Marine Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

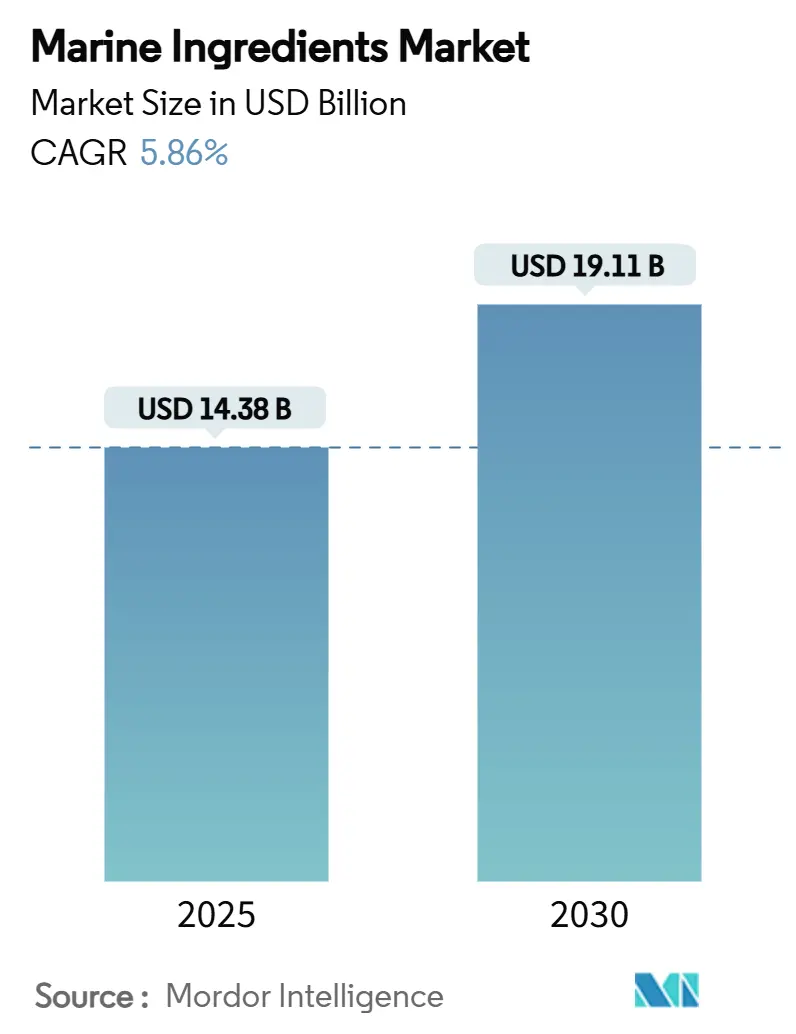

| Market Size (2025) | USD 14.38 Billion |

| Market Size (2030) | USD 19.11 Billion |

| Growth Rate (2025 - 2030) | 5.86% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Marine Ingredients Market Analysis by Mordor Intelligence

The marine ingredients market size reached USD 14.38 billion in 2025 and is projected to reach USD 19.11 billion by 2030, representing a 5.86% CAGR. The growing demand for sustainable aquaculture feed, the rapid adoption of algae-derived omega-3 oils, and regulatory pressures favoring high-efficiency formulations are steering the marine ingredients market toward advanced technologies. Industry participants are scaling precision-fermentation platforms to valorize by-products, mitigating raw-material volatility linked to Peru’s anchovy fishery. Investments in large-scale algae cultivation reduce over-reliance on wild catch supplies, while certification frameworks such as ASC Feed Standard have started rewarding traceable, low-impact products. Competitive differentiation now hinges on vertical integration, technological innovation, and verified sustainability credentials in the marine ingredients market.

Key Report Takeaways

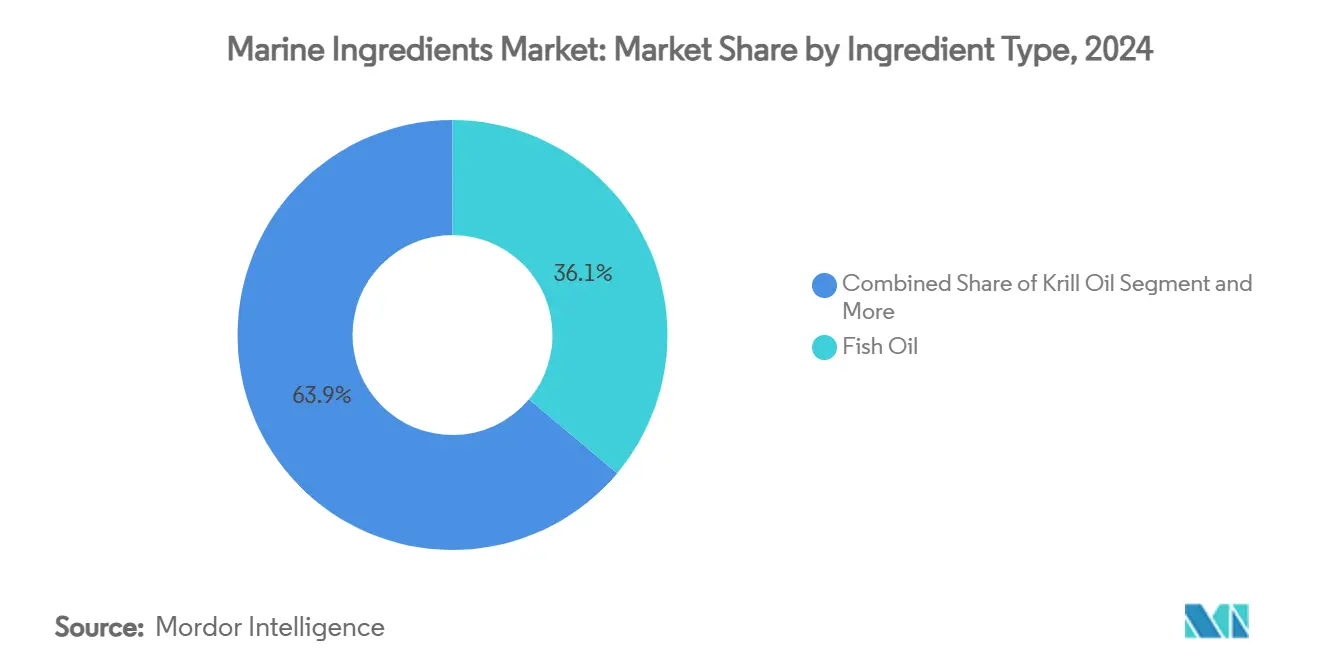

- By ingredient type, fish oil led with a 36.48% marine ingredients market share in 2024, whereas algal DHA/EPA oil posted the highest growth at a 10.80% CAGR through 2030.

- By source, fish contributed 64.39% of the marine ingredients market size in 2024, while microalgae expanded at a 9.40% CAGR, the fastest in the category.

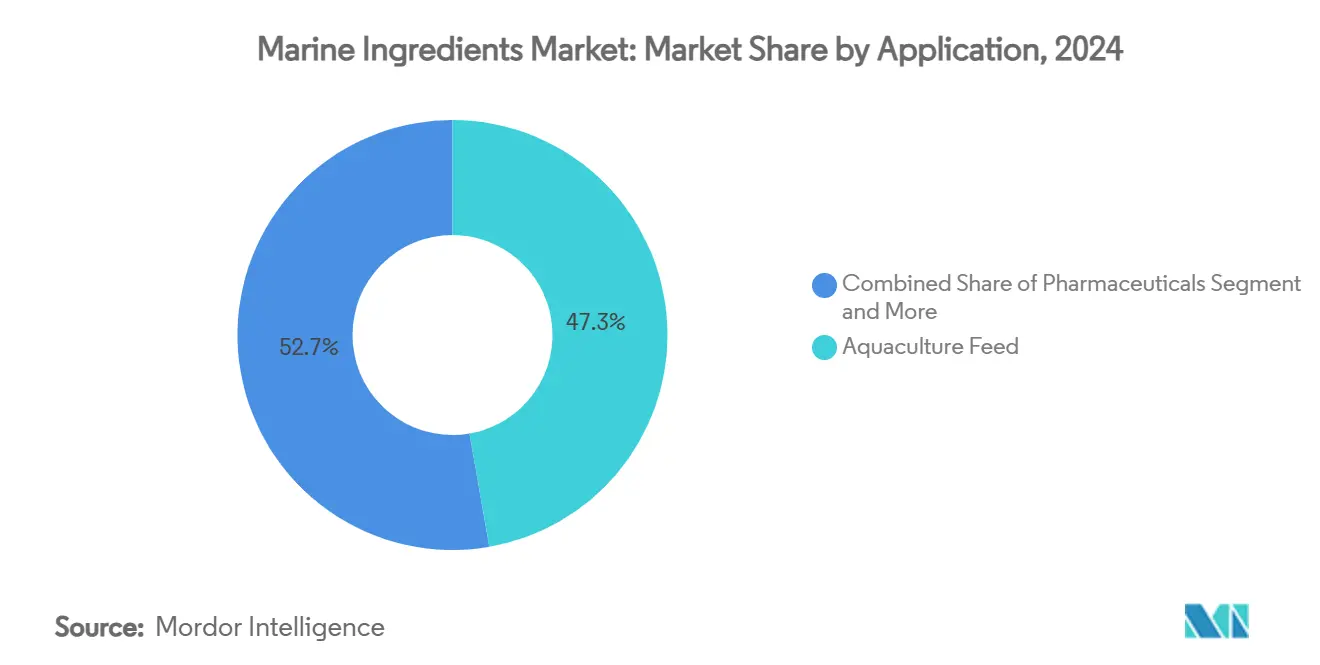

- By application, aquaculture feed held 47.74% of the marine ingredients market share in 2024; dietary supplements advanced at an 8.60% CAGR, outpacing other uses.

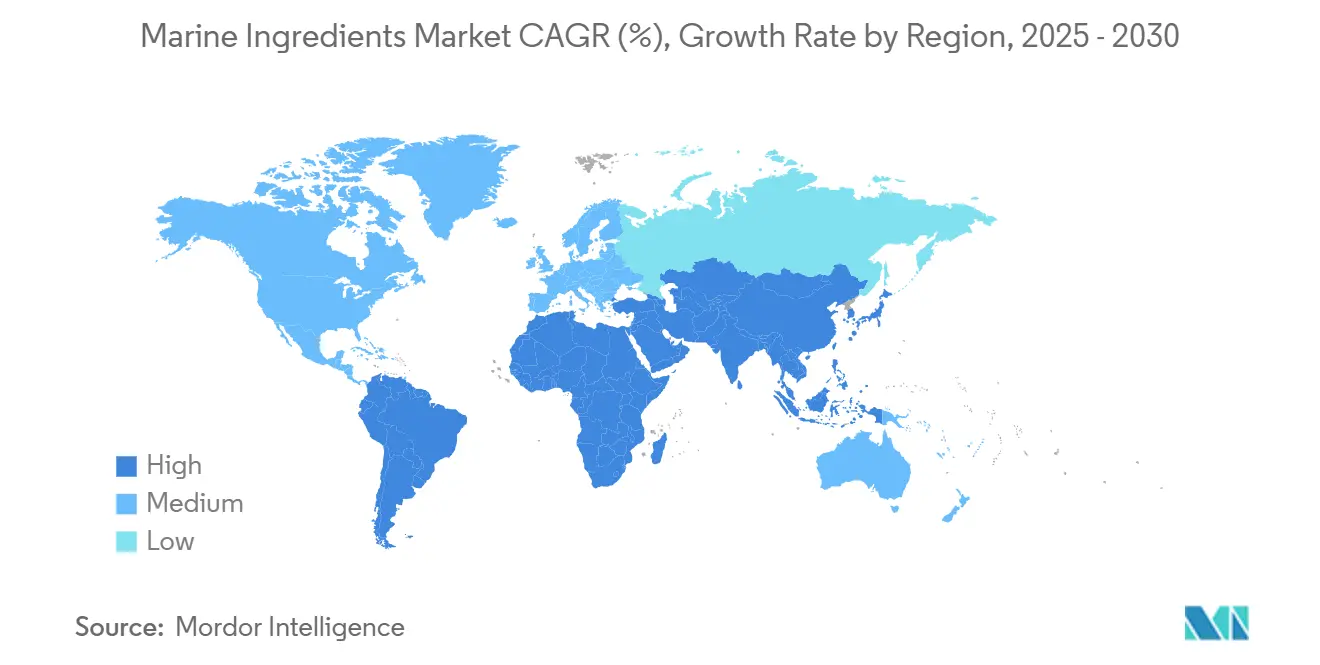

- By geography, Asia-Pacific accounted for 45.38% of the marine ingredients market in 2024, whereas the Middle East & Africa region recorded the strongest growth, at 6.92% CAGR through 2030.

Global Marine Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging aquaculture feed demand | +1.8% | Global, with concentration in Asia-Pacific and emerging MEA markets | Long term (≥ 4 years) |

| Rising consumer awareness of omega-3 supplements | +1.2% | North America & EU primary, expanding to APAC urban centers | Medium term (2-4 years) |

| Expansion of large-scale algae cultivation capacity | +0.9% | Global, with early commercial deployment in Europe and North America | Long term (≥ 4 years) |

| Regulatory push for feed-conversion efficiency | +0.7% | EU and North America leading, with spillover to export-oriented APAC producers | Medium term (2-4 years) |

| Precision-fermentation valorization of by-products | +0.5% | North America & EU innovation hubs, scaling to global markets | Long term (≥ 4 years) |

| Enzymatic hydrolysis unlocking high-value peptides | +0.4% | Global, with R&D concentration in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Aquaculture Feed Demand

Global aquaculture production is registering increased production[1]"Global aquaculture surging, with production surpassing wild-catch fisheries, 2024 UN FAO SOFIA report finds', June 2024, https://www.seafoodsource.com/news/supply-trade/global-aquaculture-surging-with-production-surpassing-wild-catch-fisheries-2024-un-fao-sofia-report-finds, creating unprecedented demand for high-quality marine ingredients that optimize feed conversion ratios and fish health outcomes. The sector's expansion reflects shifting protein consumption patterns, particularly in emerging economies where aquaculture provides affordable animal protein alternatives to traditional livestock. Feed represents over 50% of aquaculture production costs[2]Food and Agriculture Organization. "Impacts of El Niño on Marine Fisheries and Aquaculture." November 12, 2021. https://openknowledge.fao.org/server/api/core/bitstreams/66538eba-9c85-4504-8438-c1cf0a0a3903/content/sofia/2024/impacts-marine-fisheries-aquaculture.html, intensifying focus on ingredient efficiency and nutritional density to maintain economic viability. Advanced marine ingredients enable producers to reduce fishmeal dependency while maintaining growth performance, addressing both cost pressures and sustainability concerns. The integration of precision nutrition approaches allows formulators to optimize ingredient combinations for species-specific requirements, enhancing both economic returns and environmental outcomes.

Rising Consumer Awareness of Omega-3 Supplements

In 2024, consumer awareness of omega-3's health benefits has surged demand for dietary supplements, with the Global Organization for EPA and DHA Omega-3s noting a year-over-year volume uptick, even amidst supply challenges. Clinical studies have not only validated omega-3s' cardiovascular, cognitive, and anti-inflammatory advantages but have also broadened their use from traditional fish oil capsules to functional foods, beverages, and pharmaceuticals. Major markets granting regulatory approvals for health claims have bolstered the legitimacy of omega-3 supplements. Meanwhile, a rising vegetarian and vegan demographic is fueling the demand for algal-derived omega-3 alternatives. High-concentration EPA/DHA products command premium prices, presenting lucrative opportunities for marine ingredient suppliers who can offer standardized and bioavailable formulations. As developed regions reach market saturation, there's a noticeable shift towards the Asia-Pacific and Latin American markets, buoyed by rising disposable incomes that favor premium health products.

Expansion of Large-Scale Algae Cultivation Capacity

The increased technological breakthroughs, companies like DSM-Firmenich are producing marine-equivalent omega-3 oils from microalgae, achieving EPA/DHA ratios that rival traditional fish oil. Innovations in photobioreactors and optimized fermentation processes have not only slashed production costs but also ensured consistent yields. As a result, algal oils are now economically on par with premium fish oil applications. Corbion's ambitious algae roadmap underscores the industry's faith in the scalability of algal production. Many cultivation facilities are now harnessing renewable energy and waste-stream substrates, bolstering their sustainability credentials. This move resonates well with both eco-conscious consumers and evolving regulatory frameworks. Furthermore, the technology's adaptability means production can occur close to consumption hubs, curbing transportation costs and mitigating supply chain risks, a significant advantage over traditional marine harvesting.

Regulatory Push for Feed-Conversion Efficiency

High-efficiency marine ingredients, which optimize nutrient use and lessen environmental impacts, are being adopted more rapidly due to the Aquaculture Stewardship Council (ASC) feed certification requirements. BioMar has become the first in the UK to secure the ASC Feed Certification[3]BioMar. "BioMar achieves UK's first ASC Feed Certification." October 22, 2024. https://www.biomar.com/insights/insights-hub/biomar-achieves-uks-first-asc-feed-certification, underscoring the industry's dedication to evolving sustainability benchmarks. As regulatory frameworks increasingly tie aquaculture licensing to feed efficiency metrics, producers harnessing advanced marine ingredients to boost feed conversion ratios gain a competitive edge. The European Union's Blue Growth Strategy, championing sustainable aquaculture, is spurring investments in innovative feed formulations that lessen reliance on marine resources. While certification schemes reward compliant producers with market access premiums, they also encourage the adoption of high-performance marine ingredients, even if they come with steeper initial costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material supply (e.g., El Niño events) | -1.1% | Global, with primary impact on Peru-dependent supply chains | Short term (≤ 2 years) |

| Stricter sustainability certifications & catch quotas | -0.8% | Global, with strictest enforcement in EU and North America | Medium term (2-4 years) |

| Competition from single-cell protein alternatives | -0.6% | Developed markets initially, expanding globally | Long term (≥ 4 years) |

| Heavy-metal & microplastics contamination concerns | -0.4% | Global, with heightened scrutiny in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Supply

Peru's anchovy fishery, which provides over 70% of the world's omega-3 raw materials, is frequently disrupted by El Niño climate events. These disruptions can lead to a 50-80% reduction in catches during severe episodes. The 2023 El Niño event had a pronounced effect on fish populations, resulting in shortened fishing seasons and surging raw material prices that reverberated through global supply chains. Such climate variability poses inventory management challenges for processors and formulators. As a result, companies are compelled to either maintain larger safety stocks or explore alternative sourcing strategies. The concentration of omega-3 production in a singular geographic region heightens supply risks, especially with the increasing frequency and intensity of El Niño events due to climate change. After significant climate disruptions, recovery can take 2-3 years, leading to prolonged market volatility. This volatility impacts pricing stability and long-term supply contracts across the marine ingredients value chain.

Stricter Sustainability Certifications & Catch Quotas

Organizations like Marin Trust are tightening marine ingredient certification requirements, introducing rigorous traceability and sustainability standards. These heightened standards are driving up compliance costs and complicating operations. The Aquatic Life Institute's 2024 benchmark assessment highlights that aquaculture certification schemes are in a state of flux, necessitating constant adjustments in sourcing and processing practices. In key regions, fishing quota reductions are curtailing raw material availability. Simultaneously, as certification premiums push up ingredient costs, margins across the supply chain are feeling the squeeze. Smaller producers are grappling with heavier certification burdens, a challenge that could pave the way for market consolidation, benefiting larger, vertically integrated operations. The rise of multiple competing certification schemes is not only fragmenting the market but also muddying consumer understanding. Meanwhile, efforts to harmonize regulations across major markets are still a work in progress.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Fish Oil Dominance Challenged by Algal Innovation

In 2024, fish oil secures a commanding 36.48% market share, bolstered by established supply chains, cost advantages, and proven efficacy across diverse applications. The segment reaps rewards from a resurgence in Peru's anchovy fishery, with 2024 catches surpassing 4.8 million metric tons, due to favorable oceanographic conditions. Traditional fish oil processing, benefiting from economies of scale, offers competitive pricing, especially in bulk applications like aquaculture feed, where cost sensitivity is crucial. Fish oil's recognized regulatory status worldwide sidesteps approval hurdles faced by alternative sources. Coupled with extensive clinical research endorsing omega-3's health benefits, this fosters unwavering confidence among consumers and industry players. From its foundational role in aquaculture to its premium positioning in dietary supplements, fish oil's refinement processes allow for tailored EPA/DHA ratios to meet specific demands.

Algal DHA/EPA oil is on a rapid ascent, boasting a projected 10.80% CAGR through 2030. This surge is fueled by a push for sustainability and technological advancements, paving the way for large-scale production. Notably, firms like DSM-Firmenich have bridged the gap, crafting algal products that replicate traditional fish oil's EPA/DHA ratios, overcoming a significant market entry hurdle. Innovations in photobioreactors and optimized fermentation processes have slashed production costs and bolstered yield consistency. As a result, algal oils now stand tall in premium markets, where sustainability often commands a price premium. The segment is further buoyed by a rising tide of vegetarian and vegan consumers, eager for marine-equivalent nutrients devoid of animal origins. Regulatory nods for novel food status in key markets further underscore the segment's commercial promise. Corbion's ambitious algae roadmap, eyeing EUR 200 million in sales by 2028, underscores the industry's faith in scalable algal production. Notably, cultivation facilities are increasingly harnessing renewable energy, bolstering their sustainability credentials.

By Source: Fish Dependency Drives Microalgae Innovation

In 2024, fish sources command a dominant 64.39% share of the marine ingredients market, capitalizing on a well-established processing infrastructure, robust supply chain ties, and cost efficiencies in commodity applications. This segment spans a wide array of species, from Peru's anchovy fishery, a key provider of omega-3 raw materials, to various finfish and shellfish processing by-products, which are transformed into collagen, protein hydrolysates, and specialized bioactive compounds. Traditional fish sourcing leverages advanced extraction and purification technologies, maximizing yield and minimizing waste. Vertical integration strategies empower processors to derive value from multiple product streams using a single raw material input. The Global Organization for EPA and DHA Omega-3s highlights the resilience of fish-derived ingredients in the supply chain, even amidst periodic disruptions. They attribute this stability to effective inventory management and diversified sourcing strategies that counteract climate-related fluctuations. Innovations in processing, such as enzymatic hydrolysis and supercritical extraction, have unlocked high-value compounds from previously overlooked fish by-products, enhancing resource utilization and economic returns.

Microalgae, with a projected 9.40% CAGR through 2030, emerge as the fastest-growing source segment. This growth is fueled by technological advancements that facilitate consistent, year-round production, unaffected by seasonal or climatic changes. At a commercial scale, microalgae cultivation thrives in controlled environments, fine-tuning growth conditions, nutrient mixes, and harvest timings. This approach boosts target compound concentrations and ensures product consistency. One of the standout advantages of microalgae is their geographic flexibility, allowing production close to consumption hubs, slashing transportation costs and curbing supply chain risks. In contrast, traditional marine harvesting is often confined to specific oceanic regions. Research underscores that microalgae can match traditional marine sources in producing omega-3 fatty acids, proteins, and bioactive compounds. Moreover, they sidestep contamination risks tied to ocean-harvested materials. Cutting-edge fermentation technologies amplify this advantage, enabling precise production of specific compounds with superior purity and potency. This capability aligns perfectly with the pharmaceutical and nutraceutical sectors' demand for standardized ingredients, a consistency often elusive with traditional marine sources.

By Application: Aquaculture Feed Leadership with Dietary Supplement Growth

In 2024, aquaculture feed applications dominate the market with a 47.74% share, fueled by a global surge in aquaculture production and a focus on optimizing feed efficiency for economic sustainability. As the fastest-growing sector in food production, aquaculture's global output hits 90.4 million tons in 2024, with Asia accounting for 84% of this volume. Marine ingredients enhance feed conversion ratios, bolster fish health, and elevate product quality. Given that feed constitutes 60-70% of aquaculture's production costs, there's an intensified focus on ingredient efficiency. Advanced marine ingredients allow producers to reduce fishmeal reliance without compromising growth, addressing economic pressures and sustainability issues as wild fish catches stabilize. Precision nutrition enables formulators to tailor ingredient mixes to species needs, boosting financial returns and environmental benefits while adhering to stricter sustainability certifications.

Dietary supplements are the fastest-growing segment, with an 8.60% CAGR through 2030. This growth stems from rising consumer awareness of omega-3's health benefits and expanding applications beyond fish oil capsules. In 2024, the Global Organization for EPA and DHA Omega-3s noted a 1.4% year-over-year volume uptick, underscoring robust demand despite supply challenges. Clinical research validating omega-3s' cardiovascular, cognitive, and anti-inflammatory benefits has expanded their use into functional foods, beverages, and pharmaceuticals. Regulatory approvals for health claims in major markets bolster supplementation legitimacy. High-concentration EPA/DHA products command premium pricing, creating opportunities for suppliers delivering standardized, bioavailable formulations meeting pharmaceutical-grade standards. As developed regions mature, suppliers are expanding into Asia-Pacific and Latin America, where rising disposable incomes favor premium health products. Meanwhile, growing vegetarian and vegan populations drive demand for algal-derived alternatives offering similar nutritional benefits.

Geography Analysis

In 2024, Asia-Pacific commands a dominant 45.38% market share, capitalizing on its robust aquaculture infrastructure and easy access to raw materials. China's stronghold on global aquaculture, producing over 60% of the world's farmed fish, not only underscores its dominance but also fuels a heightened demand for marine ingredients. Complementing this, India's aquaculture is on an upswing, bolstered by government measures like reduced customs duties on shrimp feed inputs. In Southeast Asia, nations such as Vietnam, Indonesia, and Thailand are witnessing a surge in aquaculture, driven by favorable climates and supportive government policies, leading to increased marine ingredient consumption.

Meanwhile, the Middle East & Africa is the regions to watch, boasting the fastest growth rate at a notable 6.92% CAGR projected through 2030. In the Middle East & Africa, rapid growth is spurred by ambitious aquaculture initiatives. Notably, Saudi Arabia has rolled out a USD 4 billion investment program, aiming for an impressive 600,000 metric tons of annual production by 2030, with backing from global feed giants like Cargill. While Sub-Saharan Africa's aquaculture is expanding, it's grappling with feed accessibility issues. However, as infrastructure matures and local feed production ramps up, the region's potential for significant growth becomes evident.

Across the Atlantic, Europe is championing sustainability in marine ingredient applications. Companies like BioMar are at the forefront, securing the UK's inaugural ASC Feed Certification and pioneering feed formulations that lessen reliance on marine resources. North America, on the other hand, is channeling its efforts into premium applications like dietary supplements and functional foods. Here, consumers' readiness to pay a premium for sustainable, traceable ingredients is propelling market growth. The region is also reaping the rewards of technological strides in algae cultivation and precision fermentation, with firms crafting alternatives to conventional fish-derived ingredients.

Competitive Landscape

In the marine ingredients market, traditional fish processors, biotechnology innovators, and vertically integrated aquaculture companies engage in a fragmented competition, though the market shows signs of moderate concentration. Market leaders, like American Industrial Partners, exemplify a trend towards consolidation, as seen in their USD 590 million acquisition of Aker BioMarine's feed ingredients division. Competitive differentiation hinges more on sustainability credentials, technological innovation, and supply chain resilience than on traditional cost competition.

Three distinct competitive strategies emerge: traditional processors emphasize operational efficiency and scale, biotechnology firms pioneer alternative production methods, and integrated players oversee multiple stages of the value chain. There's a growing interest in specialized applications, such as marine-derived pharmaceuticals, cosmetic ingredients, and agricultural biostimulants. These areas, with their technical expertise and regulatory hurdles, present white-space opportunities.

New entrants, termed emerging disruptors, harness precision fermentation and synthetic biology to craft marine-equivalent compounds, sidestepping the limitations of traditional harvesting. In response, established players are forming strategic partnerships and acquiring technologies. The race for innovation is underscored by a surge in patent filings, especially in algae cultivation and bioactive compound extraction, highlighting the industry's quest for intellectual property protection in novel production methods and formulations.

Marine Ingredients Industry Leaders

-

Omega Protein Corporation

-

TASA

-

Corpesca S.A.

-

Aker BioMarine

-

Austevoll Seafood

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thai Union invested USD 30 million in a new marine collagen processing factory in Thailand with 200-tonne annual capacity, focusing on tuna skin utilization for cosmetic and nutraceutical applications, demonstrating the commercial viability of fish by-product valorization.

- April 2025: Marine Biologics launched AI-powered seaweed processing technologies to address chemical composition variability challenges, enhancing consistency in functional food ingredient applications.

- July 2024: American Industrial Partners completed the USD 590 million acquisition of Aker BioMarine's feed ingredients division, the world's largest krill harvester, aiming to leverage maritime expertise for enhanced aquaculture market growth and sustainability initiatives.

Global Marine Ingredients Market Report Scope

| Fish Meal |

| Fish Oil |

| Krill Oil |

| Algal DHA/EPA Oil |

| Marine Collagen |

| Protein Hydrolysates and Peptides |

| Astaxanthin and Other marine Carotenoids |

| Others |

| Fish |

| Krill |

| Squid |

| Seaweed |

| MicroAlgae |

| Others |

| Aquaculture Feed |

| Animal Nutrition & Pet Food |

| Dietary Supplements |

| Functional Foods & Beverages |

| Pharmaceuticals |

| Cosmetics & Personal Care |

| Fertilizers & Agriculture Biostimulants |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Israel | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Fish Meal | |

| Fish Oil | ||

| Krill Oil | ||

| Algal DHA/EPA Oil | ||

| Marine Collagen | ||

| Protein Hydrolysates and Peptides | ||

| Astaxanthin and Other marine Carotenoids | ||

| Others | ||

| By Source | Fish | |

| Krill | ||

| Squid | ||

| Seaweed | ||

| MicroAlgae | ||

| Others | ||

| By Application | Aquaculture Feed | |

| Animal Nutrition & Pet Food | ||

| Dietary Supplements | ||

| Functional Foods & Beverages | ||

| Pharmaceuticals | ||

| Cosmetics & Personal Care | ||

| Fertilizers & Agriculture Biostimulants | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Israel | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the marine ingredients market and how fast is it growing?

The marine ingredients market is valued at USD 14.38 billion in 2025 and is forecast to reach USD 19.11 billion by 2030, registering a 5.86% CAGR.

Which region leads global demand for marine-based feed ingredients?

Asia-Pacific commands 45.38% of global demand, supported by China’s large aquaculture feed sector and expanding production in India and Southeast Asia.

Why are algal omega-3 products gaining traction among supplement brands?

Large-scale photobioreactor and fermentation breakthroughs have cut production costs while matching fish-oil EPA/DHA ratios, offering vegan, traceable alternatives.

What certification trends are shaping purchasing decisions in aquafeed?

ASC Feed Standard and Marin Trust traceability criteria reward feed formulations with verified sustainability and high nutrient efficiency, prompting reformulation across supply chains.

Page last updated on: