Gourmet Salt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

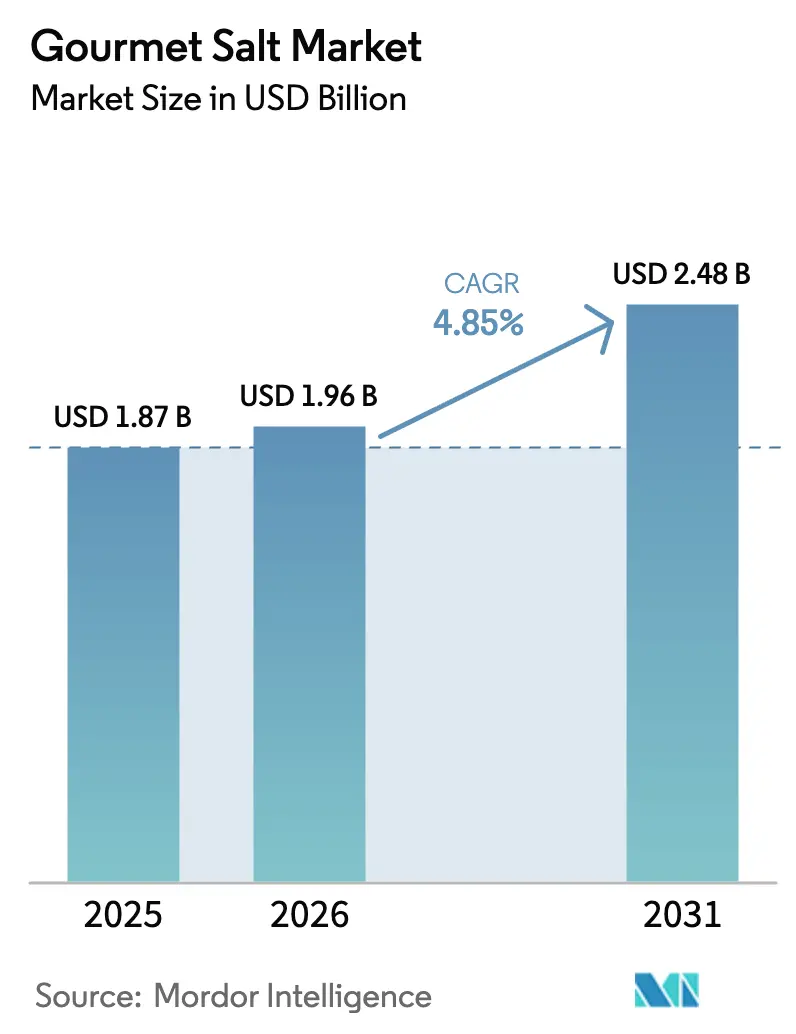

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

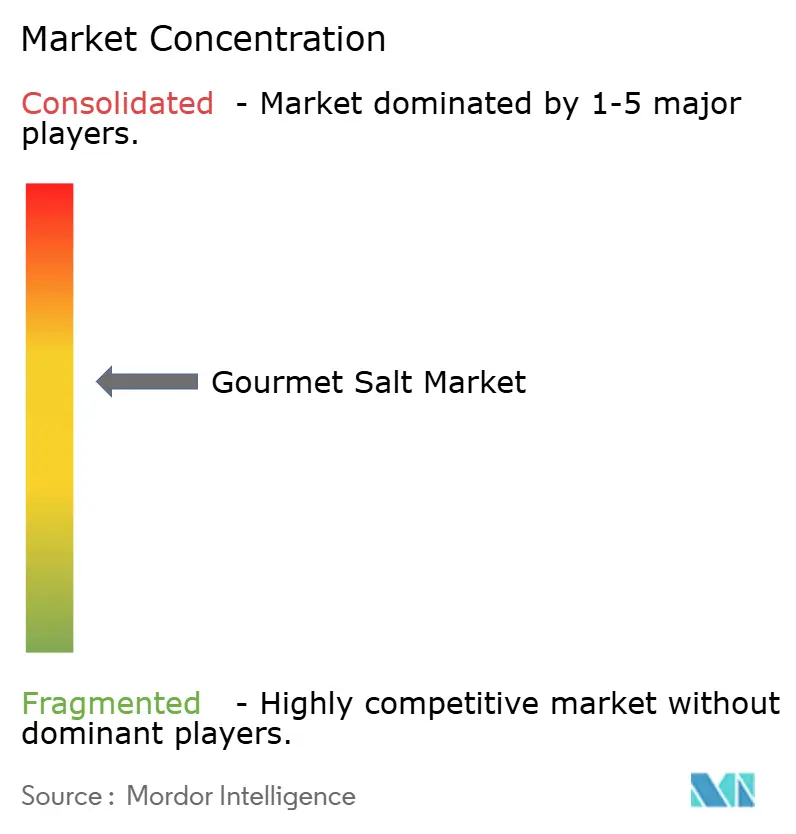

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gourmet Salt Market Analysis by Mordor Intelligence

The Gourmet Salt Market size is expected to grow from USD 1.87 billion in 2025 to USD 1.96 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 4.85% CAGR over 2026-2031. The growing trend of premiumization has significantly increased the price gap between regular table salt and artisanal, mineral-rich options, which now sell at 200% to 400% higher prices. Leading companies like Morton Salt and Cargill are making substantial investments, reflecting their confidence in the market's continued growth. This growth is driven by home cooks adopting professional cooking techniques and food manufacturers updating recipes to meet clean-label requirements. Retailers are dedicating more shelf space to flavored and smoked salt varieties, while e-commerce platforms enable small producers to reach global customers without relying on distributors. At the same time, efforts to reduce sodium intake are encouraging innovations such as salts with added trace minerals, potassium-based blends, and portion-controlled options that maintain flavor while reducing consumption. The moderate competition in the market supports both consolidation and the use of storytelling by artisanal brands, helping them maintain higher profit margins compared to standard salt products.

Key Report Takeaways

- By type, fleur de sel led with 33.88% of the gourmet salt market share in 2025. Specialty salt is forecast to advance at a 6.21% CAGR through 2031, the fastest among product categories.

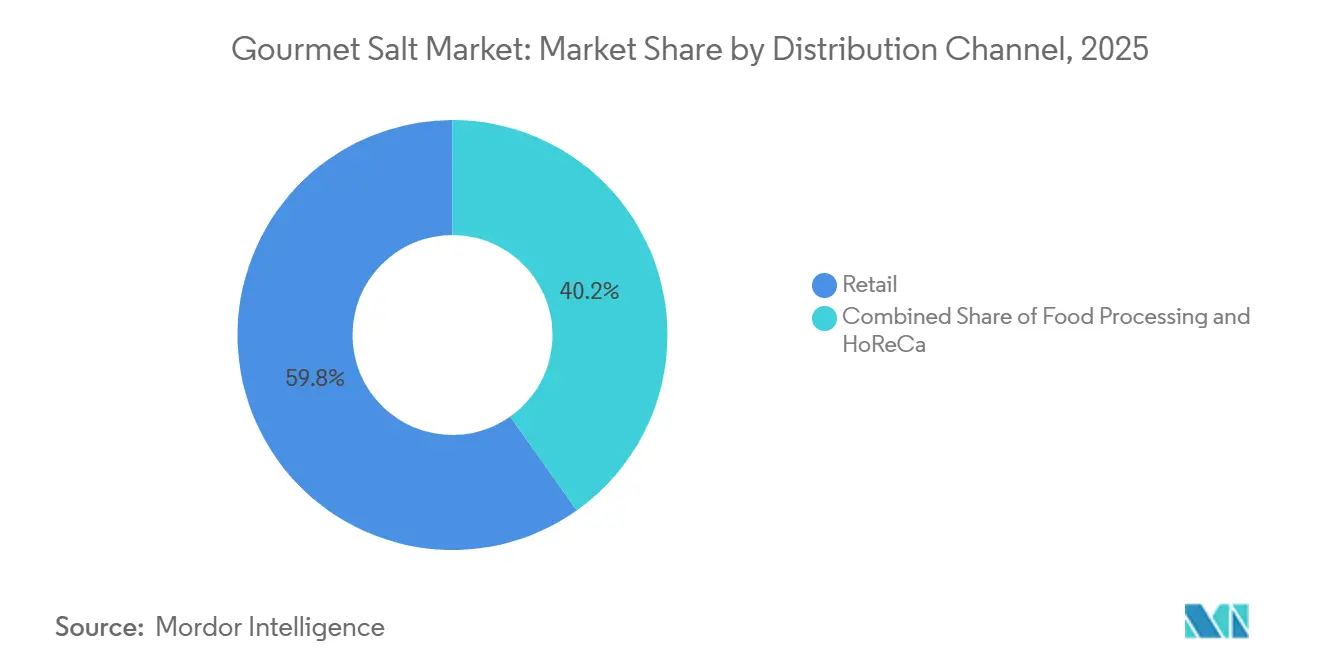

- By distribution channel, retail held 59.81% revenue share in 2025, while food processing is projected to expand at a 5.01% CAGR to 2031.

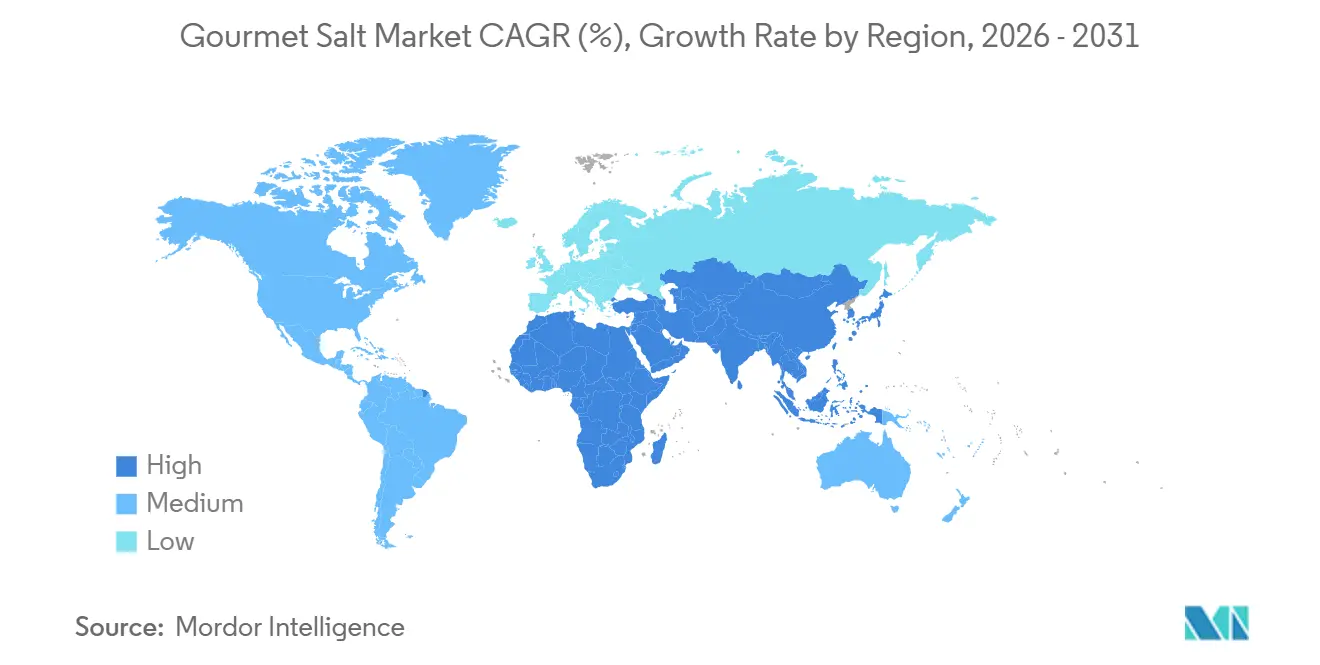

- By geography, North America accounted for 37.23% of revenue in 2025, and Asia-Pacific is predicted to grow at a 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gourmet Salt Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gourmet salt gains traction in food processing | +1.2% | North America, Europe | Medium term (2-4 years) |

| Health-conscious consumers prefer mineral-rich salts | +1.0% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Demand for natural and organic salts reflects wellness trends | +0.9% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| E-commerce and specialty retailers boost accessibility | +0.8% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Interest in international cuisines and fine dining grows | +0.7% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Influence of celebrity chefs, cooking shows, and social media | +0.6% | North America, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gourmet Salt Gains Traction in Food Processing

Food processors are shifting from commodity refined salt to gourmet varieties to meet clean-label requirements and differentiate their premium product lines. In April 2025, Cargill announced a USD 68 million investment to expand its St. Clair, Michigan facility, the only producer of Alberger salt in the world, by 40%. This expansion highlights the growing demand from snack, bakery, and prepared-meal manufacturers who prefer flake salt for its better surface adherence and enhanced flavor delivery. Similarly, in March 2025, Michigan Potash launched a food-grade salt business at its Evart plant, aiming to produce 1 million tons of high-purity salt annually. This initiative seeks to reduce the U.S.'s dependence on imports, which currently account for 25% of domestic salt consumption, primarily from Canada and Chile. The demand for gourmet salt is rising as buyers prioritize traceability and mineral content over cost. SaltWorks has also invested over USD 2 million in its Perfect Smoke Technology, a cold-smoking process using hand-selected wood varieties. This innovation allows co-packers to easily add smoked salts to sauces, seasonings, and ready-to-eat meals without extra processing. With the combined pressures of reformulation and premiumization, the adoption of gourmet salt in food processing is expected to grow steadily through 2031.

Health-Conscious Consumers Prefer Mineral-Rich Salts

Health-conscious consumers are increasingly opting for salts marketed as containing trace minerals like magnesium, potassium, and calcium, even though there is limited clinical evidence of significant health benefits at typical consumption levels. Himalayan pink salt, sourced from Pakistan's Khewra Mine, has gained popularity in health-food stores. Exports to China rose by 40% year-over-year, reaching USD 1.83 million in the first quarter of 2025. In December 2025, a TikTok trend featuring Celtic sea salt, promoted by influencer Abby Baffoe, claimed benefits such as improved sleep and clearer skin. This trend led to a surge in online searches and retail shortages, although nutrition experts have noted that the claim of 82 minerals lacks strong clinical evidence. According to the Centers for Disease Control and Prevention, most Americans consume more sodium than recommended. Despite this, the belief that "natural" salts are healthier continues to drive demand for premium products. This perception enables brands to incorporate wellness-focused messaging into basic mineral products, creating a significant growth opportunity.

Demand for Natural and Organic Salts Reflects Wellness Trends

Consumers are moving away from salts with additives like anti-caking agents and iodine fortification. Instead, they prefer unrefined salts made using traditional methods such as solar evaporation or hand-skimming. Fleur de sel from France's Guérande region is a notable example of this trend. It holds a Protected Geographical Indication (PGI) designation[1].Source: UK Government. "Protected Food Name: Guérande Salt.", gov.uk The Le Guérandais cooperative, employing over 300 salt workers, hand-harvests these crystals using wooden "lousse" tools. After harvesting, the crystals are drained for 2 to 3 years before being sold. This detailed and labor-intensive process results in retail prices exceeding USD 12.99 for just 4.4 ounces. In 2024, the United States Geological Survey reported that vacuum pan salt, known for its high purity, was priced at an average of USD 220 per ton, while solar salt was priced at USD 150 per ton. Both prices are significantly higher than the USD 45 per ton baseline for rock salt, which is mainly used for de-icing. Although salt cannot receive organic certification because it is a mineral and not an agricultural product, brands use terms like "natural," "unrefined," and "artisan" to appeal to health-conscious consumers. This trend is growing as mainstream retailers expand their organic and clean-label product ranges, giving gourmet salts more shelf space and increasing consumer awareness.

E-Commerce and Specialty Retailers Boost Accessibility

Digital channels have eliminated geographic barriers, allowing small-batch producers to reach global audiences without depending on traditional distributors directly. Sea Salt Superstore leveraged e-commerce to test customer demand before expanding into physical stores, successfully growing its presence to over 1,000 retail locations, including Costco and Kroger. In January 2025, Salted Perfection introduced a wholesale website, enabling independent grocers and specialty shops to purchase artisan salts without the high minimum-order requirements that previously benefited larger chains. Jacobsen Salt Co., which has operated the first solar saltworks in the Pacific Northwest since the 1800s, generated USD 8.6 million in 2025 through a direct-to-consumer model. This growth was further supported by partnerships with premium brands such as Oishii, offering Koyo Berry Infused Salt (USD 18 for 2.64 ounces), and Fly By Jing, featuring Tingly Sichuan Salt (USD 15). The rise of online shopping, which accelerated during the COVID-19 pandemic, has remained strong as consumers appreciate the ability to compare product origins, read reviews, and access unique varieties not typically available in local supermarkets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Traditional salt competes with gourmet options | −0.7% | Price-sensitive Asia-Pacific and South America | Long term (≥ 4 years) |

| High sodium intake raises health concerns | −0.6% | North America and Europe | Medium term (2-4 years) |

| Regulations increase compliance challenges | −0.4% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Seasonal harvesting causes supply fluctuations | −0.3% | Coastal zones in Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Traditional Salt Competes with Gourmet Options

Commodity refined salt, priced at USD 45 per ton for rock salt and USD 150 per ton for solar salt, holds a dominant share in food processing and household use. This dominance limits the market for gourmet salt to premium segments. According to the United States Geological Survey, only 4% of total salt consumption in 2024 was used in food processing[2]Source: United States Geological Survey. "Mineral Commodity Summaries: Salt." usgs.gov. Most of the salt was used for de-icing (43%), chemical feedstock (39%), and water treatment (14%), highlighting the limited role of culinary salts. In emerging markets, consumers often prioritize cost over origin. For example, in Pakistan, raw Himalayan salt is priced at USD 40 per ton domestically but sells for USD 300 per ton in European markets. This 650% price increase reflects the premium value in export markets but also shows the gap between production costs and retail pricing. Compass Minerals reported that consumer and industrial salt prices rose to USD 205.74 per ton in 2024. However, this is still far below the retail price of over USD 2,000 per ton for fleur de sel. This price difference creates a risk of substitution, especially during economic downturns when buyers focus more on value. Gourmet salt producers face the challenge of maintaining their premium image while competing with commodity salt, which provides the same sodium chloride functionality at a much lower cost.

Health-Conscious Consumers Prefer Mineral-Rich Salts

Public-health campaigns focused on reducing sodium intake face challenges because consumers often link all types of salt, including gourmet varieties, to cardiovascular risks. In 2024, the World Health Organization recommends limiting daily sodium intake to less than 5 grams, about 1 teaspoon of salt[3]Source: World Health Organization. "Salt Reduction Fact Sheet." who.int. However, the Centers for Disease Control and Prevention reports that most Americans consume more than this amount, increasing regulatory pressure on food manufacturers to modify their recipes. Gourmet salt brands promote their mineral content, such as magnesium, potassium, and calcium, as health benefits, but there is little clinical evidence to support significant advantages at typical consumption levels. This creates a conflict: as people become more aware of the risks of hypertension, even health-conscious individuals may reduce their salt use, lowering demand across all price ranges. This trend is especially noticeable in North America and Europe, where aging populations and higher rates of chronic diseases have intensified the focus on reducing dietary sodium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fleur de Sel Dominates, Specialty Salts Innovate Fastest

In 2025, Fleur de sel held 33.88% of the market value, remaining the top choice for premium finishing salt among chefs and home cooks. Its production depends on traditional methods and is heavily influenced by weather conditions. In France's Guérande region, the Le Guérandais cooperative employs over 300 workers who carefully hand-skim salt crystals from evaporation ponds using wooden "lousse" tools. This process requires dry, sunny weather and easterly winds. After harvesting, the salt crystals are drained for 2 to 3 years before being sold. The United Kingdom has awarded Protected Geographical Indication (PGI) status to Guérande fleur de sel, highlighting its superior quality and protecting it from cheaper substitutes. Although its supply is limited due to weather changes and labor-intensive harvesting, retail prices above USD 12.99 for a 4.4-ounce pack ensure strong profits for producers and show that consumers value authentic, high-quality products.

The Specialty Salt market is expected to grow at a 6.21% CAGR through 2031, making it the fastest-growing product category. This growth is driven by the rising popularity of flavored, smoked, and infused salts, which meet the demand for unique products from food processors. SaltWorks has invested over USD 2 million in its Perfect Smoke Technology, a special cold-smoking process that uses selected woods like alderwood, applewood, hickory, mesquite, and cherrywood. This technology allows co-packers to add smoked salts to sauces and seasonings without needing extra processing. Jacobsen Salt Co. has partnered with Oishii and Fly By Jing to create innovative flavors paired with visually appealing, social-media-friendly packaging that attracts millennial and Gen Z consumers. Redmond Agriculture has introduced smoked Real Salt varieties, including hickory and cherry smoked for 30 hours and a chef's blend smoked for 42 hours, targeting both retail and food-service markets.

By Distribution Channel: Retail Leads, Food Processing Accelerates

In 2025, retail distribution made up 59.81% of the market value, showing the growing popularity of gourmet salt as a pantry essential. Consumers mainly buy it from supermarkets, hypermarkets, online stores, and specialty shops. Sea Salt Superstore tested demand through e-commerce before expanding to over 1,000 physical locations, including Costco and Kroger. This strategy helped reduce inventory risks and speed up its store expansion. Online retail within the retail segment has grown quickly. Brands like Jacobsen Salt Co., which generated USD 8.6 million in revenue in 2025, and Salted Perfection, which launched its wholesale site in January 2025, avoid distributor margins to improve profitability. Supermarkets and hypermarkets remain the top sub-channels, offering shelf space to popular brands like Maldon and Morton, along with private-label gourmet products. Convenience stores and other outlets focus on impulse buyers and niche markets.

The food processing sector is expected to grow the fastest, with a projected CAGR of 5.01% through 2031. This growth is driven by manufacturers updating recipes to meet clean-label standards and create premium products. In April 2025, Cargill announced a USD 68 million investment to expand its St. Clair, Michigan, Alberger facility by 40% to meet increasing demand. Producers of snacks, baked goods, and prepared meals are looking for salt flakes that stick better to food surfaces and enhance flavor. In March 2025, Michigan Potash started a food-grade salt business at its Evart plant, aiming to produce 1 million tons of high-purity salt annually. This move is intended to reduce the U.S.'s reliance on imports, which currently make up 25% of domestic consumption, mainly from Canada and Chile. Although the HoReCa sector is smaller in volume, it has a strong influence on consumer preferences. Olsson's Salt sampled its products at 500 restaurants and reported that gourmet flakes contribute 10% of its revenue, showing how chefs impact retail trends. For example, Michelin-starred chef Adam Byatt endorsed Maldon Crystal Salt in November 2020, demonstrating how professional recommendations inspire home cooks to make similar purchases.

Geography Analysis

In 2025, North America held a 37.23% share of the market value, supported by its strong culinary traditions, growth in premium grocery products, and a well-established food-service network. The U.S. led the region's demand, with producers showing confidence through significant capacity expansions. For instance, Morton Salt announced in June 2025 that it would expand its facilities to add 500,000 tons of evaporated salt and 360,000 tons of solar salt. Similarly, in April 2025, Cargill invested USD 68 million to increase production at its St. Clair, Michigan facility by 40%, focusing on snack and bakery producers. According to the United States Geological Survey, Canada and Mexico are key suppliers, with the U.S. importing 25% of its salt from Canada and Chile, and 12% from Mexico. E-commerce is thriving, with brands like Jacobsen Salt Co., which earned USD 8.6 million in revenue in 2025, and Sea Salt Superstore, with over 1,000 retail locations, using online platforms to reach suburban and rural customers.

The Asia-Pacific region is expected to grow at the fastest rate, with a projected CAGR of 5.34% through 2031. This growth is driven by rising incomes, increasing popularity of Western cuisine, and higher demand for premium ingredients. Between June 2024 and May 2025, Japan imported USD 245 million worth of salt, making it the third-largest importer globally with a 7.09% market share. Japan mainly sources salt from Australia, China, and Mexico. A December 2025 article in The Japan Times highlighted a Yamaguchi salt artisan who compared the seasonal variations in his sea salt to the terroir of wine. In China, urbanization and a growing middle class are boosting demand for premium ingredients, although domestic producers face price competition and varying food-grade salt regulations across provinces. In December 2024, India's Goyal Salt invested INR 80 crore (USD 9.6 million) to build a natural salt plant in Gujarat with a capacity of 450,000 tons per year, aiming to lead the Indian natural salt market. Other contributors to the region's supply and demand include Australia, Indonesia, South Korea, Thailand, and Singapore, with Australia emerging as a major exporter of solar-evaporated sea salts.

Europe, South America, and the Middle East and Africa are experiencing steady but slower growth, influenced by local regulations and cultural factors. In Europe, strict food-safety standards and frameworks like the Protected Geographical Indication (PGI) - such as the 2012 PGI for Guérande fleur de sel - support premium pricing but make it harder for new players to enter the market. Key demand drivers in Europe include Germany, the U.K., Italy, France, and Spain. Maldon Crystal Salt is popular in British kitchens, while Le Guérandais is a staple in French cuisine. In South America, countries like Brazil, Argentina, and Chile are leading growth as rising incomes and exposure to global cuisines increase interest in specialty salts, though price sensitivity remains a challenge. The Middle East and Africa offer fragmented opportunities. Urban centers in South Africa, Saudi Arabia, the U.A.E., and Turkey show demand for premium products, while countries like Nigeria, Egypt, and Morocco focus on commodity salts. South Africa's Kalahari Pristine Salt Worx has found success with its Kalahari Desert salt, but overall market penetration in the region remains behind North America and Europe.

Regulatory Landscape

Gourmet salt sold for food use is governed by food-grade composition, labeling, and permitted processing aids, with Codex Alimentarius acting as a key reference for international trade. In November 2025, the Codex Alimentarius Commission adopted amendments to the Standard for Food-Grade Salt (CXS 150-1985), including updates affecting labeling for non-retail containers and references to recognized methods of analysis and sampling. The change lifts expectations for consistent documentation and testing across exporting and importing markets.

In the European Union, product positioning and innovation also run through novel food and additive compliance. Commission Implementing Regulation (EU) 2025/1530 authorized potassium magnesium trichloride hexahydrate as a novel food under defined conditions of use, reinforcing that mineral-salt blends marketed for reformulation or reduced-sodium positioning can require pre-market authorization and technical dossiers. Trade measures can further shape destination-specific availability and pricing. For example, Vietnam Circular 03/2026/TT-BCT (effective March 15, 2026) set an import tariff-rate quota of 97,020 tons for salt (HS 2501) for specified industrial uses, which puts quota access rules and end-use constraints at the center of exporter planning.

Value Chain Analysis

The gourmet salt value chain starts with raw material sourcing from sea-salt solar evaporation, mined rock salt, and mineral-rich deposits, including Himalayan-origin salts. After washing or refining where needed, producers dry, grade the material (flake, coarse, fine), and add value through steps such as smoking, infusion, and blending. Compliance and quality assurance, for example meeting Codex CXS 150-1985 food-grade expectations, rely on consistent analytical testing and documentation, including certificates of analysis, to support traceability claims and facilitate cross-border clearance for premium retail and food-manufacturing customers.

Packaging, branding, and route-to-market execution are key margin levers for this category. Gourmet salt depends on origin storytelling, format performance (including flake adhesion for toppings), and clean-label positioning. Large producers and specialist firms support processing, packaging, and private-label or co-packing to scale into retail and ingredient channels, while artisanal producers often use direct-to-consumer and specialty retail to reach buyers without relying on traditional distributors. Sector associations such as EUsalt and SEASALT Europe also contribute to standards dialogue and sustainability positioning, which is relevant for European sea-salt makers operating in regulated coastal environments and selling into PGI/PDO-sensitive premium segments.

Competitive Landscape

The gourmet salt market is moderately consolidated, with a mix of established global producers and regionally strong artisanal players shaping competitive dynamics. Large companies benefit from broad distribution networks, strong sourcing capabilities, and the ability to supply consistent quality across multiple formats, including flakes, crystals, and infused salts. Leading the charge are industry giants such as Cargill Inc, Morton Salt Inc, Saltworks Inc, CK Life Sciences Int’l. (Holdings) Inc, and Maldon Crystal Salt Company Limited. Their scale allows them to serve food processors, foodservice operators, and premium retail channels, giving them a stable share in high-volume applications while maintaining premium positioning.

At the same time, smaller and artisanal producers play a critical role in market differentiation by emphasizing origin, harvesting methods, and unique mineral profiles. These players often focus on single-source sea salts, hand-harvested varieties, and specialty infusions, catering to chefs, gourmet retailers, and consumers seeking authenticity and traceability. While their volumes are lower, strong branding, storytelling, and premium pricing enable them to compete effectively in niche segments, particularly in developed markets with high culinary experimentation.

Competition in the market is increasingly driven by product innovation, sustainability credentials, and application-specific solutions rather than price alone. Leading players are expanding portfolios with smoked, flavored, and low-sodium gourmet salts, while also investing in sustainable harvesting and eco-friendly packaging to align with clean-label and environmental trends. This balanced structure, where scale-driven leaders coexist with innovation-focused niche brands, supports steady market growth and reinforces the moderately consolidated nature of the gourmet salt industry.

Gourmet Salt Industry Leaders

-

Morton Salt, Inc.

-

Saltworks Inc.

-

CK Life Sciences Int’l., (Holdings) Inc

-

Maldon Crystal Salt Company Limited

-

Cargill Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and footprint expansion in producing regions are creating room for premium and specialty formats to deepen into food manufacturing and modern retail assortments. In North America, Cargill committed USD 68 million (April 2025) to expand its St. Clair, Michigan Alberger facility by 40%, targeting demand from snack, bakery, and prepared-meal manufacturers that use flake salts for surface adhesion and flavor delivery. Morton Salt also announced (June 2025) a major North American consumer-segment expansion, adding about 500,000 tons of evaporated salt and 360,000 tons of solar salt capacity. Together, these projects help expand availability of differentiated grain sizes and application-specific salts used in clean-label reformulation and premium line extensions.

In Asia-Pacific supply chains, new investments and resource access programs are improving both domestic and export-oriented gourmet salt positioning. In India, Tata Chemicals announced salt capex actions including a greenfield 210 KTPA Iodised Vacuum Salt Dried facility in Ramanathapuram, Tamil Nadu (February 2026) and a Mithapur debottlenecking program adding 82,500 TPA (board-approved May 2026), supporting regional sourcing optionality for branded and private-label players. Upstream, Ittefaq Salt expanded its Himalayan pink salt mining footprint by securing 1,789.72 acres across five new mining areas in Punjab, Pakistan (January 2026), improving long-term raw material access for premium pink salt export categories. On the regulatory side, the EU novel food authorization route, evidenced by Implementing Regulation (EU) 2025/1530 for a mineral salt ingredient, provides a defined pathway for mineral-rich and reformulation-oriented salt blends, supporting product development that aligns with sodium-reduction programs while maintaining gourmet positioning.

Recent Industry Developments

- March 2026: CK Life Sciences reported continued progress in its Australia and New Zealand salt operations through operational excellence and customer management across the 2025 fiscal year. The update highlights how efficiency programs and account-level pricing discipline are being used to protect supply continuity and service levels across retail and food-manufacturing demand cycles.

- June 2025: Morton Salt announced a major expansion of its North American consumer-segment production capabilities, adding about 500,000 tons of evaporated salt capacity and 360,000 tons of solar salt capacity over a 12-18 month completion window. The added output supports broader availability of culinary formats and helps stabilize supply for branded and private-label channels that increasingly carry premium and specialty salts.

- January 2025: SaltWorks debuted a new line of specialty salts aimed at food-industry and private-label markets. The portfolio expansion strengthens co-packing and customization options for manufacturers and retailers seeking differentiated salts, including distinctive grain sizes and application-driven formats, without building in-house processing capability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the gourmet salt market covers specialty salts used mainly for cooking and seasoning in homes, foodservice, and food manufacturing, and it is sized in value terms at the prices paid in the market.

Scope exclusions: We exclude commodity salt sold mainly for industrial uses (such as de-icing, chemicals, and water treatment) where the purchase decision is not driven by culinary attributes.

Segmentation Overview

-

Type

- Sel Gris

- Flakey Salt

- Himalayan Salt

- Fleur De Sel

- Specialty Salt

- Other Types

-

Distribution Channel

- Food Processing

- HoReCa

-

Retail

- Supermarkets/Hypermarkets

- Online Retail Store

- Convenience Store

- Other Distribution Channels

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to anchor it to repeatable public signals. We leaned on sources such as FAOSTAT for salt production context, UN Comtrade for trade flows of salt and related prepared food categories, and national statistics offices for household food spending and price indices that influence seasoning purchases.

To keep assumptions realistic, we also reviewed customs and food safety portals, including official regulators that publish food labeling guidance and allowable claims, along with industry association releases that describe culinary salt trends and premiumization. Company annual reports, investor decks, and reputable press were used to understand channel mix shifts and packaging moves, and a paid subscription for company financials and for news and financials helped confirm scale and timing where public disclosure is limited. These desk sources are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification checks.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, specialty retailers, and foodservice buyers across major consuming regions, so pricing, channel shares, and adoption trends could be confirmed. Respondent input was used to refine premium price bands, clarify how much value is captured through online specialty retail, and check how food processing demand is counted, and then to pressure-test the desk assumptions before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 49% |

| Mid tier: 52% | Functional/Unit leaders: 38% | EMEA: 29% |

| Smaller Players: 18% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where regional demand pools were reconstructed from food consumption and spend patterns, then adjusted for the premium-salt penetration seen across retail, foodservice, and food processing. To keep the totals realistic, we then corroborated them with selective bottom-up approximations, such as sampled brand and private-label price points multiplied by observed volumes in key channels, followed by distributor and retailer checks on movement.

Key inputs used in the model included premium price spreads versus table salt, import and export signals for specialty salt varieties, channel mix shifts between retail, Horeca, and food processing, and macro indicators like food CPI and disposable income trends that influence discretionary pantry upgrades. Where primary feedback showed large variance in pricing by format (flakes, crystals, fine grind) and origin, the model uses banded average selling prices rather than a single blended price, and gaps were handled by applying region-level price bands to verified channel volumes. Forecasts were developed using scenario analysis around premiumization pace and channel growth, and then aligned to expert consensus on how quickly gourmet salts move from occasional purchases into everyday cooking.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including trade direction changes, price index movements, and channel growth patterns that should logically move with gourmet salt sales. When large variances appeared by region or channel, the drivers were re-reviewed, and respondents were re-contacted to confirm whether it was a real shift (such as a channel spike) or a modeling issue.

A multi-step internal review was followed, where assumptions, unit conversions, and currency treatment were verified before sign-off. Reports are refreshed annually, and interim updates are made when material events occur that can change pricing or demand, followed by a final pre-delivery review pass so clients receive the most current view.

Mordor Intelligence's Gourmet Salt Market Estimate Compared With Other Published Estimates

Published market sizes for gourmet salt can look far apart because each publisher draws the market line differently, and each also uses different price logic and update timing. The main differences usually show up when one estimate mixes in broader salt categories, assumes a higher premium price level, or uses a faster growth case without aligning it to how volume is actually traded through channels.

In this market, the biggest gap drivers are whether food processing volumes are fully counted, whether flavored salts and seasoning blends are treated as part of gourmet salt, and how retail versus Horeca prices are blended into one value figure. Currency conversion timing also matters because gourmet salt is traded and premium prices can move, so an older exchange-rate set can inflate or deflate the current-year USD number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.96 B (2026) | |

| Global Publisher A | USD 2.92 B (2025) | This figure appears to use a wider product pool and a higher blended price assumption, with online and offline value aggregation that can pull in adjacent specialty seasonings beyond culinary salts. |

| Industry Publisher B | USD 5.11 B (2025) | This estimate is consistent with a much broader definition that can capture more of the overall salt and specialty seasoning value chain, and it also uses enterprise revenue framing that may not match end-market value at the same conversion timing. |

The spread is mainly explained by what gets counted as gourmet salt and how prices are blended across channels, and the table makes that visible in one place. By keeping flavored seasoning mixes out of scope and by only counting culinary specialty salts where they are actually purchased in retail, Horeca, or food processing, the sizing stays traceable to clear demand signals, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the gourmet salt market in 2026?

The gourmet salt market size is USD 2.0 billion in 2026 and is on track to approach USD 2.48 billion by 2031.

What is the expected CAGR for gourmet salt through 2031?

The market is forecast to grow at a 4.85% CAGR from 2026 to 2031.

Which product type holds the largest share?

Fleur de sel leads with 33.88% of revenue due to its artisanal harvesting and strong chef endorsement.

Which channel is expanding quickest?

Food processing is advancing at a 5.01% CAGR as manufacturers adopt gourmet flakes for clean-label reformulation.

Page last updated on: