Translation Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

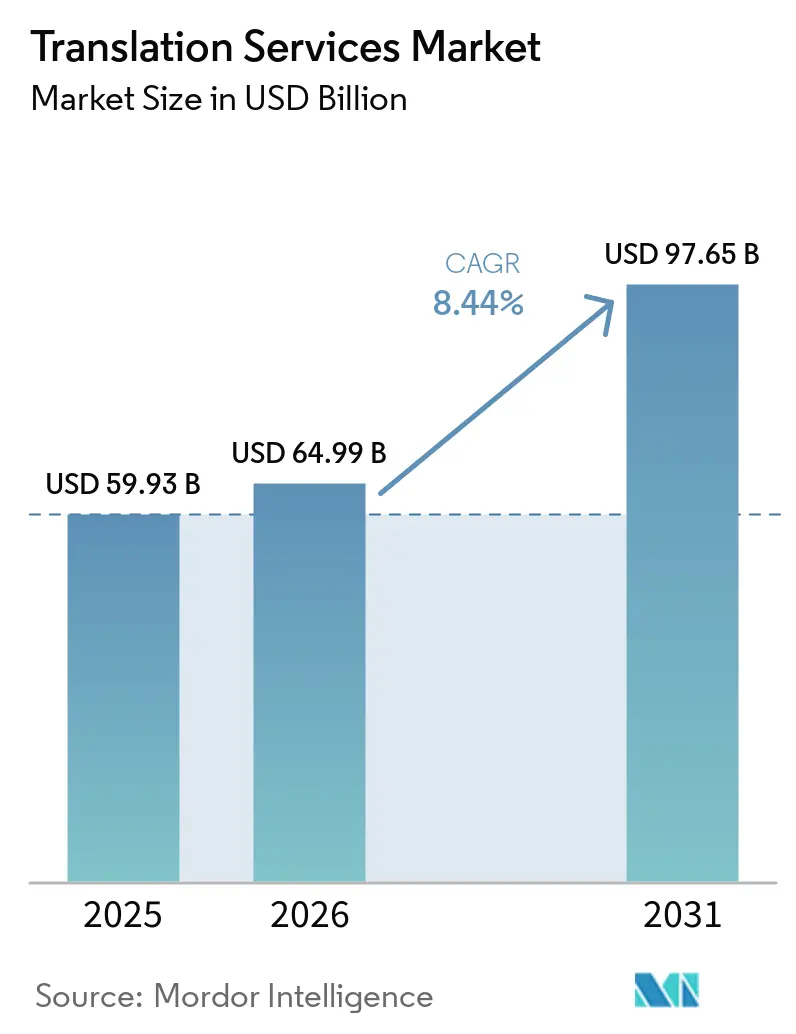

| Market Size (2026) | USD 64.99 Billion |

| Market Size (2031) | USD 97.65 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

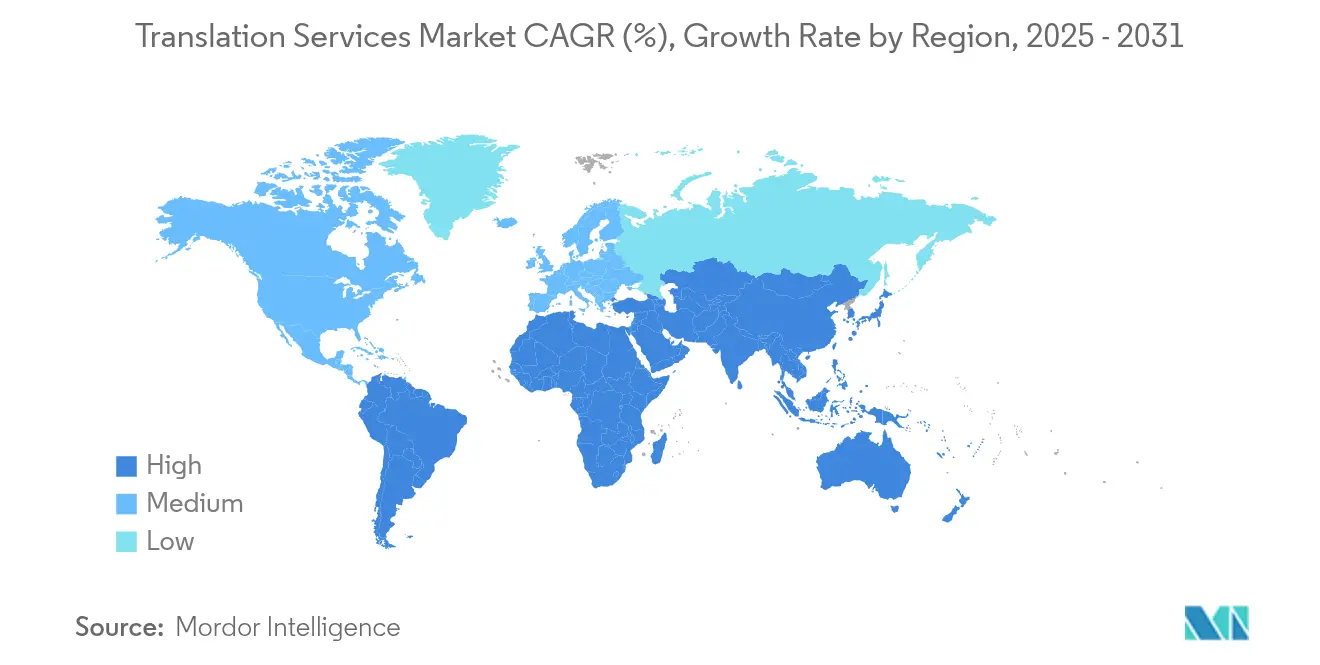

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Translation Services Market Analysis by Mordor Intelligence

Translation services market size in 2026 is estimated at USD 64.99 billion, growing from 2025 value of USD 59.93 billion with 2031 projections showing USD 97.65 billion, growing at 8.44% CAGR over 2026-2031. Growth reflects regulatory mandates that oblige healthcare providers to offer qualified interpreters, the move by global software firms toward continuous localization, and sharp increases in streaming and gaming content that demands culturally nuanced adaptation. Software-led automation is transforming cost structures as neural machine translation reduces post-editing time by up to 80%, while integrated DevOps pipelines replace traditional project workflows. Private-equity-backed consolidation is opening scale efficiencies, yet fragmentation persists because the top 100 vendors still control only 15% of sector revenue. Asia-Pacific’s mobile-first digital economy supplies the fastest incremental volumes, even as Europe retains leadership through long-standing multilingual compliance obligations.

Key Report Takeaways

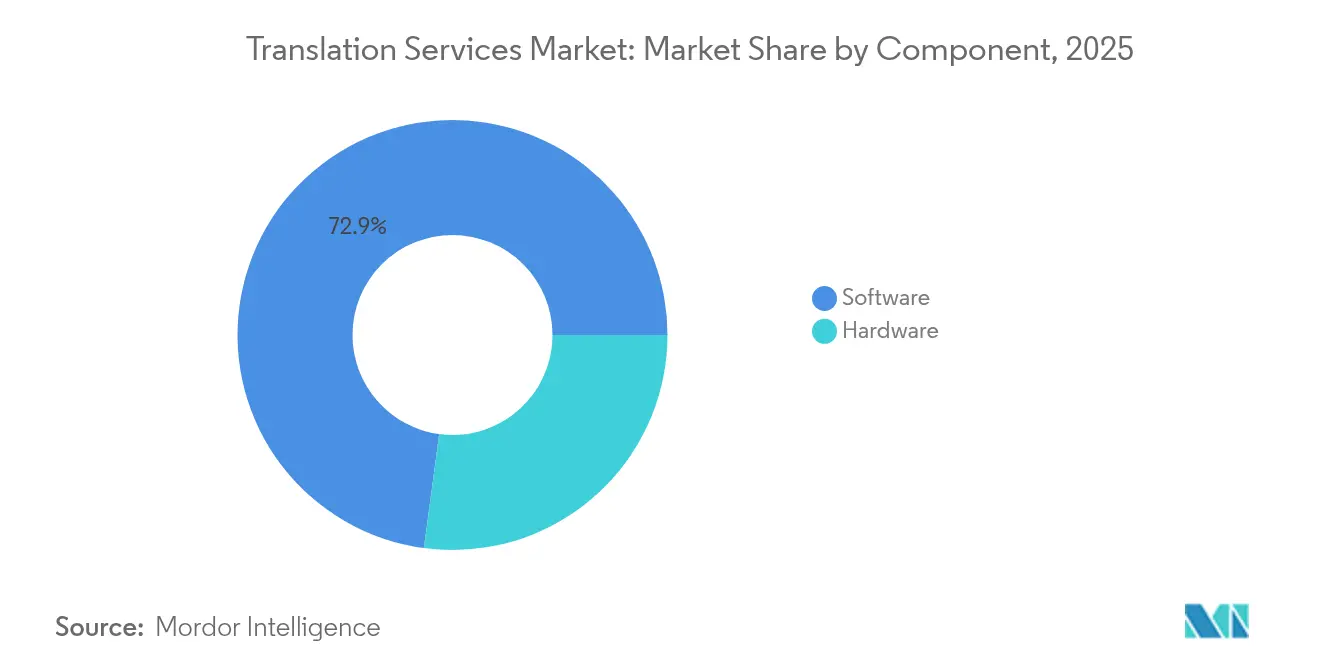

- By component, software solutions held 72.88% of the translation services market share in 2025, whereas cloud-native platforms are projected to expand at a 10.34% CAGR to 2031.

- By operation, machine and neural machine translation accounted for 61.25% of the translation services market size in 2025, and the neural MT with post-editing niche is set to grow at 10.76% through 2031.

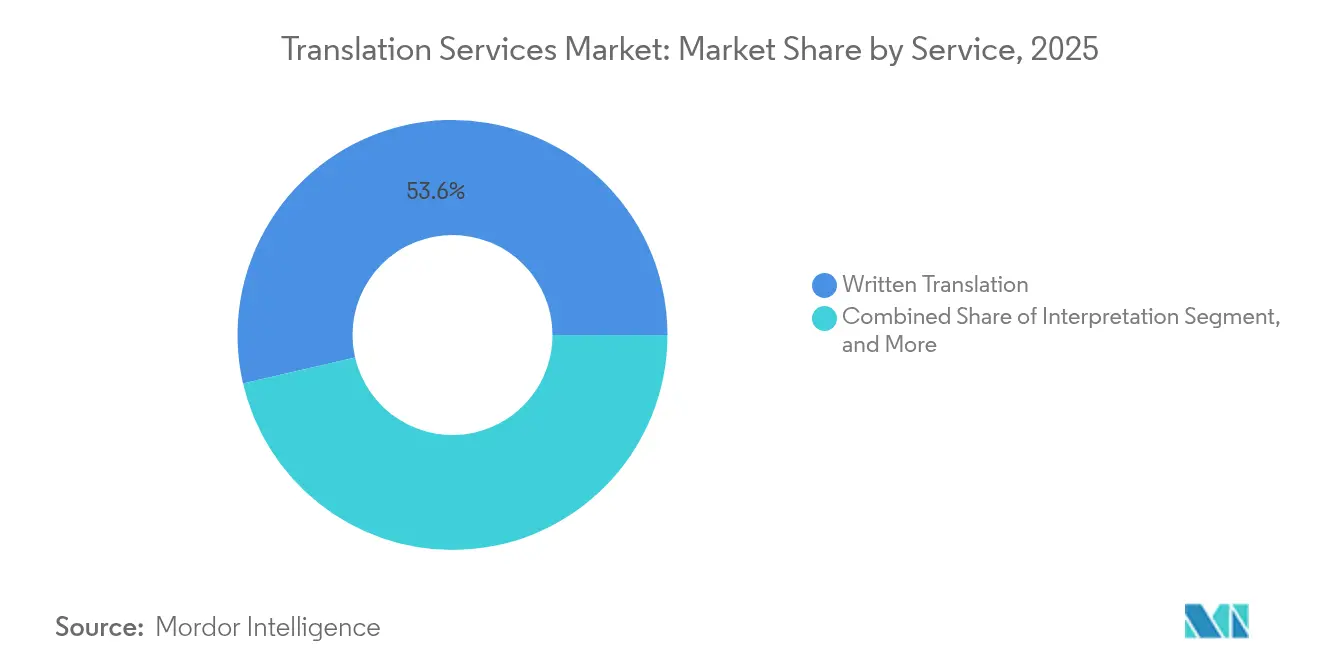

- By service, written translation dominated with 53.62% revenue share in 2025; transcreation and multimedia localization are progressing at a 12.79% CAGR to 2031.

- By end-user, IT and telecom led with a 32.55% hold on 2025 revenue, while the media and gaming segment is on track for the fastest 12.43% CAGR through 2031.

- By geography, Europe commanded 44.12% of 2025 global revenue; Asia-Pacific is anticipated to surge at a 15.02% CAGR to 2031.

- Consolidation remains active: Teleperformance’s USD 1.5 billion purchase of LanguageLine Solutions illustrates private-equity appetite for scale assets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Translation Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of global e-commerce | +2.1% | Global, Asia-Pacific leading | Medium term (2-4 years) |

| Explosion of multimedia/streaming content | +1.8% | North America and Europe | Short term (≤ 2 years) |

| Regulatory push for language access in public services | +1.4% | North America and EU | Long term (≥ 4 years) |

| Accelerating cross-border SaaS deployments | +1.6% | Global, enterprise hubs | Medium term (2-4 years) |

| Shift to continuous localization pipelines | +1.3% | Global, tech sector | Short term (≤ 2 years) |

| Mobile-commerce dominance in emerging markets | +1.0% | Asia-Pacific and LATAM | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of Global E-Commerce

Online retail sales are heading toward USD 7.4 trillion in 2025 as buyers demand native-language experiences; 76% of shoppers decline purchases when content is not localized.[1]Bureau Works, “Why Localization Matters,” bureauworks.comRetailers now translate everything from checkout flows to post-sale support, which lifts revenue performance by 1.5 times for firms that invest in end-to-end localization. City-level cultural tailoring is emerging as brands pursue hyper-local resonance, a nuance machine translation alone cannot guarantee. The smartphone surge in emerging markets fuels voice-to-text translation features that let retailers reach first-time mobile buyers. These dynamics collectively raise transaction conversion rates and sustain recurring demand for the translation services market.

Explosion of Multimedia/Streaming Content

Subscriber growth on global platforms is steering demand toward multilingual subtitles, dubbing, and voice synthesis. AI captioning now cuts production cycles by 60% while retaining emotional fidelity through neural speech cloning.[2]Streaming Media Global, “AI Dubbing Trends 2024,” streamingmediaglobal.com Netflix-style quality frameworks have spawned certification courses that blend technical and cultural skills. Gaming studios mirror this trend by localizing character voices and narratives; titles localized into 14 languages have multiplied revenue across Southeast Asia. Added to this is the rise of live-event interpretation, which broadens revenue streams for language service providers and intensifies competition within the translation services market.

Regulatory Push for Language Access in Public Services

Section 1557 of the Affordable Care Act obliges U.S. health systems to provide qualified interpreters across the 15 most-spoken local languages starting July 2025. Federal agencies must also translate vital documents into the 12 top non-English languages, ensuring a dependable pipeline of work for certified linguists. Machine translation may support triage but must be human-reviewed for clinical accuracy, anchoring hybrid models that blend AI speed with human oversigh. Similar rules now require Braille, large-print, and other accessible formats, widening the definition of language access. Collectively, these mandates secure predictable, compliance-driven growth for the translation services market.

Accelerating Cross-Border SaaS Deployments

Software companies are embedding localization APIs directly into agile DevOps workflows, shrinking release cycles from months to weeks.[3]Smartling, “Continuous Localization in DevOps,” smartling.com Applications that practise continuous localization have seen 128% jumps in downloads and 26% revenue gains. Mobile-first strategies in emerging regions oblige linguistic and design tailoring for character-dense scripts such as Chinese and Japanese. Dynamic pricing localization further maximizes market penetration by aligning subscription models with local purchasing power. This evolution cements the translation services market as an operational layer in global software delivery rather than an after-the-fact service.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and security concerns | -1.2% | EU and North America | Long term (≥ 4 years) |

| Shortage of qualified domain-specialist linguists | -0.9% | Global | Medium term (2-4 years) |

| “Good-enough” free machine translation | -1.1% | Global | Short term (≤ 2 years) |

| Gen-AI hallucination risk in regulated verticals | -0.7% | Healthcare and legal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Security Concerns

GDPR forces vendors to route EU source text through regional data centers and maintain ISO 27001 controls, raising operating expenses by up to 20%. Enterprises handling sensitive legal or financial documents increasingly insist on on-premises or private-cloud workflows to avert breaches that free online engines might invite. HIPAA overlays further escalate costs for U.S. healthcare content, a barrier that deters smaller providers from scaling. Fragmented global privacy statutes amplify admin workloads, tempering the translation services market growth outlook.

Shortage of Qualified Domain-Specialist Linguists

Technical, legal, and medical content needs linguists who pair language mastery with subject expertise; such professionals remain scarce and command premium pay.[4]Atlas Language Services, “Specialist Linguist Talent Shortage,” atlasls.com The job now also demands familiarity with AI post-editing and data-training tasks. Geographic clustering in major cities complicates scale for rare-language or niche-domain projects. Remote work has widened the talent pool but intensified wage competition, contributing to margin pressure within the translation services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Accelerates AI Integration

Software systems generated 72.88% of the translation services market share in 2025 and are forecast to widen their lead at a 10.34% CAGR. Neural-enhanced translation management systems cut project turnarounds by up to 80%, enabling enterprises to scale global content without proportional staffing. Cloud-native architectures integrate with e-commerce, CRM, and CMS platforms through open APIs, turning localization into a continuous background process.

Hardware retains presence for on-premises conference interpretation and secure healthcare kiosks, yet its revenue weight is sliding as workloads migrate to cloud services. Translation memories now operate as neural suggestion engines that lift domain-specific accuracy to 90%, and automated QA modules use large language models to flag anomalies in a fraction of the time needed by manual reviewers. These advances underscore the structural shift from labor-intensive workflows to technology-centric models that underpin the translation services market.

By Operation: Neural Machine Translation Reshapes Workflows

Machine and neural machine translation streams captured 61.25% of 2025 revenues. Neural MT with targeted post-editing is poised for an 10.76% CAGR because enterprises accept 80% machine-quality output that costs 80% less and arrives 10 times faster. Domain-critical fields such as pharmaceuticals and litigation still require human first-pass translations to mitigate liability, yet hybrid setups prevail elsewhere.

Providers now sell “engine-agnostic” pipelines that automatically pick the best model per language pair, then send results to linguists for light edits. Translators themselves are becoming data curators who train custom engines and monitor outputs for hallucinations. These role shifts are redefining skills demand across the translation services market.

By Service: Transcreation Drives Premium Growth

Written translation remained the anchor with 53.62% of 2025 revenue, but transcreation and multimedia localization are racing ahead at 12.79% CAGR as brands seek emotional authenticity. Multimedia workflows—dubbing, subtitling, voice-over—require audio engineering and lip-sync skills that push pricing 40-60% above text work.

Video remote interpreting and over-the-phone interpreting platforms are scaling 24/7 language access in healthcare and customer support, while onsite interpretation still rules courtroom and boardroom settings where body language matters. Clients increasingly bundle services to guarantee brand consistency, a trend that is enlarging the full-suite appeal of the translation services market.

By End-User: Media and Gaming Accelerate Digital Transformation

IT and telecom accounted for 32.55% of 2025 demand, anchored by product documentation and software interface localization. Media and gaming, however, will be the fastest riser at 12.43% CAGR to 2031 as streaming libraries and mobile titles localize storylines, character voices, and in-game events for Southeast Asian audiences valued at USD 40 billion.

Financial services continue to translate customer disclosures and regulatory filings, while life sciences prioritize clinical trial protocols where precision is non-negotiable. Automotive and manufacturing adopt localization for electric-vehicle manuals, and public agencies rely on certified translations for immigration and social services. Collectively these verticals broaden the addressable base for the translation services market.

Geography Analysis

Europe generated 44.12% of global revenue in 2025, supported by GDPR-driven multilingual documentation across 24 official languages. Demand remains durable as corporations headquartered in Germany, France, and the UK must file technical and legal content in multiple languages. Brexit complexities add volume as UK firms navigate overlapping EU and domestic regulations, sustaining premium pricing for specialized legal translations.

Asia-Pacific is advancing at a 15.02% CAGR and threatens Europe’s lead by 2031. China, Japan, and South Korea are funneling investment into neural MT research, while Southeast Asian gaming studios localize content across Bahasa Indonesia, Thai, Tagalog, and Vietnamese to capture smartphone-native audiences. Mobile commerce dominance also fuels voice translation tools, intensifying growth in the translation services market.

North America maintains a robust compliance-driven base: U.S. federal agencies spend USD 700–800 million a year on outsourced language services for courts, immigration, and public health. Section 1557 enforcement spurs hospital spending on interpreters, and Silicon Valley’s SaaS exporters keep pushing continuous localization practices. Canada’s bilingual statutes and Mexico’s manufacturing-supply-chain role further diversify regional demand.

Competitive Landscape

The sector remains fragmented despite USD 1.5 billion megadeals, as the top 100 suppliers still hold only 15% of global billings. TransPerfect surpassed USD 1.2 billion revenue in 2023 by layering its GlobalLink platform with generative AI modules that automate intake, routing, and quality checks. RWS shifted toward technology-centric services after absorbing SDL, making its Language Weaver engine the default for 55% of first-pass content.

DeepL’s superior BLEU scores have prompted many vendors to embed its API, forcing incumbents to renegotiate workflows or risk margin erosion. Private-equity funds are orchestrating roll-up plays; Teleperformance’s LanguageLine purchase stands out, alongside serial buyers such as Propio Language Services. The scramble now centers on proprietary AI, domain-trained data, and secure delivery models that can satisfy regulated clients.

White-space growth lies in hybrid human-AI offerings, API-first localization toolkits, and specialized engine fine-tuning for legal or life-science terminology. Firms that pair scalable software with certified human oversight are carving defensible niches, while pure play “word factories” face accelerating commoditization.

Translation Services Industry Leaders

TransPerfect

Lionbridge

LanguageLine Solutions

Acolad Group

RWS Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Phrase and Welocalize expanded a strategic alliance to merge Phrase’s localization platform with Welocalize’s global delivery network, boosting automation and scale efficiencies.

- July 2024: DeepL released a next-gen model that exceeded ChatGPT-4, Google, and Microsoft in blind tests, delivering 90% time savings and 345% ROI for enterprise clients.

- December 2024: RWS Group acquired Dublin-based Propylon Holdings to deepen its foothold in regulated-industry content management and localization.

- July 2024: Lionbridge rolled out Aurora AI, a content orchestration engine that streamlines translation workflows for gaming, IT, and e-commerce customers.

Global Translation Services Market Report Scope

Translation services are professional services that help bridge language barriers by providing accurate translations of various types of documents, texts, and content. These services are crucial in today's globalised world, where effective communication is essential for businesses, organisations, and individuals.

The translation services market is segmented by component (hardware, software), by operation (technical translation, machine translation), by service (written translation services, interpretation services), by end-user (IT and telecom, BFSI, automotive, legal, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Human Technical Translation |

| Machine / Neural Machine Translation |

| Written Translation |

| Interpretation (On-site, OPI, VRI) |

| Transcreation and Multimedia Localisation |

| IT and Telecom |

| BFSI |

| Automotive and Manufacturing |

| Healthcare and Life-Sciences |

| Legal and Public Sector |

| Media, Gaming and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| By Operation | Human Technical Translation | ||

| Machine / Neural Machine Translation | |||

| By Service | Written Translation | ||

| Interpretation (On-site, OPI, VRI) | |||

| Transcreation and Multimedia Localisation | |||

| By End-User | IT and Telecom | ||

| BFSI | |||

| Automotive and Manufacturing | |||

| Healthcare and Life-Sciences | |||

| Legal and Public Sector | |||

| Media, Gaming and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and forecast value of the translation services market?

The market is valued at USD 64.99 billion in 2026 and is expected to climb to USD 97.65 billion by 2031, reflecting a 8.44% CAGR.

Which component leads the translation services market today?

Software platforms dominate, holding 72.88% of 2025 revenue, and they are growing faster than any other component as enterprises embed AI-driven localization into core workflows.

Why is Asia-Pacific the fastest-growing region?

Mobile-first digital adoption, heavy investment in neural machine translation by China and Japan, and a USD 40 billion mobile-gaming localization surge across Southeast Asia are propelling the region at a 15.02% CAGR.

How are regulatory mandates influencing demand?

Healthcare language-access rules under Section 1557 in the United States and similar initiatives in the EU are driving steady, compliance-driven spending on certified translation and interpretation services.

Page last updated on: