Pink Himalayan Salt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

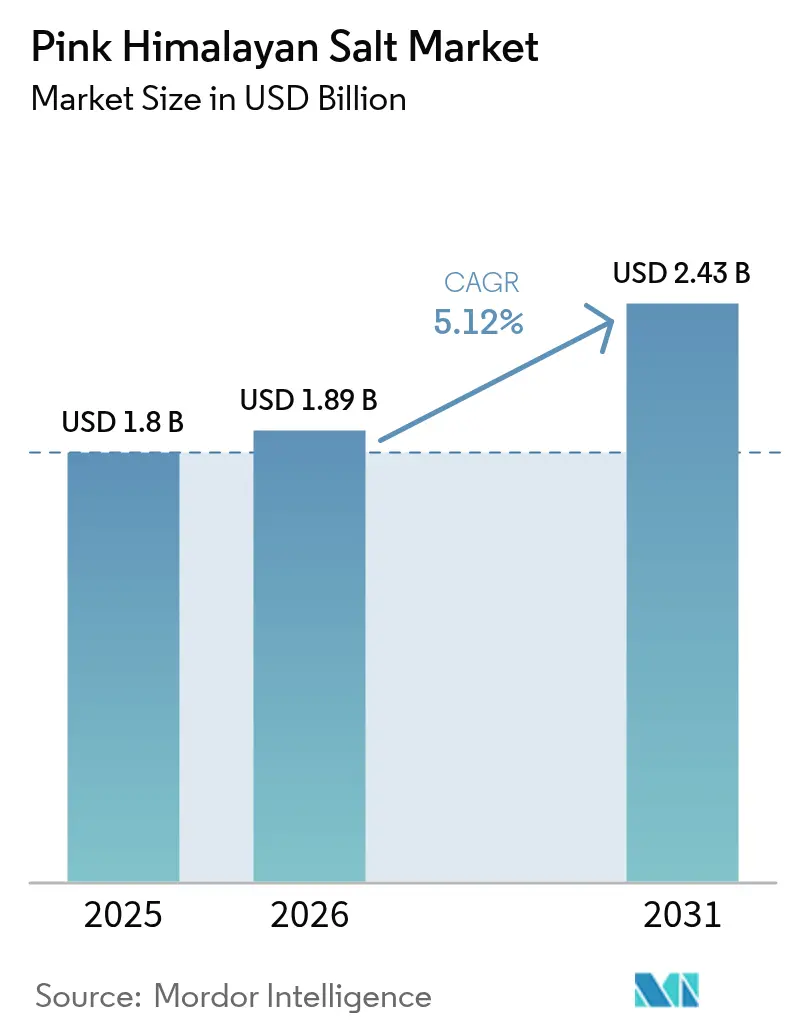

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

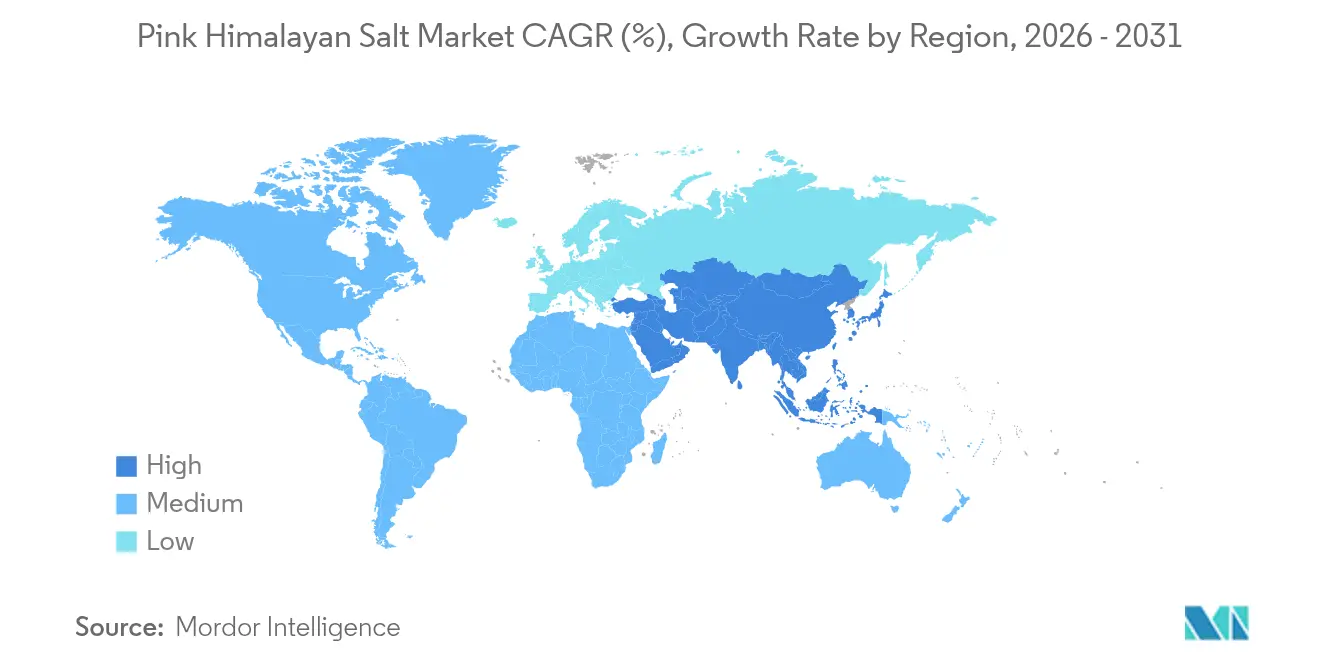

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pink Himalayan Salt Market Analysis by Mordor Intelligence

Pink himalayan Salt market size in 2026 is estimated at USD 1.89 billion, growing from 2025 value of USD 1.80 billion with 2031 projections showing USD 2.43 billion, growing at 5.12% CAGR over 2026-2031. The market demonstrates robust growth as consumers increasingly prioritize minimally processed ingredients and clean-label products in their purchasing decisions. Retailers benefit from premium positioning strategies, which enable them to command higher profit margins. The market expansion is further accelerated by packaged-food manufacturers incorporating pink himalayan salt into their product formulations, mining companies implementing vertical integration strategies to control quality and supply, and the proliferation of e-commerce platforms enhancing product accessibility. While North American consumers continue to demonstrate strong purchasing power in this segment, the Asia-Pacific region emerges as the fastest-growing market, driven by urban households transitioning from traditional table salt to premium condiment options. The competitive landscape remains dynamic, with companies focusing on distinctive branding strategies, rigorous source verification processes, and innovative packaging solutions to differentiate their products, rather than competing on supply availability.

Key Report Takeaways

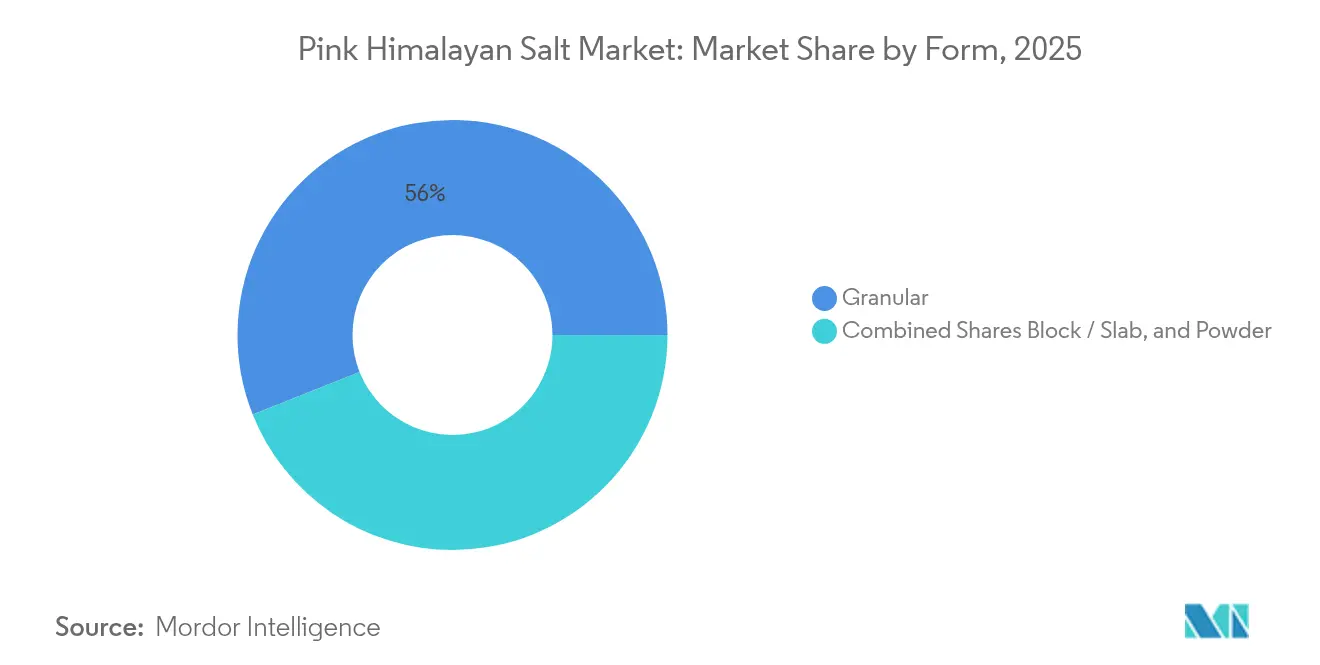

- By form, granular products held 56.02% of the pink himalayan salt market share in 2025, whereas powder products are set to post the fastest 6.28% CAGR through 2031.

- By grade, food-grade salts dominated with 85.62% share in 2025; industrial and animal grades are projected to expand at a 6.17% CAGR between 2026-2031.

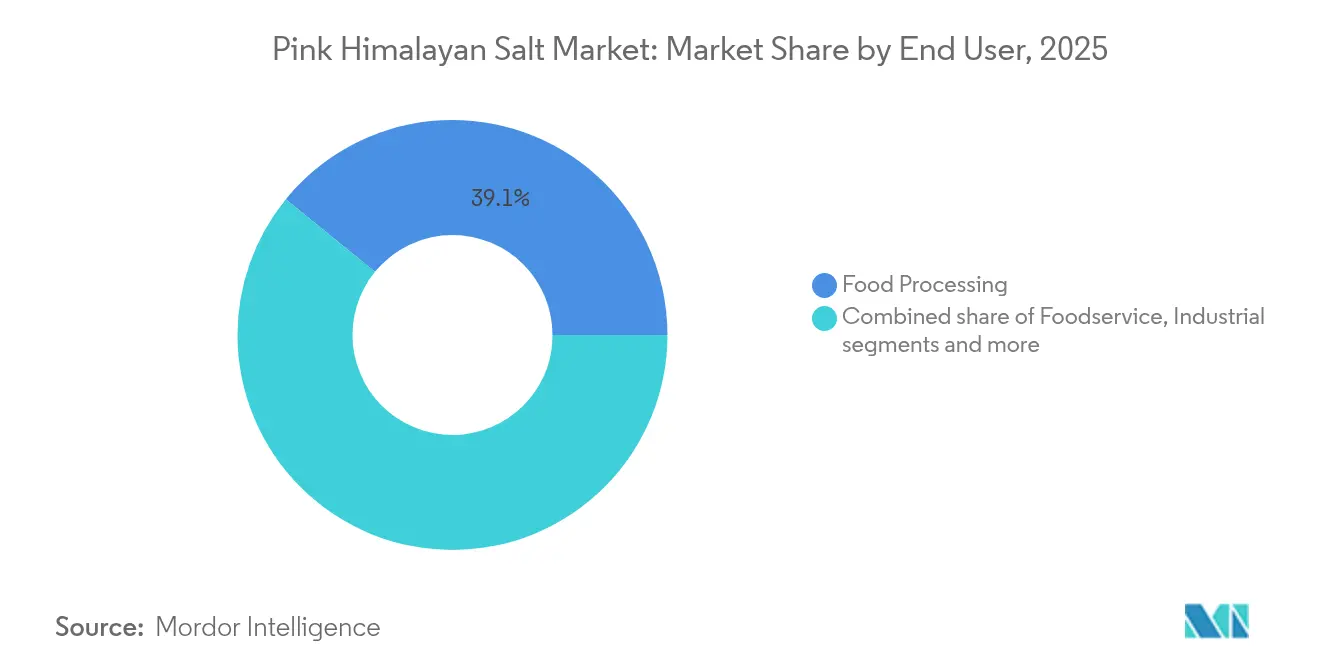

- By end user, food processing accounted for 39.12% share of the pink himalayan salt market size in 2025, while retail channels lead growth at a 6.35% CAGR to 2031.

- By geography, North America led with 31.05% revenue share in 2025; Asia-Pacific is forecast to grow the fastest at a 6.05% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pink Himalayan Salt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium and gourmet food products | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing health consciousness leads consumers to prefer natural, unprocessed salts | +1.5% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Growing preference for organic, clean-label, and eco-friendly products | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expanding innovation in flavor-enhanced and infused salt products | +0.6% | Global, led by North America | Short term (≤ 2 years) |

| Enhanced transparency and traceability in supply chains | +0.4% | Global, regulatory-driven in Europe and North America | Medium term (2-4 years) |

| Popularity of salt-based decorative products | +0.3% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium and Gourmet Food Products

Consumer preferences in the salt industry are evolving as people increasingly consider culinary ingredients part of their lifestyle choices rather than basic necessities. This shift is particularly evident in metropolitan areas, where specialty food retailers have witnessed substantial growth in artisanal salt purchases, driven by urbanization and higher disposable incomes. A notable example is ITC Aashirvaad's launch of himalayan Pink Salt in May 2024 across major Indian cities, which focuses on natural qualities and minimal processing to meet sophisticated consumer demands. The product's adoption by restaurants and culinary professionals for both flavor enhancement and visual appeal has influenced consumer purchasing decisions. This evolution has also reached the beverage and specialty food sectors, where businesses incorporate premium salts into their products to meet market demands and justify higher price points.

Increasing Health Consciousness Leads Consumers to Prefer Natural, Unprocessed Salts

Consumer preferences for health-conscious products are changing salt purchasing patterns, with many buyers moving away from processed table salt. Pink himalayan salt's appeal stems from its minimal processing and trace mineral content, though health claims remain under regulatory scrutiny. The Food and Drug Administration's December 2024 "healthy" claim regulations set specific sodium limits for products, restricting mixed products to 15% of the Daily Value per reference amount [1]Source: U.S. Food & Drug Administration, “Use of the ‘Healthy' Claim on Food Labeling,” fda.gov. These regulations enable pink himalayan salt manufacturers to align their products with compliance requirements while highlighting their natural origin. Research shows consumers increasingly consider mineral-rich salts as functional ingredients rather than basic seasonings, particularly among health-conscious consumers. While overall sodium consumption decreases, premium salt categories benefit as consumers opt to use smaller amounts of higher-priced specialty salts, seeking both enhanced flavor and potential nutritional advantages.

Growing Preference for Organic, Clean-Label, and Eco-Friendly Products

Clean-label initiatives are reshaping ingredient sourcing in the food industry, with pink himalayan salt gaining prominence due to its simple composition and clear origin. The product's natural attributes, including hand-mining and minimal processing, meet consumer demands for pure ingredients. However, regulatory requirements differ across regions. In India, Food Safety and Standards Authority of India regulations require specific front-of-pack disclaimers for products claiming to be "natural" or "pure." Environmental considerations now influence buying decisions, with consumers examining packaging materials, transportation impacts, and mining methods [2]Source: Good Food Institute, “Advertising and Claims,” gfi-india.org. While companies implement sustainable packaging and ethical sourcing practices, maintaining supply chain transparency remains difficult due to the limited geographical source of authentic pink himalayan salt. The organic certification of salt products faces distinct obstacles, as traditional organic standards primarily address agricultural practices rather than mining operations. This regulatory gap has led some producers to pursue alternative third-party sustainability certifications.

Expanding Innovation in Flavor-Enhanced and Infused Salt Products

Product innovation in the pink himalayan salt market is expanding beyond traditional offerings through the development of flavored variants and functional blends that align with changing consumer preferences. Hub Pak Salt Refinery demonstrated this trend at Gulfood 2025 by introducing the Seasoned Pink Salt Shaker in Chicken Salt flavor, targeting specific culinary applications while maintaining the product's premium positioning. Manufacturers are using flavor infusion technologies to create distinct products that combine pink himalayan salt's visual appeal with specific taste profiles. Ultimate Baker's introduction of 12 flavor options, including banana, birthday cake, and cappuccino variants, shows market segmentation toward experiential and artisanal uses. The market is also seeing innovation in packaging, with manufacturers implementing specialized dispensing systems, grinder mechanisms, and portion-controlled formats to enhance user experience and support premium pricing. These developments indicate the market's transition from commodity salt to branded specialty ingredients with specific value propositions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainties related to health claims and labeling | -0.7% | Global, strictest in Europe and North America | Medium term (2-4 years) |

| Stringent food safety and import regulations in key markets | -0.5% | Global, complex in China andIndia | Short term (≤ 2 years) |

| Limited awareness in some emerging markets | -0.4% | Asia-Pacific emerging markets, Latin America | Long term (≥ 4 years) |

| Challenges in maintaining product consistency across suppliers | -0.3% | Global supply chain issue | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainties Related to Health Claims and Labeling

The regulatory framework for pink himalayan salt marketing involves strict compliance requirements, particularly regarding health claims and mineral content declarations. The Food and Drug Administration mandates scientific validation for health-related marketing claims through its structure/function requirements, while its revised "healthy" claim criteria establish specific sodium limits that influence product marketing. In European markets, EFSA implements rigorous assessment procedures for nutrition and health claims, creating a complex regulatory landscape for global marketing operations. Companies must carefully navigate the boundaries between permissible structure/function claims and prohibited disease treatment statements, as violations can result in regulatory actions including warning letters, recalls, and market restrictions. The limited international regulatory alignment requires companies to implement region-specific labeling and marketing strategies, increasing operational costs. Small-scale producers face particular challenges due to limited resources for legal compliance and scientific validation studies.

Stringent Food Safety and Import Regulations in Key Markets

The evolving regulatory landscape in Asian markets presents significant challenges for businesses looking to enter these promising markets. In China, the upcoming GB 2760-2024 food additive standards will require businesses to undergo thorough compliance reviews for salt products with additives, while also obtaining mandatory GACC registration codes to avoid shipment rejections [3]Source: U.S. Department of Agriculture, “China: Usage Standard for Food Additives Finalized,” fas.usda.gov. Similarly, India's FSSAI system demands comprehensive documentation through FICS, with lengthy processing times that can impact business operations. These requirements become more stringent for products with health claims, requiring additional validations. Small businesses find themselves particularly disadvantaged, as they often lack the resources to manage these complex compliance requirements effectively. The frequent and sudden regulatory changes in these markets continue to pose operational risks for both importers and exporters in the specialty salt industry, making it essential for businesses to maintain vigilant compliance monitoring and adaptation strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Granular Dominance Drives Culinary Applications

The pink himalayan salt market demonstrates a clear preference for granular formats, which currently hold 56.02% of the market share in 2025. This substantial market presence reflects the format's versatility and practical benefits across the food industry. Commercial kitchens value its consistent dissolution properties for precise seasoning, while home cooks appreciate its aesthetic appeal when used as a finishing salt. The granular format's widespread adoption in both professional and residential settings has established it as the industry standard.

The powder segment, though smaller in market share, is experiencing remarkable growth with a 6.28% CAGR projected through 2031. This acceleration is primarily driven by changing consumer preferences toward convenience and versatility in food preparation. The powder format's ability to blend seamlessly into smoothies, baked goods, and seasoning mixtures has made it increasingly popular among health-conscious consumers and home bakers. Meanwhile, block and slab formats maintain a specialized position in the market, catering to high-end restaurants and culinary enthusiasts who seek distinctive cooking methods and presentation options for their dishes.

By Grade: Food Grade Supremacy Faces Industrial Diversification

Food grade pink himalayan salt dominates the market with an 85.62% share in 2025, establishing its strong presence as a premium culinary ingredient. The product's superior quality, distinctive pink color, and rich mineral content have made it the preferred choice among consumers and food manufacturers who prioritize natural, high-quality ingredients in their products.

The industrial and animal grade segments are experiencing substantial growth at 6.17% CAGR through 2031, as manufacturers explore new applications beyond traditional food uses. The expansion into pharmaceuticals, cosmetics, and livestock nutrition sectors demonstrates the versatility of pink himalayan salt, with specific mineral content and purity requirements driving demand in these segments. Manufacturers have successfully implemented quality-based differentiation strategies to maximize value across multiple end-use categories while preserving the premium positioning of their food-grade offerings.

By End User: Retail Growth Challenges Food Processing Leadership

Food processing maintains its dominance as the largest end-user segment, capturing a 39.12% market share in 2025. This substantial presence stems from commercial food manufacturers increasingly incorporating pink himalayan salt into their product formulations to meet consumer demands for premium ingredients and clean-label compliance. The manufacturers recognize the value proposition of pink Himalayan salt in enhancing their product portfolios and meeting stringent quality standards.

The retail segment demonstrates remarkable growth potential with a projected CAGR of 6.35% through 2031, signaling a significant transformation in distribution channels. This growth is primarily fueled by the rapid expansion of e-commerce platforms and a sustained increase in home cooking activities. The shift represents a democratization of specialty ingredients, as consumers gain direct access to professional-grade products previously limited to commercial kitchens. Meanwhile, the foodservice sector continues its steady expansion, with restaurants and culinary professionals incorporating pink himalayan salt both for its superior flavor-enhancing properties and its ability to elevate visual presentation in dishes.

Geography Analysis

North America maintains its market leadership with a commanding 31.05% share in 2025. The region's market strength is built on a foundation of sophisticated consumer understanding, deeply rooted premium food culture, and an extensive distribution infrastructure that spans specialty retail and foodservice channels. North American consumers demonstrate a mature appreciation for specialty salt varieties, showing consistent willingness to invest in products that deliver superior quality and tangible health benefits. The region's distribution network efficiency ensures products reach consumers through multiple touchpoints, from high-end specialty stores to mainstream retail outlets.

Asia-Pacific has emerged as the market's primary growth catalyst, recording an impressive 6.05% CAGR through 2031. This remarkable growth trajectory is powered by fundamental shifts in consumer dynamics, including substantial increases in disposable income, accelerated urbanization patterns, and evolving dietary preferences across major economies like China, India, and Japan. The Japanese market exemplifies this transformation, with its sophisticated convenience store networks playing an instrumental role in premium food product distribution. The region's growth story is further strengthened by increasing consumer education about specialty food products and growing appreciation for international culinary influences.

Europe maintains its position with steady growth, characterized by increasing consumer preference for organic and clean-label products. The Middle East and Africa markets demonstrate promising development, leveraging their diverse expatriate communities and robust tourism sectors to drive market expansion. South American markets, while currently showing lower penetration rates, represent significant untapped potential as regional economies continue to develop and consumer awareness strengthens. Success in these diverse markets requires carefully calibrated strategies that address specific local regulations, optimize distribution channels, meet regional packaging requirements, and align with cultural preferences, all while maintaining unwavering product quality standards across all territories.

Competitive Landscape

The pink himalayan salt market demonstrates a highly fragmented competitive landscape, where numerous companies of varying sizes and capabilities actively compete for consumer attention and market share. Large multinational food companies like McCormick & Company operate alongside specialized producers such as SaltWorks Inc., while regional suppliers maintain strong connections to the authentic source - Pakistan's Khewra Salt Mine. This diversity in market participants creates a dynamic environment where companies can establish their unique market positions through different strategies.

The market's competitive dynamics are shaped by distinct operational approaches. Major companies have invested in comprehensive vertical integration strategies, maintaining control over the entire value chain from mining operations to retail distribution channels. In contrast, smaller market participants have found success by focusing on specific market segments, differentiating themselves through organic certification, innovative packaging solutions, and direct-to-consumer sales channels. The integration of blockchain technology has become increasingly important, as companies respond to growing consumer demands for transparency in product authenticity and ethical sourcing practices.

Several untapped opportunities exist within the market, particularly in product innovation and market expansion. Companies are exploring new flavor developments, investigating sustainable packaging solutions, and venturing into non-culinary applications, including decorative products and wellness-focused offerings. The market's current fragmented structure presents significant opportunities for industry consolidation, with well-positioned companies having the potential to strengthen their market presence through strategic acquisitions of smaller, specialized players.

Pink Himalayan Salt Industry Leaders

McCormick & Company Inc.

K+S AG

SaltWorks Inc.

WBM International

San Francisco Salt Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Goyal Salt Limited launched a new product called "Goyal Himalayan Pink Salt." Himalayan Pink Salt, also known as "Sendha Namak" or "Rock Salt," offers several health benefits. The salt aids in digestion, helps reduce gas, acidity, and heartburn. Additionally, it supports the body's water absorption process and helps prevent dehydration.

- January 2024: ITC Aashirvaad launched Himalayan Pink Salt across major Indian metros with no added colors positioning and 1-kilogram pack pricing at INR 120. The launch targets modern trade and e-commerce channels with transparent packaging design.

- January 2024: Salted Perfection launched wholesale site targeting retailers, expanding distribution capabilities for artisanal salt and seasoning products. The initiative follows the company's national distribution partnership with Specialty Food Partners established in 2024.

Global Pink Himalayan Salt Market Report Scope

Pink Himalayan salt is a type of rock salt that is mined from the Khewra Salt Mine in the Punjab region of Pakistan. The salt gets its pinkish hue from trace minerals, such as iron, magnesium, potassium, and calcium, that are present in the salt. Pink Himalayan salt is popular as a healthier alternative to refined table salt because it is less processed and contains more minerals. It is often used in cooking and food preparation, as well as in food presentation, due to its attractive pink color.

Distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retailers, and other distribution channels. The report also analyzes the emerging and established geographical regions by covering regions such as North America, Europe, Asia-Pacific, South America, and Middle East, and Africa.

The report offers market size and forecasts in value (USD million) for the above segments.

| Granular |

| Block/Slab |

| Powder |

| Food Grade |

| Industrial/Animal Grade |

| Food Processing | |

| Foodservice | |

| Industrial | |

| Retail | Supermarket/Hypermarket |

| Convenience Store | |

| Online Retailer | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Form | Granular | |

| Block/Slab | ||

| Powder | ||

| By Grade | Food Grade | |

| Industrial/Animal Grade | ||

| By End User | Food Processing | |

| Foodservice | ||

| Industrial | ||

| Retail | Supermarket/Hypermarket | |

| Convenience Store | ||

| Online Retailer | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the pink Himalayan salt market?

The category is valued at USD 1.89 billion in 2026 and is projected to reach USD 2.43 billion by 2031.

Which region shows the fastest growth for premium pink salt?

Asia-Pacific is expected to record a 6.05% CAGR through 2031, outpacing all other regions.

Which product form leads sales today?

Granular crystals command 56.02% of 2025 revenue thanks to culinary versatility and visual appeal.

Why are retailers gaining momentum?

Direct-to-consumer e-commerce, subscription spice boxes, and influencer recipes are lifting retail segment sales at a 6.35% CAGR.

How will regulation impact marketing claims?

Stricter sodium thresholds in “healthy” labeling and heightened additive standards mean brands must substantiate wellness claims and reformulate packaging for each market.

Page last updated on: