Cyber Deception Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 4.12 Billion |

| Growth Rate (2026 - 2031) | 13.01% CAGR |

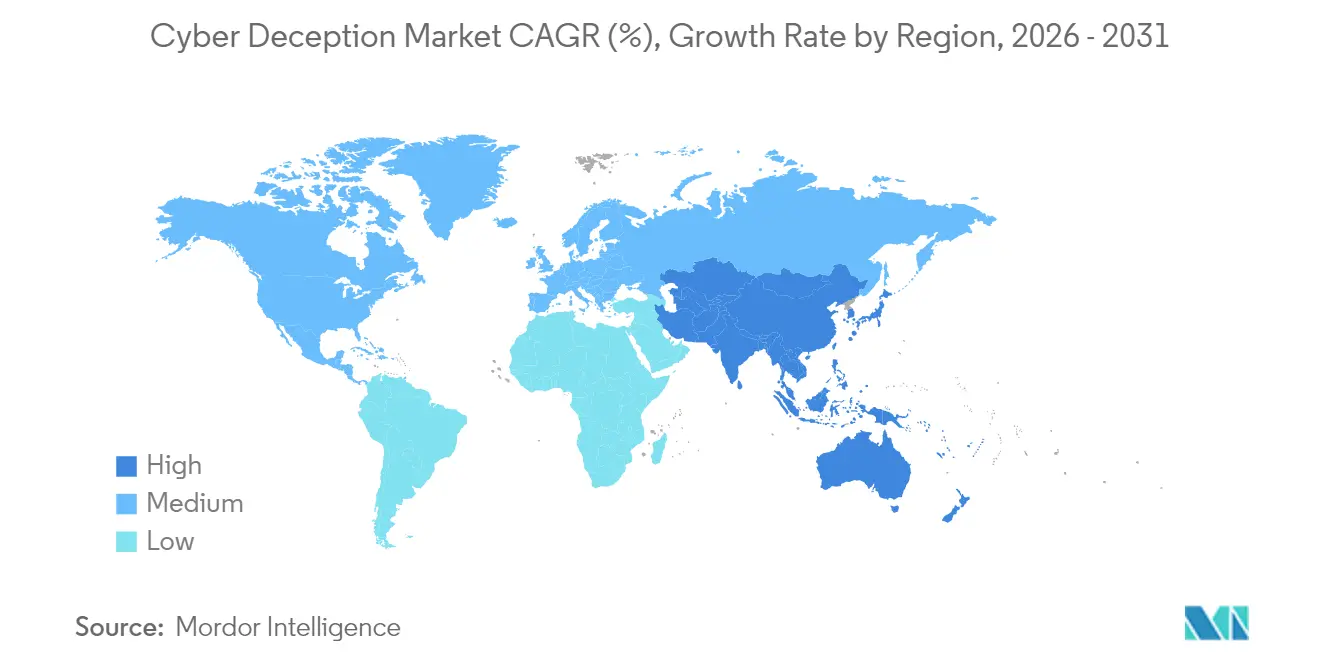

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cyber Deception Market Analysis by Mordor Intelligence

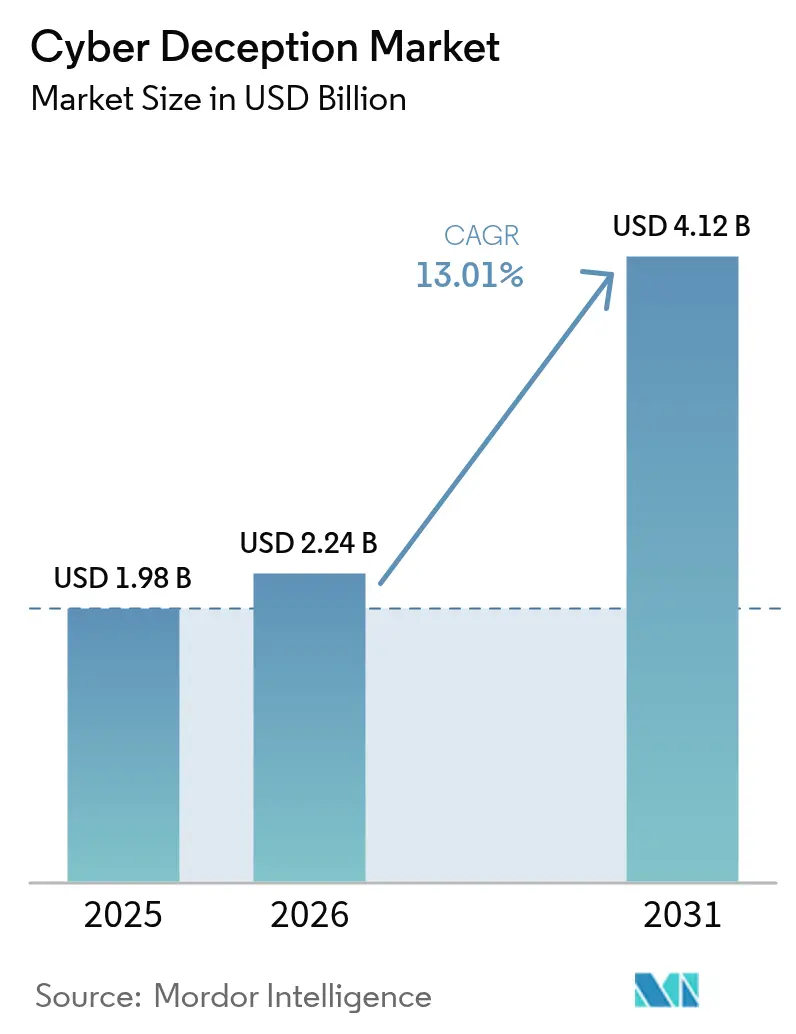

The cyber deception market size was valued at USD 1.98 billion in 2025 and estimated to grow from USD 2.24 billion in 2026 to reach USD 4.12 billion by 2031, at a CAGR of 13.01% during the forecast period (2026-2031).[1]Tomer Weingarten, “SentinelOne Completes Acquisition of Attivo Networks,” SentinelOne.com Citation Growing attacker sophistication, the pivot toward zero-trust architectures, and the embedding of honeypots inside extended detection and response (XDR) platforms drive that expansion.

Vendors are integrating identity-aware decoys, container-based traps, and fake data artifacts directly into cloud-native security stacks, turning deception into a mainstream control rather than a specialized add-on. For instance, large financial groups now pair deceptive credentials with transaction scoring engines so that anomalous payments trigger both account throttling and attacker telemetry capture. Parallel cost pressures continue to steer mid-sized enterprises toward managed deception services that wrap 24/7 monitoring, threat hunting, and tuning in a single subscription. As a result, competitive momentum favors providers that can demonstrate low-touch deployment, API-level orchestration, and measurable threat intelligence value per dollar invested.

Key Report Takeaways

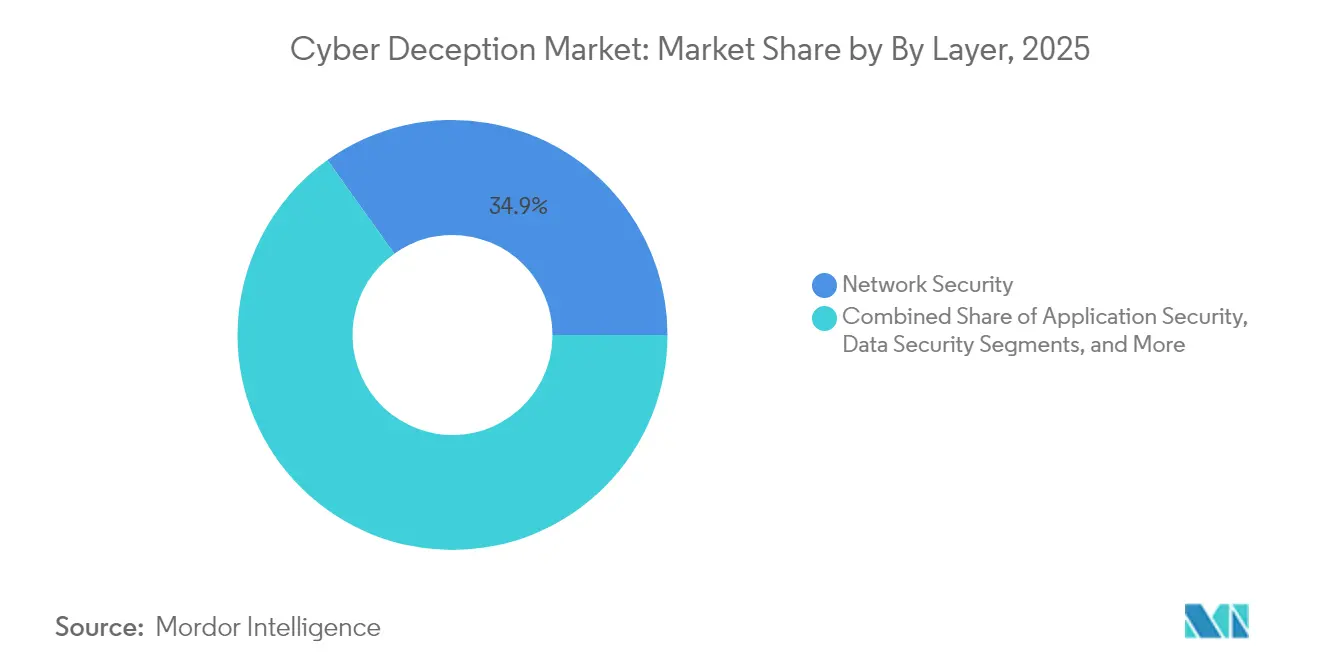

- By layer, network security led with a 34.88% revenue share in 2025, whereas endpoint security is advancing at a 17.63% CAGR through 2031.

- By service type, managed services captured 38.74% of the cyber deception market share in 2025, and the same segment posts the highest forecast growth at 17.72% through 2031.

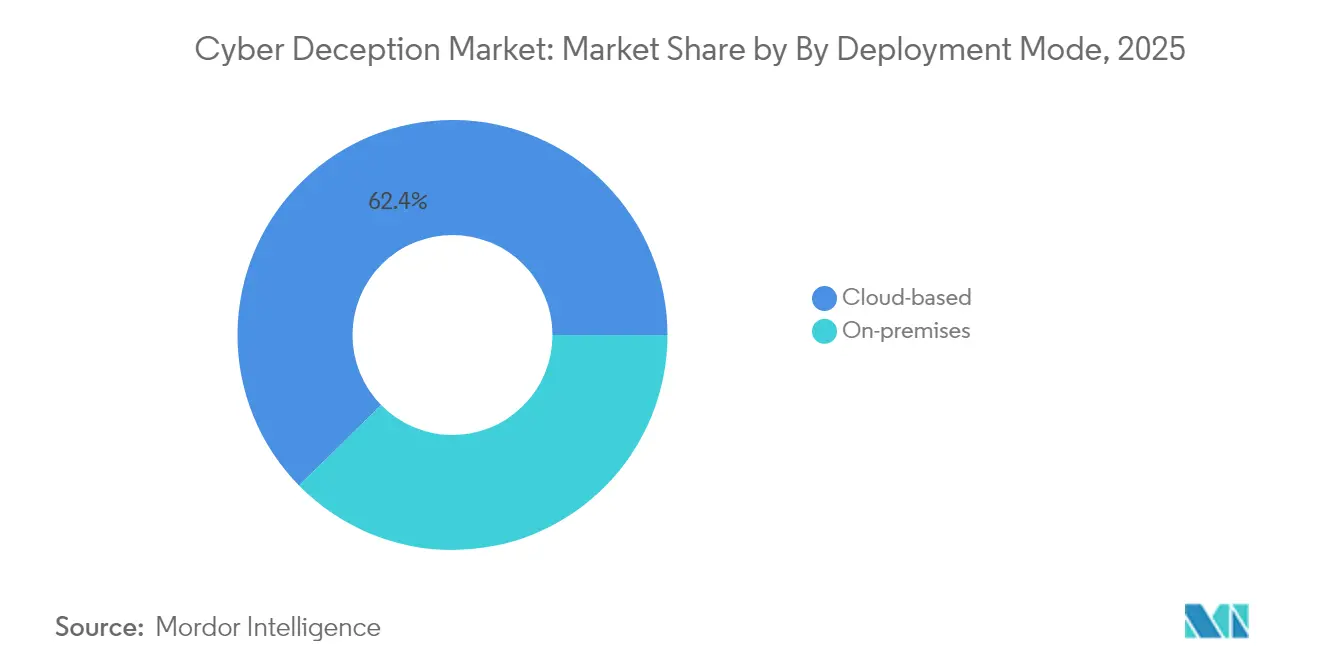

- By deployment mode, cloud-based solutions held 62.35% of the cyber deception market size in 2025 and are projected to expand at an 18.02% CAGR to 2031.

- By end-user industry, financial services commanded a 26.62% share of the market in 2025; government and defense are forecast to accelerate at a 19.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cyber Deception Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating sophistication and volume of cyber-attacks | +3.2% | Global | Short term (≤ 2 years) |

| Rapid cloud migration and API-first architectures | +2.8% | North America and Europe, Asia Pacific core | Medium term (2-4 years) |

| Mandates for zero-trust and breach-assumed postures | +2.5% | North America and Europe | Medium term (2-4 years) |

| Shortage of skilled cyber workforce boosting automation demand | +2.1% | Global | Long term (≥ 4 years) |

| Convergence with Identity Threat Detection and Response (ITDR) | +1.8% | North America and Europe | Medium term (2-4 years) |

| Shift of deception tooling into XDR/SSE platforms | +1.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication and Volume of Cyber-Attacks

Advanced persistent threats now leverage living-off-the-land tactics, supply-chain infiltration, and AI-generated phishing lures that bypass signature engines. Deception fills detection gaps by luring adversaries into high-fidelity decoys that log every command and payload. The U.K. National Cyber Security Centre’s 5,000-node deception program, launched in 2024, illustrates how national agencies harvest attacker tradecraft to refine defense playbooks.[2]NATIONAL CYBER SECURITY CENTRE, “Nation-Scale Cyber Deception Evidence Base,” ncsc.gov.uk Enterprises mirror that approach: a U.S. healthcare network, for example, seeded honey tokens across its electronic records cluster and cut ransomware dwell time from days to under two hours after the first decoy trigger.

Rapid Cloud Migration and API-First Architectures

Serverless functions, microservices, and multicloud data paths multiply attack surfaces beyond the reach of perimeter firewalls. Containerized deception appliances now deploy via Terraform scripts and autoscale with Kubernetes clusters, letting security teams cloak every new workload in minutes. Research published in Scientific Reports demonstrated that a single-tenant cloud honeypot caught 67% of credential-stuffing attempts missed by WAF rules while adding under 1% latency to API calls. Organizations adopting Infrastructure-as-Code rally around such evidence because decoys move at the same velocity as DevOps pipelines.

Mandates for Zero-Trust and Breach-Assumed Postures

Policy is a force multiplier. The U.S. Department of Defense now stipulates deception layers as one of nine zero-trust pillars required across all agencies by 2027. Parallel updates to the NIST Cybersecurity Framework position deception as a control for “continuous validation” activities, pushing federal contractors to embed traps alongside identity, endpoint, and network controls.[3]NATIONAL INSTITUTE OF STANDARDS AND TECHNOLOGY, “NIST Cybersecurity Framework Revision,” nist.gov Commercial banks in Europe echo that alignment; one pan-European lender added synthetic SWIFT messages to detect fraudulent transfers and met new PSD2 monitoring clauses without re-architecting its core banking host.

Shortage of Skilled Cyber Workforce Boosting Automation Demand

The global shortfall of roughly 4 million practitioners drives buyers to tools that “self-drive.” Modern platforms auto-generate decoys tied to Active Directory attributes, update kernel lures in real time, and surface distilled attacker paths rather than raw alerts. A U.S. Army Research Office grant to Penn State University funds automated honeypot farms capable of adapting to contested radio links with no operator input, proving that autonomous deception is technically viable.[4]PENN STATE UNIVERSITY, “Army Research Office Grant Funds Autonomous Deception Research,” psu.edu Managed service providers seize that model to deliver deception at scale to resource-constrained mid-market clients.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration and tuning costs for brown-field networks | -1.8% | Global, particularly legacy-heavy industries | Short term (≤ 2 years) |

| Limited cybersecurity budgets among SMBs | -1.5% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Proliferation of open-source decoy frameworks lowering perceived value | -1.2% | Global | Long term (≥ 4 years) |

| Adversarial-AI capable of fingerprinting decoy | -0.9% | Advanced economies with AI capabilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration and Tuning Costs for Brown-Field Networks

Organizations running flat, legacy networks lack segmentation points for realistic decoy placement. Retrofitting virtual LANs, span ports, and identity services drives up project costs and extends timelines beyond 12 months in industries such as energy or manufacturing. One European petro-chemical firm reported that prerequisite network upgrades doubled its initial deception budget before the first trap was online, proving that tooling alone cannot solve architectural rot.

Limited Cybersecurity Budgets Among SMBs

While ransomware groups target small suppliers to leapfrog into enterprise ecosystems, most SMBs still prioritize antivirus renewals over deception investments. Open-source projects such as Modern Honey Network and T-Pot offer basic trap functionality, but many owners lack the expertise to interpret alerts, eroding perceived ROI. For example, a Latin-American logistics broker deployed Cowrie SSH decoys yet disabled them within weeks after alert fatigue overwhelmed its two-person IT staff.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Layer: Network Security Dominates Despite Endpoint Acceleration

Network deception products accounted for a 34.88% share of the cyber deception market in 2025, reflecting their historical role as perimeter tripwires. Endpoint deception, however, is scaling at a 17.63% CAGR as every remote laptop and IIoT gateway becomes a pivot point. That growth reshapes the cyber deception market because device-centric lures close visibility gaps that network taps cannot monitor behind encrypted tunnels.

In practice, vendors push lightweight agents that spin up bogus registry hives, fake browser cookies, and decoy USB drives whenever a threat actor lands on an endpoint. For instance, a Southeast-Asian telecom placed false 5G management scripts on engineering laptops; attackers triggered the lure within hours, enabling security teams to isolate compromised accounts before any core switch was touched. Application security deception also gathers momentum—the rise of API honeypots that mimic GraphQL endpoints lets SaaS providers detect credential abuse in real time. Data-centric deception, meanwhile, embeds honey-tokens inside structured query language tables and object storage buckets; one retailer used that tactic to discover rogue warehouse APIs siphoning customer PII within minutes. Altogether, the layered approach moves the cyber deception market toward unified consoles that orchestrate decoys across packets, processes, and data artifacts.

By Service Type: Managed Services Lead Growth and Share

Managed deception services held 38.74% of the cyber deception market share in 2025 and carry an 17.72% CAGR, evidence that many enterprises would rather outsource trickery than recruit scarce deception engineers. Providers run centralized “Decoy Operations Centers” that manage thousands of traps, share new indicators across tenants, and supply post-incident forensics. That model aligns with board mandates to reduce mean-time-to-detect without ballooning headcount.

Professional services still matter because successful deception demands network baselining, crown-jewel mapping, and cultural buy-in. Consultants now embed field exercises, phishing simulations, and purple-team labs into deployment phases so that internal responders learn how to act on decoy telemetry. For example, a Fortune 100 manufacturer hired a boutique integrator to knit deception alerts directly into its SAP GRC console, proving value to auditors within a single quarter. This blended approach underlines why the cyber deception industry monetizes both recurring managed fees and high-margin consulting.

By Deployment Mode: Cloud-Based Solutions Accelerate Market Transformation

Cloud-hosted products captured 62.35% of the cyber deception market in 2025 and are on course for an 18.02% CAGR. Elastic scalability, pay-per-decoy billing, and API-level provisioning lower barriers for DevSecOps teams. A global media streamer, for instance, uses Terraform modules to spin up regional honeypots side-by-side with customer data clusters, obtaining attacker telemetry in under 20 minutes per region.

On-premises appliances persist in air-gapped military and critical-infrastructure zones, but even those owners adopt cloud dashboards for analytics. Hybrid models, therefore, blend local decoys with SaaS-based control planes that crunch billions of log entries daily. As cloud-native adoption widens, attack surface coverage grows faster than staff capacity, reinforcing managed service demand and, in turn, lifting the entire cyber deception market.

By End-User Industry: Financial Services Lead While Government Accelerates

Banks, insurers, and payment processors retained the largest 26.62% slice of the cyber deception market in 2025. They rely on decoy SWIFT connectors, fake employee portals, and synthetic payment files to spot lateral movement and account takeover. Case in point: a multinational bank embedded honey-tokens in dormant trading accounts; threat actors triggered those tokens during an insider scheme, allowing compliance teams to freeze assets within hours.

Government and defense organizations are the fastest climbers, growing at 19.78% CAGR because zero-trust mandates attach budget to deception rollouts. Initiatives like the U.S. DoD’s phased migration plan funnel procurement toward platforms that report readiness metrics directly into program management dashboards. Healthcare operators adopt deception to protect connected imaging devices, while retail chains deploy it to flag fraudulent gift-card APIs. Energy utilities use SCADA decoys that mirror Modbus traffic, revealing state-sponsored reconnaissance well before a breaker-trip attempt. Collectively, these case studies keep the cyber deception market responsive to sector-specific pain points.

Geography Analysis

North America controlled 43.10% of the cyber deception market in 2025, anchored by mature budgets, R&D clusters in Silicon Valley and Tel Aviv, and regulatory catalysts such as executive orders on zero-trust migration. U.S. technology consolidators continue to absorb niche vendors; SentinelOne’s USD 616.5 million purchase of Attivo Networks merged deception with autonomous endpoint protection in a single agent. Canadian telcos likewise deploy deception inside 5G cores to meet CRTC supply-chain directives.

Asia-Pacific is the fastest riser at 22.05% CAGR. Nations such as Singapore, Australia, and Japan issue sectoral cyber frameworks that explicitly call for threat-hunting controls, spawning budgets for deception pilots. For example, an Australian energy grid deployed containerized ICS decoys to comply with the Security of Critical Infrastructure Act amendments, catching credential-harvesting bots within weeks. Chinese cloud hyperscalers bundle deception APIs so that domestic SaaS developers can add “honeypot as code” to CI/CD pipelines. Meanwhile, Indian fintech start-ups lure carding gangs with fake Unified Payments Interface endpoints, feeding intelligence to local CERT teams.

Europe maintains steady mid-teens growth. The EU Cyber Resilience Act pushes continuous monitoring, and Germany’s BSI agency cites deception as a recommended control. Strict data-residency rules mean several vendors now offer sovereign-cloud nodes in Frankfurt, Paris, and Madrid. In the Middle East and Africa, smart-city build-outs in Riyadh and Dubai allocate funding for OT decoys inside district cooling plants. South American growth is modest yet rising; Brazil’s PIX instant-payment rails drive banks to plant decoy APIs that emulate transaction gateways, intercepting credential sprays directed at small merchants.

Competitive Landscape

The cyber deception market remains moderately fragmented but is tilting toward platform suites. Beyond SentinelOne’s Attivo deal, Proofpoint picked up Illusive Networks to dock decoys inside email threat-intelligence loops, while Commvault absorbed TrapX Security to fuse ransomware detection with data-backup orchestration. CrowdStrike and Fortinet stitched together Falcon and FortiDeceptor telemetry, showcasing how cross-vendor alliances matter when customers already run heterogeneous security stacks.

Competitive moats now revolve around AI-driven decoy generation, low-code orchestration, and integration mileage across SIEM, SOAR, and identity tools. Vendors focusing on vertical add-ons—SCADA lures for manufacturing, 5G protocol decoys for telecom—gain traction because generic Windows traps no longer suffice. Adversarial-AI research challenges vendors to deliver adaptive deception that randomizes fingerprints each time an attacker probes. Given that the top five suppliers collectively control under 50% of revenue, room remains for specialists like CounterCraft to carve public-sector niches.

Cyber Deception Industry Leaders

SentinelOne Inc.

Akamai Technologies Inc.

CrowdStrike Holdings Inc.

Trend Micro Incorporated

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SentinelOne completed the roll-up of Attivo Networks deception code into its Singularity platform, achieving single-agent deployment parity across Windows, Linux, and macOS hosts.

- December 2024: Palo Alto Networks disclosed its intent to buy Protect AI for USD 700 million, signaling a future in which AI model hardening and decoy pipelines share telemetry.

- November 2024: CrowdStrike deepened its Fortinet alliance to stream Falcon behavioral hashes into FortiDeceptor lures, producing near-real-time cross-vector containment.

- October 2024: Commvault acquired TrapX Security, embedding ransomware-triggered snapshots that spin up immutable backups once a decoy alarm fires.

Global Cyber Deception Market Report Scope

System breaching is an activity carried out by cyber hacker to extract sensitive information which may lead to cyber-attacks. Cyber deception is one of the emerging trends in cyber defense systems. It is a controlled act to capture the network, create uncertainty and confusion against sudden attacks establishing situational awareness. Instances such as software infiltration and cloud-hacks increase the need for cyber deception solutions in several sectors. These solutions can identify, analyze, and protect against various forms of cyber-attacks in real time. The best-known attempts of cyber deception in different commercial sectors are honeypots and honeynets. Cyber deception solutions have been gaining increasing momentum to protect networks, devices from malicious attacks, ransom wares, sophisticated cybercriminals, and Advanced Persistent Threats (APTs).

| Application Security |

| Network Security |

| Data Security |

| Endpoint Security |

| Professional Services |

| Managed Services |

| On-premises |

| Cloud-based |

| BFSI |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Retail and e-Commerce |

| Energy and Utilities |

| Government and Defense |

| Other Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Layer | Application Security | ||

| Network Security | |||

| Data Security | |||

| Endpoint Security | |||

| By Service Type | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | On-premises | ||

| Cloud-based | |||

| By End-user Industry | BFSI | ||

| IT and Telecommunications | |||

| Healthcare and Life Sciences | |||

| Retail and e-Commerce | |||

| Energy and Utilities | |||

| Government and Defense | |||

| Other Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the cyber deception market in 2026?

The cyber deception market size is USD 2.24 billion in 2026 and is forecast to grow at a 13.01% CAGR to USD 4.12 billion by 2031.

Which segment grows fastest within cyber deception?

Endpoint deception is advancing at a 17.63% CAGR as remote work and IoT proliferation make every device a potential decoy platform.

Why are managed services popular for cyber deception deployments?

Managed offerings supply 24/7 monitoring, expert tuning, and shared threat intelligence, allowing firms to adopt deception without expanding internal headcount.

What drives adoption of deception in government and defense?

Zero-trust mandates and nation-state threat escalation push agencies to deploy decoys that validate user and device behavior continuously.

How does cloud migration influence cyber deception strategies?

Cloud-native workloads need decoys that autoscale and integrate through APIs, making SaaS deception platforms the preferred deployment mode.

Page last updated on: