Telecom Managed Services Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

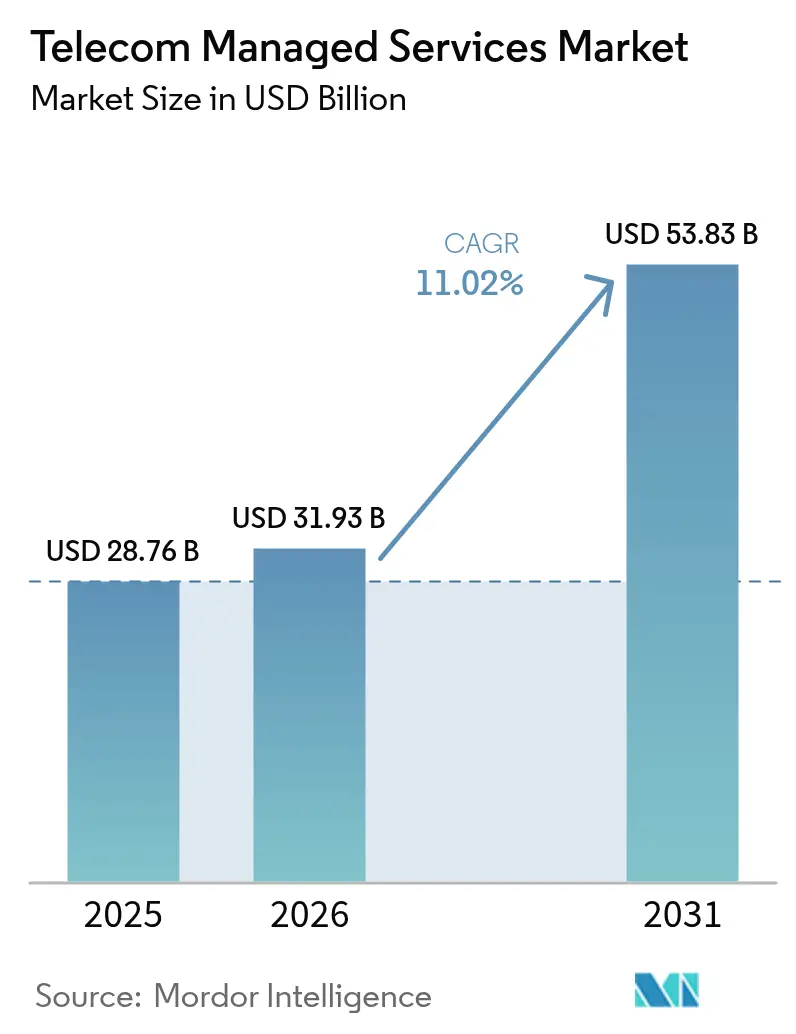

| Market Size (2026) | USD 31.93 Billion |

| Market Size (2031) | USD 53.83 Billion |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

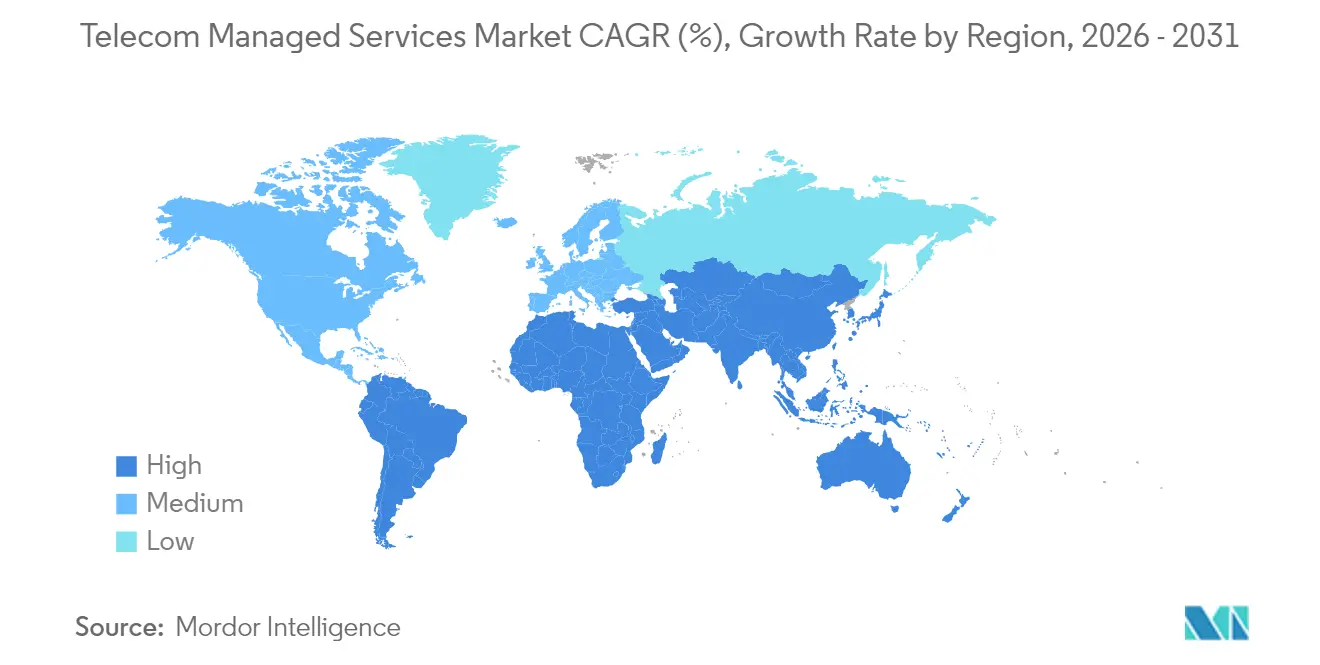

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

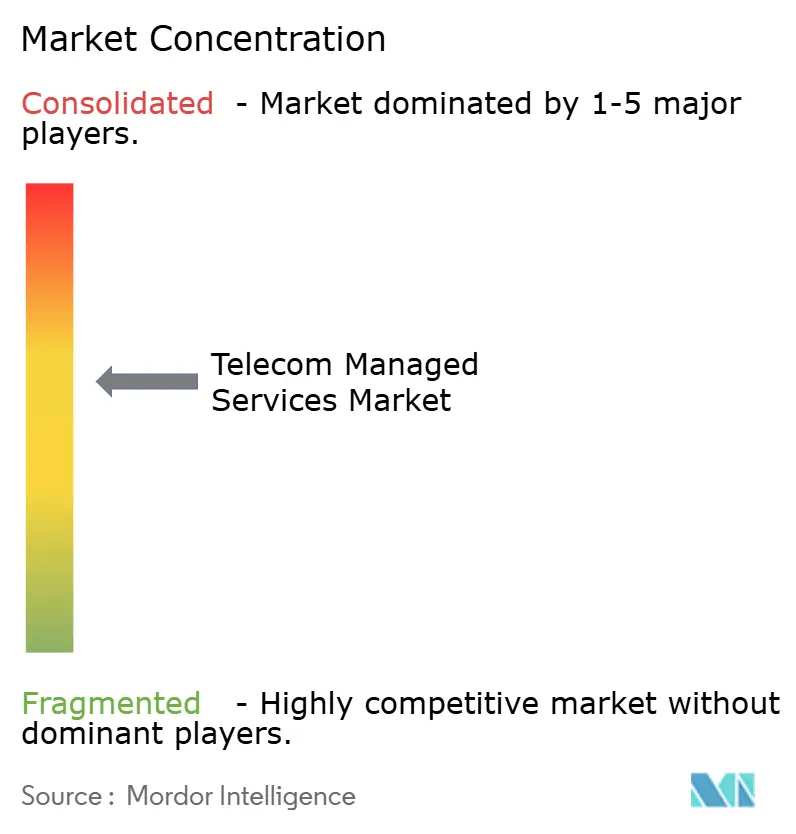

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Managed Services Market Analysis by Mordor Intelligence

The telecom managed services market size was valued at USD 28.76 billion in 2025 and estimated to grow from USD 31.93 billion in 2026 to reach USD 53.83 billion by 2031, at a CAGR of 11.02% during the forecast period (2026-2031). This translates into a 70% expansion over the forecast period, reflecting operators’ pivot from capital-intensive in-house activities to outcome-based partnerships that streamline operating costs and accelerate 5G roll-outs. Demand is strongest for cloud-hosted operations support systems because they shorten service-launch cycles and enable network automation at scale. Enterprises are adopting managed network slicing to secure predictable latency and bandwidth, while mobile operators rely on predictive maintenance to curb unplanned outages and protect revenues. Competitive bidding now revolves around AI-driven analytics, zero-trust security frameworks and multicloud orchestration skills, creating headroom for specialized providers that can guarantee performance-based SLAs.

Key Report Takeaways

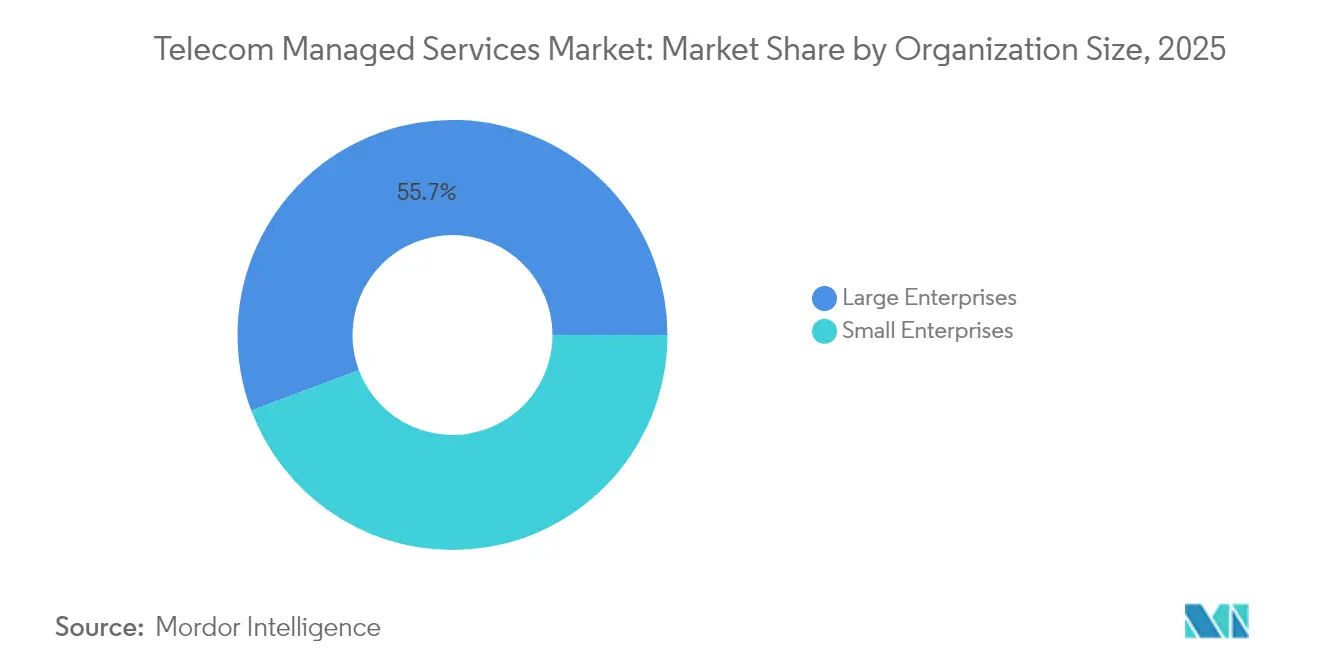

- By organization size, large enterprises led with 55.72% of telecom managed services market share in 2025, while SMEs are set to grow at 11.15% CAGR through 2031.

- By service type, managed network services held 32.08% revenue share in 2025; managed security is forecast to expand at a 11.78% CAGR to 2031.

- By deployment model, cloud-hosted platforms accounted for 62.15% of the telecom managed services market size in 2025 and are advancing at a 12.74% CAGR through 2031.

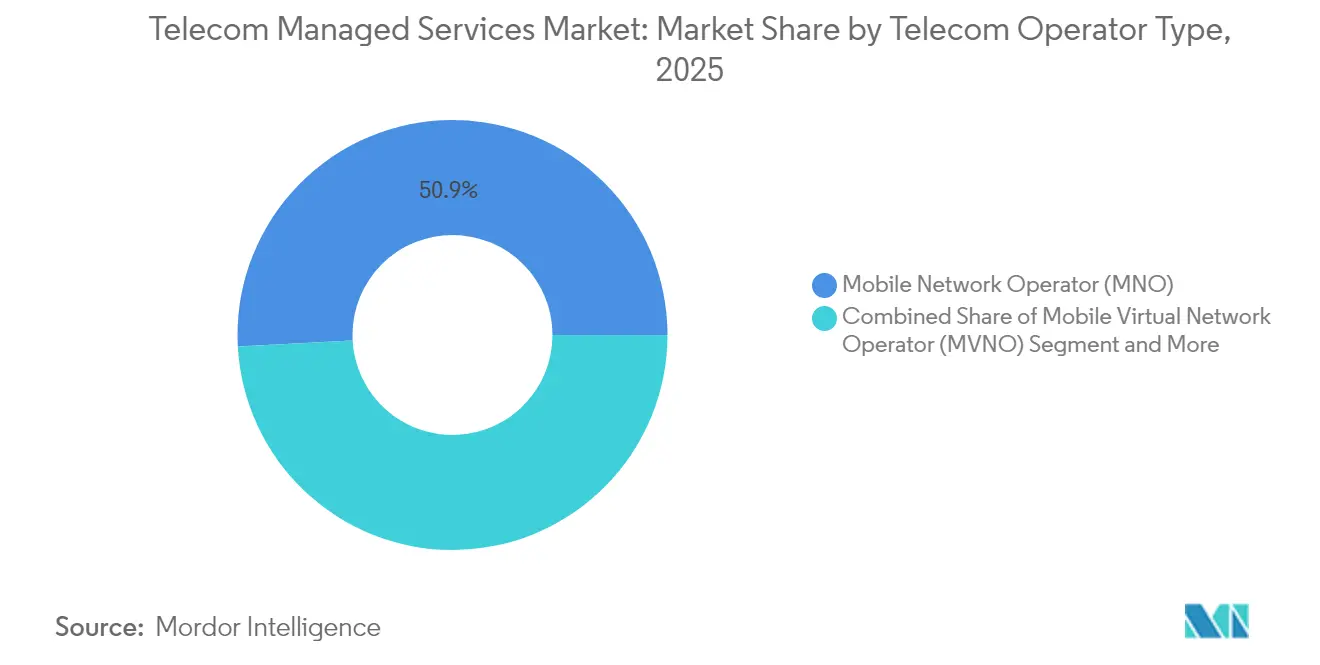

- By telecom operator, mobile network operators commanded 50.86% share of the telecom managed services market size in 2025, but internet service providers record the highest projected CAGR at 12.02% to 2031.

- By end-user vertical, the consumer segment captured 46.21% revenue share in 2025; enterprise demand is climbing at 11.91% CAGR on the back of Industry 4.0 projects.

- By geography, North America held 30.88% revenue share in 2025, whereas Asia Pacific is the fastest-growing region at an 11.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telecom Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out accelerating enterprise demand for managed network slicing | +2.1% | Global, with early gains in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Cloud-native OSS/BSS adoption among Tier-1 operators | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Shift to outcome-based SLAs lowering churn for MSPs | +1.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-driven predictive maintenance cutting OPEX | +1.6% | Global, with advanced deployment in Asia-Pacific core | Short term (≤ 2 years) |

| Demand for zero-trust architectures pushing managed security | +1.9% | Global, regulatory-driven in EU and North America | Short term (≤ 2 years) |

| Private 5G campus networks for Industry 4.0 | +1.3% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Network Slicing Drives Enterprise Transformation

Enterprise adoption of 5G network slicing is reshaping the telecom managed services market as organizations require isolated virtual networks with guaranteed performance for mission-critical applications. Verizon’s collaboration with FIFA for the 2026 World Cup highlights how event operators rely on private slices to deliver low-latency video streams and interactive fan experiences. Manufacturing leaders such as Tesla use private 5G to orchestrate autonomous production lines, pushing specialized managed service contracts that traditional IT teams cannot support. Singtel’s Southeast Asian smart-factory deployments demonstrate monetization potential by offering premium slices that lock in stringent latency and reliability targets.[1]Singtel, “Singtel powers smart manufacturing with 5G slicing,” singtel.com The complexity of simultaneously operating multiple slices each with distinct QoS parameters makes external expertise indispensable, stimulating multi-year outsourcing deals across automotive, healthcare and entertainment verticals.

Cloud-Native OSS/BSS Adoption Accelerates Operational Efficiency

Operators are migrating from monolithic systems to cloud-native architectures, generating sustained demand in the telecom managed services market. Ericsson’s cloud-native suite helped T-Mobile cut network operations costs by 30% and compress service-launch cycles from weeks to hours. Nokia’s USD 2.3 billion purchase of Infinera in 2024 indicates that integrated hardware-software portfolios are critical for seamless migration to containerized environments. Managed service providers (MSPs) supply Kubernetes engineering, CI/CD pipelines and microservices orchestration skills that remain scarce in-house. As operators decommission legacy platforms, cloud-hosted models unlock elastic scaling, enabling rapid introduction of edge computing services for industrial IoT.

AI-Driven Predictive Maintenance Transforms Network Operations

Artificial intelligence has moved network management from reactive fault handling to predictive prevention. Huawei reports 40% fewer outages among operators deploying its AI-based management suite, which analyzes multiband radio data to flag performance anomalies days in advance.[2]Huawei Technologies, “AI-enabled autonomous driving network,” huawei.com NTT Docomo’s self-optimizing network adjusts parameters on the fly, reducing manual interventions by 60% while boosting user-experience scores. Generative AI now synthesizes root-cause analyses and recommends remediation steps in real time, enabling MSPs to commit to tighter SLA thresholds and differentiate on guaranteed uptime.

Zero-Trust Security Architectures Drive Managed Security Demand

The shift toward virtualized network functions expands the attack surface, prompting operators to adopt zero-trust frameworks that authenticate every device, user and application. Palo Alto Networks found that 78% of operators intend to deploy zero-trust by 2026, yet only 23% possess sufficient internal talent.[3]Palo Alto Networks, “Zero Trust adoption in telecom 2025 survey,” paloaltonetworks.com Dish Network’s cloud-native 5G core on AWS required an end-to-end zero-trust overlay delivered by external security specialists. EU directives such as the Digital Operational Resilience Act intensify compliance pressures, steering operators toward managed security providers that combine threat intelligence, policy automation and multicloud visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skill-gap inflation in telecom DevSecOps talent | -1.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Vendor lock-in fears for cloud-hosted network functions | -0.8% | Global, regulatory concerns in EU | Medium term (2-4 years) |

| Latency-sensitive 5G URLLC use-cases limiting off-prem outsourcing | -0.6% | Asia-Pacific and North America, industrial applications | Long term (≥ 4 years) |

| Fragmented regulatory compliance across regions | -0.9% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DevSecOps Talent Shortage Constrains Service Delivery

Telecommunications DevSecOps vacancies remain open for 4.2 months on average versus 2.8 months for general IT roles, pushing wage inflation to 18% annually. The scarcity is most acute in 5G cloud-native environments, where engineers must combine radio expertise with container security. MSPs are responding with global training hubs and graduate academies, but onboarding cycles lengthen project timelines and limit the speed at which providers can scale service portfolios.

Vendor Lock-in Concerns Slow Cloud Migration

High-profile dependence on hyperscale clouds such as Dish Network’s AWS-centric 5G rollout has raised alarms with regulators seeking to preserve competitive neutrality. The European Commission now requires operators to document multicloud strategies for critical functions. Operators are therefore negotiating exit clauses and federation architectures before signing managed service contracts, extending procurement cycles and tempering migration momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Build Adoption Momentum

Large enterprises accounted for 55.72% revenue in 2025, underpinning the telecom managed services market with global rollouts that span transport, IT and security domains. Their budgets support tailored solutions encompassing network slicing, private 5G and unified observability dashboards. In contrast, SMEs expand at an 11.15% CAGR to 2031, unlocking fresh volume for service providers. The telecom managed services market size for SMEs is projected to climb steadily as standardized, pay-as-you-grow bundles remove hefty capital barriers. Healthcare clinics, mid-tier manufacturers and regional retailers collectively drive this surge by outsourcing compliance-heavy communication stacks to offset limited in-house expertise.

SMEs gravitate toward cloud-first networking, managed SD-WAN and turnkey security gateways that meet sector regulations without deep technical staffing. Meanwhile, multinationals leverage AI-assisted automation to rationalize sprawling multi-vendor estates, freeing up internal teams for innovation initiatives. The convergence of price-competitive packages for SMEs and highly customized enterprise frameworks ensures that providers must maintain dual go-to-market plays.

By Service Type: Security Services Overtake Network Management

Managed network services retained 32.08% revenue share in 2025, underscoring their status as the core layer of the telecom managed services market. Yet managed security is the fastest riser at a 11.78% CAGR as operators confront nation-state threats and stringent data-residency rules. The telecom managed services market size for managed security is expected to swell notably, propelled by zero-trust rollouts and 5G core protection. Data center, communication and mobility services grow at steady mid-single-digit rates, while analytics-as-a-service emerges as an adjacent revenue stream.

Security demand spans threat hunting, SOC-as-a-service and compliance reporting across on-prem and multicloud estates. Providers differentiate via AI-powered anomaly detection and automated policy enforcement at network edges. Network management, though mature, is undergoing reinvention through intent-based networking and closed-loop assurance, keeping the segment relevant but less dynamic than security.

By Deployment Model: Cloud Dominance Deepens

Cloud-hosted deployments captured 62.15% share in 2025 and continue to expand at 12.74% CAGR, reflecting broad confidence in hyperscale reliability and elasticity. Operators value the ability to spin up network functions on-demand and pay only for utilized capacity, translating into leaner balance sheets. The telecom managed services market share of cloud models is forecast to widen as advanced security certifications and availability zones allay sovereignty fears. On-prem implementations persist for ultra-reliable low-latency communications and sensitive public-sector networks but their relative weight falls over time.

SoftBank’s large-scale core validation in public clouds validates performance parity with proprietary data centers. Hybrid blueprints that anchor user-plane functions at the edge while orchestrating control planes in cloud data centers are proliferating, affording MSPs an avenue to bundle consulting, migration and lifecycle operations.

By Telecom Operator Type: ISPs Challenge Mobile Incumbents

Mobile network operators (MNOs) retained 50.86% market share in 2025 thanks to spectrum ownership and established enterprise relationships. However, internet service providers (ISPs) grow at 12.02% CAGR to 2031 as fiber roll-outs create sizable footprints ripe for managed value-adds. The telecom managed services market size attributed to ISPs is expanding faster than that of MNOs, especially among regional carriers that tailor offerings to local businesses.

ISPs leverage unified fiber backbones to upsell SD-WAN, security and edge compute services, often partnering with MSPs for turnkey delivery. Mobile virtual network operators depend heavily on external expertise to match incumbent service breadth, presenting niche opportunities for white-label managed platforms. Competitive dynamics hinge on cross-selling prowess and the integration depth of cybersecurity, analytics and multicloud connectivity.

By End-User Vertical: Enterprises Accelerate Outsourcing

Consumers held 46.21% share in 2025, anchored by residential broadband and mobile bundles that incorporate basic device management and parental-control features. The enterprise segment, however, advances at 11.91% CAGR as digital-first strategies demand integrated connectivity, security and analytics. Financial institutions outsource network monitoring to assure algorithmic trading latency, while manufacturers deploy private 5G with managed edge compute for robotics.

Government and public-safety agencies adopt carrier-grade push-to-talk and mission-critical video services underpinned by stringent SLAs, supporting steady but smaller absolute growth. Enterprise uptake reinforces the telecom managed services market because cloud-native transformations, compliance mandates and IoT adoption exceed the operational capacity of internal IT staff.

Geography Analysis

North America led with 30.88% revenue in 2025 owing to early 5G deployment, high enterprise cloud adoption and supportive regulatory frameworks that encourage private-network experimentation. Verizon surpassed 4.2 million fixed-wireless access subscribers ahead of schedule, attesting to strong demand for managed broadband alternatives. AT&T posted 17 consecutive quarters of fiber subscriber gains, underscoring the robust appetite for carrier-operated managed connectivity. Mature competition pushes operators to outsource advanced automation, analytics and security tasks to sharpen differentiation.

Asia Pacific is the fastest-growing region at an 11.53% CAGR through 2031, buoyed by large-scale 5G infrastructure builds and government-backed Industry 4.0 programs. China deployed 3.4 million 5G base stations by 2024, fuelling unprecedented network-management requirements. Japan emphasized private 5G for smart factories, while India’s Reliance Jio established a business unit to commercialize private networks and managed services for midsize manufacturers. South Korea’s first private 5G licence issued to NAVER Cloud shows how hyperscalers are entering enterprise connectivity.

Europe registers steady mid-single-digit growth amid mature penetration levels, yet regulatory frameworks such as the Cyber Resilience Act press operators to outsource compliance-driven security and reporting. Middle East and Africa and South America exhibit rising interest in outsourcing to streamline OpEx and extend coverage into underserved areas. Regional players adopt managed satellite backhaul and energy-efficient RAN services to cope with challenging terrains and energy costs.

Competitive Landscape

Competition is moderate, with top vendors combining software, hardware and professional services to win multi-year contracts. Cisco integrates closed-loop automation into its Crosswork portfolio, giving operators real-time optimisation levers. Ericsson expands beyond RAN into managed cloud operations, bolstered by AI-enabled assurance platforms. IBM pivots Watsonx AI assets toward predictive maintenance, targeting network fault avoidance and SLA adherence.

M&A accelerates scale and capability expansion: Nokia’s Infinera deal deepens optical-packet integration, while ATSG and Evolve IP merged to form XTIUM, forecasting USD 230 million revenue from converged managed IT and telecom services. Amdocs launched Amdocs Studios to embed generative AI into digital-transformation programs. Niche entrants focus on AI-driven network analytics or zero-trust orchestration, carving high-margin sub-segments. Providers differentiate on outcome-based SLAs, multicloud neutrality and domain-specific expertise such as private-5G for manufacturing. The combined share of the top five players sits near 45%, supporting active but not hyper-concentrated rivalry.

Telecom Managed Services Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

International Business Machines Corporation

Telefonaktiebolaget LM Ericsson

Verizon Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NWN Corporation acquired InterVision Systems to broaden AI-powered cloud and security offerings for public-sector and mid-market clients.

- May 2025: YFM Equity Partners backed The Networking People (TNP) in a management buyout to scale critical ICT network services for UK health and emergency sectors.

- April 2025: Comcast Business completed its purchase of Nitel, adding managed SD-WAN and cybersecurity capabilities spanning 6,600 enterprise clients.

- May 2025: ServiceNow agreed to acquire Moveworks for USD 2.85 billion to embed conversational AI in service workflows for telecom operators.

Global Telecom Managed Services Market Report Scope

Managed services refer to a concept where a third-party service provider manages an organization's in-house, day-to-day management functions. Telecom-managed services allow organizations to minimize their costs in business operations, focusing more on fundamental techniques and essential business exercises, cutting down dangers primarily related to business operations, and upgrading operational precision and effectiveness.

The Telecom Managed Services Market is Segmented by Organization Size (Large Enterprises, Small and Medium Enterprises), Service Type (Managed Data Center Services, Managed Security Services, Managed Network Services, Managed Data and Information Services), and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Large Enterprises |

| Small Enterprises |

| Managed Data Center Services |

| Managed Security Services |

| Managed Network Services |

| Managed Data and Information Services |

| Managed Communication Services |

| Managed Mobility Services |

| On-Premises |

| Cloud / Hosted |

| Mobile Network Operator (MNO) |

| Mobile Virtual Network Operator (MVNO) |

| Internet Service Provider (ISP) |

| Consumer Segment |

| Enterprise Segment |

| Government and Public Safety |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Organization Size | Large Enterprises | ||

| Small Enterprises | |||

| By Service Type | Managed Data Center Services | ||

| Managed Security Services | |||

| Managed Network Services | |||

| Managed Data and Information Services | |||

| Managed Communication Services | |||

| Managed Mobility Services | |||

| By Deployment Model | On-Premises | ||

| Cloud / Hosted | |||

| By Telecom Operator Type | Mobile Network Operator (MNO) | ||

| Mobile Virtual Network Operator (MVNO) | |||

| Internet Service Provider (ISP) | |||

| By End-user Vertical | Consumer Segment | ||

| Enterprise Segment | |||

| Government and Public Safety | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the telecom managed services market expected to grow?

The market is forecast to advance at an 11.02% CAGR, reaching USD 53.83 billion by 2031.

Which deployment model is expanding the fastest?

Cloud-hosted services lead with a 12.74% CAGR and captured 62.15% market share in 2025.

Why are managed security services growing rapidly?

Zero-trust mandates and 5G core virtualization create complex threat vectors, driving managed security at a 11.78% CAGR.

Which region will experience the highest growth rate?

Asia Pacific leads with an 11.53% CAGR through 2031, propelled by extensive 5G infrastructure investment and Industry 4.0 uptake.

Page last updated on: