manchurian, Masala, Kung Pao, and Spicy Korean 1X. The noodles are manufactured without refined flour (maida), palm oil, or monosodium glutamate (MSG).

- August 2024: Noodle Lovers introduced two microwaveable pasta varieties, 'Toowoomba Pasta' and 'Rosé Pasta,' which deliver restaurant-quality taste through simple microwave preparation. These dishes represent Korean adaptations of traditional Italian pasta, featuring cream-based sauces with added spices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global noodles and pasta market as all industrially produced strands, sheets, or shaped pieces of unleavened dough, irrespective of ingredient base (wheat, rice, corn, millet, or blends), sold in dried, instant, canned, frozen, or chilled form to retail, food-service, and institutional channels.

Scope exclusion: Ready-to-eat composite meals where pasta or noodles account for less than half of the serving weight are kept out of scope.

Segmentation Overview

- By Ingredient Type

- Rice

- Wheat

- Corn

- Millet

- Others

- By Product Type

- Dried

- Instant

- Canned and Frozen

- Chilled / Refrigerated

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Others Distribution Channels

- By Geography

- North America

- United States

- Mexico

- Canada

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Netherlands

- Sweden

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple structured conversations with processors, contract packers, large wholesalers, and specialty e-grocers across Asia-Pacific, Europe, and the Americas validated pack-size trends, average selling prices, and margin pass-throughs. Follow-up surveys with dietitians and QSR procurement managers helped stress-test health-trend assumptions embedded in the forecast.

Desk Research

We first compiled baseline consumption and trade indicators from open, authoritative sources such as FAO commodity balances, UN Comtrade export logs, USDA production briefs, and Eurostat retail indices. Nutritional intake statistics from the World Instant Noodles Association and packaging-waste filings helped map volume shifts to value. Company 10-Ks, investor decks, and selected news archived on Dow Jones Factiva supplemented price and brand-mix insights. The sources listed illustrate the breadth consulted; many additional datasets were reviewed for cross-checks and clarification.

Government nutrition surveys, national household expenditure panels, and trade-association shipment dashboards were then screened for ingredient splits and channel dynamics, allowing us to refine regional weightings before any modeling work began.

Market-Sizing & Forecasting

A top-down reconstruct anchored on per-capita intake and customs-adjusted production supplied the initial 2025 value pool, which we then corroborated through selective bottom-up supplier roll-ups and sampled ASP x volume checks.

Key model drivers include: average daily servings per capita, retail unit price trajectories, wheat and rice commodity indices, penetration of instant formats in emerging cities, online grocery share of packaged foods, and regulatory sodium caps influencing reformulation costs.

Five-year outlooks are generated using multivariate regression blended with scenario analysis, where ingredient inflation and channel-mix elasticity act as primary variables. Any country series that lacked consistent trade data was gap-filled using peer averages before final triangulation.

Data Validation & Update Cycle

Outputs pass two analyst reviews, an automated variance screen against historical ratios, and senior sign-off. Models refresh annually; interim updates trigger when feedstock prices swing >15% or when a top-five producer issues material guidance. A last-mile sense check is repeated just before each client delivery.

Why Mordor's Pasta and Noodles Baseline Stands Solid

Published figures often diverge because firms choose different product mixes, channel scopes, and update cadences. By aligning intake statistics with trade reconciliations and refreshing every year, Mordor limits drift and keeps comparability high.

Key gap drivers include rival studies focusing on pasta alone, omitting food-service flows, or extrapolating retail scanner data without ingredient inflation controls. Currency translation timing and shorter forecast windows add further variance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 102.08 B (2025) | Mordor Intelligence | - |

| USD 75.50 B (2025) | Global Consultancy A | Pasta-only scope, excludes noodles and chilled SKUs |

| USD 87.97 B (2024) | Industry Association B | Earlier base year; relies mainly on retail sales receipts |

| USD 83.10 B (2024) | Trade Journal C | Limited geography set and shipment-value conversion factors |

The comparison shows that when ingredient breadth, dual-channel coverage, and up-to-date currency fixes are applied, Mordor delivers a balanced, transparent baseline that decision-makers can replicate and audit with confidence.

Key Questions Answered in the Report

What is the projected value for the global noodles and pasta market in 2031?

The market is forecast to reach USD 135.25 billion by 2031.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is poised for the quickest expansion, advancing at an 8.87% CAGR.

Which product type is gaining the most momentum?

Instant formats show the fastest growth, set to rise at a 6.88% CAGR.

What role is e-commerce playing in distribution?

Online channels are expanding at a 7.55% CAGR as direct-to-consumer and subscription models gain scale.

Page last updated on: