Deception Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

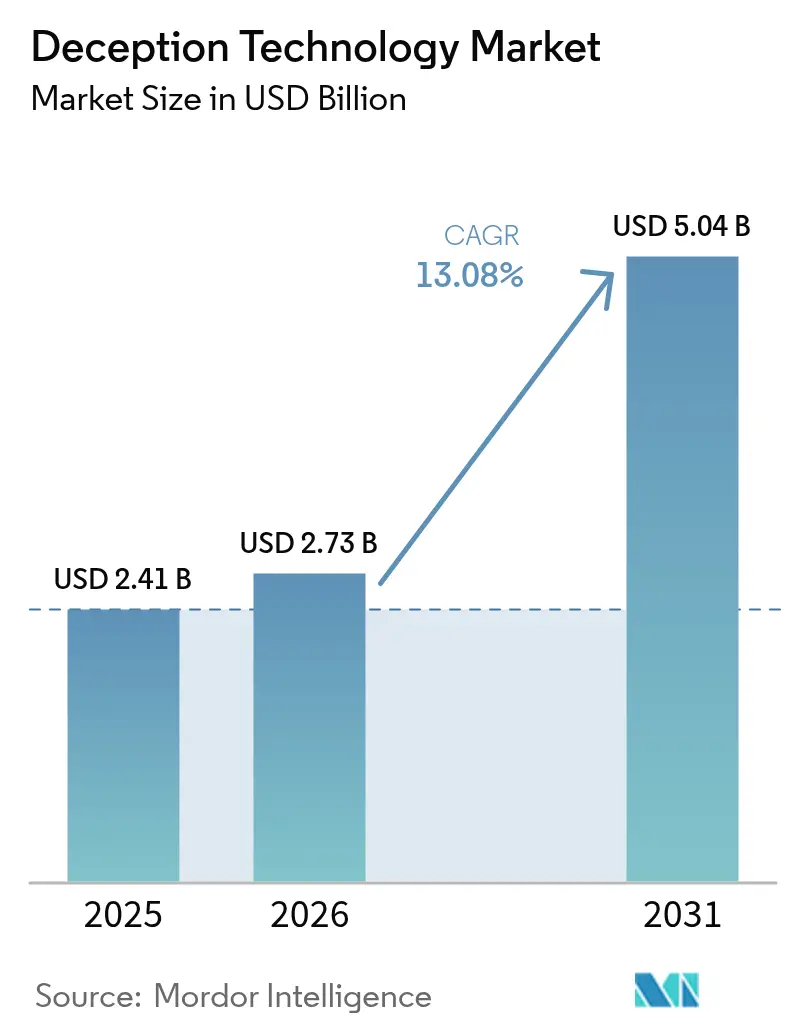

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 5.04 Billion |

| Growth Rate (2026 - 2031) | 13.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deception Technology Market Analysis by Mordor Intelligence

The deception technology market size was valued at USD 2.41 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 5.04 billion by 2031, at a CAGR of 13.08% during the forecast period (2026-2031). Rising zero-day exploits, AI-driven deepfake fraud, and cloud-native workload expansion compel security teams to adopt early-warning controls that spot attackers inside the network before damage occurs. Vendors now weave decoys into zero-trust micro-segmentation, giving defenders tripwires that work even when identities or endpoints are compromised. Demand also accelerates because cyber-insurance carriers require proactive lateral-movement detection as a condition for favorable premiums. Although North America keeps spending leadership, the deception technology market gains rapid momentum in Asia-Pacific as multicloud adoption surges and local regulators tighten breach-notification rules.

Key Report Takeaways

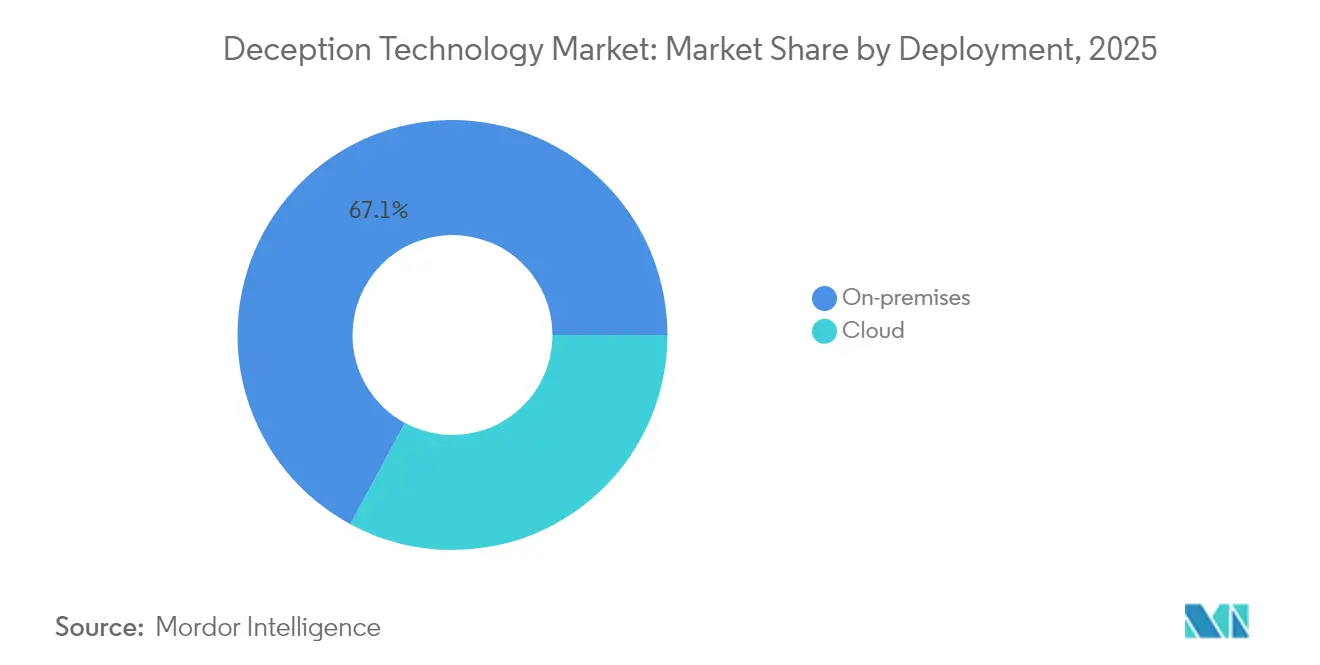

- By deployment, on-premises models led with 67.12% of deception technology market share in 2025, while cloud implementation records the fastest 14.84% CAGR through 2031.

- By organization size, large enterprises captured 69.55% revenue in 2025; the SME segment is projected to expand at 14.41% CAGR to 2031.

- By service, managed services accounted for 67.93% of the deception technology market size in 2025 and are set to post a 14.28% CAGR through 2031.

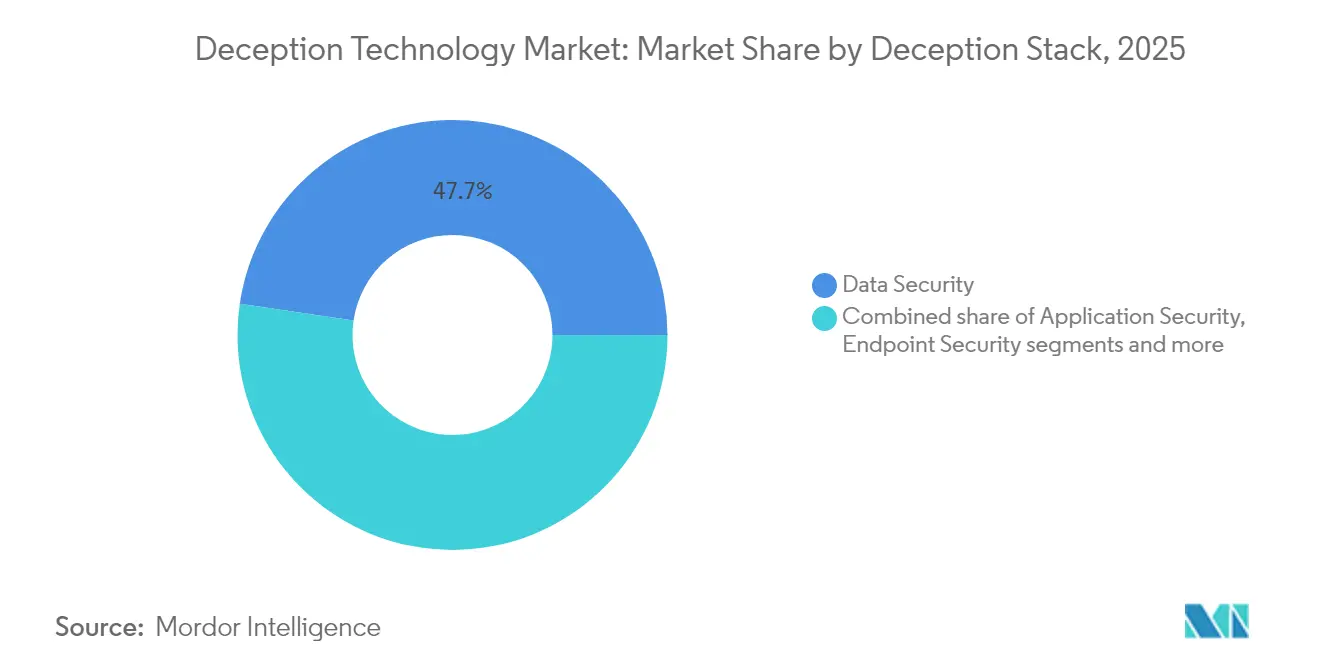

- By deception stack, data security remained dominant at 47.68% share in 2025, whereas endpoint security is forecast to grow 13.81% annually to 2031.

- By end-user, BFSI held 35.72% share in 2025; healthcare is forecast to grow at a 13.17% CAGR.

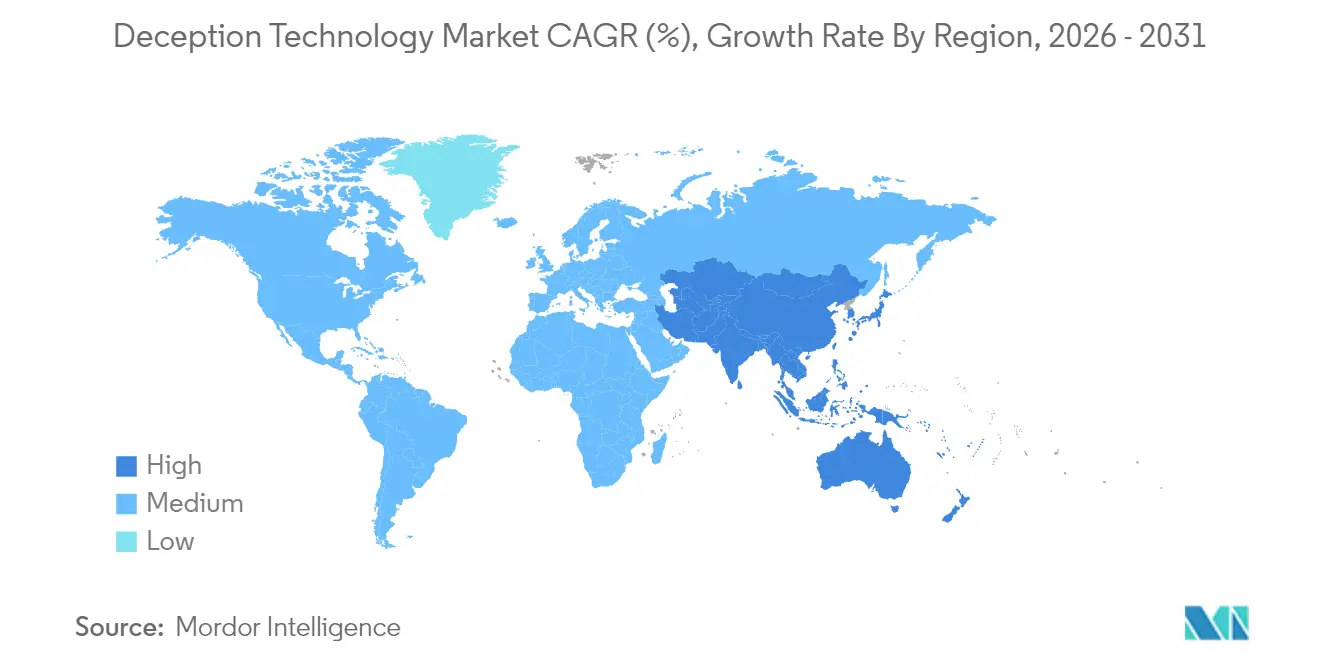

- By geography, North America contributed 41.35% revenue in 2025; Asia-Pacific will grow fastest at 13.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Deception Technology Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in zero-day exploits and targeted APTs | 3.2% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Escalating cloud-native workloads broaden attack surface | 2.8% | Global, led by APAC and North America | Medium term (2-4 years) |

| CISO preference for low-friction, agent-less detection tools | 2.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Rise of AI-generated deepfake identity attacks | 1.9% | Global, with early impact in BFSI and government sectors | Short term (≤ 2 years) |

| Convergence of deception with zero-trust micro-segmentation | 1.7% | North America & Europe, gradual APAC adoption | Long term (≥ 4 years) |

| Cyber-insurance policies demanding proactive lateral-movement detection | 1.6% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Zero-Day Exploits and Targeted APTs

State-sponsored collectives automate reconnaissance with AI, finding novel vulnerabilities faster than signature-based defenses adapt. The Institute for Security and Technology notes that automated reconnaissance compresses attacker dwell time, forcing defenders to rethink reactive playbooks. Deception platforms insert believable but fake assets that weaponize curiosity; once probed, alerts trigger in seconds while production systems stay untouched. Because detection is based on attacker behavior rather than threat-intelligence feeds, the deception technology market provides resilience against bespoke malware that evades hash-matching controls. Vendors now pre-package decoys for industrial control systems and SaaS APIs, reflecting attacker pivot toward operational technology.

Escalating Cloud-Native Workloads Broaden Attack Surface

Containerized and serverless applications can spin up and down within minutes, leaving security operations centers blind to east-west traffic. Zscaler deploys generative-AI decoys that mimic large-language-model endpoints, luring attackers into instrumented sandboxes[1]Zscaler, “Zscaler Introduces Generative AI Decoys for Cloud-Native Environments,” zscaler.com. Because decoys scale automatically inside Kubernetes namespaces, defenders gain continuous coverage even as underlying microservices change. The deception technology market capitalizes on cloud providers’ metadata APIs to place traps inside virtual private clouds without installing agents. As organizations adopt multi-cloud strategies, cross-provider decoy orchestration becomes a buying criterion, especially in regulated industries that cannot centralize logs in a single region.

CISO Preference for Low-Friction, Agent-Less Detection Tools

Tool sprawl produces alert fatigue and ballooning license costs. CISOs gravitate toward technologies that integrate smoothly, emit few false positives, and require little maintenance. Deception platforms meet these demands because asset placement is passive; nothing touches the endpoint. SC Media reports that organizations reduce mean-time-to-detect by 48 hours when shifting to deception-first strategies. Vendor dashboards now expose attack paths graphically, enabling junior analysts to act without deep forensics skills. These usability gains drive procurement, particularly in mid-market firms that lack specialized threat hunters.

Rise of AI-Generated Deepfake Identity Attacks

Voice cloning and synthetic video enable fraudsters to bypass traditional verification checks. Reality Defender recorded a 245% year-over-year spike in enterprise deepfake incidents, with one-quarter impacting finance workflows. Deception solutions respond by placing counterfeit executive credentials in privileged-access vaults; any authentication attempt against these phantom identities reveals compromise. Lucinity documented a USD 25 million transfer initiated through a deepfake video call, underscoring why real-time lateral-movement flags are crucial[2]Lucinity, “Arup Deepfake Case Study,” lucinity.com. The deception technology market embeds media-forensics hooks that score the authenticity of voice traffic, linking anomalies to specific network sessions for rapid containment.

Restraints Impact Analysis of Deception Technology Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entrenched reliance on legacy honeypots | -1.8% | Global, particularly in cost-sensitive SME segments | Long term (≥ 4 years) |

| Scarcity of deception-skilled SecOps staff | -1.5% | Global, acute in APAC and emerging markets | Medium term (2-4 years) |

| Adversary use of large-language-model recon to spot decoys | -1.2% | Advanced threat actors globally | Short term (≤ 2 years) |

| Budget cannibalization by bundled EDR/XDR platforms | -0.9% | North America & Europe enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Entrenched Reliance on Legacy Honeypots

Many firms still run static honeypots deployed years ago. Attackers now fingerprint such assets through protocol quirks or uptime patterns, bypassing them with ease. This sunk-cost bias delays upgrades to adaptive decoys able to morph operating-system banners or rotate credentials automatically. Legacy honeypots also demand manual log parsing, consuming resources that should focus on real attack paths. Because these tools produce few actionable alerts, boards question ROI, thereby constraining new investment and dampening growth of the deception technology market.

Scarcity of Deception-Skilled SecOps Staff

Deploying credible decoys requires knowledge of attacker psychology, asset valuation, and network topology. Universities seldom teach these skills, so employers compete for a limited talent pool. Shortfalls are most acute in Asia-Pacific, where cybersecurity curricula concentrate on compliance rather than active defense. To close the gap, vendors embed guided workflows and offer managed services, but salaries for deception architects still command premiums that small enterprises cannot match. This workforce constraint slows broad adoption even though the technology’s value proposition is widely acknowledged.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Deception Technology Market Segment Analysis

By Deployment:

Cloud Acceleration Despite On-Premises DominanceOn-premises deployment commanded 67.12% of deception technology market share in 2025, illustrating enterprises’ need to keep high-interaction decoys close to crown-jewel systems for compliance and forensic control. That control, however, brings hardware refresh cycles and change-management overhead that limit agility. Cloud deployment contributes a modest slice today but is slated to rise at a 14.84% CAGR through 2031, the fastest pace within the deception technology market. Cloud-based consoles spin up decoys across regions within minutes, making them attractive for global branch rollouts.

Hybrid models emerge as a pragmatic bridge, letting teams place sensitive database decoys on-premises while offloading analysis and scaling tasks to public clouds. As multicloud adoption rises, buyers demand single-pane views across AWS, Azure, and Google Cloud, pushing providers to invest in identity federation and immutable infrastructure blueprints. These capabilities enhance the deception technology market size for cloud modules and convince regulation-bound sectors that shared-responsibility models can still satisfy audit controls.

By Organization Size:

SMEs Drive Adoption Through Managed ServicesLarge enterprises retained 69.55% revenue share in 2025 and continue shaping feature roadmaps by insisting on API depth, MITRE ATT&CK alignment, and advanced analytics. Yet SMEs now register a 14.41% growth trajectory, outpacing big-company spending within the deception technology market. Subscription-based managed deception services, billed per asset, cut entry barriers and deliver curated alerts that fit smaller teams’ bandwidth.

Savings compound because cloud consoles eliminate hardware purchase, allowing SMEs to reallocate capital toward employee awareness programs. For vendors, the segment’s scale effect is compelling; thousands of mid-sized customers can equal the license revenue of a handful of Fortune 500 accounts. Consequently, roadmap priorities now include low-code playbooks and automated decoy placement, features designed to compress onboarding from weeks to hours and thereby expand deception technology market size among smaller firms.

By Service:

Managed Services Dominate Through Operational EfficiencyManaged services represented 67.93% of the deception technology market size in 2025, a reflection of buyer preference for turnkey operations that offer measurable risk-reduction without headcount spikes. Growth remains brisk at 14.28% CAGR because service providers integrate deception layers with 24×7 security operations centers, handing clients curated attack timelines rather than raw logs.

Professional services still play a vital role in day-zero architecture assessments, regulatory mapping, and red-team validation. However, once baseline deployment is done, most organizations prefer subscription renewals to internal tooling. Vendors upsell premium tiers that include annual breach simulations, threat-intel enrichment, and automatic decoy refresh, driving predictable recurring revenue while broadening overall deception technology market.

By Deception Stack:

Data Security Leads While Endpoint Security AcceleratesData-centric deception kept 47.68% share in 2025 as privacy regulations impose stiff fines for record exposure. Finance and healthcare clients deploy fake database tables and document lures to spot illicit queries against personal data. This dominance underlines why the deception technology market remains tightly coupled with governance, risk, and compliance priorities.

Endpoint security decoys, though smaller today, are growing at 13.81% annually. Remote workforces, bring-your-own-device policies, and ransomware spikes drive investment in fake process trees, memory artifacts, and local credential stores that look indistinguishable from actual laptops. Integration with EDR telemetry allows security teams to pivot from detection to device isolation in seconds, raising the combined value proposition and expanding deception technology market share for endpoint-focused solutions.

By End-User:

BFSI Leadership with Healthcare AccelerationThe BFSI sector held 35.72% revenue in 2025, reflecting banks’ and insurers’ low tolerance for insider fraud and credential-stuffing risk. High-interaction decoys now imitate SWIFT terminals and trading platforms, enabling head-office SOCs to trace lateral-movement attempts that aim at payment systems.

Healthcare records command high prices on underground forums, explaining why the segment is expected to grow 13.17% annually. Hospital networks deploy medical device decoys that mimic infusion pumps or radiology equipment, catching threat actors targeting Internet-of-Medical-Things attack surfaces. Budget boosts come as regulators tighten breach-notification timetables, reinforcing the business case for the deception technology market in clinical settings.

Geography Analysis

North America Deception Technology Market

North America generated 41.35% of revenue in 2025, buoyed by stringent mandates such as CISA’s directive on incident reporting and a concentration of Fortune 100 headquarters that can fund specialized controls. Federal contracts increasingly specify deception capabilities, further cementing the region’s leadership within the deception technology market.

Europe Deception Technology Market

Europe advances steadily as the NIS2 Directive broadens the scope of entities required to maintain proactive threat-detection programs Local vendors stress data-sovereignty features, ensuring logs stay inside EU borders. Emerging EU cloud providers now embed deception natively, offering compliance-ready bundles that appeal to mid-market industrial manufacturers.

APAC, LATAM and MEA Deception Technology Market

Asia-Pacific remains the fastest-growing territory at 13.44% CAGR. Governments in Japan, India, and Singapore launch grant programs that co-fund zero-trust pilots incorporating deception. Telecom rollouts of 5G standalone cores enlarge attack surfaces, pushing operators to install signaling-protocol decoys that detect rogue base-station registration attempts. These initiatives collectively enlarge deception technology market size in the region. Meanwhile, Latin America and Middle East and Africa start integrating deception into critical-infrastructure revamps, although budget constraints and talent gaps temper near-term uptake.

Regulatory Landscape

Regulation affecting deception technology is increasingly framed through cyber-risk-management and secure-by-design requirements rather than product-specific rules. In the United States, NIST SP 800-53 Rev. 5 formalizes deception-aligned controls such as SC-26 (Decoys) and SC-30 (Concealment and Misdirection), which agencies and contractors use as a benchmark for control mapping in security programs. In Europe, the NIS2 Directive (Directive (EU) 2022/2555) expands the scope of entities required to implement risk-management measures and incident handling, reinforcing demand for high-fidelity detection tools that provide auditable evidence of attacker activity.

In October 2024, the EU Cyber Resilience Act (Regulation (EU) 2024/2847) introduced lifecycle cybersecurity obligations for manufacturers of products with digital elements, increasing scrutiny on how security capabilities are designed, maintained, and updated across the product lifecycle. Commission Implementing Regulation (EU) 2024/2690, effective from October 2024, also sets technical and methodological requirements for NIS2 risk-management measures. ENISA published technical implementation guidance on cybersecurity risk-management measures in December 2025, giving operators and suppliers clearer expectations for controls selection, documentation, and verification. At the policy level, cross-border compliance complexity remains a theme, reflected in the OECD May 2026 work on international coherence of cybersecurity regulations and related alignment efforts by industry bodies such as the Cybersecurity Tech Accord.

Value Chain Analysis

The value chain starts with threat research and deception-content engineering, where vendors design realistic decoys, honeytokens, and breadcrumbs mapped to enterprise environments (identity systems, cloud workloads, endpoints, networks, and OT/IoT). Platform development then combines orchestration (policy, placement, rotation), telemetry collection, and analytics, followed by integrations into SOC tooling such as SIEM/SOAR/XDR for alert enrichment and automated response. Delivery typically splits between direct software subscriptions (often cloud-managed consoles) and channel-led implementations where MSSPs and system integrators package deception with monitoring, incident response playbooks, and continuous tuning, reflecting demand for managed services.

Downstream, deployment and operations depend heavily on access to enterprise control planes and visibility layers, including directory services, cloud APIs, container platforms, EDR sensors, and network telemetry. This makes partnerships and integration ecosystems a key route to scale. NIST Cybersecurity Framework 2.0 (SP 1305) reinforces governance for cyber-supply-chain risk management, and buyers increasingly ask for proof that deception telemetry can be operationalized within existing SOC processes rather than remaining an isolated tool. Defense and government procurement also drives specialized packaging via integrators, illustrated by CounterCrafts December 2025 partnership with Mission First Cyber to integrate deception into the Rhombus Fly-Away Kit for US federal and defense operations, linking product capabilities with fieldable deployment kits and services.

Competitive Landscape

Top Companies in Deception Technology Market

The deception technology market shows moderate fragmentation. Large cybersecurity suites integrate native deception modules, while specialist pure-plays innovate aggressively on AI-driven lures. Illusive Networks’ integration with CrowdStrike Falcon enriches endpoint telemetry with deception-triggered attribution, slashing average dwell time by 60%[4]CrowdStrike, “Illusive Networks Integration Unlocks Endpoint Deception,” crowdstrike.com. Zscaler collaborates with NVIDIA to accelerate model-based decoy generation that adapts to attacker behavior in real time.

Mergers and acquisitions reshapes boundaries: Google’s USD 32 billion purchase of Wiz expands cloud-native coverage, while CyberArk’s Venafi acquisition injects machine-identity risk data into decoy placement logic. Start-ups such as CyberTrap target mid-size European firms with subscription bundles combining deception and managed detection, capitalizing on skills shortages. For incumbents, proof-of-value cycles focus on measurable ROI—principally reduced mean-time-to-detect and improved audit outcomes—as procurement boards grow wary of shelfware.

Competitive intensity is expected to rise as privacy-enhancing computation and quantum-safe protocols create new decoy formats. Vendors able to demonstrate seamless orchestration across endpoints, cloud, and operational technology, without adding analyst workload, will gain share. Conversely, firms that rely on static honeypot architectures risk marginalization as attackers exploit pattern recognition to evade detection, reinforcing dynamic deception as the baseline expectation within the deception technology market.

Deception Technology Industry Leaders

Illusive Networks

Commvault Systems Inc.

Smokescreen Technologies Pvt. Ltd

Attivo Networks Inc. (SentinelOne Inc.)

Rapid7 Inc.

- *Disclaimer: Major Players sorted in no particular order

Deception Technology Market Companies Covered in this Report

- Illusive Networks

- Attivo Networks (SentinelOne)

- Rapid7

- Acalvio Technologies

- CounterCraft

- CyberTrap

- TrapX Security

- Smokescreen Technologies

- Ridgeback Network Defense

- LogRhythm

- WatchGuard Technologies

- Broadcom (Symantec)

- Morphisec

- Fortinet (FortiDeceptor)

- Zscaler

- Microsoft (Security Honeytokens)

- Akamai

- Palo Alto Networks

- Fidelis Cybersecurity

- Commvault (TrapX integration)

Market Opportunities and Future Outlook

Opportunity is expanding where organizations need measurable, low-false-positive internal detection that complements zero trust and incident reporting obligations. Deception controls map cleanly to established frameworks such as NIST SP 800-53 Rev. 5 (SC-26 Decoys, SC-30 Concealment and Misdirection), and incident handling guidance is increasingly explicit about monitoring third-party and external service activity, including via deception techniques (as reflected in NIST SP 800-61r3). That creates whitespace for vendors and service providers to package deception as an auditable control with clear operational runbooks and evidence artifacts, particularly in regulated sectors where boards and insurers ask for proof of lateral-movement detection.

National and sector programs also provide direct pull-through for broader deployments and validation. The UK National Cyber Security Centre documented national-scale cyber deception trials involving 121 organizations and 14 commercial providers across cloud and OT environments (December 2025), highlighting practical deployment patterns and integration needs beyond legacy honeypots. Product strategy and commercialization benefit from demand for adaptive, rotating decoy ecosystems that place breadcrumbs across identity, cloud, and hybrid environments, while feeding telemetry into SOC orchestration for faster containment. Managed services can reduce skills barriers for SMEs and constrained security teams. Separately, compliance pressure around secure-by-design product lifecycles in the EU (Cyber Resilience Act, published October 2024) supports continued demand for deception capabilities that can be maintained, updated, and documented as part of ongoing security engineering processes, not only as a one-time deployment.

Recent Industry Developments in Deception Technology Market

- May 2026: The OECD published a policy paper on international coherence of cybersecurity regulations, highlighting the ongoing compliance fragmentation faced by global operators and suppliers. The focus on alignment and comparable control expectations increases the value of deception capabilities that map to commonly referenced standards and generate auditable evidence across jurisdictions.

- August 2025: Commvault closed its acquisition of Satori Cyber Ltd to strengthen data security and AI governance capabilities, adding data discovery, classification, and access control features within the Commvault Cloud platform. This supports deception-led data protection use cases where organizations place lures around sensitive datasets and need stronger governance context to prioritize and validate alerts.

- April 2024: Commvault announced the acquisition of Appranix to add cloud-native cyber recovery and application rebuild capabilities to Commvault Cloud. Enhanced recovery workflows complement deception deployments by shortening restoration timelines after confirmed compromise and tightening the loop between early attacker detection and resilient recovery execution.

Deception Technology Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers vendor revenues earned from deception technology software and related services that place realistic decoys and lures in IT environments to detect, misdirect, and study attackers after initial access.

Scope exclusions: We exclude hardware-only honeypot appliances used mainly for lab or academic testing, and we do not count general SIEM, EDR, or firewall spending unless deception capabilities are the paid item.

Segments Covered in This Report

- By Deployment

- On-premises

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Service

- Managed Services

- Professional Services

- By Deception Stack

- Data Security

- Application Security

- Endpoint Security

- Network Security

- By End-User

- Government

- Defense

- BFSI

- IT and Telecommunication

- Healthcare

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base context and to keep assumptions anchored to real cybersecurity activity and IT spending direction. We leaned on public sources such as NIST publications, CISA advisories, SEC filings and annual reports, and cybersecurity incident datasets and papers published through platforms like NIST NVD and IEEE.

We also referenced cloud adoption and enterprise security spending indicators from sources such as the World Bank, OECD, and selected national statistics portals, then we matched them to product documentation and publicly available pricing disclosures. To validate supplier footprints and revenue mix at a high level, a paid subscription covering company financials and another covering patents were used where helpful. The sources listed here are illustrative, and many other public documents and references were reviewed to fill gaps and cross-check assumptions.

Primary Interviews and Surveys

Primary work focused on confirming what is actually purchased under deception budgets and how deployments are scoped across networks, endpoints, identities, and cloud workloads. We spoke with solution leaders, security managers, and functional owners across the Americas, EMEA, and APAC, so pricing logic, adoption rates, and service attach assumptions could be tested region by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 21% | APAC: 51% |

| Mid tier: 40% | Functional/Unit leaders: 22% | EMEA: 29% |

| Smaller Players: 21% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction of the addressable spend pool using enterprise security software and services trends, then it is narrowed using adoption and deployment intensity for deception use cases. Once the demand pool is shaped, the model is checked with selective bottom-up approximations from supplier revenue signals, sampled pricing ranges, and channel and partner feedback.

Key inputs are kept practical, such as active cyber intrusion frequency, zero trust and breach-assumption program adoption, cloud workload growth, average deployed decoy density per environment, and the mix shift between licenses and managed services. When a data point is missing for smaller countries or newer buyers, we interpolate using comparable IT spending and security maturity indicators, then we re-test the output in interviews.

For forecasting, we rely on scenario analysis supported by a light multivariate regression, where independent variables include security budget growth, cloud migration pace, and breach exposure trends. Assumptions are adjusted only after the variable movement is consistent with what practitioners say they are budgeting for next.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals, including cybersecurity spending direction, cloud adoption pace, and reported breach activity trends. Where large jumps appear, the inputs are re-reviewed, and follow-up calls are triggered to confirm whether it is a real demand shift or an assumption error.

Before publication, the model is reviewed in multiple steps by analysts who did not build the first version. This helps catch currency timing issues, double counting between software and services, and unrealistic pricing curves. Reports are refreshed annually, and interim updates are made when major events materially change buyer priorities. Right before delivery, we run a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Deception Technology Market Size Measured Against Other Published Estimates

Published market numbers for deception technology often vary because the product scope is defined differently and the year anchors are not always the same. Differences also come from how services are treated, what counts as a deception platform versus a broader threat detection stack, and how pricing is converted across currencies and contract terms.

In practice, the widest spread is usually driven by whether adjacent security tools are bundled into the same spending bucket, plus whether managed services are fully included or treated as optional add-ons. Another driver is the starting year used for growth curves, since a one-year shift in a fast-growing cybersecurity niche can move the market value by a noticeable amount.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.73 B (2026) | |

| Industry Research Publisher A | USD 2.18 B (2024) | Uses an earlier anchor year and a shorter horizon, which can understate near-term uplift when cloud workload coverage and service attach rates rise after 2024. |

| Global Research Publisher B | USD 2.54 B (2025) | Targets a different base year and a longer forecast window, and may apply a smoother pricing progression that can dilute step changes from new managed service bundles and multi-year contract repricing. |

The table indicates that timing and what is counted inside the buying basket explain most of the gap, not just math. By treating platform revenue and attached services as included only when they are directly tied to deception deployments, and by keeping the 2026 starting point consistent with the forecast curve, the estimate stays aligned to the purchase reality used in Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the deception technology market?

The market reached USD 2.73 billion in 2026 and is projected to climb to USD 5.04 billion by 2031.

Which segment is growing fastest within the deception technology market?

Cloud deployment is pacing the field with a 14.84% CAGR thanks to its agility and ease of rollout.

Why are insurers pushing companies toward deception solutions?

Many cyber-insurance policies now require proactive lateral-movement detection, and decoys provide verifiable evidence that attackers have breached internal networks.

How does deception technology help against deepfake attacks?

Vendors place fake executive identities and voice patterns within decoy systems so that any deepfake attempt trips an alert before real credentials are touched.

Which region is forecast to lead growth?

Asia-Pacific is expected to expand at a 13.44% CAGR as digital-transformation projects accelerate and regulators tighten security mandates.

Are deception platforms difficult to manage?

Modern offerings are agent-less and often delivered as managed services, letting even small security teams gain high-fidelity alerts without heavy operational overhead.

Page last updated on: