Commercial Seaweed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

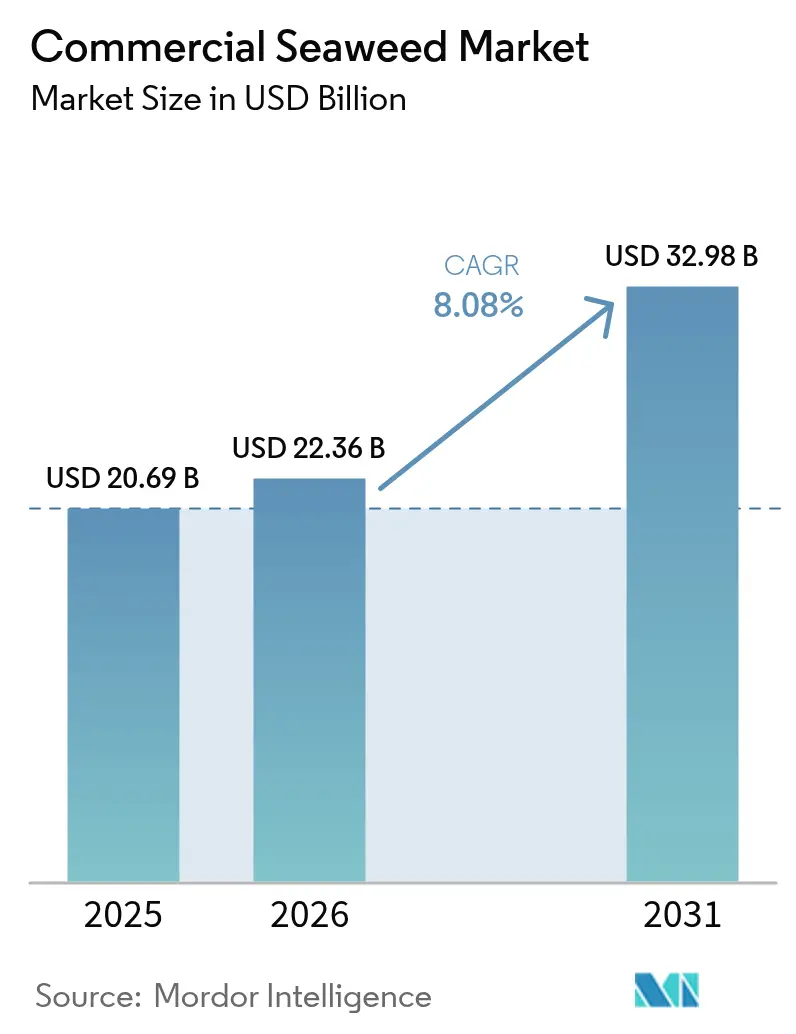

| Market Size (2026) | USD 22.36 Billion |

| Market Size (2031) | USD 32.98 Billion |

| Growth Rate (2026 - 2031) | 8.08% CAGR |

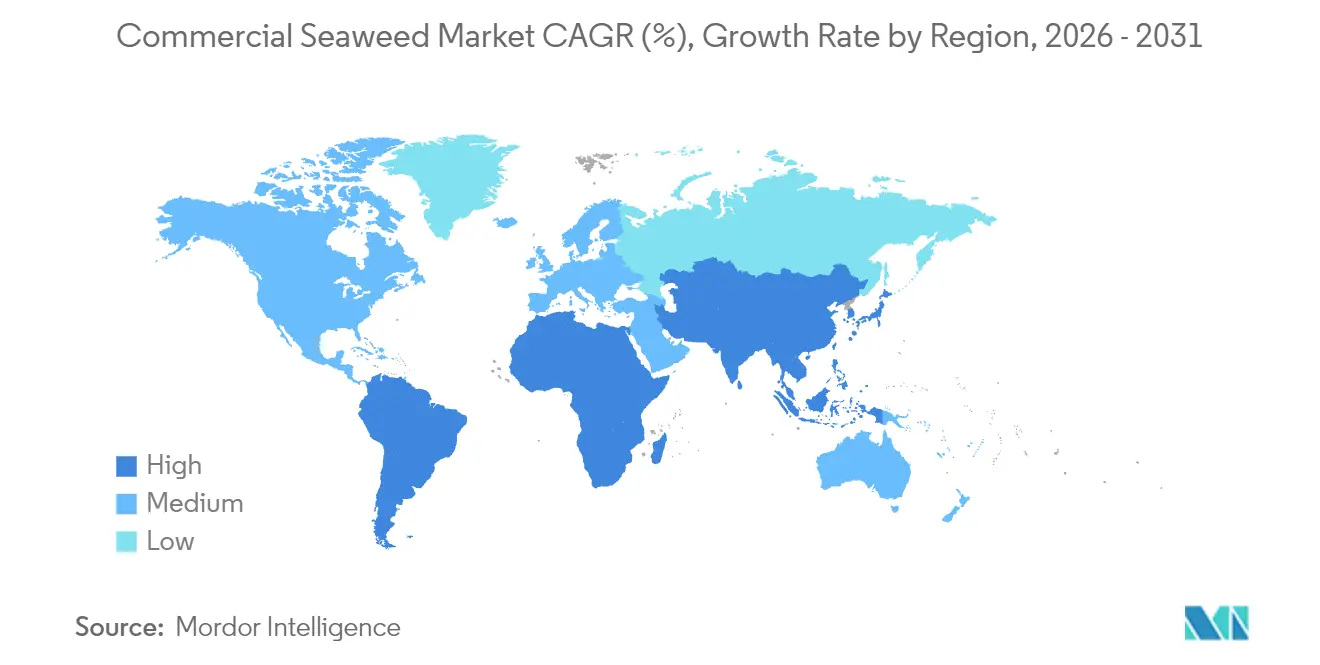

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Seaweed Market Analysis by Mordor Intelligence

The seaweed market size was valued at USD 20.69 billion in 2025 and estimated to grow from USD 22.36 billion in 2026 to reach USD 32.98 billion by 2031, at a CAGR of 8.08% during the forecast period (2026-2031). This growth is primarily driven by increasing demand for seaweed across food and beverage, pharmaceuticals, agriculture, and personal care applications due to its nutritional value and functional properties. Rising consumer preference for plant-based and sustainable ingredients has further accelerated market adoption globally. Additionally, expanding utilization of seaweed-derived hydrocolloids such as agar, carrageenan, and alginate in processed foods is supporting revenue growth. Technological advancements in seaweed cultivation and harvesting methods are improving production efficiency and supply consistency. Government initiatives promoting sustainable aquaculture and marine resource utilization are also contributing to market expansion. Furthermore, increasing investments in seaweed-based bio-products and alternative protein sources are expected to create new growth opportunities, strengthening the market outlook through the forecast period.

Key Report Takeaways

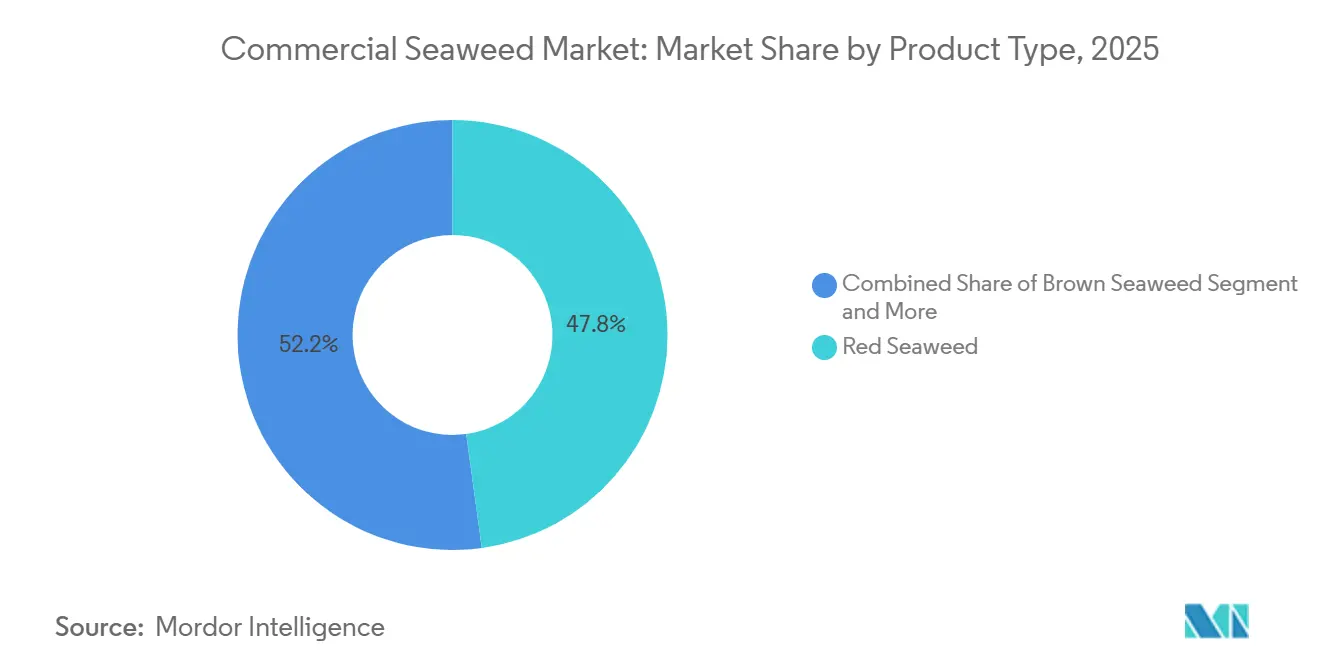

- By product type, red seaweed led with 47.82% revenue share in 2025, while brown seaweed is projected to expand at a 9.87% CAGR through 2031.

- By flavor, plain formats captured 62.07% of 2025 revenue, and flavored variants are advancing at a 9.57% CAGR to 2031.

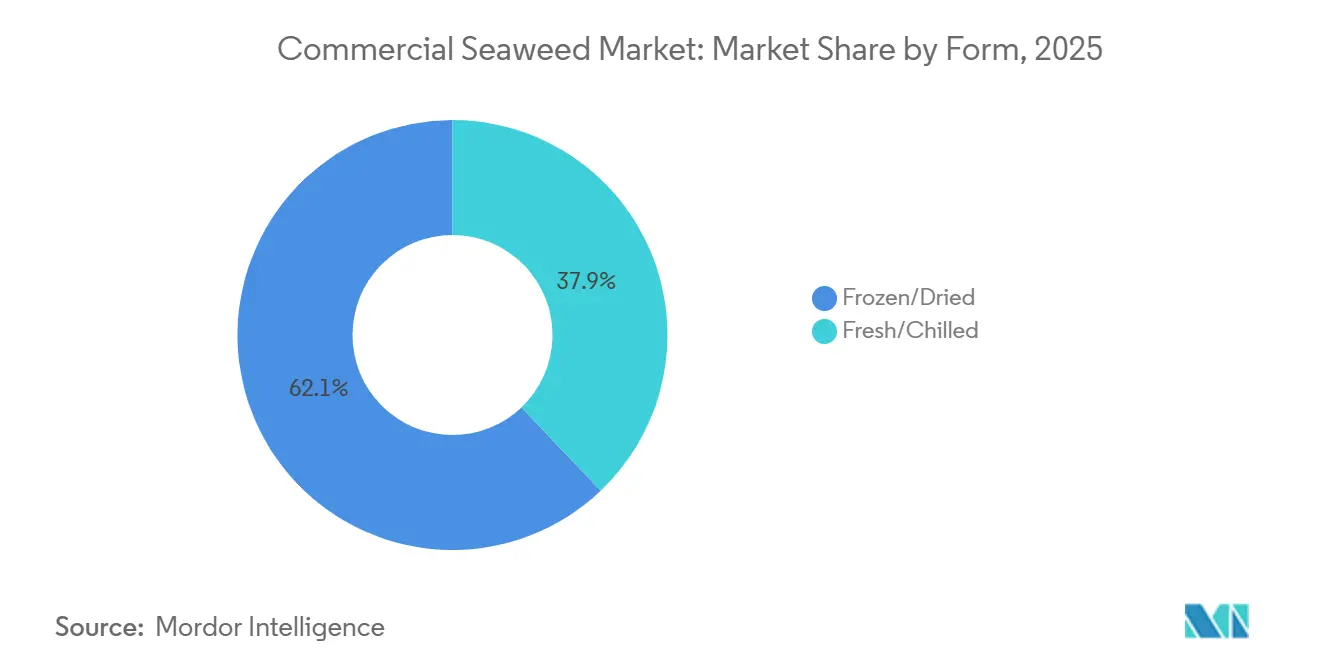

- By form, frozen and dried products accounted for 42.11% revenue in 2025; fresh and chilled is the fastest-growing form at a 10.25% CAGR.

- By cultivation method, aquaculture delivered 91.63% of 2025 volume, whereas wild harvest is forecast to rise at a 9.13% CAGR.

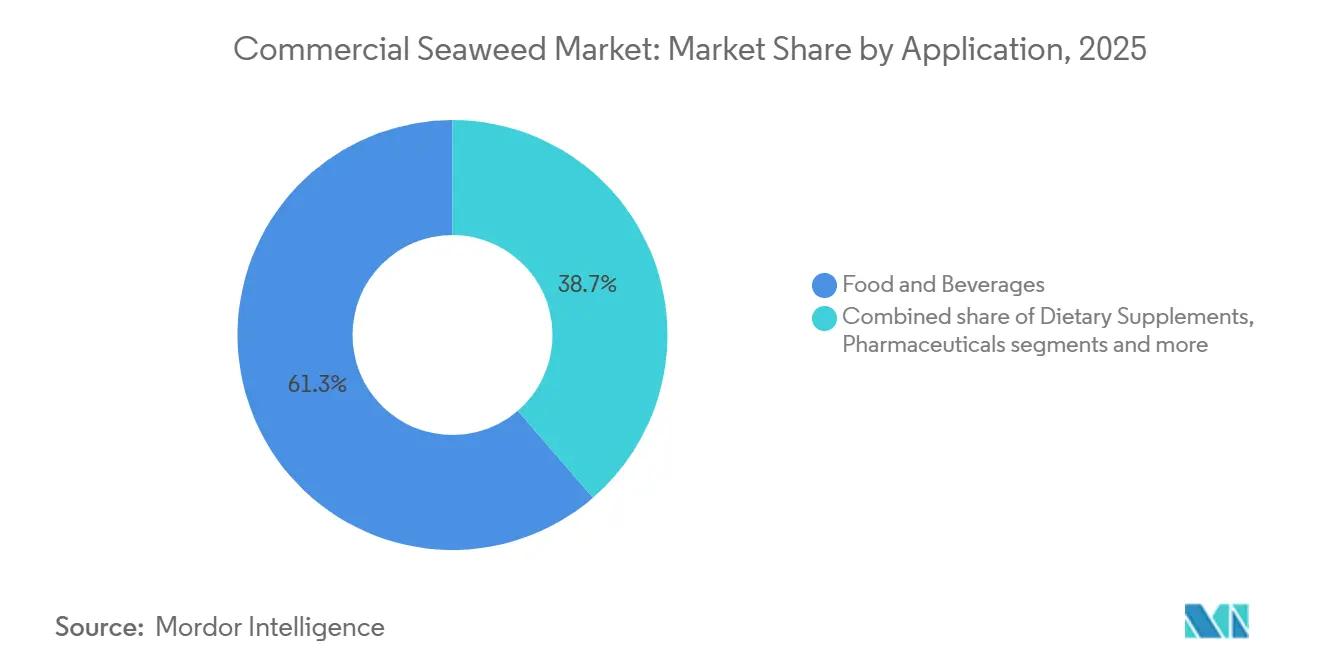

- By application, food and beverages commanded 61.34% revenue in 2025; animal feed and pet food record the highest projected growth at 9.74% CAGR.

- By geography, Asia-Pacific held 37.38% of 2025 value, while Europe represents the quickest regional expansion at a 9.48% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Seaweed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer awareness of health benefits of seaweed | +1.2% | Global, with concentrated uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising use of seaweed in functional foods and nutraceuticals | +1.5% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Increasing applications in cosmetics and personal care products | +0.9% | Europe, North America, premium segments in Asia-Pacific | Long term (≥4 years) |

| Expansion of seaweed use in animal feed and aquaculture | +1.8% | Global, led by Europe, North America, Australia; spillover to Latin America | Short term (≤2 years) |

| Government support for sustainable aquaculture and seaweed farming | +1.3% | Europe (EU Blue Bioeconomy), Asia-Pacific (China, Indonesia, South Korea), North America (NOAA grants) | Long term (≥4 years) |

| Technological advancements improving seaweed cultivation and processing | +1.1% | Global, with innovation hubs in Norway, Netherlands, United States, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer awareness of health benefits of seaweed

Increasing consumer awareness about the nutritional and functional benefits of seaweed is a key driver of the commercial seaweed market. Seaweed is recognized for being rich in vitamins, minerals, dietary fiber, and bioactive compounds, which support immunity, digestion, and cardiovascular health. Rising interest in plant-based, clean-label, and superfood products has encouraged greater incorporation of seaweed into everyday diets. Educational campaigns, media coverage, and health-focused product labeling have further reinforced its image as a natural and sustainable ingredient. Consumers are increasingly seeking functional foods that offer tangible health benefits, which is driving demand for seaweed in both retail and foodservice channels. This growing health consciousness is motivating manufacturers to innovate with new seaweed-based products to meet evolving consumer preferences.

Rising use of seaweed in functional foods and nutraceuticals

The use of seaweed in functional foods and nutraceuticals is rapidly increasing, supporting market growth. Seaweed extracts such as carrageenan, alginate, and fucoidan are widely utilized for their health-promoting properties, including antioxidant, anti-inflammatory, and metabolic benefits. Nutraceutical applications, including dietary supplements and fortified foods, are driving high-value demand for seaweed-based ingredients. Global market data indicates strong adoption in both food and health sectors, with new product launches consistently integrating seaweed as a functional ingredient. The trend toward plant-based nutrition, immunity-boosting products, and clean-label formulations further fuels this growth. Additionally, scientific research validating the bioactive and functional properties of seaweed strengthens its appeal among manufacturers and consumers. Consequently, seaweed is emerging as a preferred ingredient in health-oriented product development, contributing to sustained market expansion.

Technological advancements improving seaweed cultivation and processing

Technological advancements are driving growth in the commercial seaweed market by enhancing cultivation efficiency, processing quality, and overall supply chain reliability. Innovations such as improved long-line and offshore farming techniques, automated harvesting systems, and advanced drying and storage technologies have increased yield, reduced losses, and ensured consistent product quality. Regulatory and standardization developments are also supporting market expansion; for instance, the International Organization for Standardization published ISO 24516 in 2024, establishing quality benchmarks for dried seaweed products[1]Source: International Organization for Standardization, “Sustainable Development Goals”, iso.org. These standards help harmonize international trade, reduce rejection rates during import inspections, and build confidence among global buyers. In addition, advancements in extraction and processing methods are enabling the production of high-value ingredients such as carrageenan, alginate, and fucoidan for functional foods, nutraceuticals, and industrial applications.

Government support for sustainable aquaculture and seaweed farming

Government support for sustainable aquaculture and seaweed farming has strengthened significantly in recent years, particularly through policy-driven initiatives aimed at promoting environmentally responsible marine production. The European Union has reinforced institutional support for seaweed cultivation through new projects funded under the European Maritime, Fisheries and Aquaculture Fund (EMFAF). In 2025, four major initiatives were launched with approximately EUR 5.7 million in funding to scale sustainable algae farming and establish regional innovation hubs across Spain, Portugal, Ireland, and Italy[2]Source: European Commission, “The European Union launches four new projects to advance sustainable algae farming and blue innovation hubs”, cinea.ec.europa.eu. These initiatives focus on advancing regenerative ocean farming practices, improving cultivation technologies, and supporting collaboration between research institutions and industry stakeholders. The funding also aims to accelerate commercialization while ensuring environmental sustainability and biodiversity protection across coastal regions. Such policy measures are aligned with the EU’s broader blue economy and climate strategies, recognizing seaweed farming as a low-impact aquaculture activity with carbon sequestration potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal and geographic limitations impacting year-round production | -0.8% | Temperate zones (North America, Northern Europe, parts of Asia-Pacific) | Short term (≤2 years) |

| High initial investment for seaweed farming infrastructure | -1.0% | Emerging markets (South America, Middle East, Africa), small-scale entrants globally | Medium term (2-4 years) |

| Fluctuations in seaweed yield due to environmental conditions | -0.7% | Global, with acute impact in regions affected by marine heatwaves and ocean acidification | Short term (≤2 years) |

| High cost of processing and extraction technologies | -0.9% | Global, particularly affecting mid-tier processors in Asia-Pacific and Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Seasonal and geographic limitations impacting year-round production

Seasonal and geographic limitations pose a significant restraint on the commercial seaweed market, as production is highly dependent on specific coastal regions with suitable water temperature, salinity, and nutrient conditions. Natural growth cycles and seasonal variations restrict year-round harvesting, leading to fluctuations in supply and challenges in meeting consistent demand. Regions prone to extreme weather, such as storms or temperature anomalies, can further disrupt cultivation and harvesting schedules. Geographic constraints also limit the expansion of large-scale operations to areas with optimal marine conditions, increasing reliance on imports in non-producing regions. These limitations can result in higher production costs and supply chain uncertainties, particularly for manufacturers seeking continuous raw material availability. Additionally, variability in seasonal yields affects quality consistency, which is critical for functional foods, nutraceuticals, and industrial applications.

High initial investment for seaweed farming infrastructure

High initial investment requirements pose a major restraint to the commercial seaweed market, as establishing a viable seaweed farming operation demands substantial capital for infrastructure, equipment, and cultivation systems. In regions like Chile, prospective farmers face additional financial and regulatory challenges, including 18–24 month permitting timelines and the need to comply with rigorous environmental impact assessments. Legal and consulting fees associated with these approvals can exceed USD 50,000, significantly increasing the upfront cost burden[3]Source: National Fisheries and Aquaculture Service, “Fishery Regulations”, sernapesca.cl. Beyond regulatory expenses, farmers must invest in long-line cultivation systems, harvesting machinery, and processing facilities to ensure consistent quality and yield. These high capital requirements can discourage small-scale or new entrants from entering the market. Additionally, the extended time to achieve a return on investment, combined with environmental and operational uncertainties, makes seaweed farming a capital-intensive venture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brown Seaweed Gains on Alginate Demand

Red seaweed accounted for the largest revenue share of 47.82% in 2025, establishing itself as the leading segment within the commercial seaweed market. Its dominance is primarily attributed to extensive usage in food processing, particularly for the extraction of hydrocolloids such as agar and carrageenan, which are widely utilized as stabilizing and thickening agents. The strong demand from the food and beverage industry, especially in dairy, confectionery, and processed food applications, continues to support the segment’s growth. In addition, red seaweed benefits from well-established cultivation practices and a stable supply chain across major producing regions. Increasing consumer preference for natural and plant-based ingredients has further strengthened its market position. Moreover, its application in pharmaceuticals and nutraceuticals due to bioactive compounds and nutritional benefits continues to reinforce its leading revenue contribution.

Brown seaweed is anticipated to emerge as the fastest-growing segment, projected to expand at a CAGR of 9.87% through 2031. The growth of this segment is driven by rising demand for alginate extracts used in food, cosmetics, and medical applications owing to their functional and binding properties. Increasing adoption of brown seaweed in agricultural applications, particularly as biofertilizers and soil conditioners, is also contributing to accelerated market expansion. Furthermore, growing research into its potential use in biofuels, alternative proteins, and sustainable packaging solutions is opening new avenues for commercialization. The segment is also benefiting from increased investments in large-scale seaweed farming and improved harvesting technologies.

By Flavor: Umami Innovation Drives Flavored Segment

Plain formats accounted for the largest share of the commercial seaweed market in 2025, capturing 62.07% of total revenue. The dominance of this segment is largely attributed to its widespread use as a raw material in food processing, hydrocolloid extraction, and industrial applications. Plain seaweed is preferred by manufacturers due to its versatility and ease of incorporation into various end-use products, including soups, snacks, seasonings, and processed foods. It also serves as a foundational ingredient for producing agar, carrageenan, and alginate, which are extensively used as stabilizers and gelling agents. Additionally, bulk procurement of unflavored seaweed by foodservice operators and ingredient manufacturers supports high-volume sales. The segment further benefits from lower processing requirements compared to flavored variants, making it cost-efficient and suitable for large-scale industrial utilization.

Flavored variants are projected to be the fastest-growing segment, expanding at a CAGR of 9.57% through 2031. This growth is driven by rising consumer demand for ready-to-eat and value-added seaweed snacks with enhanced taste profiles. Increasing health consciousness among consumers has fueled interest in convenient, nutrient-rich snack alternatives, positioning flavored seaweed products favorably in retail channels. Manufacturers are introducing innovative flavors tailored to regional preferences, thereby expanding their consumer base. The growing penetration of flavored seaweed in supermarkets, online platforms, and specialty health stores is also supporting segment growth. Moreover, premiumization trends and branding strategies are helping flavored variants command higher margins, further contributing to their accelerated market expansion over the forecast period.

By Form: Cold-Chain Logistics Propel Fresh Segment

Frozen and dried products held the largest share of the commercial seaweed market in 2025, accounting for 62.11% of total revenue. The strong market position of this segment is primarily driven by its extended shelf life, ease of storage, and convenience in transportation across domestic and international markets. Frozen and dried seaweed products are widely utilized in food processing, foodservice, and ingredient manufacturing due to their stable quality and year-round availability. These formats also help reduce post-harvest losses while maintaining nutritional content, making them highly preferred by large-scale buyers. In addition, the growing demand for packaged and export-ready seaweed products continues to support the segment’s dominance.

Fresh and chilled seaweed is projected to be the fastest-growing segment, expanding at a CAGR of 10.25% through 2031. The increasing consumer preference for minimally processed and natural food products is a key factor driving growth in this segment. Fresh and chilled seaweed is gaining traction in restaurants and premium retail outlets due to its perceived freshness, taste, and higher nutritional value. Rising demand for authentic Asian cuisine and healthy meal options has further contributed to the growing consumption of fresh seaweed products. Improvements in cold chain logistics and distribution networks are also enabling wider availability of fresh and chilled seaweed beyond traditional coastal markets.

By Cultivation Method: Aquaculture Dominance Reflects Traceability Demands

Aquaculture represented the dominant cultivation method in the commercial seaweed market, accounting for 91.63% of total volume in 2025. The strong share of aquaculture is primarily attributed to its ability to ensure consistent supply, controlled quality, and scalable production compared to wild harvesting. Commercial seaweed farming enables producers to meet rising global demand while reducing dependency on seasonal and environmental variations. Advancements in farming techniques, including rope cultivation and offshore farming systems, have further improved yield efficiency and cost-effectiveness. In addition, government support and investments in sustainable aquaculture practices have encouraged large-scale cultivation across major producing regions. The reliability of aquaculture in supporting industrial applications such as food processing, hydrocolloid extraction, and nutraceutical production continues to reinforce its leading market position.

Wild harvest, on the other hand, is projected to be the fastest-growing cultivation segment, expanding at a CAGR of 9.13% through 2031. Growth in this segment is driven by increasing demand for naturally sourced and minimally processed seaweed, particularly in premium and specialty product categories. Wild-harvested seaweed is often perceived as more natural and environmentally sustainable, which appeals to health-conscious and eco-aware consumers. The segment is also benefiting from growing interest in traditional harvesting practices and artisanal food products. Furthermore, rising demand from niche markets such as organic foods and specialty ingredients is supporting increased harvesting activities.

By Application: Methane Mitigation Fuels Animal Feed Surge

The food and beverages segment accounted for the largest share of the commercial seaweed market in 2025, contributing 61.34% of total revenue. This dominance is primarily driven by the widespread use of seaweed as a functional and nutritional ingredient in a variety of food applications, including snacks, soups, salads, seasonings, and processed foods. Seaweed-derived hydrocolloids such as agar, carrageenan, and alginate are extensively used in food processing as stabilizers, thickeners, and gelling agents, further strengthening segment demand. Increasing consumer preference for plant-based, clean-label, and nutrient-rich food products has also supported higher incorporation of seaweed in mainstream diets.

Animal feed and pet food is projected to be the fastest-growing application segment, registering a CAGR of 9.74% through 2031. The growth is driven by increasing recognition of seaweed as a natural source of minerals, vitamins, and bioactive compounds that support animal health and nutrition. Seaweed-based feed additives are gaining traction due to their potential benefits in improving digestion, enhancing immunity, and reducing methane emissions in livestock production. Rising demand for premium and functional pet food products is also contributing to increased adoption of seaweed ingredients in pet nutrition formulations. Furthermore, growing awareness regarding sustainable and alternative feed resources is encouraging manufacturers to incorporate marine-based ingredients into feed products.

Geography Analysis

In 2025, Asia-Pacific commands a 37.38% market share, capitalizing on its established aquaculture infrastructure and traditional consumption habits. However, the region grapples with challenges like climate change repercussions and rising production costs. China stands at the forefront, harnessing advanced cultivation technologies and integrated processing. Yet, it's not without challenges: environmental regulations and surging labor costs squeeze profit margins. Meanwhile, Japan and South Korea are carving niches in premium product segments. Their focus on technological innovations, such as automated harvesting and value-added processing, ensures they maintain a competitive edge, even with elevated production costs. Indonesia and the Philippines enjoy favorable growing conditions and government backing, but face hurdles like disease outbreaks and quality control issues that hinder their export ambitions.

Europe is on a growth trajectory, boasting a 9.48% CAGR through 2031. This surge is fueled by regulatory endorsements for sustainable packaging and pharmaceutical advancements, tapping into the continent's robust bioprocessing expertise. Nordic nations spearhead Europe's cultivation initiatives. Iceland and Norway are pioneering offshore farming systems tailored for challenging marine environments. In contrast, the Netherlands and Germany are advancing land-based cultivation methods, ensuring year-round yields. The European market's stringent quality and traceability standards command premium pricing, creating entry barriers. Yet, compliant suppliers enjoy lucrative margins. Policymakers are also recognizing seaweed's role in carbon sequestration, weaving it into broader blue economy strategies, solidifying Europe's growth narrative.

North America is making waves, especially in specialty applications and tech innovations. The U.S. is leading the charge, pouring USD 25 million into offshore seaweed biomass ventures and setting up cutting-edge processing hubs in Maine and Alaska. Canada champions sustainable harvesting, forging partnerships with indigenous communities. Meanwhile, Mexico reaps benefits from Ocean Rainforest's strategic takeover of Alamarsa, ushering in advanced cultivation methods to Latin America. With vast coastal territories ripe for cultivation and a burgeoning appetite for natural food ingredients, North America's growth horizon looks promising.

Note: Regional shares of all individual regions will be available upon report purchase

Competitive Landscape

The commercial seaweed market is characterized by a moderately fragmented competitive landscape, with the presence of numerous regional and international players operating across cultivation, processing, and distribution stages. Market participants range from large-scale aquaculture companies to small and medium-sized producers specializing in niche or specialty seaweed products. The diversity of applications across food and beverages, pharmaceuticals, agriculture, and personal care industries has enabled multiple companies to coexist without a single dominant market leader. Regional producers, particularly in Asia-Pacific, maintain strong positions due to established cultivation infrastructure and favorable coastal conditions. At the same time, emerging players are entering the market by focusing on value-added products and sustainable production practices. This fragmentation encourages continuous innovation and product differentiation among competitors.

Competition within the market is largely driven by product quality, pricing strategies, processing capabilities, and access to reliable raw material sources. Companies are investing in advanced cultivation technologies and processing methods to enhance yield, maintain consistency, and meet evolving regulatory standards. Strategic collaborations, partnerships, and long-term supply agreements with food manufacturers and ingredient suppliers have become common approaches to strengthen market positioning. In addition, players are increasingly expanding their product portfolios to include organic, clean-label, and functional seaweed ingredients to cater to changing consumer preferences.

Furthermore, sustainability and environmental responsibility have emerged as key competitive factors shaping the market landscape. Companies are emphasizing eco-friendly farming practices, traceability, and responsible harvesting methods to align with global sustainability goals and regulatory expectations. Investments in research and development are increasing as firms explore new applications for seaweed in biotechnology, nutraceuticals, and agricultural solutions. Smaller companies are gaining market visibility by targeting premium and specialty segments, while larger firms are leveraging economies of scale to strengthen their global presence.

Commercial Seaweed Industry Leaders

Gelymar

Qingdao Bright Moon Seaweed Group

Cargill, Incorporated

CP Kelco Inc.

Acadian Seaplants Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Biotech startup Seadling launched a second processing facility in Malaysia to expand production capacity for fermented seaweed-based functional ingredients used in human and pet nutrition. The expansion followed a seed funding round and aims to strengthen the company’s ability to scale manufacturing of value-added seaweed ingredients. The new facility enhances processing capacity and supports increasing global demand for functional marine-based ingredients.

- August 2025: BPH Global secured trade financing to expand its seaweed operations in Indonesia, including the development of processing capacity at a new warehouse facility in Makassar, South Sulawesi. The expansion is aimed at increasing procurement volumes, strengthening supply chain independence, and supporting export growth. The initiative also strengthens partnerships with local farming communities and improves traceability and sustainability across the supply chain.

- February 2025: Ocean Rainforest acquired a majority stake in Mexican seaweed producer Alamarsa, combining Alamarsa's extraction expertise with Ocean Rainforest's open-ocean farming technology to enhance sustainable seaweed-based products and expand market access in North America.

Global Commercial Seaweed Market Report Scope

Seaweeds are a group of photosynthetic, non-flowering, plant-like organisms (called microalgae) that live in the sea. The commercial seaweed market is segmented by product type, flavor, cultivation method, application, and geography. By product type, the market is segmented into Red, Brown, and Green Seaweed. Based on flavor, the market is segmented into plain and flavored. Based on cultivation method, the market is segmented by aquaculture and wild harvest. Based on application, the market is segmented into food and beverages, dietary supplements, pharmaceuticals, animal feed and pet food, cosmetics and personal care and other applications. Based on geography, the market includes major geographies across the region, North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Brown Seaweed |

| Green Seaweed |

| Red Seaweed |

| Plain |

| Flavored |

| Fresh/Chilled |

| Frozen/Dried |

| Aquaculture (Farmed) |

| Wild Harvest |

| Food & Beverages |

| Dietary Supplements |

| Pharmaceuticals |

| Animal Feed & Pet Food |

| Cosmetics & Personal Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Brown Seaweed | |

| Green Seaweed | ||

| Red Seaweed | ||

| By Flavor | Plain | |

| Flavored | ||

| By Form | Fresh/Chilled | |

| Frozen/Dried | ||

| By Cultivation Method | Aquaculture (Farmed) | |

| Wild Harvest | ||

| By Application | Food & Beverages | |

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Animal Feed & Pet Food | ||

| Cosmetics & Personal Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the seaweed market be by 2031?

The commercial seaweed market size is projected to reach USD 32.98 billion by 2031, growing at an 8.08% CAGR from 2026-2031.

Which seaweed product type is expanding fastest?

Brown seaweed is advancing at a 9.87% CAGR thanks to rising alginate demand in plant-based dairy and wound dressings.

Why is animal feed a high-growth application?

Regulatory pressure to reduce methane emissions drives adoption of Asparagopsis-based supplements, lifting the segment at a 9.74% CAGR.

What region shows the quickest revenue growth?

Europe leads regional growth at a 9.48% CAGR, propelled by the EU’s EUR 1 billion Blue Bioeconomy initiative that funds offshore farms.

How dominant is aquaculture in global supply?

Aquaculture accounts for 91.63% of total volume, satisfying traceability rules and enabling controlled year-round production.

Page last updated on: