Ashwagandha Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

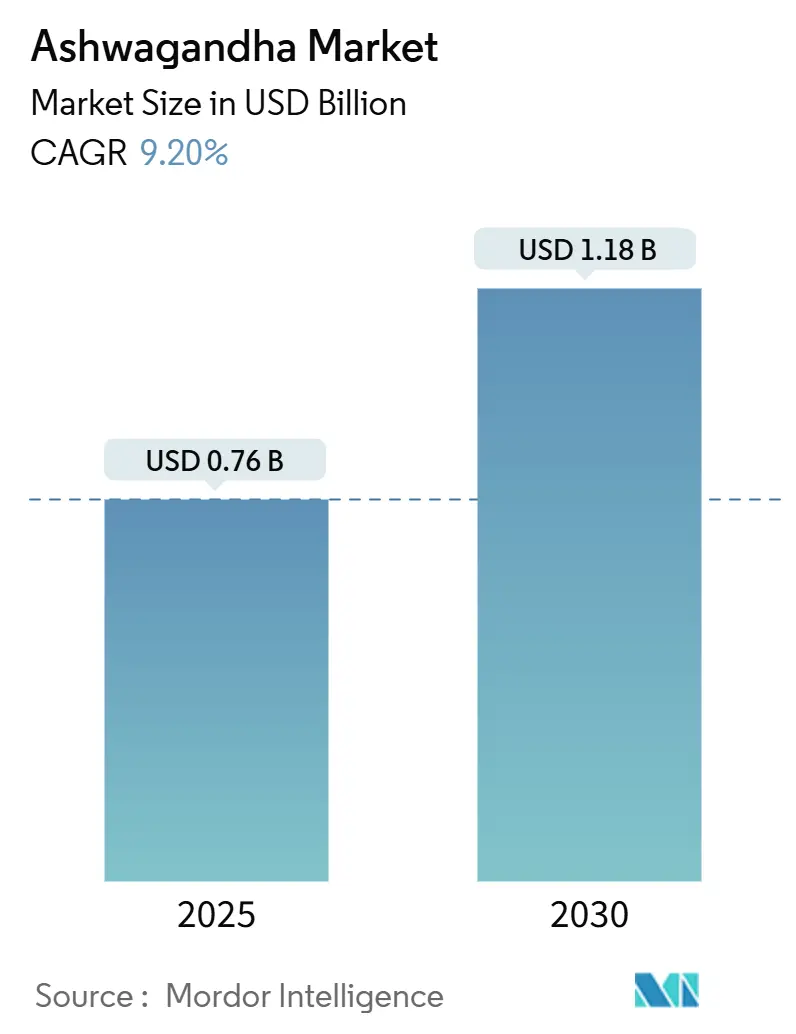

| Market Size (2025) | USD 0.76 Billion |

| Market Size (2030) | USD 1.18 Billion |

| Growth Rate (2025 - 2030) | 9.20% CAGR |

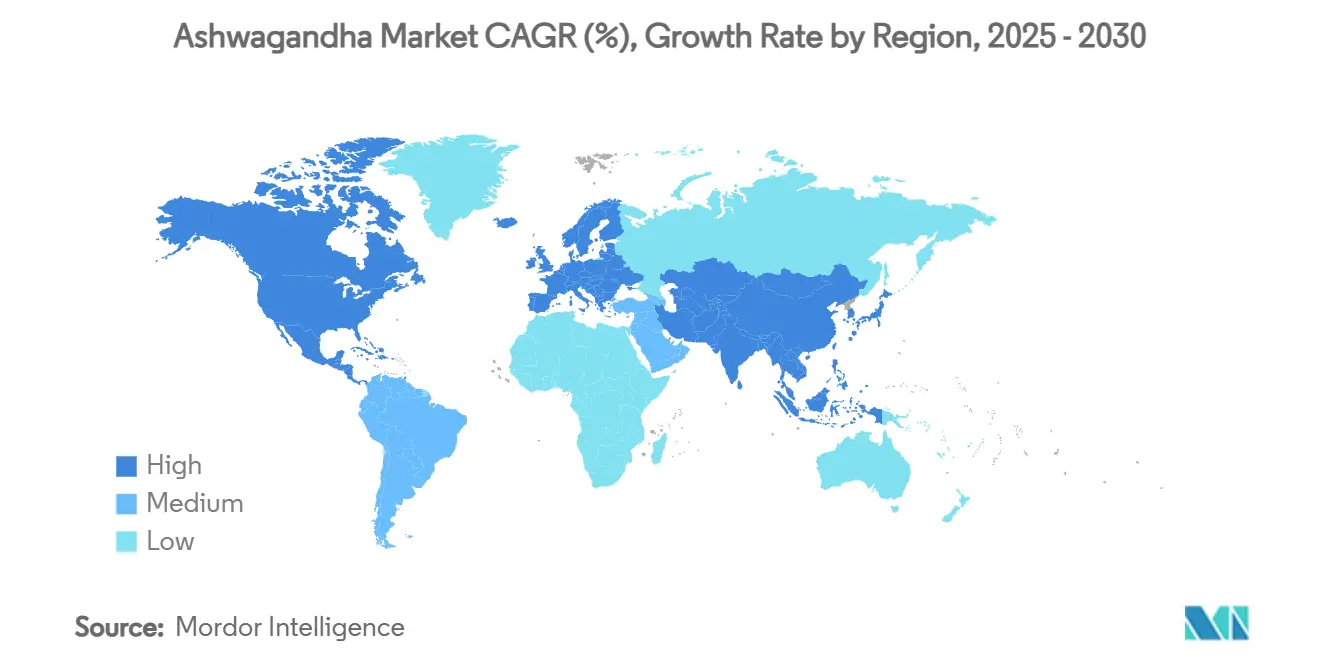

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ashwagandha Market Analysis by Mordor Intelligence

The Ashwagandha Market size is estimated at USD 0.76 billion in 2025, and is expected to reach USD 1.18 billion by 2030, at a CAGR of 9.20% during the forecast period (2025-2030).

This expansion stems from the herb’s progression from an Ayurvedic staple to a mainstream wellness asset, bolstered by mounting peer-reviewed evidence of cortisol-lowering efficacy, accelerating e-commerce penetration, and sustained product innovation across supplements, foods, and beverages. Rapid uptake in the United States after the pandemic catalyzed global momentum, while vertical integration among leading extract suppliers helped mitigate raw-material inflation. At the same time, heightened regulatory scrutiny in parts of Europe underscores the necessity of rigorous safety dossiers, pushing manufacturers toward clinically validated, traceable supply chains. Market opportunities are increasingly tied to differentiated delivery formats, functional food launches, and emerging veterinary applications, even as commodity suppliers face rising quality-control barriers.

Key Report Takeaways

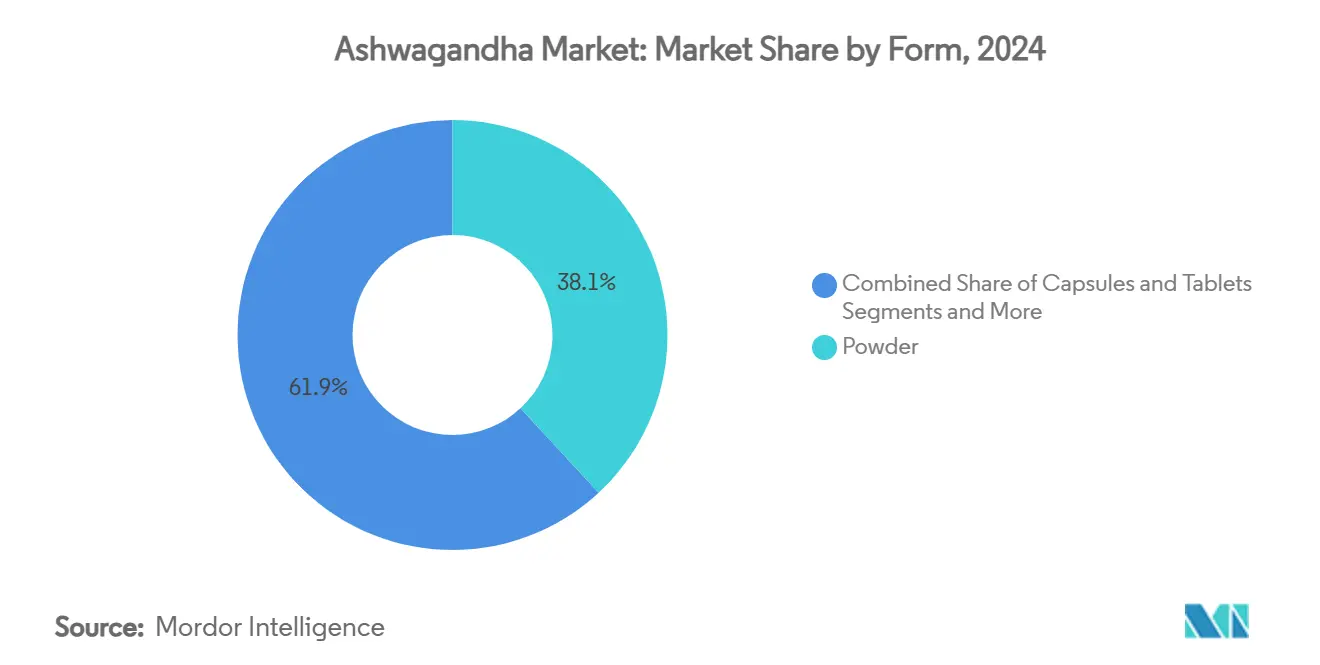

- By form, powder retained 38.1% of the Ashwagandha market share in 2024, whereas gummies and chews are advancing at a 12.8% CAGR through 2030.

- By application, dietary supplements captured 62.5% of the ashwagandha market share in 2024, but functional foods and beverages are projected to grow at a 15.6% CAGR to 2030.

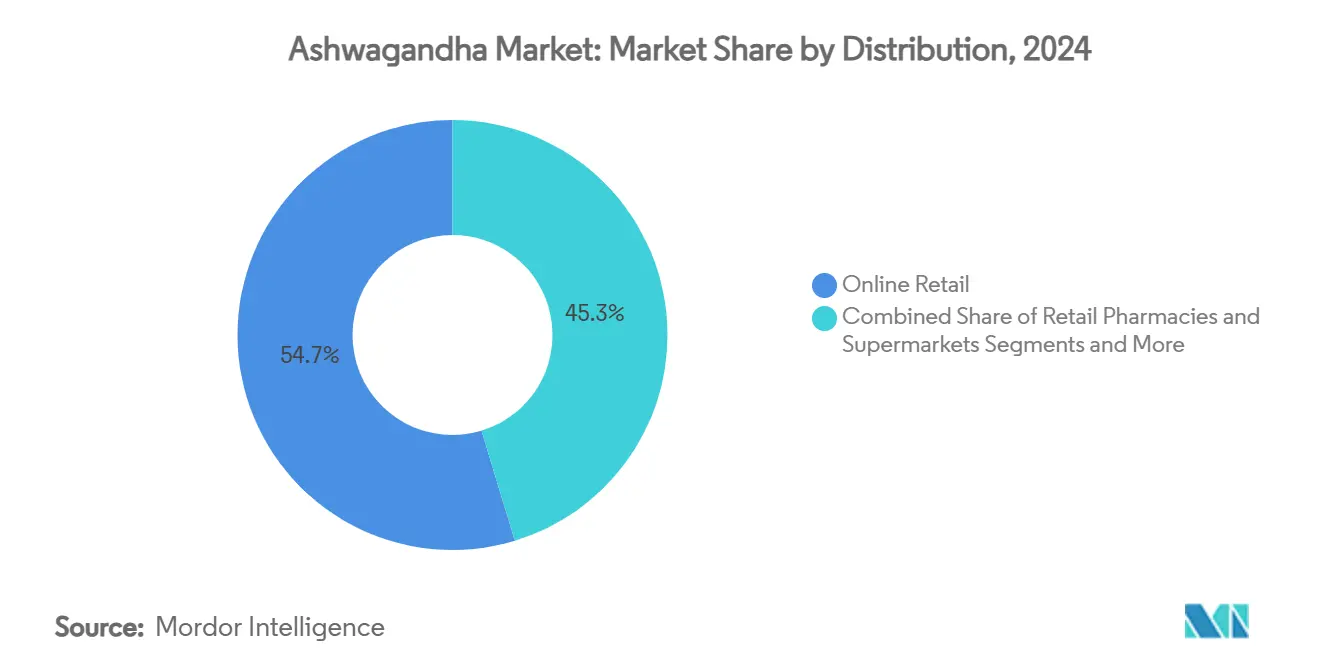

- By distribution, online retail captured 54.7% of the ashwagandha market revenue share in 2024, and direct-to-consumer channels are set to post a 13.4% CAGR between 2025-2030.

- By geography, North America led with 38.7% revenue contribution in 2024, while Asia-Pacific is on track for a 9.40% CAGR through 2030.

Global Ashwagandha Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid demand for stress-support nutraceuticals | +2.10% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Expansion of e-commerce supplement sales | +1.80% | Global, led by North America & Asia Pacific | Short term (≤ 2 years) |

| Clinical validation of branded extracts (KSM-66, Sensoril) | +1.50% | Global, regulatory-sensitive markets | Long term (≥ 4 years) |

| Entry of beverage brands using water-soluble ashwagandha | +1.20% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Government subsidies for medicinal-herb farming in India | +0.90% | Global supply impact, India-centric production | Long term (≥ 4 years) |

| Adoption in pet wellness products | +0.70% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Demand for Stress-Support Nutraceuticals

Escalating stress levels since 2020 shifted consumer purchasing toward adaptogens, positioning Ashwagandha as the top mood-support botanical by revenue. Randomized trials have documented cortisol reductions of up to 67%, reinforcing practitioner confidence and stimulating premium product launches.[1]Mishra Deo Nidhi & Manoj Kumar, “Shoden Promotes Relief from Stress and Anxiety,” ScienceDirect, sciencedirect.com Consistent results across adult and pediatric cohorts broaden the addressable user base, while new product formats such as liquid shots and micro-encapsulated powders help brands differentiate. Multinational beverage firms are incorporating standardized extracts into ready-to-drink SKUs to address daily stress needs, further embedding the herb in mainstream wellness routines, thereby driving the ashwagandha market.

Expansion of E-commerce Supplement Sales

Digital channels now account for the majority of global Ashwagandha market transactions, driven by subscription models, algorithm-based product recommendations, and direct-to-consumer brand strategies. Online platforms enhance transparency through ingredient traceability dashboards and user-generated reviews, factors that build trust in an herb with centuries-old ethnopharmacological roots. Lower entry barriers allow niche brands to compete, although rising sponsored-ad costs favor clinically validated SKUs with higher price realization.

Clinical Validation of Branded Extracts

Proprietary extracts such as KSM-66, Sensoril, and Shoden have amassed more than 40 human trials combined, substantiating claims for stress, sleep, cognition, and sports performance. Regulatory agencies in Canada and select Asia-Pacific jurisdictions now reference these datasets when reviewing product dossiers, giving clinically supported suppliers a decisive edge. The high cost of double-blind trials acts as a deterrent for late entrants, effectively concentrating value among research-active producers and their finished-product partners.

Entry of Water-Soluble Formats in Beverages

Technological breakthroughs in dispersibility and taste masking enable Ashwagandha integration into sparkling waters, juices, and shots without the earthy bitterness of raw powder. Early-stage launches have gained shelf presence in natural grocery chains and convenience outlets, tapping consumers who prefer drinkable wellness. Brands leverage GRAS-affirmed extracts to sidestep supplement-specific label restrictions, while positioning products for on-the-go stress relief.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -1.40% | Global, India supply-dependent markets | Short term (≤ 2 years) |

| Adulteration & quality-control failures | -1.10% | Global, particularly powder formulations | Medium term (2-4 years) |

| Emerging liver-toxicity case reports | -0.90% | Europe & regulatory-sensitive markets | Medium term (2-4 years) |

| Tight Canadian/European health-claim regulations | -0.80% | Canada, EU, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Heavy reliance on farms in arid Indian regions exposes supply chains to monsoon variance and logistics disruptions. Sharp farm-gate price spikes during adverse weather have compressed gross margins for formulators lacking long-term contracts. Government incentive schemes for medicinal-plant cultivation are expanding acreage, yet the six-month crop cycle limits near-term elasticity.[2]Press Information Bureau, “Measures Taken to Promote the Cultivation of Medicinal Plants,” pib.gov.in

Adulteration and Quality-Control Failures

DNA barcoding studies have found non-authentic material in nearly one-quarter of market samples, with powder products most vulnerable. Leaf substitution introduces Withaferin-A levels that can exceed safe intake guidelines, elevating safety-review flags at national agencies. Rigorous identity testing, root-only sourcing pledges, and third-party certifications are becoming table stakes for brand survival amid growing professional-health-care oversight.[3]Amritha Nagendraprasad et al., “Authentication of Market Samples of Ashwagandha,” ScienceDirect, sciencedirect.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Gummies Gain Ground Among New Users

Powder retained leadership, accounting for 38.1% of the Ashwagandha market in 2024 on the back of cost efficiency and formulation versatility. However, gummies and chews are expanding at a 12.8% CAGR as consumers migrate toward pill-free, flavor-forward supplementation options. The gummy surge is particularly pronounced among millennials and adults averse to large capsules, widening consumer reach for the Ashwagandha market. Manufacturers embracing pectin-based matrices and natural sweeteners have overcome prior texture challenges, while eco-friendly packaging appeals to sustainability-oriented buyers.

Although powder formats will preserve scale advantages, their susceptibility to adulteration is spurring investment in traceability protocols. Meanwhile, beverage-compatible liquid extracts carry premium price tags tied to higher withanolide standardization guarantees. Across formats, water-soluble granules and nano-emulsions are enabling clean-label formulations in energy drinks and relaxation shots, supporting long-run diversification of the Ashwagandha industry.

By Application: Functional Foods Outpace Supplements

Dietary supplements still captured 62.5% of the Ashwagandha market size in 2024, yet functional foods and beverages are on a 15.6% CAGR trajectory through 2030. This acceleration mirrors broader consumer acceptance of everyday foods fortified for mood, sleep, and focus benefits. Beverage launches with 200 mg standardized extract per serving play to convenience-driven shoppers, while sports powders target endurance and recovery niches. Clinical meta-analyses observe VO₂max improvements of 4.1 ml/min/kg in trained adults, anchoring athletic-performance positioning.[4]Ranil Jayawardena et al., “Effect of Ashwagandha on Sports Performance,” Journal of Sports Medicine, journalofsportsmedicine.org

Cosmetic and personal-care applications remain nascent but promising, leveraging antioxidant properties for anti-aging serums. P harmaceutical prospects hinge on future trials assessing anxiety-disorder endpoints, although regulatory hurdles remain high. Application breadth helps dilute channel risk and rewards suppliers that can tailor particle size, flavor profile, and bioavailability to category-specific needs.

By Distribution: Direct-to-Consumer Accelerates Margin Capture

Online retail controlled 54.7% of the ashwagandha market revenue in 2024, riding a pandemic-era leap in supplement e-commerce. Within this sphere, direct-to-consumer brands are growing at 13.4% CAGR by bundling subscription replenishment with lifestyle content, effectively locking in repeat orders. Brick-and-mortar pharmacies still cater to older demographics seeking pharmacist reassurance, but shelf space is contracting as retailers rationalize SKUs. Supermarkets have carved out functional-beverage end-caps, exposing the Ashwagandha market to impulse purchasers outside supplement aisles.

Geography Analysis

North America remained the single largest region, reflecting robust dietary-supplement penetration and an accommodating regulatory framework. The United States alone absorbed more than one-third of global finished-product sales in 2024, aided by extensive direct-to-consumer advertising and health-practitioner endorsements. Canada’s recent novel-food approval for a standardized extract illustrates the region’s openness to clinically backed dossiers, reinforcing a premium-priced segment for the Ashwagandha market.

Asia-Pacific continues to gain momentum in the ashwagandha market with a forecast 9.40% CAGR through 2030. Rising middle-class incomes in China, South Korea, and Japan have accelerated demand for natural anti-stress solutions, while India’s domestic market benefits from government Ayush campaigns that position the herb as a daily immunity booster. Regulatory heterogeneity persists across the bloc, yet locally adapted labeling and traditional-medicine registrations ease entry for suppliers allied with regional contract manufacturers.

Europe presents a more complex outlook. Denmark’s 2022 prohibition and subsequent warnings from France and the Netherlands prompted heightened product-safety evaluations, slowing near-term uptake. Nevertheless, dossiers featuring root-only, low-withaferin A extracts are gaining conditional clearances, and pharmacovigilance data may eventually support a harmonized intake threshold. Elsewhere, the Middle East and Africa remain frontier territories, while Latin America’s adoption is tempered by currency volatility and fragmented distribution infrastructures.

Competitive Landscape

Moderate fragmentation characterizes the Ashwagandha market, with scale advantages accruing to companies that own farms, extraction facilities, and research pipelines. Ixoreal Biomed’s KSM-66, Natreon’s Sensoril, and Arjuna Natural’s Shoden together supplied roughly one-third of branded extract tonnage in 2024, underpinned by more than 40 peer-reviewed trials. Vertical integration shields these firms from raw-material price swings and supports consistent withanolide titration, a key differentiator for multinational supplement and beverage customers.

Strategic alliances between extract producers and consumer-brand houses are proliferating, often structured as co-branded ingredient labeling that signals quality to end users. New-product pipelines are tilting toward water-soluble granules, effervescent powders, and liposomal liquids aimed at expanding the Ashwagandha market into beverage and sports-nutrition segments. Meanwhile, commodity suppliers anchored in bulk-powder exports face eroding price premiums due to sustained scrutiny over leaf adulteration and heavy-metal contamination. Market entrants lacking clinical data now confront higher barriers as retailers integrate safety-certificate audits into vendor onboarding.

A potential consolidation wave looms as midsize processors seek investment to upgrade to pharma-grade production or exit under cost pressure. Intellectual-property stakes around extraction technologies and bio-availability enhancements further raise the bar for emergent participants, suggesting a gradual shift toward an oligopolistic equilibrium within the Ashwagandha market.

Ashwagandha Industry Leaders

Ixoreal Biomed

Natreon Inc.

Arjuna Natural Pvt Ltd

Himalaya Wellness

Dabur India Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Arjuna Natural received Health Canada approval for Shoden, enabling stress-management and sleep-improvement claims.

- September 2024: The UK Food Standards Agency initiated a safety assessment of Ashwagandha supplements.

- August 2024: Organic India debuted 300 mg Ashwagandha gummies in reusable glass jars.

Global Ashwagandha Market Report Scope

| Powder |

| Capsules & Tablets |

| Liquid Extracts |

| Gummies & Chews |

| Dietary Supplements |

| Functional Foods & Beverages |

| Sports Nutrition |

| Pharmaceuticals |

| Cosmetics & Personal Care |

| Retail Pharmacies |

| Online Retail |

| Health Stores |

| Supermarkets/Hypermarkets |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Form | Powder | |

| Capsules & Tablets | ||

| Liquid Extracts | ||

| Gummies & Chews | ||

| By Application | Dietary Supplements | |

| Functional Foods & Beverages | ||

| Sports Nutrition | ||

| Pharmaceuticals | ||

| Cosmetics & Personal Care | ||

| By Distribution Channel | Retail Pharmacies | |

| Online Retail | ||

| Health Stores | ||

| Supermarkets/Hypermarkets | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the global Ashwagandha market?

The Ashwagandha market size reached USD 0.76 billion in 2025 and is projected to hit USD 1.18 billion by 2030.

Which form of Ashwagandha is growing fastest?

Gummies and chews are expanding at a 12.8% CAGR through 2030 as consumers favor convenient, palatable formats.

Which region leads Ashwagandha sales?

North America held 38.7% revenue share in 2024 due to high supplement penetration and favorable regulations.

Why are branded extracts important?

Clinically validated extracts such as KSM-66 and Shoden possess extensive human-trial evidence that supports health claims and eases regulatory approvals.

What are the main risks facing the Ashwagandha industry?

Key challenges include raw-material price swings linked to India-centric production, adulteration in powder formats, and emerging liver-toxicity case reports prompting stricter oversight.

How will functional foods influence market growth?

Functional foods and beverages are set to grow at 15.6% CAGR, broadening Ashwagandha intake beyond traditional supplement users.

Page last updated on: