Sea Salt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.54 Billion |

| Market Size (2031) | USD 24.77 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

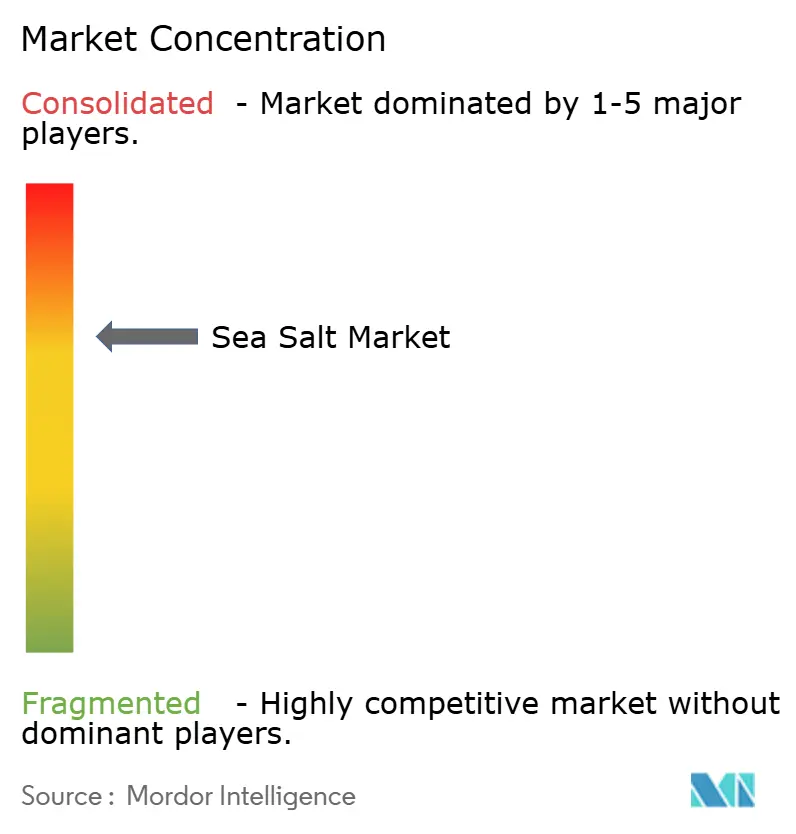

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sea Salt Market Analysis by Mordor Intelligence

The sea salt market was valued at USD 19.86 billion in 2025 and is projected to reach USD 24.77 billion by 2031 from USD 20.54 billion in 2026, growing at a CAGR of 3.82% from 2026 to 2031. The market is at a critical juncture, with demand for commodity-grade products and the trend toward artisanal premiumization moving in opposite directions. While volume growth remains moderate, premium products are generating significantly higher revenue per tonne. Growth in 2026 is expected to be driven by consistent demand from the food and beverage processing sector, alongside increasing adoption in personal care formulations and premium foodservice channels. The shift away from refined table salt, influenced by clean-label sourcing preferences in packaged foods, has broadened the market for sea salt beyond traditional culinary applications. Industrial buyers are increasingly incorporating sea-origin salt in product reformulations, further expanding its market potential.

Key Report Takeaways

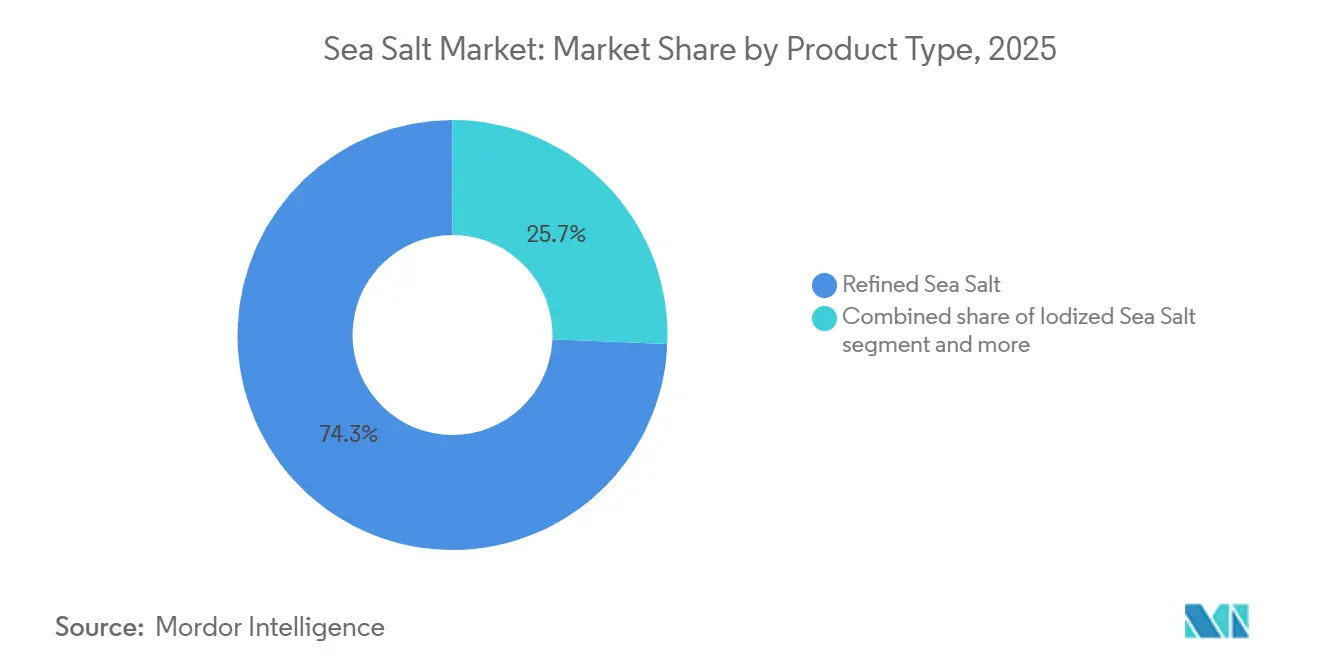

- By product type, refined sea salt held 74.34% of 2025 revenue, while iodized sea salt will post a 4.89% CAGR through 2031.

- By nature, conventional led with 92.19% in 2025; organic recorded the fastest 5.33% CAGR to 2031.

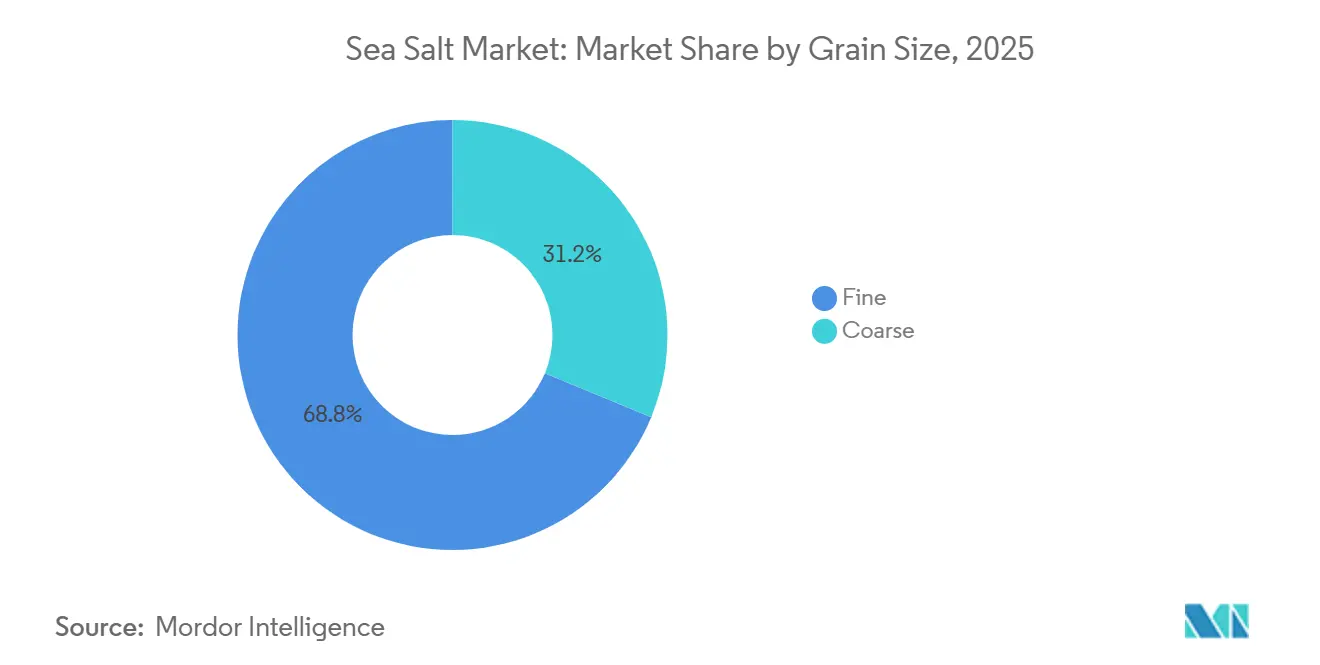

- By grain size, fine generated 68.76% of 2025 demand, whereas the coarse segment is forecast to accelerate at a 5.07% CAGR through 2031.

- By end use, industrial captured a 70.11% share in 2025, while the foodservice/HoReCa segment is forecast to register a 4.96% CAGR over 2026-2031.

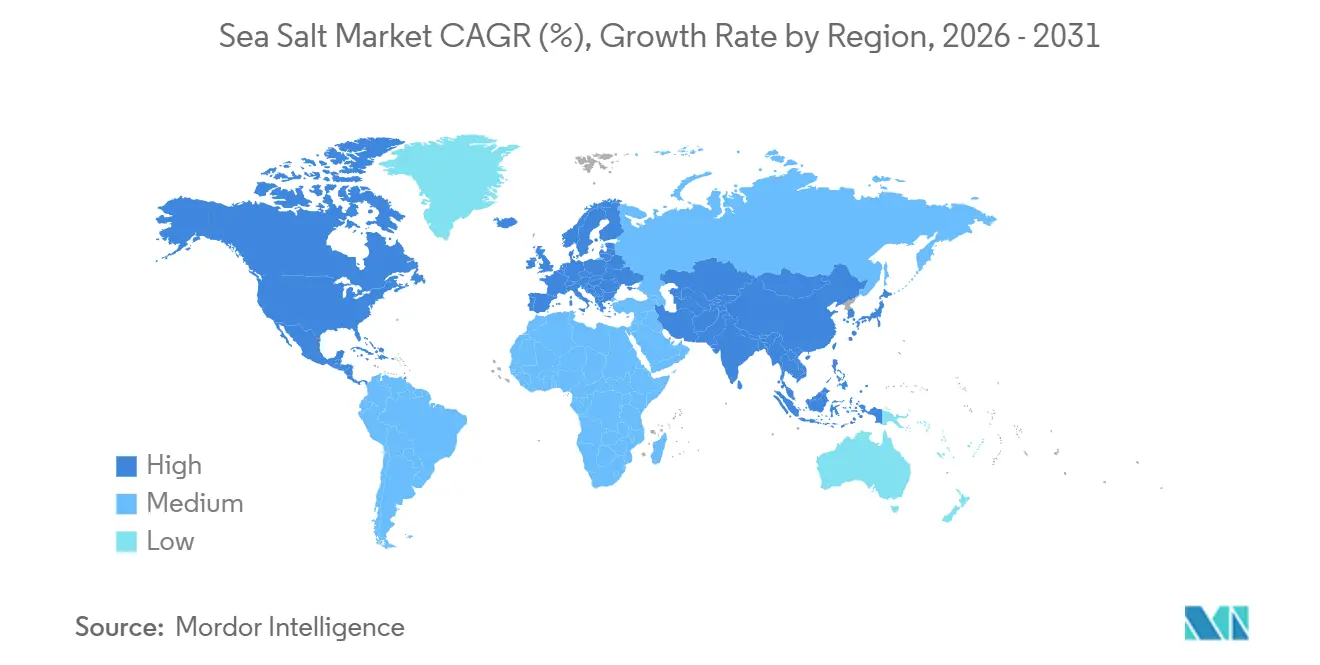

- By geography, North America commanded 34.02% of 2025 sales, while Asia-Pacific will expand at a 5.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sea Salt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean label and minimally processed ingredients | +0.9% | Global, with concentration in North America and Western Europe | Long term (≥ 4 years) |

| Expansion of premium and gourmet food consumption | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Growing consumption of processed food | +0.7% | Asia-Pacific, Middle East and Africa, South America | Medium term (2–4 years) |

| Rising utilization in personal care and cosmetic products | +0.6% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Strong demand from foodservice and fine-dining establishments | +0.7% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Growing demand for organic and natural food ingredients | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label and minimally processed ingredients

The growing consumer preference for clean-label, minimally processed food ingredients is a significant driver of the sea salt market. As consumers pay closer attention to ingredient labels and prioritize products perceived as authentic, simple, and less processed, sea salt has emerged as a popular alternative to conventional refined salt. Its natural harvesting process, minimal processing, and association with trace mineral content align with the growing demand for clean-label and wellness-focused food products. This trend has prompted food manufacturers to incorporate sea salt into reformulated products, including snacks, bakery items, ready meals, seasonings, and processed foods, to enhance ingredient transparency and reinforce a natural product image. Shifting consumer eating habits further support this trend. According to IFIC, by 2025, 19% of consumers identified with mindful eating practices, while 13% adopted clean eating approaches, highlighting a growing preference for food perceived as natural, minimally processed, and easy to understand [1]Source: International Food Information Council (IFIC), "2025 IFIC Food & Health Survey", ific.org. Consequently, manufacturers are focusing on recognizable ingredients that appeal to health-conscious consumers, fostering increased adoption of sea salt across both retail and industrial applications.

Expansion of premium and gourmet food consumption

The increasing consumption of premium and gourmet foods is significantly driving the growth of the sea salt market. As consumers seek enhanced culinary experiences, there is a rising demand for high-quality ingredients that improve flavor, texture, and product differentiation. Sea salt is widely valued in premium food applications for its unique taste profile, natural origin, and artisanal characteristics, making it a preferred choice among gourmet food producers, specialty retailers, and foodservice operators. Its applications span a variety of products, including gourmet snacks, bakery items, specialty seasonings, premium dairy products, and restaurant offerings. The rising influence of culinary trends, food tourism, chef-driven dining concepts, and home gourmet cooking is further boosting the demand for premium sea salt products. As consumers continue to prioritize taste, quality, and ingredient authenticity, sea salt is expected to maintain its strong position within the premium and gourmet food segment, supporting sustained market growth over the long term.

Growing consumption of processed food

The increasing consumption of processed foods is a significant driver of the sea salt market. Sea salt is extensively used in packaged foods, snacks, bakery products, sauces, ready meals, dairy products, and meat processing applications. Food manufacturers utilize sea salt not only for flavor enhancement but also for its preservative properties, texture modification, and clean-label appeal. As consumer demand for convenient, ready-to-eat, and shelf-stable food products grows, the need for high-quality salt ingredients has risen, driving the adoption of sea salt in industrial food processing. This trend is evident on a global scale of processed food consumption. For example, a 2025 study by the National Heart, Lung, and Blood Institute (NHLBI), titled "Spotlight on UPFs: NIH explores link between ultra-processed foods and heart disease," revealed that up to 70% of the U.S. diet consists of ultra-processed foods, underscoring the prominent role of processed food in modern diets [2]Source: National Heart, Lung, and Blood Institute, "Spotlight on UPFs: NIH explores link between ultra-processed foods and heart disease", nhlbi.nih.gov. To meet consumer expectations for ingredient transparency and clean-label products, manufacturers are increasingly incorporating sea salt into reformulated products as a natural alternative to conventional salt ingredients.

Growing demand for organic and natural food ingredients

The growing demand for organic and natural food ingredients is a key factor driving the sea salt market. Consumers are increasingly focused on ingredient sourcing, production processes, and product transparency, leading to a stronger preference for food products made with natural and minimally processed ingredients. Sea salt aligns well with this trend due to its natural origin, straightforward processing, and compatibility with clean-label and organic food standards. As food manufacturers expand their offerings of natural, organic, and premium products, the use of sea salt has become a practical approach to enhance ingredient authenticity and meet changing consumer expectations. This shift is particularly pronounced among younger demographics, such as Gen Z and Millennials. These consumers are increasingly willing to pay 20–30% more for products labeled as organic, natural, high-protein, or free from artificial ingredients [3]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. Consequently, food and beverage manufacturers are reformulating products to include ingredients that support these claims and reinforce premium positioning. Sea salt's natural image and suitability for organic and clean-label formulations make it a preferred choice across categories such as snacks, bakery products, seasonings, sauces, and prepared foods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sodium-reduction policies limiting volume growth in packaged food | -0.5% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Substitution pressure from Himalayan pink salt and kosher salt | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Limited functional differentiation in many applications | -0.3% | Global, primarily industrial end-use | Long term (≥ 4 years) |

| Fragmented market with intense competition | -0.3% | Global, particularly Asia-Pacific and South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Sodium-reduction policies limiting volume growth in packaged food

Sodium-reduction policies and public health initiatives aimed at decreasing dietary salt intake are emerging as significant constraints on the sea salt market, particularly in packaged food applications. Governments, health organizations, and regulatory bodies in various countries are increasingly urging food manufacturers to lower sodium levels in processed foods to address growing concerns about hypertension, cardiovascular disease, and other health-related issues. Since sea salt and conventional salt have similar sodium content by weight, these initiatives can reduce overall salt usage volumes regardless of the source, posing challenges for long-term volume growth in the market. Additionally, rising consumer awareness about sodium consumption is prompting some individuals to limit their overall salt intake, influencing purchasing patterns across packaged food categories. While premium, organic, and specialty sea salt segments benefit from clean-label and gourmet food trends, broader sodium-reduction strategies within the food industry may slow the rate of volume growth for the sea salt market, particularly in mature food processing sectors where reformulation efforts are more advanced.

Substitution pressure from Himalayan pink salt and kosher salt

The sea salt market is experiencing increasing substitution pressure from alternative specialty salts, such as Himalayan pink salt and kosher salt, which target similar consumer groups seeking premium, natural, and minimally processed seasoning options. Himalayan pink salt is promoted for its unique color, mineral content, and premium positioning, while kosher salt is favored by chefs and foodservice operators for its texture, ease of use, and versatility in cooking. The growing availability and visibility of these alternatives in retail and foodservice channels may restrict the growth of sea salt demand in specific applications. This challenge is particularly pronounced in premium retail and gourmet food segments, where consumers frequently switch between specialty salts based on flavor preferences, culinary trends, and marketing claims. Although sea salt benefits from its strong clean-label and natural ingredient appeal, the presence of well-established substitutes can limit market share growth and constrain opportunities, particularly in higher-margin specialty salt categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refined Sea Salt Anchors Industrial Volume, Iodized Variants Accelerate

Refined sea salt accounted for 74.34% of the total sea salt market revenue in 2025, underscoring its widespread use in food manufacturing, chemical processing, and water treatment applications. These industries prioritize consistent purity and particle size over mineral complexity. The dominance of refined sea salt is attributed to procurement scale, as industrial buyers in the food and beverages sub-sector typically source it in multi-thousand-tonne contracts. This level of demand exceeds the capacity of smaller specialty producers, effectively concentrating the majority of market value among large-scale, vertically integrated operators.

Iodized sea salt is projected to be the fastest-growing product type from 2026 to 2031, with a CAGR of 4.89%. This growth is driven by mandatory iodization policies in countries such as India, China, Indonesia, and the Philippines. These governments enforce universal salt iodization as a public health initiative to combat iodine deficiency disorders. In South and Southeast Asia, government-mandated iodization programs create a stable demand for iodized sea salt, independent of consumer preference trends. For instance, India's Food Safety and Standards Authority (FSSAI) and China's national iodine standards mandate the iodization of all edible salt at the processing level, ensuring consistent institutional procurement volumes.

By Nature: Conventional Concentration Masks Organic Growth Premium

Conventional sea salt accounted for 92.19% of total market revenue in 2025, highlighting the market's reliance on large-scale industrial supply chains where organic certification adds costs without yielding a proportional procurement premium. This dominance reflects the widespread use of conventional sea salt in various industries, including food processing, cosmetics, and de-icing, where cost efficiency and availability are prioritized over organic certification. The organic sub-segment, projected to grow at a CAGR of 5.33% from 2026 to 2031, is expanding faster than any other nature segment and outpacing the overall market growth rate of 3.82%. This growth is driven by increasing demand from health-conscious retail buyers, specialty food manufacturers, and direct-to-consumer brands seeking certified organic supply to meet evolving consumer preferences for natural and sustainably sourced products.

Organic sea salt commands significantly higher retail prices, as premium retail and specialty food manufacturers increasingly require certified-organic supply chains with traceability documentation from harvest to packaging. This premium pricing is supported by the growing consumer perception of organic products as healthier and more environmentally friendly. France and Japan demonstrate the strongest preference for organic sea salt. In France, artisanal producers in Guérande and Brittany maintain certified-organic production practices that meet the procurement standards of domestic specialty retailers and export-focused gourmet food brands. These regions are renowned for their traditional harvesting methods, which align with the sustainability and quality expectations of organic certification, further enhancing their appeal in both domestic and international markets.

By Grain Size: Fine Dominates Processing, Coarse Gains on Culinary Premiumisation

Fine sea salt accounted for 68.76% of the total market revenue in 2025, primarily due to its compatibility with automated dosing systems in food processing, its rapid dissolution in brine and cooking applications, and its suitability for pharmaceutical-grade and cosmetic formulations requiring consistent particle distribution. In food manufacturing, grain size is typically dictated by production line design, with fine grades often specified. Additionally, high switching costs in existing manufacturing setups limit the adoption of grain size changes.

Coarse sea salt, projected to grow at a rate of 5.07% from 2026 to 2031, is gaining market share as its use expands in foodservice, retail packaging, and personal care applications, where the visual grain structure adds to the product's value. Artisanal producers are increasingly positioning coarse sea salt as a sensory ingredient. Textured flakes and pyramid crystals from brands such as Maldon and Jacobsen Salt Co. compete directly with fine-ground alternatives by offering a tactile finish that fine variants cannot replicate.

By End-Use: Industrial Sub-segments Broaden, Foodservice Segment Leads Growth Rate

In 2025, industrial end-use accounted for 70.11% of the total sea salt market revenue, with the food and beverages segment contributing the largest share. This was followed by personal care and cosmetics, and pharmaceuticals as significant sub-applications. Food and beverage manufacturers use sea salt as a key ingredient in baking, dairy, snack production, and cured meat applications. The preference for sea salt is driven by its clean-label attributes, which increasingly justify the higher costs compared to commodity rock salt alternatives.

From 2026 to 2031, the foodservice/HoReCa segment is projected to experience the fastest end-use growth, with a CAGR of 4.96%. This growth is attributed to restaurants progressively shifting from bulk commodity salt to origin-specific finishing varieties. This trend is further supported by the rise of culinary tourism and chef-led social media content highlighting salt as a prominent ingredient. Additionally, the personal care and cosmetics segment is expected to be the fastest-growing industrial sub-segment. Research on marine bioactives has validated sea salt's role in skin exfoliation, hydration, and mineral supplementation, driving demand from cosmetic manufacturers seeking scientifically supported ingredient claims.

Geography Analysis

In 2025, North America accounted for the largest share of the sea salt market, representing 34.02% of total revenue. This dominance is attributed to the widespread use of sea salt in food processing, foodservice, and retail applications, alongside strong consumer preference for natural and clean-label ingredients. Food manufacturers are increasingly incorporating sea salt in reformulation efforts to meet consumer demand for recognizable ingredients while maintaining product taste and functionality. Additionally, the well-established packaged food industry and the growing popularity of gourmet and specialty salts continue to drive market demand in the United States and Canada.

The Asia-Pacific region is projected to be the fastest-growing sea salt market during the forecast period from 2026 to 2031, with a CAGR of 5.38%. This growth is fueled by rising consumption of processed and convenience foods, expanding food manufacturing activities, and increasing consumer awareness of premium and natural food ingredients. Countries such as China, India, Japan, and South Korea are experiencing heightened demand for sea salt across industrial and retail channels. Furthermore, rapid urbanization, evolving dietary preferences, and the expansion of modern retail and e-commerce platforms are expected to further accelerate market growth in the region.

Europe remains a significant market for sea salt, supported by a strong tradition of specialty and gourmet salt consumption and increasing demand for organic and sustainably sourced food ingredients. South America and the Middle East and Africa are witnessing gradual market expansion, driven by increasing food processing activities, rising consumer interest in natural seasonings, and improving retail distribution networks. As awareness of clean-label products and premium food ingredients grows, these regions are expected to contribute steadily to the overall growth of the sea salt market during the forecast period.

Competitive Landscape

The sea salt market is moderately consolidated, with numerous regional salt producers, specialty sea salt brands, and large-scale industrial suppliers competing across food processing, retail, and foodservice channels. Global players benefit from established sourcing networks, production scale, and distribution capabilities, while regional producers often focus on origin-specific branding, artisanal harvesting methods, and premium product positioning. Competition primarily revolves around product quality, mineral composition, pricing, supply reliability, and sustainability credentials, rather than technological differentiation.

Market participants are increasingly emphasizing value-added product development to enhance their competitive positioning. Innovations such as lower-sodium sea salt solutions, organic-certified products, flavored variants, and gourmet-grade offerings are helping companies cater to evolving consumer preferences for clean-label, natural, and premium ingredients. Strategic investments in production capacity expansion, sustainable harvesting practices, and partnerships with food manufacturers have become critical priorities as demand from industrial food processing applications continues to grow. Additionally, companies are leveraging transparency in sourcing and environmental stewardship to strengthen brand differentiation in both retail and B2B markets.

White-space opportunities are concentrated at the intersection of sea salt and emerging functional applications. Segments such as electrolyte hydration products, mineral-enriched beverages, mineral-fortified cosmetics, personal care formulations, and pharmaceutical-grade saline solutions remain relatively underpenetrated compared to their long-term demand potential. As manufacturers seek multifunctional ingredients that combine performance with natural positioning, sea salt suppliers have opportunities to expand beyond traditional seasoning applications into higher-value wellness, health, and specialty industrial categories. These emerging use cases are expected to become increasingly important competitive growth avenues over the coming years.

Sea Salt Industry Leaders

-

Cargill, Incorporated

-

Morton Salt, Inc

-

Compass Minerals International, Inc.

-

SaltWorks, Inc.

-

Maldon Crystal Salt Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: True Salt expanded its premium sea salt as a preferred ingredient for food manufacturers focused on clean-label and sodium-reduction objectives. The company emphasized that food producers are under increasing pressure from regulators and consumers to reduce the use of artificial additives and simplify ingredient lists, while maintaining taste, texture, and product performance.

- November 2025: True Salt announced a significant expansion of its production operations in Baja California, Mexico, to meet the growing demand for premium sea salt across the food manufacturing, foodservice, and consumer markets. The expansion increases the company's production capacity by over 40%, enhancing its ability to provide a scalable, reliable, and sustainable supply of sea salt to customers throughout North America.

- November 2024: Cornish Sea Salt expanded its food manufacturing portfolio with the introduction of TekSalt, a lower-sodium sea salt solution designed to help food manufacturers reduce sodium without compromising flavor. TekSalt is a mineral-balanced sea salt enriched with naturally occurring minerals and electrolytes, including calcium, potassium, and magnesium. This formulation delivers strong taste intensity while containing less sodium than conventional salt alternatives.

Global Sea Salt Market Report Scope

| Refined Sea Salt |

| Unrefined Sea Salt |

| Iodized Sea Salt |

| Others |

| Conventional |

| Organic |

| Fine |

| Coarse |

| Industrial | Food and Beverages |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Others | |

| Foodservice/HoReCa | |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Refined Sea Salt | |

| Unrefined Sea Salt | ||

| Iodized Sea Salt | ||

| Others | ||

| By Nature | Conventional | |

| Organic | ||

| By Grain Size | Fine | |

| Coarse | ||

| By End-Use | Industrial | Food and Beverages |

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| Others | ||

| Foodservice/HoReCa | ||

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the sea salt market?

The sea salt market was valued at USD 19.86 billion in 2025 and is projected to reach USD 24.77 billion by 2031.

Which product type holds the largest share of the sea salt market?

Refined sea salt led the market in 2025, accounting for 74.34% of total revenue.

Which end-use segment dominates the sea salt market?

The industrial segment held the largest share in 2025, representing 70.11% of the market.

Which region is expected to grow the fastest in the sea salt market?

Asia-Pacific is projected to be the fastest-growing regional market, registering a 5.38% CAGR during 2026–2031.

Page last updated on: