Secrets Management Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

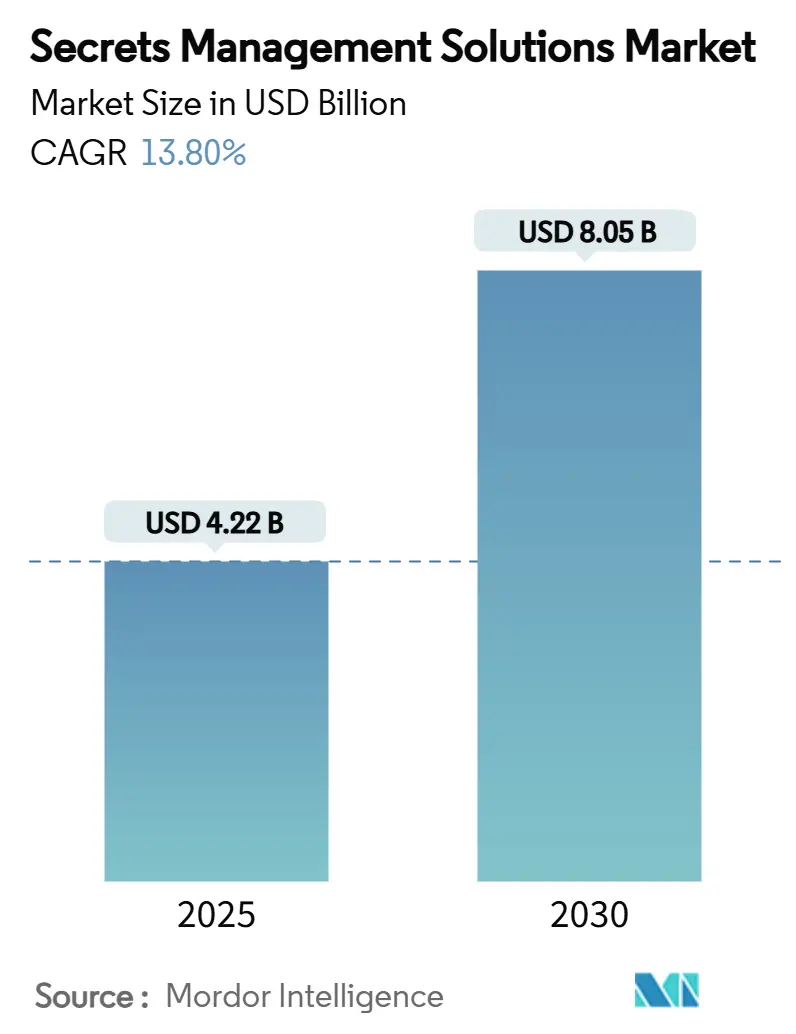

| Market Size (2025) | USD 4.22 Billion |

| Market Size (2030) | USD 8.05 Billion |

| Growth Rate (2025 - 2030) | 13.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secrets Management Solutions Market Analysis by Mordor Intelligence

The secrets management solutions market size stood at USD 4.22 billion in 2025 and is forecast to reach USD 8.05 billion by 2030, advancing at a 13.8% CAGR over the period. Ongoing migration toward DevSecOps, rapid growth in machine identities, and expanding multi-cloud footprints continue to shift spending from reactive credential vaults to proactive secrets governance. Enterprises now handle machine-to-human identity ratios of 45:1, forcing investment in automated discovery, rotation, and audit capabilities. [1]CyberArk, “How to Secure Secrets in Multi-cloud Environments,” cyberark.com Vendors are consolidating certificate lifecycle management, privileged access, and vault functions into unified platforms, while regulatory mandates such as GDPR, PCI-DSS, and NIS 2 elevate secrets management from an optional safeguard to a board-level compliance line item. Hybrid deployment demand is accelerating as organizations seek the operational elasticity of cloud alongside the data-sovereignty assurances of on-premises infrastructure, and this architectural flexibility is opening fresh opportunities for SaaS-first challengers that bundle AI-driven anomaly detection into subscription offerings.

Key Report Takeaways

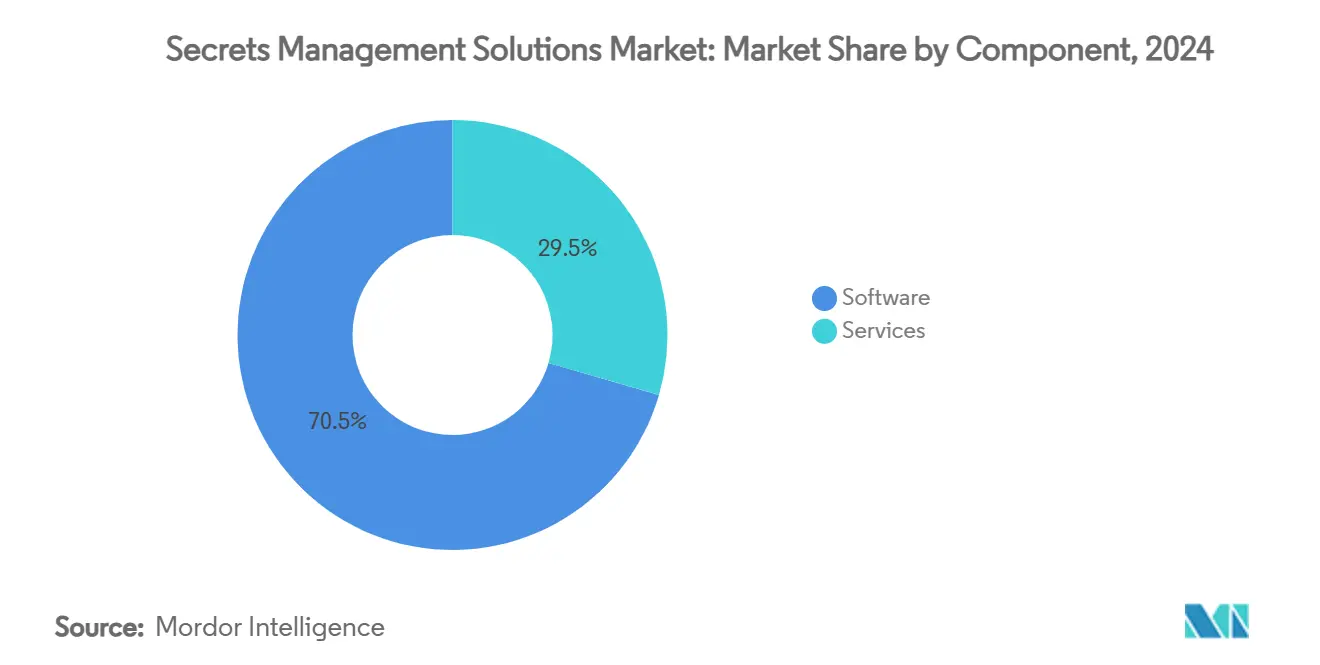

- By component, software led with 70.5% revenue share of the secrets management solutions market in 2024; services are projected to rise at a 15.4% CAGR to 2030.

- By deployment model, cloud-based solutions captured 56.7% of the secrets management solutions market share in 2024, while hybrid deployments are set to expand at a 15.2% CAGR through 2030.

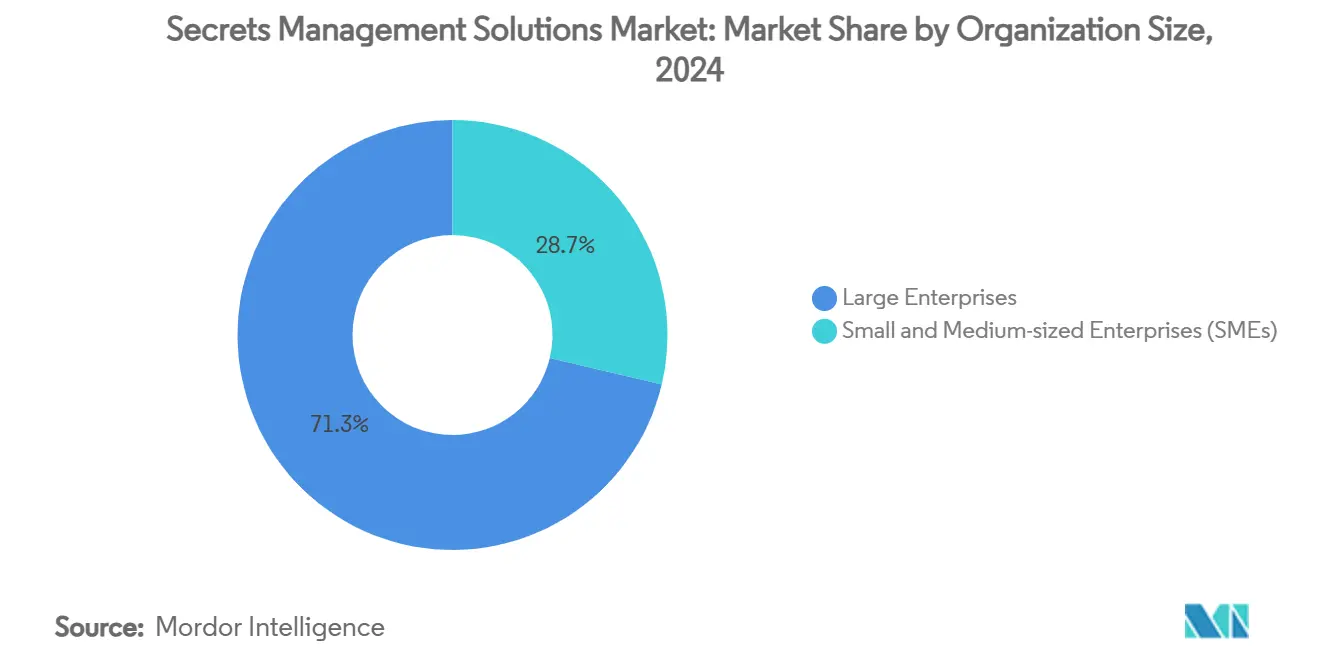

- By organization size, large enterprises held 71.3% share of the secrets management solutions market size in 2024, yet SMEs are anticipated to register the fastest 15.5% CAGR over the outlook period.

- By end-use industry, BFSI commanded 28.3% share of the secrets management solutions market in 2024; government and public sector workloads are forecast to grow at a 14.9% CAGR by 2030.

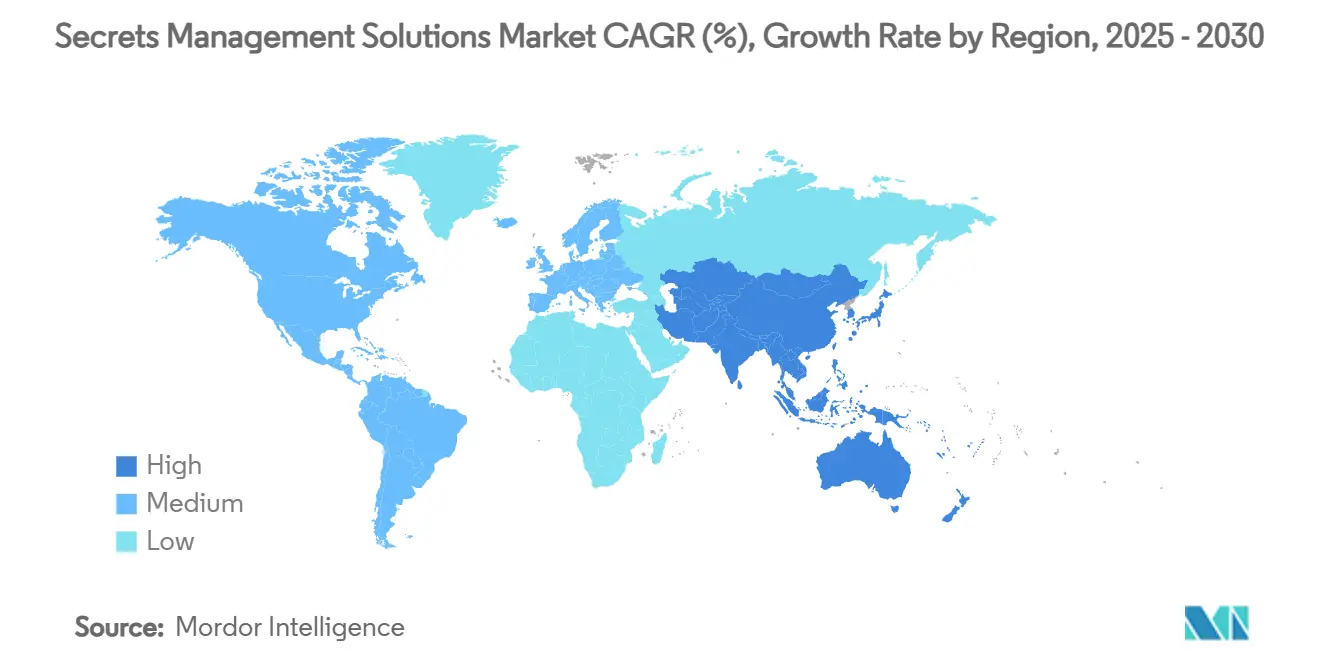

- By geography, North America accounted for 38.4% revenue share of the secrets management solutions market in 2024, whereas Asia-Pacific is poised for the highest 15.0% CAGR to 2030.

Global Secrets Management Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of DevOps and CI/CD pipelines | +2.8% | North America, Europe | Medium term (2-4 years) |

| Multi-cloud adoption and need for centralized vaults | +2.5% | North America, APAC | Long term (≥ 4 years) |

| Regulatory compliance (GDPR, PCI-DSS, etc.) | +2.2% | Europe, North America | Short term (≤ 2 years) |

| Explosion of machine identities and API workloads | +3.1% | Global | Long term (≥ 4 years) |

| Quantum-ready cryptography roadmaps | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Rise of secret-less architectures in Kubernetes | +1.4% | Container-intensive industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of DevOps and CI/CD Pipelines

Organizations integrating secrets orchestration directly into automated pipelines have witnessed daily secrets-request volumes surpass 300 million, as shown by athenahealth’s Vault deployment. [2]HashiCorp, “A New Prescription for Secrets Management,” hashicorp.com Automated retrieval and rotation now eliminate up to 80% of manual credential work, freeing engineers for product delivery. Infrastructure-as-Code and GitOps accelerate this shift, while secret-less designs based on OpenID Connect are emerging as the next step toward removing static keys altogether. Vendor platform roadmaps that embed workload identities natively into build systems are therefore gaining procurement priority across large development organizations.

Multi-cloud Adoption and Need for Centralized Vaults

Ninety-five percent of APAC enterprises already run workloads across multiple cloud providers, magnifying configuration drift and compliance risk if credentials remain siloed. Centralized, cloud-agnostic vaults mitigate an estimated 40–60% cost premium created by unmanaged vault sprawl and reduce exposure to credential-based attacks through unified rotation policies. Partnerships such as CyberArk-Wiz underscore the demand for shared policy engines that stretch across AWS, Azure, Google Cloud, and on-premises estates. For large cloud programs, these platforms are no longer a defensive add-on but a prerequisite for workload portability and audit readiness.

Regulatory Compliance (GDPR, PCI-DSS, etc.)

The NIS 2 Directive obliges 89% of European entities to enlarge cybersecurity teams with skills tied directly to secrets governance. PCI-DSS rule sets now require automated key rotation and immutable audit logs, achievable only with dedicated vaults. [3]Evervault, “Encryption Requirements for PCI Compliance 2025,” evervault.com Healthcare operators using centralized secrets vaults have trimmed compliance preparation time by as much as 70%, underscoring the operational value of automated evidence gathering. Impending quantum-safety clauses in financial services are also catalyzing upgrades to platforms that support hybrid and post-quantum algorithms.

Explosion of Machine Identities and API Workloads

Non-human identities already form 68% of access entities, and the growth of microservices, IoT, and AI workloads continues to accelerate the curve. Centralized credential stores cut advanced-threat risk by half, largely by removing hard-coded secrets and enforcing scheduled rotation. Standards such as SPIFFE introduce verifiable workload identities, nudging the market toward secret-less patterns where x.509 certificates replace passwords altogether. Secrets management technology, therefore, evolves from vaulting data to orchestrating cryptographic identity at machine speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy environments | −1.8% | Global | Short term (≤ 2 years) |

| High total cost of ownership of enterprise platforms | −2.1% | SMEs worldwide | Medium term (2-4 years) |

| Skills shortage in secrets governance | −1.5% | APAC, emerging markets | Long term (≥ 4 years) |

| Vendor lock-in risk from proprietary vault formats | −1.2% | Multi-cloud adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Environments

Retrofitting dynamic secret retrieval into decades-old applications consumes up to 70% of project budgets and can see services spend exceeding license fees by a factor of three. Regulated workloads often demand dual-stack credential stores during migration, prolonging parallel-run periods and widening attack surfaces. Organizations therefore stagger adoption, starting with low-risk workloads before touching mission-critical mainframes, slowing overall rollout momentum in the short term.

High Total Cost of Ownership of Enterprise Platforms

First-year deployment for 10,000 users can climb to USD 385,000 once licenses, infrastructure, and professional services are tallied. Required administrator training ranges from 40-80 hours, adding soft costs to already stretched cybersecurity budgets. Although SaaS-based offerings reduce infrastructure burden, many SMEs hesitate for fear of data-sovereignty constraints and future price escalations, constraining near-term uptake outside the top enterprise tier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Platform Consolidation

Software captured 70.5% of the secrets management solutions market size in 2024 as enterprises converged on unified vault, rotation, and policy engines that integrate seamlessly with DevOps pipelines. Growing preference for consolidated platforms over point tools reflects procurement pressures to control tool sprawl and streamline audit workflows. Professional services, while forming a smaller revenue base, are charting the quickest 15.4% CAGR because legacy modernization and multi-cloud integration often require specialized expertise unavailable in-house.

Managed service providers now bundle 24/7 monitoring, automated incident remediation, and compliance reporting, easing adoption for mid-market firms that lack dedicated security staff. Software roadmaps increasingly layer certificate lifecycle, privileged access controls, and encryption-as-a-service to widen wallet share. As a result, vendors that deliver deep API extensibility and out-of-the-box integrations with CI/CD toolchains reinforce their position at the center of enterprise security stacks in the secrets management solutions market.

By Deployment Model: Hybrid Architectures Reshape Cloud Strategy

Cloud-based offerings accounted for 56.7% of 2024 revenue, yet hybrid setups are forecast to post the fastest 15.2% CAGR as organizations balance latency, sovereign-data mandates, and disaster-recovery obligations across dispersed footprints. Hybrid vaults lower operational cost 30-40% relative to pure on-premises installations while retaining localized control over high-sensitivity keys.

Edge and IoT expansions amplify demand for distributed secret replication without compromising policy consistency. Vendors are therefore investing in lightweight agents and mesh gateways capable of synchronous rotation across on-prem, public cloud, and edge nodes. The resulting flexibility encourages late-mover industries, notably manufacturing and utilities, to engage the secrets management solutions market without overhauling existing datacenter investments.

By Organization Size: SME Adoption Accelerates Digital Transformation

Large enterprises dominated with a 71.3% share of the secrets management solutions market in 2024, thanks to larger budgets and stringent regulatory exposure. Even so, SMEs are projected to chart a 15.5% CAGR through 2030 as SaaS vaults democratize access to enterprise-grade credential hygiene. Consumption-based pricing and browser-based consoles remove capital barriers and cut setup times from months to days.

Smaller firms view secrets management as foundational insurance against costly breaches that could jeopardize brand viability. Ease-of-integration with public-cloud identity brokers also tilts the value proposition away from manual key handling. These dynamics ensure that SME spending will become a pivotal growth vector for the secrets management solutions market.

By End-Use Industry: Financial Services Lead Regulatory-Driven Adoption

The BFSI sector held 28.3% of revenue in 2024, illustrating the primacy of regulated data environments and high-value targets. Government and public entities, however, are forecast to record the highest 14.9% CAGR as national cybersecurity strategies embed secrets governance within digital services modernization.

Healthcare and life sciences accelerate adoption to satisfy HIPAA and patient privacy mandates, whereas industrial and manufacturing players face new credential challenges as OT and IT networks converge. Each vertical encounters unique compliance triggers, but all trend toward unified audit trails and crypto-agile key stores to future-proof against evolving standards, reinforcing broad-based momentum for the secrets management solutions market.

Geography Analysis

North America led with a 38.4% share in 2024, fueled by mature DevOps cultures and early cloud adoption. Regional enterprises such as Starbucks manage secrets for over 100,000 edge devices, underscoring operational scale. US regulators continue to tighten disclosure rules around cyber incidents, pushing firms toward automated vault logging and tamper-proof evidence capture. Canada and Mexico contribute incremental growth via cross-border data-residency requirements that favor centralized, policy-driven vaults.

Asia-Pacific is projected to notch a 15.0% CAGR to 2030, buoyed by cybersecurity budgets expected to hit USD 52 billion in 2027. Japan and Singapore showcase leading implementations across high-compliance finance sectors, while China and India supply volume through massive digitization initiatives. Heightened cyber-attack frequency—31% of global incidents—propels urgency for robust secrets governance. Government grants and skills-training incentives further lubricate adoption across mid-market cohorts.

Europe experiences steady uptake anchored in GDPR and NIS 2. Germany, France, and the UK prioritize hybrid deployment to reconcile strict privacy laws with cloud efficiencies. Only 4% of European firms currently budget for quantum-safe encryption, pointing to a sizeable runway for post-quantum-ready vault upgrades. Information-security spend now averages 9.0% of IT budgets, providing sustained tailwinds for the secrets management solutions market across the continent.

Competitive Landscape

The market remains moderately fragmented, yet consolidation is intensifying. CyberArk’s USD 1.54 billion purchase of Venafi in 2025 merged human and machine identity capabilities, expanding its addressable opportunity by USD 10 billion. HashiCorp leverages its Terraform and Consul ecosystems to foster stickiness among DevOps practitioners, while Akeyless pioneers a SaaS-first unified secrets and machine-identity platform supported by a Deutsche Bank investment. [4]Akeyless, “Introducing Unified Secrets Platform,” akeyless.io

Technological differentiation centers on AI-assisted anomaly detection, secret scanning, and workload identity issuance. HashiCorp’s HCP Vault Radar, now in limited release, automatically discovers hard-coded credentials across repositories, scoring early interest from heavily regulated DevOps teams. Venture funding momentum continues; Infisical captured USD 16 million to broaden its open-source stack for AI-era workloads.

White-space opportunities lie in OT-specific solutions where vault protocols must operate on deterministic industrial timelines. Vendors capable of bridging IT-OT credential needs without compromising latency stand to outflank incumbents as smart-factory rollouts gather pace. Overall, competition is shifting from vault capacity toward orchestration intelligence, favoring players that can collapse multiple secrets-adjacent functions into a single control plane across the secrets management solutions market.

Secrets Management Solutions Industry Leaders

HashiCorp, Inc.

CyberArk Software Ltd.

Delinea Inc.

Akeyless Security Ltd.

BeyondTrust Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Infisical raised USD 16 million Series A led by Elad Gil to enhance its open-source platform.

- May 2025: Thales named Overall Leader in KuppingerCole Leadership Compass for Enterprise Secrets Management.

- April 2025: CyberArk launched its machine-identity security solution covering all environments.

- March 2025: HashiCorp introduced HCP Vault Radar for unmanaged secret discovery.

- February 2025: CyberArk completed the USD 1.54 billion acquisition of Venafi.

- December 2024: Thales launched CipherTrust Enterprise Secrets Management powered by Akeyless.

Global Secrets Management Solutions Market Report Scope

| Software | Vault and Key-Management Software |

| Secret-Detection/Scanning Tools | |

| Services | Professional Services |

| Managed Services |

| On-Premises |

| Cloud-Based |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Retail and E-commerce |

| Manufacturing and Industrial |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | Vault and Key-Management Software | |

| Secret-Detection/Scanning Tools | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Model | On-Premises | ||

| Cloud-Based | |||

| Hybrid | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-Use Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Retail and E-commerce | |||

| Manufacturing and Industrial | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the secrets management solutions market in 2030?

The market is expected to reach USD 8.05 billion by 2030, growing at a 13.8% CAGR.

Which deployment model is growing fastest for secrets management?

Hybrid deployments are forecast to expand at 15.2% CAGR as firms balance cloud scalability with on-premises data-sovereignty needs.

Why are SMEs increasingly investing in secrets governance?

Cloud-native SaaS vaults with consumption pricing lower entry costs, allowing SMEs to meet compliance mandates and reduce breach risk without large capital spend.

Which region shows the highest growth potential?

Asia-Pacific is poised for the fastest 15.0% CAGR through 2030 due to rising cybersecurity budgets and government-backed digital transformation programs.

How are regulations influencing adoption?

Frameworks such as GDPR, PCI-DSS, and NIS 2 require automated key rotation and audit trails, making secrets management platforms essential for compliance.

What technological shift could disrupt traditional vaults?

Secret-less architectures that rely on workload identity frameworks are emerging, potentially reducing dependence on static credential storage.

Page last updated on: