Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Infrastructure Solution Integration Service Market is Segmented by Component (Solutions, Services), Deployment Model (On-Premises, Public Cloud, Private Cloud, Hybrid/Multi-Cloud), End-User Industry (BFSI, IT and Telecommunications, and More), Organization Size (Large Enterprises, Smes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

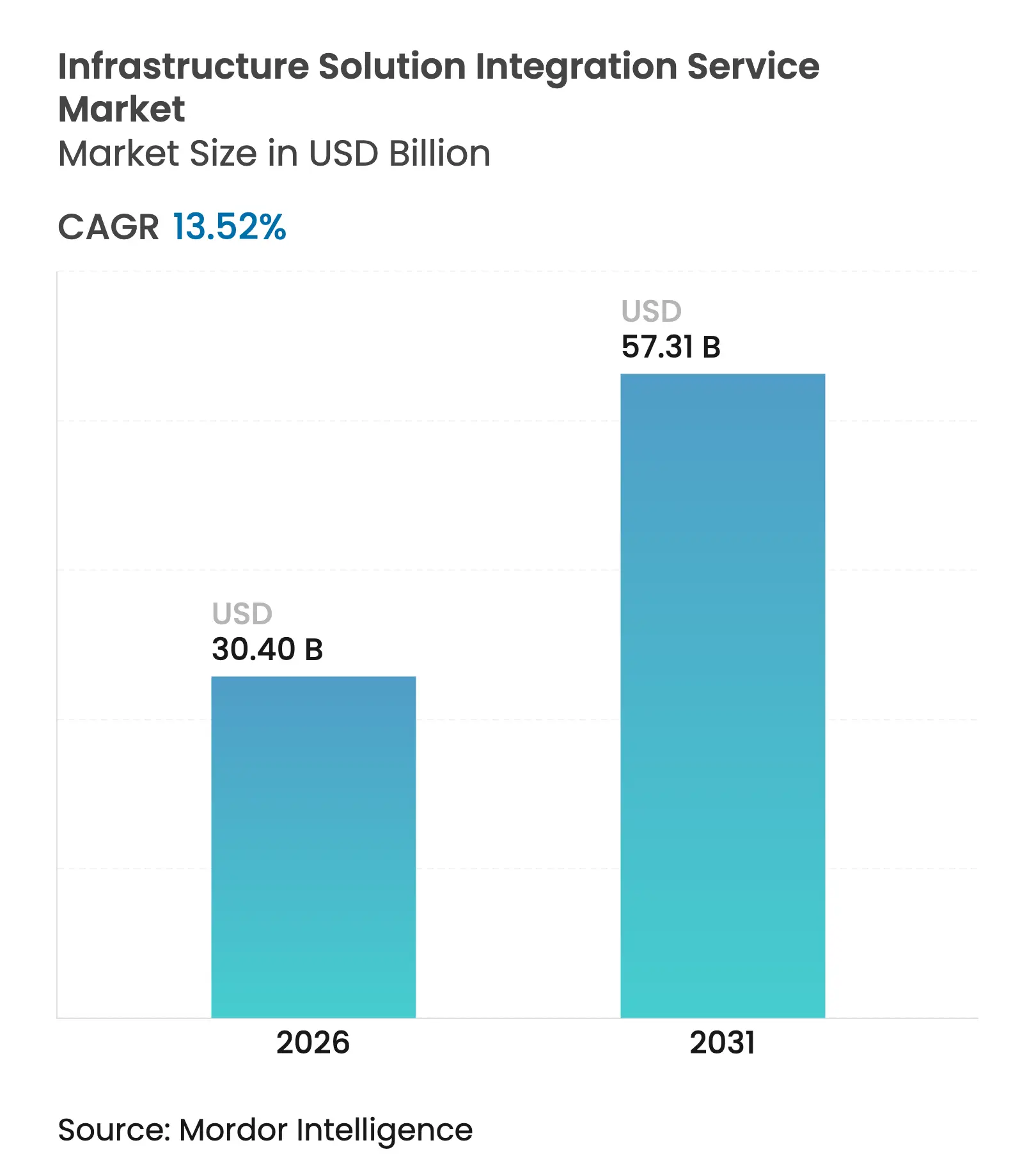

| Market Size (2026) | USD 30.4 Billion |

| Market Size (2031) | USD 57.31 Billion |

| Growth Rate (2026 - 2031) | 13.52 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The infrastructure solution integration service market size is expected to grow from USD 26.78 billion in 2025 to USD 30.4 billion in 2026 and is forecast to reach USD 57.31 billion by 2031 at 13.52% CAGR over 2026-2031. Cloud-first road-maps, zero-trust mandates and AI-enabled platforms are the primary forces behind this acceleration. Enterprises are re-architecting legacy estates to support hybrid, multi-cloud operations, fuelling demand for expert integration of applications, data and security controls. Public cloud remains the preferred launch pad, yet hybrid designs are scaling fastest as organisations balance sovereignty, latency and cost considerations. In parallel, AI-driven iPaaS tools are reshaping integration economics, while 5G-edge roll-outs open fresh “last-mile” opportunities for managed integration services. Heightened regulatory scrutiny, especially in North America and Europe, further elevates the need for zero-trust and data-sovereignty alignment, strengthening the value proposition of specialised service partners across the infrastructure solution integration service market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Cloud-first enterprise-wide transformation

Cloud-first enterprise-wide transformation

| +3.2% | Global | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+3.2%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Hyper-converged and composable infrastructure

Hyper-converged and composable infrastructure

| +2.8% | North America and EU | Short term (≤ 2 years) | |||

Zero-trust and data-sovereignty mandates

Zero-trust and data-sovereignty mandates

| +2.1% | Global, early gains in US and EU | Medium term (2-4 years) | |||

AI-enabled iPaaS expansion

AI-enabled iPaaS expansion

| +2.4% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) | |||

5G/Edge roll-outs

5G/Edge roll-outs

| +1.9% | Asia-Pacific, North America | Long term (≥ 4 years) | |||

Sustainability-linked IT stack rationalisation

Sustainability-linked IT stack rationalisation

| +1.3% | EU, North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Cloud-First Enterprise Transformation Accelerates Infrastructure Integration Demand

Enterprises continue to replace point-to-point connections with API-led integration fabrics that operate consistently across public, private, and edge environments. Microsoft and Oracle have expanded their multicloud alliance to 24 new regions, signalling hyperscalers’ response to growing cross-platform requirements.[1]CIO Dive, “Microsoft, Oracle to add 24 regions to multicloud alliance,” ciodive.com This pivot is expanding the addressable edge-integration opportunity, valued at USD 26 billion by 2032. Hybrid adoption intensifies complexity Gartner estimates 90% of organisations will rely on hybrid cloud by 2027, forcing a demand spike for integration expertise that unifies governance, observability, and policy enforcement. Accenture’s technology-managed services grew 11% YoY in Q1 FY25, reflecting corporate appetite for end-to-end integration outsourcing.

Hyper-Converged Infrastructure Drives Composable Architecture Adoption

Composable infrastructure lets operations teams allocate compute, storage and networking on demand, easing AI and analytics workload placement. Dell’s XC Plus with Nutanix Cloud Platform embodies this trend, offering software-defined flexibility for hybrid multicloud estates. AI workloads magnify the need for dynamic resource pooling; HPE invested USD 26.3 billion in 2024 to future-proof capacity. [2]Canonical, “Networked edge computing will present a USD 26 billion opportunity by 2032,” canonical.com Collectively, these forces increase demand for service partners who can align composable, AI-ready infrastructure with robust governance frameworks.

Zero-Trust Mandates Reshape Security Integration Requirements

Executive Order 14028 obliges US federal agencies to achieve zero-trust postures, and similar rules emerge globally, turning security architecture into a mandatory integration pillar. NIST’s 19 reference designs illustrate the breadth of capabilities—from identity to micro-segmentation—that must co-exist seamlessly.[3] NIST, “Guidance on Implementing a ZTA,” nist.gov Integration providers now orchestrate multi-vendor identity, network and data-protection solutions, ensuring policy consistency across cloud and edge footprints. Microsoft and SAP’s plan to migrate SAP Identity Management users to Microsoft Entra ID by 2027 highlights vendor collaboration to simplify security integration. These developments embed security integration budgets within almost every infrastructure modernisation initiative, sustaining the infrastructure solution integration service market.

AI-Enabled iPaaS Platforms Transform Integration Paradigms

AI is shifting integration from rule-based mapping to predictive automation. Financial institutions are early adopters—74% of banks have generative-AI pilots, while 42% earmark dedicated budgets, amplifying demand for AI-ready data pipelines.Tray.ai predicts most enterprises will retrofit stacks for AI within two years. Integration specialists, therefore, move beyond connectivity into intelligent orchestration, embedding machine learning to harmonise structured and unstructured data. This evolution underpins premium project values across the infrastructure solution integration service market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Persistent multi-cloud lock-in risk

Persistent multi-cloud lock-in risk

| -2.1% | Global | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-2.1%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Scarcity of integration talent

Scarcity of integration talent

| -1.8% | North America, EU | Short term (≤ 2 years) | |||

Technical debt in brown-field datacentres

Technical debt in brown-field datacentres

| -1.4% | North America, EU | Long term (≥ 4 years) | |||

Escalating cyber-insurance prerequisites

Escalating cyber-insurance prerequisites

| -0.9% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Multi-Cloud Lock-In Concerns Constrain Integration Investments

While 76% of enterprises now operate multi-cloud, many underestimate the effort required to maintain workload portability, triggering caution around large-scale integration projects. VMware’s Cloud Foundation and Broadcom’s OEM alliances with Dell, HPE , and Lenovo promise “any-cloud” mobility yet still depend on disciplined configuration management. Migrating data among providers raises egress costs and governance overheads, diluting ROI projections. Decision cycles, therefore, elongate, temporarily moderating capital flows into the infrastructure solution integration service market.

Integration Talent Shortage Drives Service Premium Pricing

Global construction and manufacturing are short 465,000 skilled professionals, a symptom mirrored in IT, where 75% of firms struggle to secure integration architects. High day rates inflate project budgets, especially for AI and security experts whose profiles command premium remuneration. TCS added 5,090 employees in Q1 FY26 and trained 114,000 staff in AI, but supply still trails demand. As a result, some enterprises phase implementations, delaying revenue recognition for vendors in the infrastructure solution integration service market.

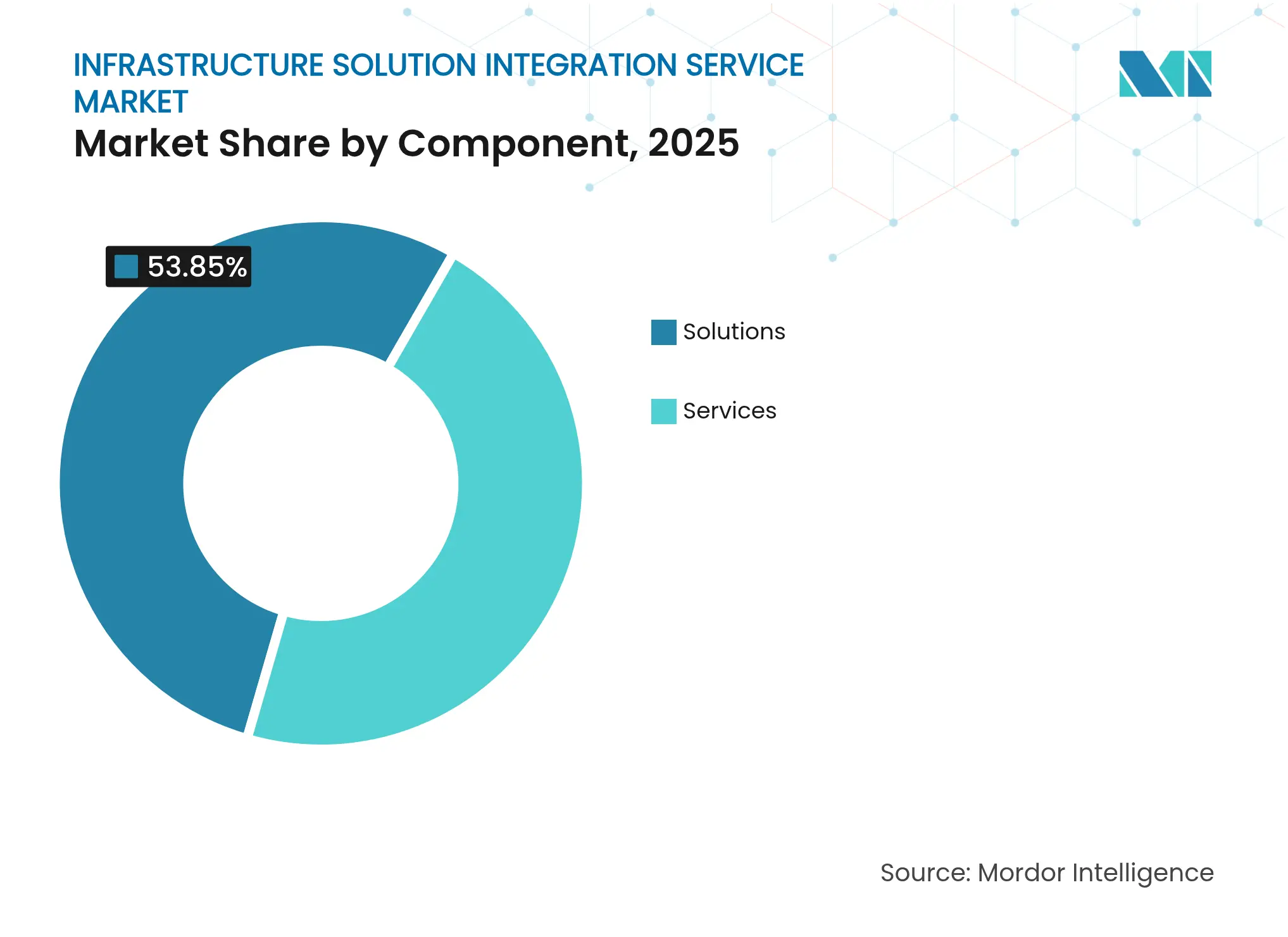

By Component: Services Acceleration Outpaces Solution Maturity

Solutions captured 53.85% share in 2025, reflecting ongoing investment in management, security and observability software foundations. However, services are expanding at a 13.74% CAGR, outstripping product revenue growth across the infrastructure solution integration service market. Consulting demand climbs as firms design cloud migration blueprints aligned with zero-trust imperatives. Design and build engagements follow, epitomised by Accenture’s double-digit managed-service growth, driven by full-stack infrastructure projects.

Managed and support services now wrap AI-enabled monitoring and compliance automation around deployed platforms. This evolution pushes recurring revenue higher and deepens client reliance on strategic partners. Consequently, the services segment is set to narrow the infrastructure solution integration service market share gap with software before 2030, signalling a structural tilt toward human expertise.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Model: Hybrid Cloud Emergence Challenges Public Cloud Dominance

Public cloud retained 52.62% revenue in 2025, yet hybrid designs clock the fastest 15.68% CAGR, propelled by latency-sensitive applications and sovereignty rules. Enterprises blend on-premises assets with cloud services to optimise cost and performance, spurring demand for integration fabrics that synchronise policies across domains. The infrastructure solution integration service market size for hybrid deployments is forecast to accelerate steadily as Microsoft-Oracle dual-deploy models proliferate.

Private cloud remains relevant, especially for industries with deterministic workloads or strict data classifications. Meanwhile, on-premises installations decline gradually but persist where edge-computing or OT-IT convergence mandates site-local processing. Service providers target this heterogeneous reality with platform-agnostic integration blueprints that ensure consistent operations regardless of host location.

By End-User Industry: Healthcare Digitisation Accelerates Beyond BFSI Leadership

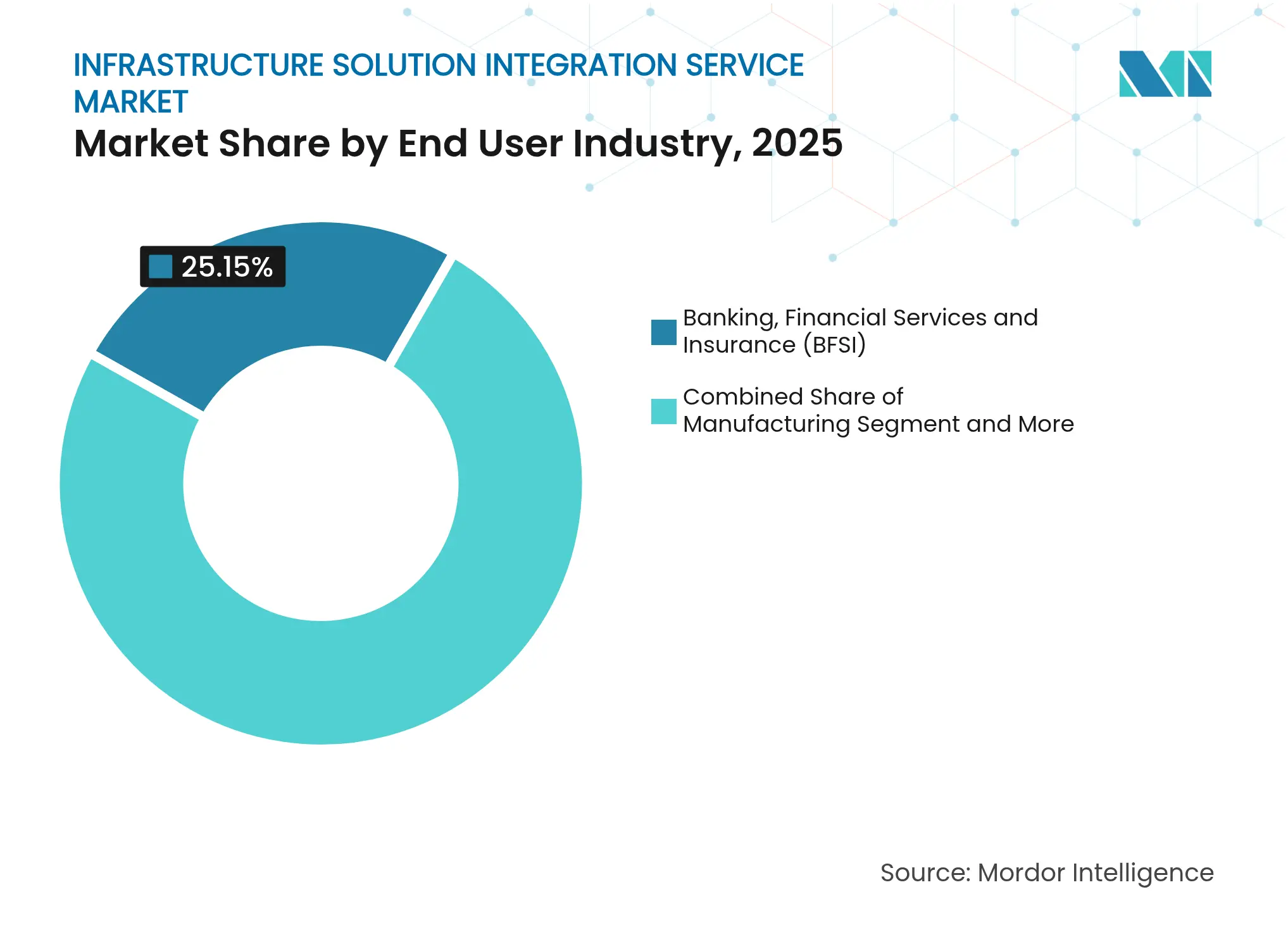

BFSI stood atop revenue tables with 25.15% share in 2025, underpinned by real-time risk analytics and regulatory reporting needs. Yet healthcare edges ahead on growth, set for a 14.02% CAGR as telehealth, electronic medical records and AI diagnostics demand secure, interoperable data flows. The infrastructure solution integration service market size for healthcare is projected to double before 2030, encouraged by privacy mandates and outcome-based reimbursement models.

Manufacturing invests steadily in IoT and predictive maintenance projects, integrating sensor data with cloud analytics to improve uptime. Retail and e-commerce prioritise omnichannel supply chain synchronisation, while government adoption rises sharply owing to zero-trust deadlines. Each vertical therefore contributes unique requirements that reinforce the necessity of specialised integration services.

Note: Segment shares of all individual segments available upon report purchase

By Organization Size: SME Adoption Accelerates Through Cloud Accessibility

Large enterprises remained dominant at 66.40% of 2025 spend, reflecting complex estates that span multiple geographies and regulatory regimes. They engage tier-one integrators for multi-year transformation deals. Conversely, SMEs exhibit the briskest 14.12% CAGR, benefiting from low-code iPaaS and marketplace ecosystems worth USD 5.3 billion in 2024, projected to double by 2028. These platforms lower entry barriers, allowing modestly resourced firms to implement robust data pipelines and security integrations without in-house architects, thereby broadening the addressable infrastructure solution integration service market.

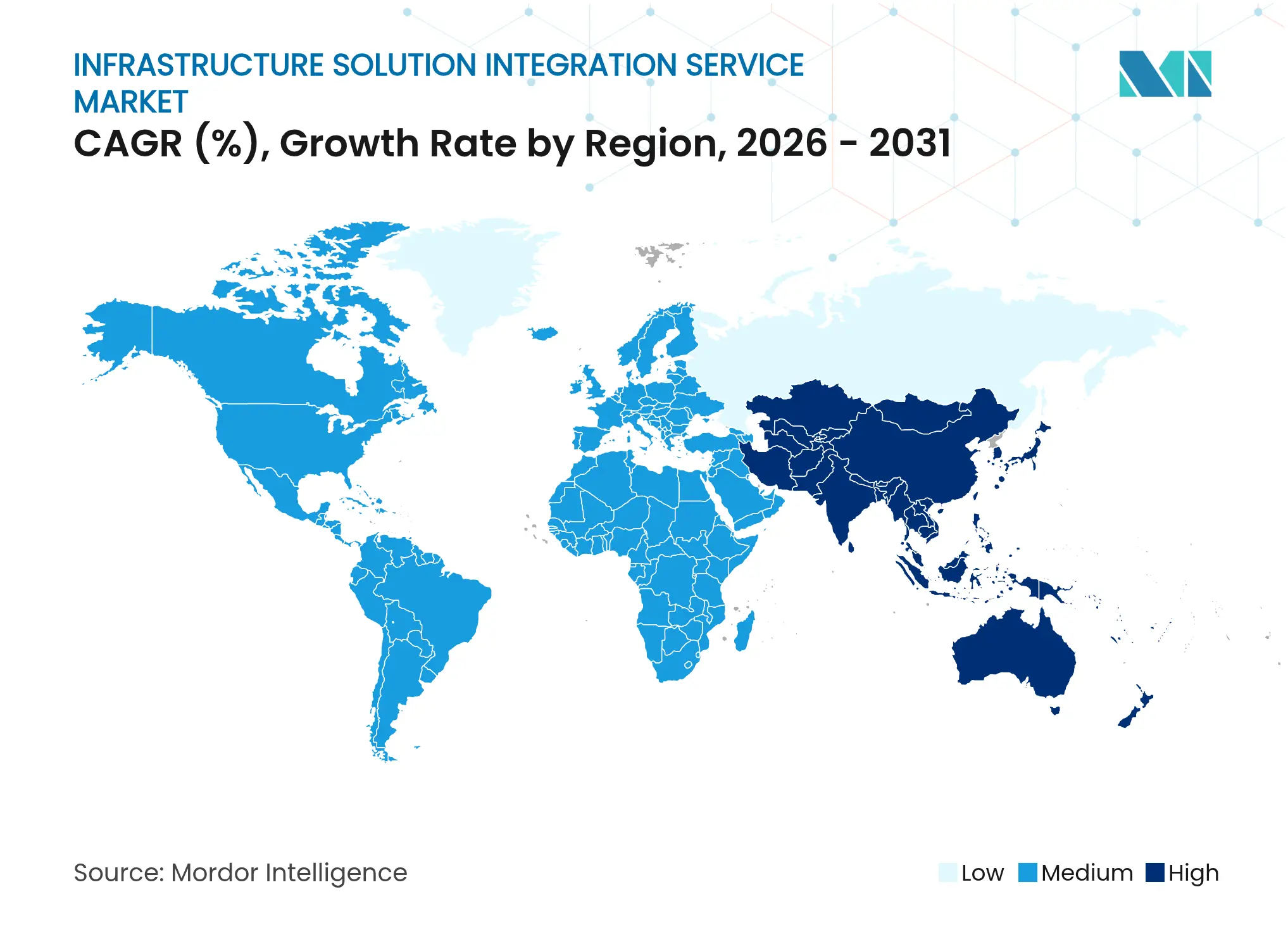

North America retained leadership with 32.35% revenue in 2025, fuelled by the USD 1.2 trillion Bipartisan Infrastructure Law, which has already allocated USD 695 billion to more than 74,000 projects. Mandatory zero-trust frameworks and sizeable private investments such as Microsoft-BlackRock’s USD 30 billion data-centre initiative bolster regional demand. The presence of global integrators and hyperscalers fosters a mature competitive ecosystem that continuously refreshes service offerings.

Asia-Pacific leads growth with a 15.28% CAGR, driven by an major infrastructure investment requirement through 2035. Data-centre capacity is expected to rise nearly 20% annually until 2028. Governments promote digital transformation, and local giants such as TCS and Infosys scale regional service delivery, strengthening indigenous capability. As a result, the infrastructure solution integration service market is expanding rapidly across APAC’s emerging economies.

Market Concentration

The infrastructure solution integration service market exhibits moderate concentration; the top five providers hold roughly 40% revenue. Accenture’s Q1 FY25 revenue of USD 17.7 billion, boosted by 11% growth in technology-managed services, epitomises scale leverage .IBM’s USD 6.4 billion acquisition of HashiCorp fortifies its hybrid cloud toolset, signalling a trend toward platform consolidation. TCS surpassed USD 30 billion in FY25 revenue, anchored by expanding AI-led infrastructure engagements.

Strategic alliances are vital competitive levers. Dell pairs with Nutanix for composable hybrid offerings, while Microsoft and Oracle expand multicloud reach. HPE’s Juniper Networks acquisition doubles its networking portfolio and accelerates AI-centric integration plays. Specialized cybersecurity and AI integrators are gaining traction, applying best-of-breed proficiency to niche workloads and nudging incumbents toward faster innovation.

Price competition remains disciplined due to scarce integration talent and high switching costs. Vendors differentiate through outcome-based SLAs, vertical accelerators and sovereign-cloud variants that align with local regulations. These dynamics sustain healthy margins even as the infrastructure solution integration service market matures.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Infrastructure solution and integration services are essential for any business organization to run its business operations efficiently and cost-effectively. With the overview of the numerous kinds of software and solutions, businesses use infrastructure solutions and integration services to run their procedures smoothly.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.