Salts And Flavored Salts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.56 Billion |

| Market Size (2031) | USD 11.19 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Salts And Flavored Salts Market Analysis by Mordor Intelligence

The Salts and Flavored Salts Market size was valued at USD 9.26 billion in 2025 and estimated to grow from USD 9.56 billion in 2026 to reach USD 11.19 billion by 2031, at a CAGR of 3.21% during the forecast period (2026-2031). Market expansion is primarily supported by increasing consumer preference for premium salt products, continuous innovation in developing unique flavored salt combinations, and necessary product reformulations to meet evolving regulatory standards. However, traditional salt segments maintain steady but modest growth patterns. The Asia-Pacific region continues to dominate the market, driven by substantial per-capita sodium consumption, robust food processing industry operations, and a rapidly expanding middle-class consumer base. North American and European markets exhibit strong growth in specialty salt segments, influenced by increasing health consciousness, demand for clean-label products, and growing interest in gourmet cooking. The market dynamics are shaped by weather-dependent production fluctuations and strategic industry consolidation through mergers and acquisitions, while technological advancements in flavor enhancement capabilities continue to unveil new market opportunities.

Key Report Takeaways

- By product type, table salt held 84.65% of the Salts and Flavored Salts Market share in 2025, whereas seasoned variants are forecast to expand at a 4.69% CAGR to 2031.

- By source, rock salt captured 45.12% of the Salts and Flavored Salts Market size in 2025, while naturally harvested alternatives are expected to advance at a 4.49% CAGR through 2031.

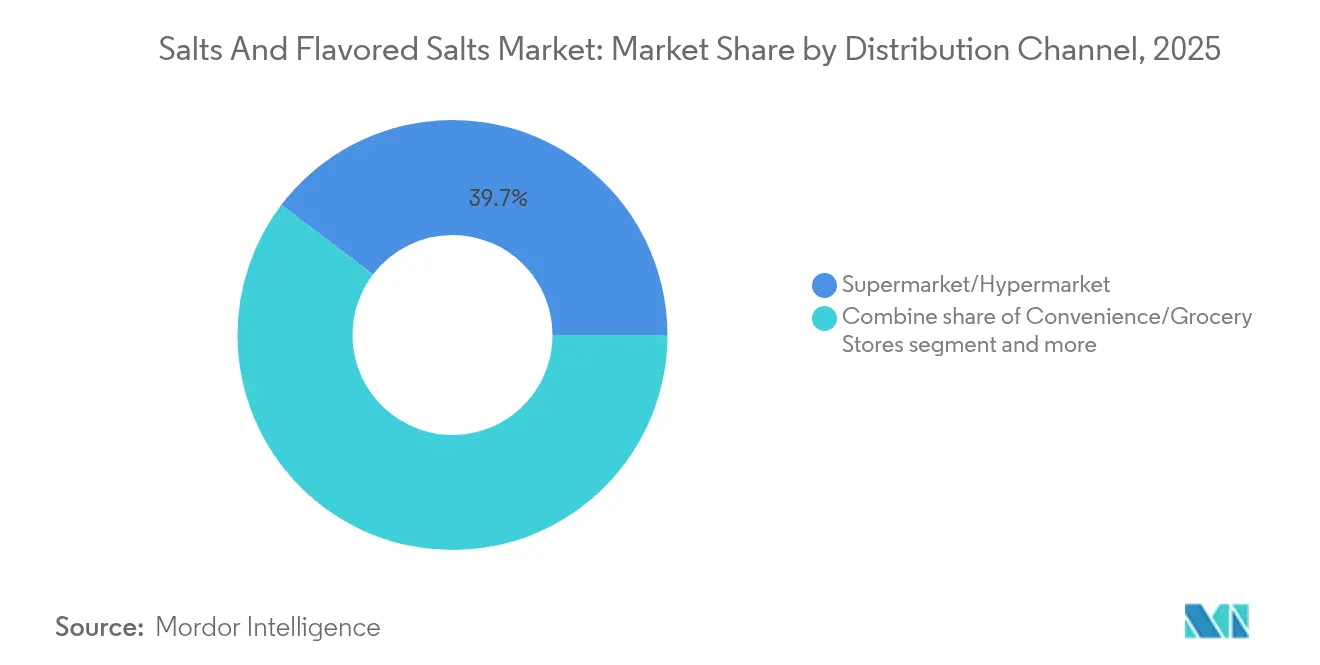

- By distribution channel, supermarket/hypermarket outlets controlled 39.65% of revenue in 2025; online stores are projected to deliver the highest 5.29% CAGR between 2026-2031.

- By geography, Asia-Pacific accounted for 55.72% of global sales in 2025, while the Middle East and Africa region is set to post the fastest 4.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Salts And Flavored Salts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for natural, organic, and clean-label ingredients | +1.2% | Global, with premium focus in North America and Europe | Medium term (2-4 years) |

| Popularity of gourmet and specialty foods | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Increase in global culinary cultural exchange and awareness | +0.7% | Global, accelerated in metropolitan areas | Long term (≥ 4 years) |

| Preference for artisanal, minimally processed products | +0.6% | North America, Europe, affluent Asia-Pacific markets | Medium term (2-4 years) |

| Innovation in low-sodium salt blends and fortified products | +0.5% | Global, regulatory-driven in developed markets | Long term (≥ 4 years) |

| Increase in global culinary cultural exchange and awareness | +0.4% | Emerging markets, food service sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Natural, Organic, and Clean-Label Ingredients

Consumer demand for food transparency is influencing product formulations across food categories, as consumers show willingness to pay higher prices for clean-label products. Salt producers have responded by implementing traceable sourcing protocols and minimal processing methods, particularly for naturally harvested sea salts and rock salts with verified origins. McCormick's 2025 introduction of finishing salts with natural flavor infusions, free from artificial additives, reflects the industry's alignment with clean-label requirements. The FDA's updated voluntary sodium reduction guidelines present dual requirements for clean ingredients and functional reformulation. The combination of health awareness and premium positioning allows salt producers to maintain higher profit margins while meeting consumer demands for ingredient authenticity and minimal processing. The organic products market shows significant expansion, with organic purchases present in over 95% of households last year and an addition of 2 million new buyers. Consumer preference for organic products continues to exceed that of conventional products, primarily driven by younger consumers' value-based purchasing decisions. Market growth stems from increased online and direct-to-consumer sales, alongside retailers expanding their organic product offerings. Despite a slowdown in organic product innovation, with companies adopting more strategic approaches, organic products remain central to the natural products industry in 2025 [1]Source: Naturally Network, "Natural Products Industry Update," naturallynetwork.org.

Popularity of Gourmet and Specialty Foods

Specialty food retailers demonstrated substantial growth in their annual performance, effectively securing their competitive position against traditional grocery retail channels. The fusion of sweet and salty flavors has become increasingly prominent in consumer preferences, with market projections indicating significant expansion in menu offerings through 2027. This evolution has positioned flavored salts as fundamental ingredients, driving innovative culinary applications throughout the food service industry. Premium salt varieties consistently generate substantial price premiums compared to conventional table salt, reflecting strong consumer acceptance and willingness to invest in distinguished flavor experiences and premium-quality ingredients. The market dynamics showcase a clear shift in consumer behavior, where value perception extends beyond basic functionality to encompass enhanced taste experiences and culinary sophistication. This trend has encouraged specialty food retailers to expand their premium salt offerings, capitalizing on the growing consumer appetite for gourmet ingredients and unique flavor profiles.

Increase in Global Culinary Cultural Exchange and Awareness

Southeast Asian flavors continue to establish a strong presence in Western markets, with consumers increasingly embracing Thai, Vietnamese, and Indonesian seasonings characterized by umami-rich salt blends. The influence of social media platforms has transformed how these flavors spread, as viral food content generates immediate market response for innovative seasoning combinations. Traditional Asian fermentation practices are reshaping Western salt manufacturing processes, with companies investing in the development of fermented salt products that deliver enhanced umami profiles. The expansion of global trade networks facilitates broader access to diverse salt varieties, from the mineral-rich Himalayan pink salt to the delicate French fleur de sel, enabling consumers to appreciate the distinct characteristics of regional salt products. The continuous sharing of international culinary experiences through digital platforms sustains market demand for authentic flavor experiences, which premium and specialty salt products effectively deliver to discerning consumers.

Preference for Artisanal, Minimally Processed Products

Artisanal salt producers use traditional harvesting methods and small-batch production processes to differentiate themselves from industrial producers. Their use of solar evaporation and hand-harvesting techniques helps maintain premium market positioning. At the Great Salt Lake, declining water levels create operational challenges for traditional harvesting while increasing the value of naturally produced salts. Consumer preference for minimally processed products has increased demand for salts with distinct textures, mineral profiles, and verified geographic origins. By focusing on sustainable harvesting and environmental preservation, artisanal producers attract environmentally conscious consumers willing to pay premium prices. These producers have developed effective direct-to-consumer sales channels, maintaining profitable margins while building brand relationships through product education. The growing preference for minimally processed foods reflects consumer interest in healthier, natural options and concerns about artificial ingredients. Although processed foods are often considered unhealthy, consumers recognize that some minimal processing can be acceptable. The need for convenience and time savings continues to influence purchasing decisions, making minimally processed ready-to-eat foods important in modern diets. This combination of health consciousness and convenience requirements influences grocery shopping patterns across all income levels [2]Source: The Trustees of Purdue University, "Most Consumers See Processed Foods as Potentially Unhealthy but Buy Them Anyway," ag.purdue.edu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory challenges in flavor formulation and labeling | -0.9% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Safety concerns about artificial additives in certain flavored salts | -0.7% | Global, heightened in developed markets | Medium term (2-4 years) |

| Limited awareness in developing markets for premium salts | -0.6% | Asia-Pacific emerging markets, Africa, Latin America | Long term (≥ 4 years) |

| Environmental impact of salt harvesting practices | -0.5% | Global, regulatory focus in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Challenges in Flavor Formulation and Labeling

The FDA's 2024 voluntary sodium reduction targets present significant operational challenges for flavored salt manufacturers, who must now navigate the intricate process of product reformulation while ensuring their products maintain consumer-preferred taste profiles and necessary shelf stability. In North America, manufacturers face a complex regulatory environment, with Mexico's NOM-051 labeling requirements and Canada's nutritional labeling standards creating distinct compliance obligations in each market. The European Union's comprehensive Farm to Fork strategy introduces additional layers of requirements focused on sustainability and labeling, which directly impact how companies source their salt and maintain processing documentation. These diverse regulatory frameworks across international markets necessitate companies to develop and maintain separate product formulations and implement multiple labeling systems, resulting in increased operational complexity and resource allocation. The situation becomes particularly challenging in the flavored salt category, where manufacturers must ensure their natural flavor declarations align with varying international requirements for ingredient transparency and safety documentation, while meeting local market expectations.

Safety Concerns About Artificial Additives in Certain Flavored Salts

The growing consumer demand for clean-label products is driving reformulation across food categories, particularly in flavored salt varieties that traditionally used synthetic flavor enhancers and preservatives. Research linking artificial colorants and flavor compounds to potential health risks has increased regulatory oversight and consumer concerns, compelling manufacturers to adopt natural alternatives. These natural ingredients often have higher costs and reduced shelf stability. This transition particularly affects mass-market flavored salt products, where artificial additives previously enabled consistent flavor profiles and extended shelf life at competitive prices. The shift to natural ingredients requires substantial research and development investment and typically increases production costs, potentially affecting profit margins or retail prices. Sourcing natural flavor compounds that maintain food safety standards and deliver uniform sensory qualities across production runs has also increased supply chain complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seasoned Variants Drive Premium Growth

Table salt holds an 84.65% market share in 2025, maintaining its essential position across global markets. Its dominance stems from widespread use in food processing operations, diverse industrial applications, and consistent household consumption patterns. The seasoned salt/flavored salt segment demonstrates robust growth potential, advancing at a 4.69% CAGR through 2031, as consumers increasingly seek convenient options and innovative flavor experiences.

McCormick's strategic 2025 product line expansion encompasses 5 new finishing salts, including Balsamic & Herb, Smoky Garlic & Rosemary, and Watermelon Lime, responding to evolving consumer preferences. In the flavored segments, truffle salt and smoked salt variants continue to command premium prices, while garlic salt maintains steady demand across both retail and food service sectors. The market observes notable growth in jalapeño salt and lime-lemon varieties, which align with the emerging "swicy" trend. This flavor profile is projected to experience significant menu growth over the next 4 years, indicating strong potential for increased adoption in restaurant applications.

By Source: Natural Harvesting Gains Premium Positioning

Rock salt maintains its market leadership with a 45.12% share in 2025, building on decades of established mining infrastructure and providing consistent supply reliability for both industrial applications and consumer markets. Natural harvested salt demonstrates remarkable market performance, achieving the highest growth rate at 4.49% CAGR through 2031, as consumers increasingly value products with traceable origins and traditional production methods.

Environmental challenges significantly impact the market dynamics, with the Great Salt Lake's declining water levels creating operational constraints for solar evaporation facilities while simultaneously enhancing the market value of naturally produced varieties. The industry faces additional pressures from heightened environmental scrutiny of mineral salt extraction, particularly concerning ecosystem preservation and water resource management. Recent market disruptions, exemplified by severe winter conditions, compelled American Rock Salt to increase production capacity by 25% through continuous operations, highlighting the infrastructure limitations that affect market stability and pricing mechanisms.

By Distribution Channel: E-Commerce Accelerates Specialty Access

Supermarkets and hypermarkets hold a dominant 39.65% market share in salt distribution in 2025. These retail formats maintain their market leadership through established consumer shopping habits and their ability to offer a wide range of salt products, from basic to premium varieties. The online retail segment is growing at 5.29% CAGR through 2031, driven by the growth of specialty food e-commerce platforms and direct-to-consumer models that increase profit margins for artisanal producers. The U.S. Census Bureau's Quarterly Retail E-Commerce Sales report for Q2 2025 shows e-commerce sales reached 16.3% of total retail sales, a 5.3% increase year-over-year. The online food retail segment expanded due to increased consumer preference for convenience and safety, particularly after the pandemic .

Convenience stores and grocery outlets continue to serve as essential points of access for consumers seeking daily salt purchases while maintaining competitive pricing structures for standard table salt varieties. The market's distribution network is further complemented by specialized channels, including food service providers, industrial suppliers, and specialty gourmet retailers, each serving distinct market segments with specific product requirements and volume demands. Digital platforms have emerged as powerful tools for consumer education and product storytelling, offering advantages that traditional retail environments cannot match. This digital advantage becomes particularly significant in the premium salt category, where factors such as product origin, processing methodologies, and distinct flavor profiles significantly influence consumer purchasing decisions.

Geography Analysis

In 2025, Asia-Pacific is projected to hold a 55.72% share of the global salt market. This dominance is attributed to the region's large population and cultural preference for sodium-rich cuisines. Consumption patterns highlight significant intake levels, with South Korea at 12.3g per day, Singapore at 11.5g, and Thailand at 10.8g. The market is deeply rooted in traditional fermentation practices and umami-focused culinary traditions, driving demand for specialty salt varieties. Additionally, the growing middle-class populations in India, Indonesia, and Southeast Asia present opportunities for premium products. However, there is a clear urban-rural divide, as specialty salt products primarily cater to urban areas with higher purchasing power.

The Middle East and Africa region is expected to achieve a robust compound annual growth rate (CAGR) of 4.38% through 2031. This growth is fueled by expanding food processing capabilities, urbanization, and increased cultural exchange through tourism. Key markets such as the UAE, Saudi Arabia, and South Africa are witnessing shifts in consumer preferences and rising prosperity, which support demand for premium salt products. Traditional preservation methods and spice-rich culinary practices in the region align well with flavored salt varieties. Growth is further supported by strategic infrastructure development and improved distribution networks, facilitating the availability of both local and imported salt products.

North America and Europe continue to hold significant positions in the global salt market, despite operating in mature consumption landscapes. These regions are experiencing shifts driven by regulatory measures, such as the FDA's sodium reduction guidelines and the EU's sustainability standards. These regulations encourage innovation in low-sodium alternatives and clean-label products. The premium segment remains strong, with consumers willing to pay 300-500% more for artisanal and specialty salts that offer unique flavor profiles and transparent sourcing practices.

Competitive Landscape

The salt market demonstrates moderate concentration, characterized by a diverse competitive landscape where established multinational companies operate alongside regional specialists and artisanal producers. These companies compete across various price segments and applications, each targeting specific market niches and consumer preferences. The industry structure reflects a balance between large-scale industrial production and specialized local manufacturing capabilities.

Industry consolidation has become increasingly prominent, as evidenced by Stone Canyon Industries' significant USD 3.2 billion acquisition of K+S Americas' salt business, which included Morton Salt operations. This trend continues with Compass Minerals attracting attention from potential buyers such as Koch, Rio Tinto, Cargill, and private equity firms, despite facing challenges with its USD 868.8 million debt burden and operational issues. The market's technological landscape varies considerably, with larger companies investing in advanced processing innovations like Cargill's Potassium Pro Ultra Fine technology for sodium reduction, while smaller artisanal producers maintain their focus on traditional production methods and direct consumer engagement.

The industry presents several growth opportunities, particularly in developing fermentation-enhanced salt varieties, implementing AI-assisted flavor development, and creating sustainable packaging solutions that address environmental concerns while ensuring product quality and stability. Innovation continues to shape the market, as demonstrated by companies like Kirin Holdings, which introduced the Electric Salt Spoon at CES 2025. This technology utilizes electrical current to enhance perceived saltiness without increasing sodium content, potentially revolutionizing how consumers interact with salt products.

Salts And Flavored Salts Industry Leaders

-

Morton Salt Inc.

-

McCormick & Company Inc.

-

K+S AG

-

SaltWorks Inc.

-

Tata Consumer Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: McCormick has launched a new range of finishing salts designed to enhance flavor and texture in cooking. These premium salts include unique varieties that cater to diverse culinary tastes, providing home cooks with easy-to-use options for elevating dishes with a professional touch. The launch reflects growing consumer interest in gourmet seasoning.

- August 2024: Lawry's unveiled four new offerings: Jerk Seasoning, Seasoned Cajun, Salt & Pepper Vinegar, and Hot Garlic Parmesan. These blends promise rich flavors and premium ingredients, perfect for enhancing chicken, seafood, potatoes, vegetables, and more, all without MSG (monosodium glutamate).

- May 2024: ITC Limited, through its Aashirvaad brand, launched Himalayan Pink Salt. Aashirvaad's variant is free from added colors and is packed with essential minerals like calcium and magnesium.

Global Salts And Flavored Salts Market Report Scope

Salts and flavored salts encompass both natural and processed sea salts, which may or may not have added flavorings, and are utilized in a variety of food and beverage products.

The global salts and flavored salts market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into table salt and seasoned and flavored salt. By seasoned and flavored salt, the market is further segmented into truffle salt, garlic salt, lime and lemon salt, smoked salt, jalapeno salt, and others. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. The market is divided based on geography into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Table Salt | |

| Seasoned Salt/Flavored Salt | Truffle Salt |

| Garlic Salt | |

| Lime and Lemon Salt | |

| Smoked Salt | |

| Jalapeño Salt | |

| Others |

| Mineral |

| Rock |

| Naturally Harvested |

| Supermarket/Hypermarket |

| Convenience/Grocery Stores |

| Online Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Table Salt | |

| Seasoned Salt/Flavored Salt | Truffle Salt | |

| Garlic Salt | ||

| Lime and Lemon Salt | ||

| Smoked Salt | ||

| Jalapeño Salt | ||

| Others | ||

| By Source | Mineral | |

| Rock | ||

| Naturally Harvested | ||

| By Distribution Channel | Supermarket/Hypermarket | |

| Convenience/Grocery Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Salts and Flavored Salts Market?

The market was worth USD 9.56 billion in 2026 and is forecast to exceed USD 11.19 billion by 2031.

Which region generates the largest demand?

Asia-Pacific contributes 55.72% of global revenue, reflecting high sodium usage and large food-processing volumes.

Which product segment is growing fastest?

Seasoned and flavored salts are projected to expand at a 4.69% CAGR through 2031, outpacing plain table salt.

How are online channels influencing sales?

Online stores are forecast to post a 5.29% CAGR, enabling long-tail assortment and direct-to-consumer sales for artisanal brands.

What technological innovations are shaping the industry?

Advances include potassium-based low-sodium formulations and electro-sensory devices like Kirin’s Electric Salt Spoon that enhance taste perception without extra sodium.

Page last updated on: