Privacy Enhancing Technologies Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.97 Billion |

| Market Size (2030) | USD 12.26 Billion |

| Growth Rate (2025 - 2030) | 19.79% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

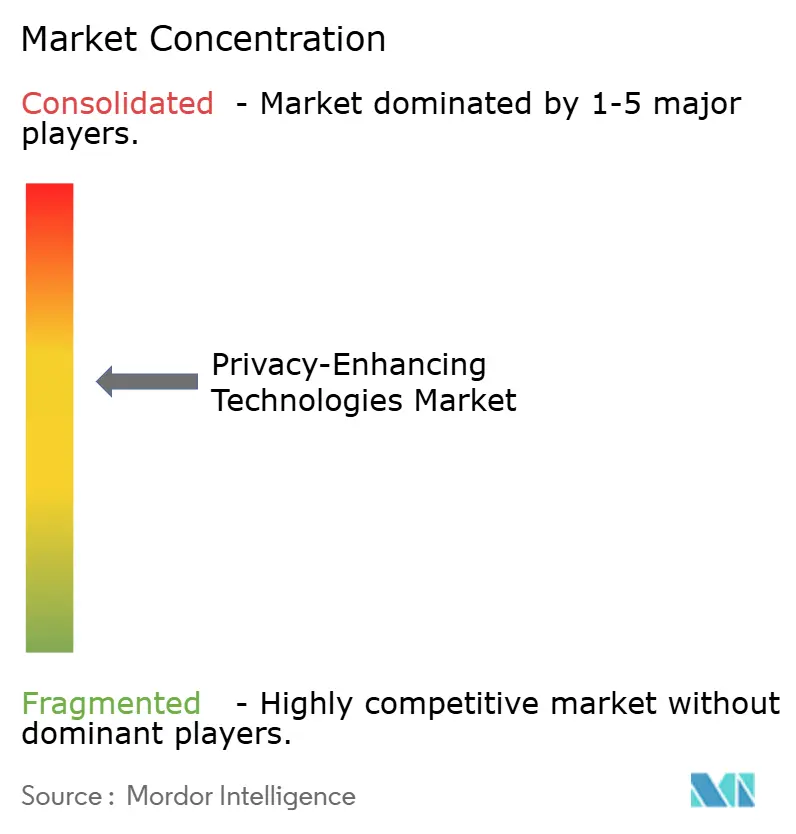

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Privacy Enhancing Technologies Market Analysis by Mordor Intelligence

The Privacy-Enhancing Technologies (PETs) market size stood at USD 4.97 billion in 2025 and is forecast to expand to USD 12.26 billion in 2030, reflecting a 19.79% CAGR during the period. This rapid growth comes as enterprises balance data utility with tightening privacy rules such as PCI-DSS 4.0 and FedRAMP-High that call for cryptographically enforced protections. Momentum also stems from quantum-safe deadlines, AI-driven data processing, and venture capital inflows that help vendors commercialize advanced cryptography. Strategic alliances among chipmakers, cloud hyperscale’s, and PET specialists shorten deployment cycles, while hardware progress narrows the cost gap between encrypted and clear-text computation. Demand is highest in regulated sectors that view PETs as a license to operate, yet retail and Web3 innovators increasingly treat confidential computing as a competitive differentiator.[1]Greg Lavender, “Confidential AI: The Convergence of Security, Privacy and AI,” Intel Community, intel.com

Key Report Takeaways

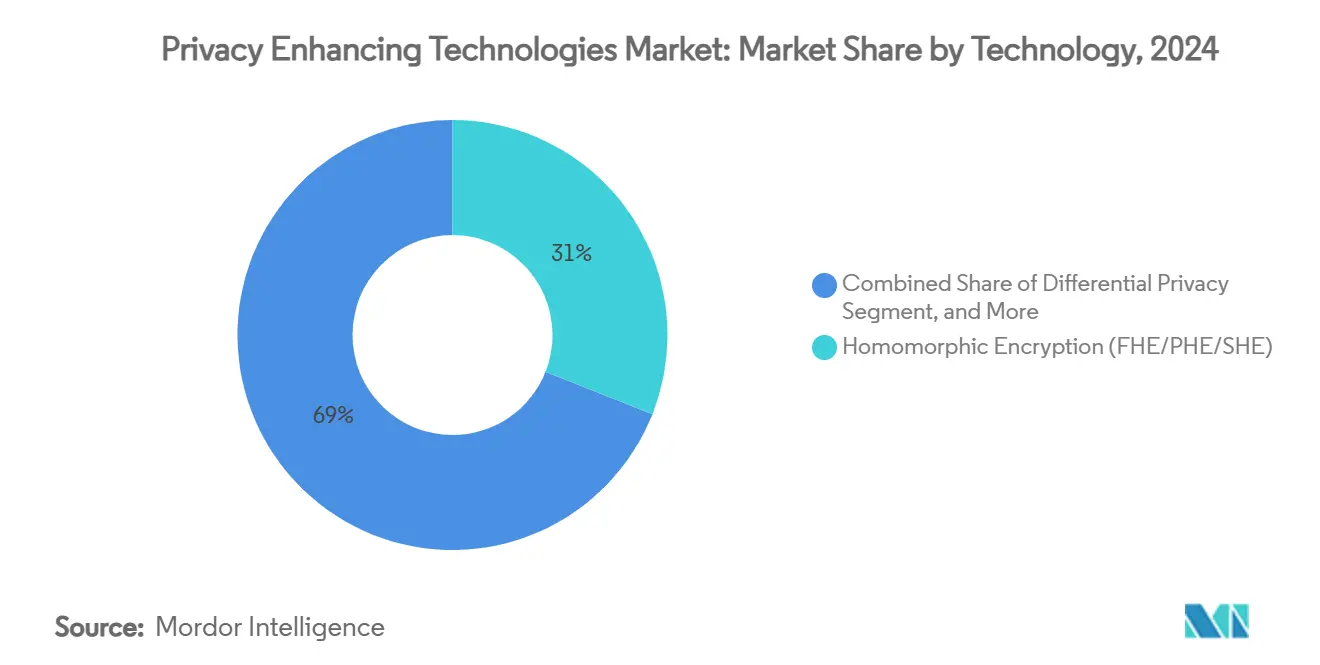

- By technology, homomorphic encryption led with a 31.20% revenue share in 2024, while zero-knowledge proofs posted the fastest CAGR at 25.71% through 2030.

- By application, AI/ML model training accounted for 26.40% of the Privacy-Enhancing Technologies market share in 2024, whereas blockchain and Web3 are advancing at a 26.82% CAGR to 2030.

- By deployment model, cloud-based PET services commanded 58.00% of the 2024 Privacy-Enhancing Technologies market size, with edge and IoT nodes set to grow at 24.55% CAGR over the forecast period.

- By end-user industry, BFSI held 27.90% share of the 2024 Privacy-Enhancing Technologies market size, while retail and eCommerce are projected to expand at 26.22% CAGR through 2030.

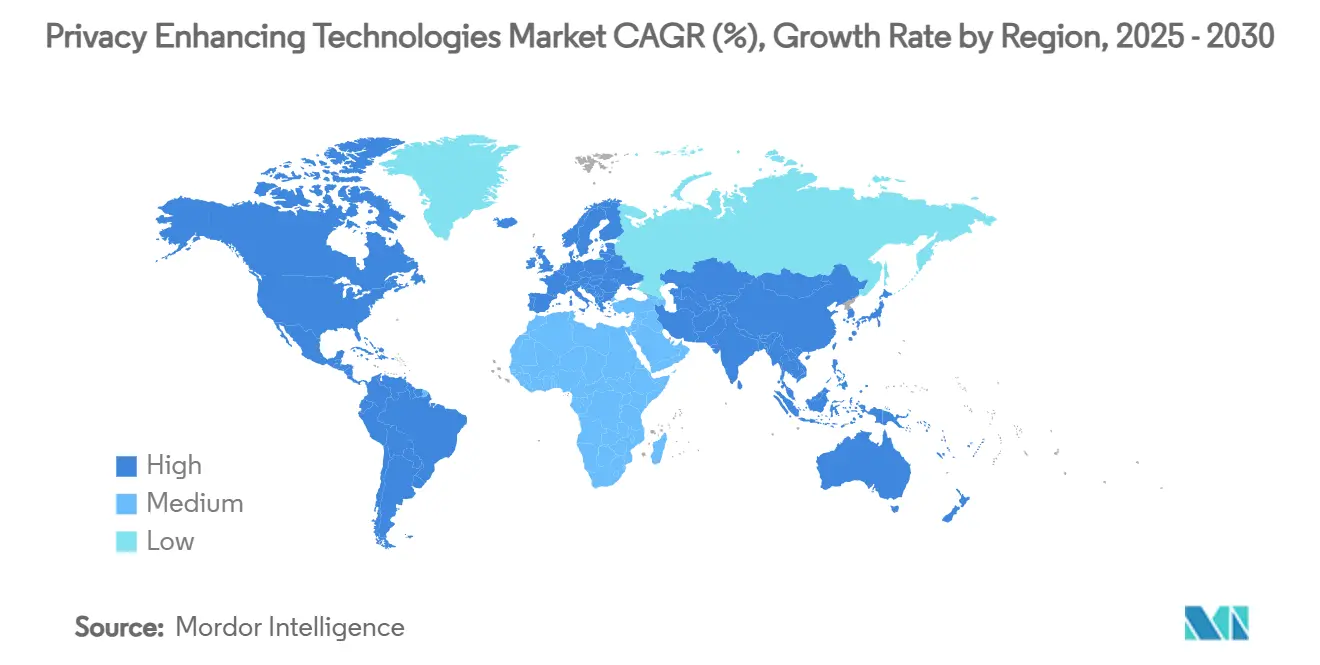

- By geography, North America captured 38.60% revenue share in 2024; South America is projected to grow at 27.90% CAGR to 2030.

Global Privacy Enhancing Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream PET adoption mandated by PCI-DSS 4.0 and FedRAMP-High certifications | +4.20% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Rapid efficiency gains in FHE and ZKP lowering TCO | +3.10% | Global, with early gains in North America, EU | Short term (≤ 2 years) |

| Explosion of AI/LLM privacy-by-design use-cases | +2.80% | Global | Short term (≤ 2 years) |

| Quantum-safe cryptography deadlines in critical infrastructure | +2.50% | North America and EU core, spill-over to APAC | Long term (≥ 4 years) |

| Rise of DeCC protocols (Aleo, Fhenix) in Web3 data markets | +1.90% | Global, concentrated in crypto-friendly jurisdictions | Medium term (2-4 years) |

| Sovereign data-space projects in EU (Gaia-X, Catena-X) standardising PET APIs | +1.70% | EU core, potential global standardization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream PET adoption mandated by PCI-DSS 4.0 and FedRAMP-High certifications

Card-present and cloud service standards now couple privacy to compliance. PCI-DSS 4.0 obliges quantum-ready algorithms by 2026, and FedRAMP-High assesses trusted execution environments for federal workloads. Non-compliance risks outweigh costs, pushing banks to budget USD 50–100 million each year on PET infrastructure.[2]International Business Machines Corporation, “2023 Annual Report,” ibm.com

Rapid efficiency gains in FHE and ZKP lowering TCO

Intel’s TDX Connect on Xeon 6 chips slashes encrypted-VM latency fivefold, and Zama’s Concrete library delivers tenfold speedups, making real-time analytics on 100 GB datasets practical. Recursive proof systems trim ZKP verification from minutes to milliseconds, so enterprises now justify broader deployments beyond high-value niche tasks.

Explosion of AI/LLM privacy-by-design use cases

Federated learning lets hospitals train models without sharing patient files, while confidential inference on Azure shields prompts with trusted execution environments. Swift and 12 banks use PET-based fraud detection that shares threat intelligence but hides transaction patterns. The EU AI Act amplifies uptake by linking transparency to liability.

Quantum-safe cryptography deadlines in critical infrastructure

NIST plans to retire quantum-vulnerable algorithms by 2030. IBM readiness audits show enterprises scoring 21 / 100 on preparedness, exposing the gap. Operators with 20-year equipment lifecycles must begin migration now or face “harvest-now-decrypt-later” risks that undermine long-term confidentiality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High computational overhead for FHE at petabyte scale | -2.30% | Global, particularly affecting hyperscale deployments | Short term (≤ 2 years) |

| Shortage of PET-skilled cryptographers and DevSecOps talent | -1.80% | Global, acute in North America and EU | Medium term (2-4 years) |

| Legal uncertainty around synthetic-data GDPR equivalence | -1.40% | EU core, with global implications for multinational operations | Long term (≥ 4 years) |

| Side-channel leak risks in TEEs and GPU-based MPC clusters | -1.20% | Global, particularly affecting cloud and edge deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High computational overhead for FHE at petabyte scale

Even with GPUs, homomorphic workloads need 10,000–100,000 × the compute of clear-text jobs, and H100 clusters demand costly cooling upgrades. Cloud FHE instances can exceed USD 1,000 per terabyte processed, dwarfing the USD 10–50 typical for conventional analytics.

Shortage of PET-skilled cryptographers and DevSecOps talent

Universities graduate fewer than 500 PhD cryptographers yearly, yet demand has surged tenfold in three years. Senior experts command USD 300,000-500,000 salaries, and reskilling programs take up to five years, delaying deployments despite budget availability.[3]Anna Kondrashova, “Differential Privacy Enforcement in BigQuery Data Clean Rooms,” Google Cloud, cloud.google.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Cryptographic Rigour Gains Traction

Homomorphic encryption yielded 31.20% of the 2024 Privacy-Enhancing Technologies market share. Enterprises prefer its mathematically proven ability to compute on ciphertext. The segment underpins USD 1.55 billion of the 2024 Privacy-Enhancing Technologies market size and is projected to grow in step with post-quantum standards. Zero-knowledge proofs record a 25.71% CAGR, reflecting surging Web3 identity and compliance use cases. Trusted execution environments accelerate because Intel and AMD ship silicon with built-in attestation, letting developers embed confidentiality at the hardware layer. Synthetic-data generators round out offerings by giving AI teams privacy-safe corpora for model training. Vendors differentiate on performance, developer tooling, and regulatory certification.

The technology mix signals a move away from privacy through obscurity toward verifiable cryptographic guarantees. Microsoft’s expansion of Azure confidential computing makes TEEs a routine feature in cloud provisioning, while VCs back niche players that specialize in FHE optimizations. NIST’s upcoming post-quantum algorithm suite drives all vendors to adopt lattice-based primitives, ensuring future-proof roadmaps.

By Application: AI Leads, Web3 Accelerates

AI/ML training contributed 26.40% of 2024 revenue as federated learning lets firms share gradient updates, not raw data. The need to protect sensitive prompts fuels confidential inference services that hide inputs within hardware-isolated enclaves. Blockchain and Web3 show the sharpest trajectory at 26.82% CAGR, where zero-knowledge rollups enable private yet auditable transactions. Data analytics remains steady because encrypted queries now meet latency targets. Fraud management solutions employ secure multi-party computation to share threat signals across banks without exposing proprietary rulesets. Cloud and SaaS vendors embed differential privacy in usage telemetry to comply with global data residency laws.

By Deployment Model: Cloud Dominance Meets Edge Push

Cloud offerings held 58.00% of 2024 spending thanks to managed services that hide cryptographic complexity. The model accounts for USD 2.88 billion of the 2024 Privacy-Enhancing Technologies market size. Hyperscale’s combine key management, TEEs, and FHE libraries in turnkey stacks. Edge and IoT nodes grow at 24.55% CAGR as factories, hospitals, and vehicles require on-device privacy with millisecond latency. Intel-backed projects show fivefold throughput gains for edge MPC engines, making local analytics feasible. On-premises appliances persist in defense and critical infrastructure where air-gapped operation is mandated.

By End-User Industry: BFSI Sets the Pace

BFSI controlled 27.90% of 2024 spending due to mandated PCI-DSS 4.0 upgrades and CBDC pilots. Financial institutions budget for quantum-safe roadmaps years ahead of the deadline. Retail and eCommerce grow fastest at 26.22% CAGR as loyalty platforms adopt differential privacy and secure enclaves to respect consumer consent. Healthcare lifts synthetic-data tools for research without breaching HIPAA. Governments fund multi-agency data spaces that rely on MPC to aggregate intelligence. Telecom operators embed confidential computing in 5G edge clouds, selling privacy-assured slices to enterprise customers.

Geography Analysis

Routine Refresh Cycles of HSMs and TLS Stacks

North America generated 38.60% of 2024 revenue, equal to USD 1.92 billion of the Privacy-Enhancing Technologies market size, benefiting from FedRAMP-High rules and venture funding rounds such as Zama’s USD 130 million raises. Banks, cloud providers, and federal agencies co-invest in confidential computing labs that seed a specialized talent pool. Canada uses PET analytics for anti-money-laundering across borders, and Mexico’s fintech harness ZKPs for remittance privacy.

South America leads growth at 27.90% CAGR, driven by Brazil’s DREX CBDC that encodes privacy in core monetary rails. Argentine fintech use zero-knowledge architectures to skirt capital-control disclosure while staying compliant. The Inter-American Development Bank backs PET pilot programs in Colombia and Chile for digital-government services.

Europe aligns PET adoption with GDPR enforcement and sovereign data initiatives. Germany’s automotive OEMs employ MPC for supply-chain optimisation without sharing trade secrets, and France’s health data hub applies differential privacy to population research. The UK positions PETs as a post-Brexit advantage for fintech exports. These moves keep Europe among the top three spenders despite mid-teens CAGR.

Asia-Pacific shows uneven maturity. Japan embeds PETs in Society 5.0 smart-city projects, Singapore mandates confidential computing for cross-border banking data, and Australia funds quantum-safe migrations in critical infrastructure. China pursues domestic PET stacks to meet data-localisation law, although export controls limit visibility.

The Middle East and Africa start from a lower base but record double-digit growth. Israel’s cryptography talent drives start-up exports, while Gulf states pilot privacy-preserving digital identity schemes for public services.[4]Magda Gianola and Anurag Peshne, “Differential Privacy Enforcement in BigQuery Data Clean Rooms,” Google Cloud, cloud.google.com

Competitive Landscape

The Privacy-Enhancing Technologies market features moderate fragmentation. Hyperscale’s-IBM, Google, Microsoft, AWS-embed PETs in mainstream cloud, leveraging existing compliance certificates to win workloads. IBM couples z16 mainframes with lattice-based algorithms to address banking latency needs. Google standardizes differential privacy across ads and analytics, proof-pointing commercial viability. Microsoft extends Azure confidential computing with FIPS 140-3 HSMs that attract government buyers.

Specialists fill protocol gaps: Zama optimises FHE for sub-second inference, Duality offers MPC toolkits for joint analytics, Enveil focuses on encrypted search for sensitive intelligence queries. Hardware alliances shape the road map. Intel pairs Xeon 6 and Gaudi 2 accelerators with TDX Connect, while NVIDIA collaborates on verifiable compute attestations. Start-ups link to these ecosystems for go-to-market reach rather than stand-alone offerings.

M and A activity centres on capability aggregation. Cloud vendors acquire niche FHE and ZKP teams to integrate cryptography into DevOps-friendly SDKs. Competition will intensify as post-quantum deadlines near, and buyers favour vendors with certified quantum-safe stacks.

Privacy Enhancing Technologies Industry Leaders

International Business Machines Corporation

Google LLC

Microsoft Corporation

Amazon Web Services, Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Intel announced TDX Connect support on Xeon 6 processors for encrypted CPU-to-GPU communications.

- January 2025: EQTY Lab launched its Verifiable Compute AI framework with Intel and NVIDIA to ease AI Act compliance.

- December 2024: Google Cloud and Swift began a federated anti-fraud network with 12 global banks under confidential computing.

- December 2024: Microsoft integrated Marvell FIPS 140-3 Level-3 HSMs into Azure Key Vault to harden quantum-safe key storage.

Global Privacy Enhancing Technologies Market Report Scope

| Homomorphic Encryption (FHE/PHE/SHE) |

| Differential Privacy |

| Secure Multi-Party Computation (MPC) |

| Trusted Execution Environments (TEE) |

| Synthetic Data Generation |

| Zero-Knowledge Proofs (ZKP) |

| AI / Machine Learning Model Training |

| Data Analytics and BI |

| Fraud and Risk Management |

| Cloud and SaaS Security |

| Blockchain and Web3 |

| Cloud-based PET Services |

| On-premise / Appliance |

| Edge / IoT Nodes |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Government and Defense |

| IT and Telecom |

| Retail and eCommerce |

| Others (Energy, Manufacturing) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Homomorphic Encryption (FHE/PHE/SHE) | |

| Differential Privacy | ||

| Secure Multi-Party Computation (MPC) | ||

| Trusted Execution Environments (TEE) | ||

| Synthetic Data Generation | ||

| Zero-Knowledge Proofs (ZKP) | ||

| By Application | AI / Machine Learning Model Training | |

| Data Analytics and BI | ||

| Fraud and Risk Management | ||

| Cloud and SaaS Security | ||

| Blockchain and Web3 | ||

| By Deployment Model | Cloud-based PET Services | |

| On-premise / Appliance | ||

| Edge / IoT Nodes | ||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | ||

| Government and Defense | ||

| IT and Telecom | ||

| Retail and eCommerce | ||

| Others (Energy, Manufacturing) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the post-quantum cryptography market by 2030?

The post-quantum cryptography market size is set to reach USD 4.60 billion by 2030, growing at a 39.27% CAGR.

Which algorithm family holds the largest revenue share?

Lattice-based schemes, led by Kyber and Dilithium, commanded 52% of 2024 revenue.

Which deployment mode is expanding fastest?

Cloud-hosted implementations are advancing at a 44.85% CAGR as hyperscalers embed quantum-safe services.

Why are government mandates influential in adoption?

Statutory deadlines require agencies and contractors to migrate by 2026, guaranteeing early-stage demand and shaping vendor roadmaps.

Page last updated on: