Low Sodium Sea Salt Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

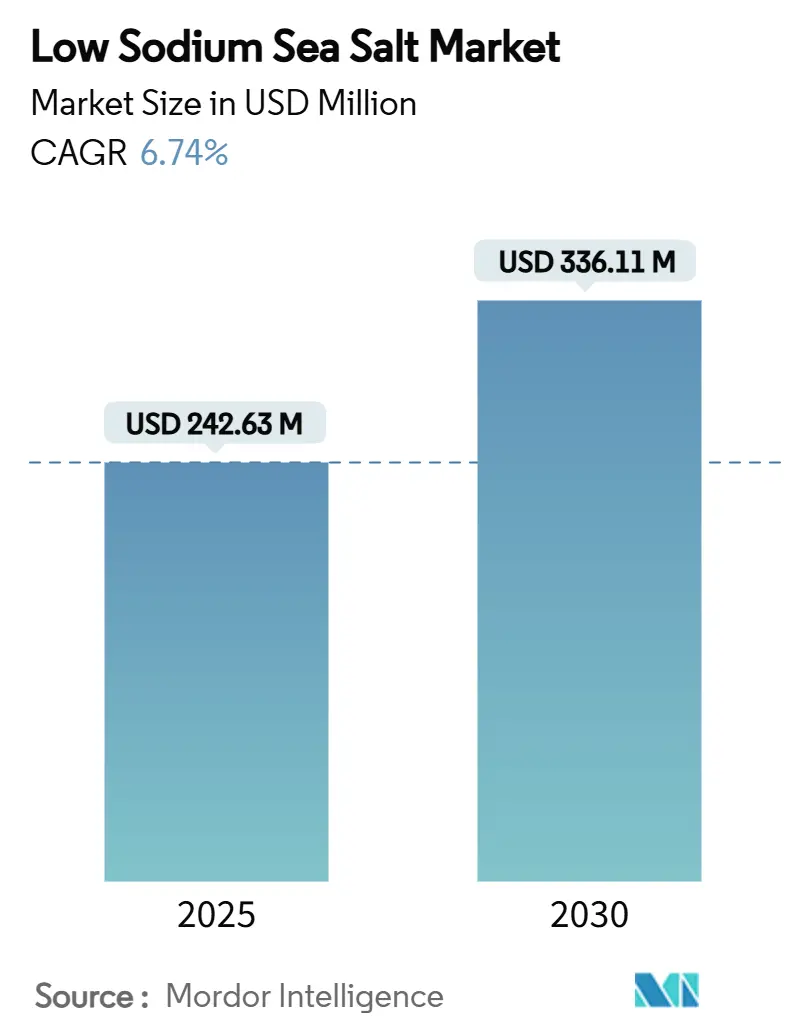

| Market Size (2025) | USD 242.63 Million |

| Market Size (2030) | USD 336.11 Million |

| Growth Rate (2025 - 2030) | 6.74% CAGR |

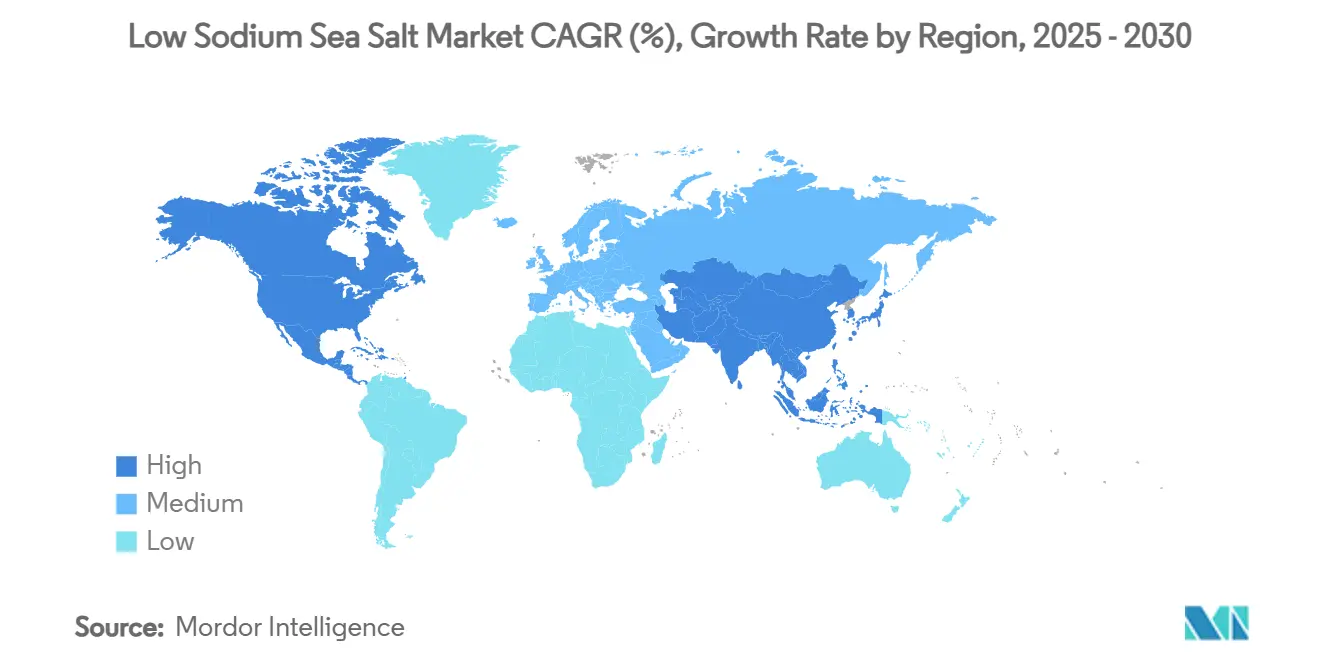

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Low Sodium Sea Salt Market Analysis by Mordor Intelligence

The Low Sodium Sea Salt Market size is estimated at USD 242.63 million in 2025, and is expected to reach USD 336.11 million by 2030, at a CAGR of 6.74% during the forecast period (2025-2030). This growth trajectory reflects the market's critical role in addressing the 1.9 million annual deaths attributed to excessive sodium intake, as highlighted by the WHO's 2025 guidelines on lower-sodium salt substitutes [1]Source: World Health Organization, "Launch of the WHO guideline on the use of lower-sodium salt substitutes", who.int. The FDA's Phase II voluntary sodium reduction targets, aiming to lower average intake to 2,750 mg per day, create substantial reformulation opportunities for food manufacturers seeking potassium-based alternatives[2]Source: U.S. Food and Drug Administration, "Milestone in Sodium Reduction Efforts, Issues Draft Guidance with Lower Target Levels for Certain Foods", fda.gov. The market includes a variety of product types, formulations, and applications, with food seasoning remaining the dominant segment due to its wide usage in processed and packaged foods. Innovation is ongoing with new low-sodium salt alternatives enriched with essential minerals to address concerns about nutrient deficiencies from reduced sodium consumption. Packaging innovations and convenience-focused formats also contribute to market expansion. However, the market faces challenges such as maintaining product taste and texture, possible price premiums of specialized low sodium salts, and supply chain complexities. Overall, the outlook for the low sodium salt market is positive, supported by evolving consumer lifestyles, regulatory support, and ongoing product innovation to meet health and taste expectations.

Key Report Takeaways

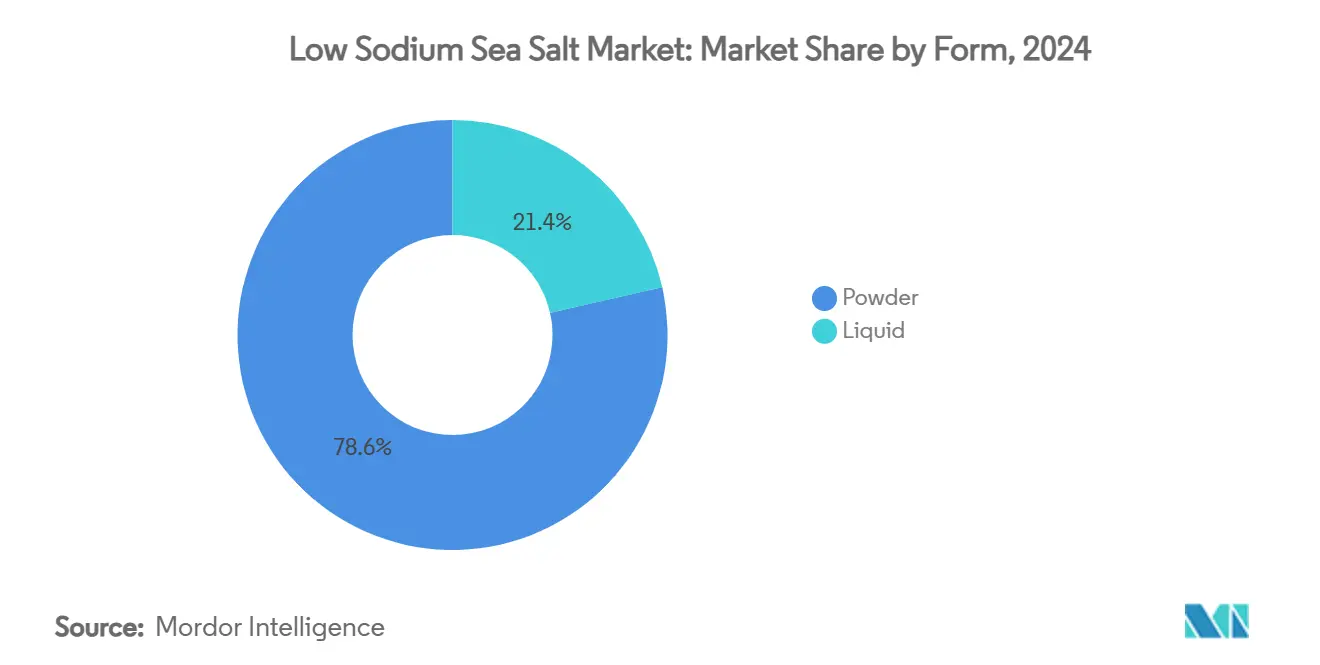

- By form, powder led with 78.56% of the low sodium sea salt market share in 2024; liquid variants are projected to expand at 8.31% CAGR through 2030.

- By flavor, plain variants captured 86.77% of total revenue in 2024 and flavored options are on track for a 7.43% CAGR up to 2030.

- By category, conventional products held 83.41% of the low sodium sea salt market size in 2024, while organic lines are forecast to advance at 8.39% CAGR between 2025-2030.

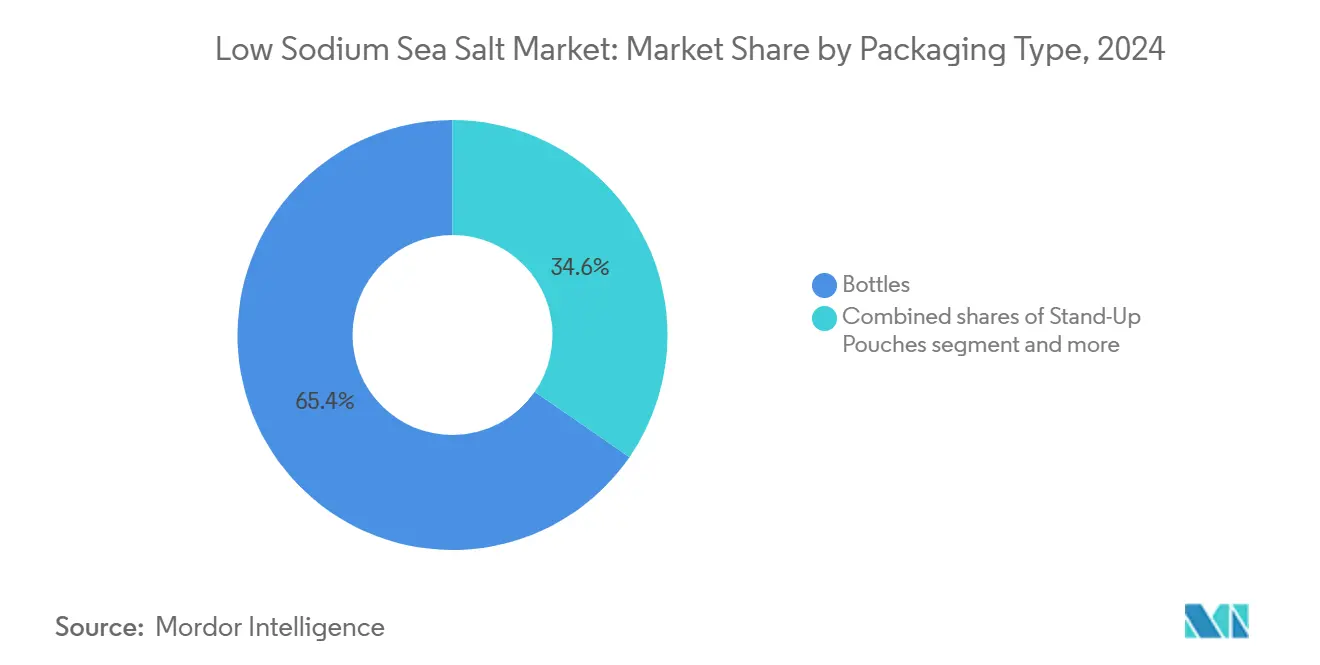

- By packaging type, bottles maintained 65.38% share of the low sodium sea salt market size in 2024, while stand-up pouches are projected to grow at 7.24% CAGR during 2025-2030.

- By distribution channel, off-trade/retail commanded 70.46% revenue in 2024; on-trade/foodservice adoption is set to accelerate at 7.64% CAGR to 2030.

- By geography, Asia-Pacific accounted for 35.63% of global sales in 2024, whereas North America is poised for the fastest 6.82% CAGR through 2030.

Global Low Sodium Sea Salt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Hypertension and Cardiovascular Diseases | +1.5% | Global, with highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Global Sodium Reduction Initiatives and Regulations | +1.2% | Global, led by WHO/FDA guidance in developed markets | Medium term (2-4 years) |

| Clean-Label Movement | +0.8% | North America & European Union, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Technological Advances in Salt Processing | +0.9% | Global, with innovation centers in North America and Europe | Long term (≥ 4 years) |

| Increasing Popularity of Organic and Specialty Food Retail | +0.6% | North America & European Union, premium segments in Asia-Pacific | Short term (≤ 2 years) |

| E-commerce Expansion | +0.4% | Global, accelerated in post-pandemic digital adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hypertension and Cardiovascular Diseases

Hypertension affects 28% of Korean adults and contributes to 10.8 million cardiovascular deaths globally, creating unprecedented demand for dietary sodium reduction solutions. Furthermore, according to BAPPENAS (Ministry of National Development Planning, Republic of Indonesia), the Projected number of people suffering from heart diseases in Indonesia rose from 5.75 million in 2020 to 6.23 million in 2024 [3]Source: BAPPENAS (Ministry of National Development Planning, Republic of Indonesia-UNICEF), "People suffering from heart diseases in Indonesia", unicef.org. The WHO's 2023 global hypertension report emphasizes potassium-enriched salt substitutes as affordable interventions to combat high salt consumption, particularly in low- and middle-income countries where sodium intake exceeds 5 grams daily. China's average daily salt intake of 10.5 grams, more than double the WHO target, positions salt substitutes as critical public health tools, with studies indicating potential prevention of 450,000 cardiovascular deaths through potassium chloride adoption. This health burden drives institutional procurement policies and consumer behavior shifts toward lower-sodium alternatives. The disease burden among youth aged 15-39 increased 36.11% from 1990 to 2021, expanding the addressable market beyond traditional elderly demographics. Healthcare cost considerations further amplify adoption, with every dollar spent on sodium reduction potentially saving USD 12 in healthcare expenses.

Global Sodium Reduction Initiatives and Regulations

The WHO's January 2025 guideline launch on lower-sodium salt substitutes provides authoritative endorsement for potassium-based alternatives, recommending adults reduce sodium intake below 2,000 mg daily while considering salt substitute adoption. PAHO's regional sodium reduction targets mandate 30% intake reduction by 2025, creating regulatory pressure across 35 member countries. The FDA's Phase II voluntary sodium reduction goals target 163 food categories, aiming to lower average intake to 2,750 mg daily—still above recommended levels but representing significant reformulation opportunities. Portugal's mandatory salt targets for bread and voluntary food industry agreements demonstrate successful policy implementation models that other nations increasingly adopt. Regulatory harmonization across jurisdictions creates scalable market opportunities for compliant salt substitute technologies. The FDA's proposed amendments to standards of identity for salt substitutes in standardized foods signals regulatory evolution toward mainstream acceptance.

Clean-Label Movement

Consumer demand for recognizable ingredients drives 60% of Americans to scrutinize ingredient lists, with the "free-from" foods market projected to reach USD 899 million. European natural food additives market growth reflects health-conscious consumption patterns and regulatory preferences for natural alternatives over synthetic ingredients according to the CBI. Tata Consumer Products' 31% growth in value-added salt portfolio demonstrates premiumization opportunities within clean-label positioning, with products like Tata Salt Iron Health addressing micronutrient deficiencies through natural fortification. Sea salt and potassium chloride blends enhance consumer perception compared to standalone potassium chloride, enabling premium pricing strategies while maintaining clean-label credentials. The movement extends beyond ingredient simplification to encompass sustainability concerns, with 68% of salt packaging now recyclable and companies pursuing zero-waste manufacturing targets . Plant-based meat alternatives increasingly adopt potassium chloride for sodium reduction without compromising taste profiles, expanding addressable market segments.

Technological Advances in Salt Processing

MicroSalt's patented microparticle technology delivers 50% sodium reduction while maintaining flavor intensity, representing breakthrough innovation in salt substitute functionality. Hydroextraction techniques achieve 99.87% NaCl purity for pharmaceutical applications, addressing quality standardization challenges that previously limited industrial adoption. Cargill's patent-pending compacting technology for FlakeSelect Potassium Chloride/Sea Salt creates low bulk density particles with enhanced solubility and blendability, solving traditional processing limitations. Enzyme technology advances enable solvent-free flavor ester production, enhancing taste profiles in reduced-sodium formulations without artificial additives. Pressurized carbon dioxide treatment for salt-reduced fish sauce demonstrates innovative processing methods that maintain sensory qualities while achieving significant sodium reduction. These technological convergences enable food manufacturers to achieve sodium reduction targets without compromising product functionality or consumer acceptance, accelerating mainstream adoption across diverse food categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adulteration and Quality Concerns | -0.7% | Global, particularly in emerging markets with weak regulatory oversight | Medium term (2-4 years) |

| Competition from Alternative Salt Substitutes | -0.5% | North America & European Union, where innovation in sodium reduction is highest | Long term (≥ 4 years) |

| Supply Chain Challenges | -0.4% | Global, with acute impacts in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Limited Market Education and Marketing Efforts | -0.3% | Emerging markets and rural areas with low health awareness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adulteration and Quality Concerns

FDA warning letters to food ingredient suppliers highlight persistent quality control failures, with High Quality Organics receiving citations for inadequate supply-chain controls and failure to implement risk-based programs for raw materials. Potassium chloride safety concerns, particularly hyperkalemia risks for individuals with chronic kidney disease, require careful labeling and medical supervision, limiting addressable market segments. The USDA's 2024 technical report on calcium chloride handling establishes organic certification standards, but enforcement gaps across global supply chains create quality inconsistencies. Consumer trust erosion from adulteration incidents affects premium positioning strategies, particularly for organic and specialty salt substitute categories. Regulatory harmonization challenges across jurisdictions complicate quality assurance protocols for multinational food manufacturers. The complexity of potassium labeling requirements, including mandatory warnings for products exceeding 975 mg daily doses, creates compliance burdens that smaller manufacturers struggle to navigate according to the U.S. Food and Drug Administration.

Competition from Alternative Salt Substitutes

One significant restraint facing the global low sodium sea salt market is the limited market education and marketing efforts. Despite growing consumer interest in healthier dietary options, many potential buyers remain unaware of the benefits and availability of low sodium sea salt products. Insufficient promotional activities and lack of clear, accessible information result in low consumer understanding about how these products can help reduce sodium intake without compromising taste. This gap in education hampers broader adoption, especially in regions where traditional salts dominate or where health awareness campaigns are less prevalent. Consequently, manufacturers and marketers face challenges in driving mass-market penetration and need to invest more in targeted communication strategies and awareness programs to effectively convey the value proposition of low sodium sea salts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Variants Gain Processing Advantages

Powder forms command 78.56% market share in 2024, reflecting established manufacturing processes and consumer familiarity with granulated salt substitutes across both retail and foodservice applications. However, liquid alternatives accelerate at 8.31% CAGR through 2030, driven by enhanced solubility characteristics and uniform distribution capabilities in processed food manufacturing. Cargill's Potassium Pro Ultra Fine Potassium Chloride exemplifies powder innovation, offering faster dissolution and smoother mouthfeel that addresses traditional texture limitations in seasoning applications. The liquid segment benefits from growing adoption in meat processing, where injectable brines enable precise sodium reduction without compromising yield or texture properties.

Food manufacturers increasingly flavor liquid formulations for automated processing systems, where consistent dosing and mixing capabilities reduce production variability. Pressurized carbon dioxide treatment technologies enable liquid salt substitute production with enhanced microbial quality and extended shelf life, particularly relevant for sauce and condiment applications. The powder segment maintains dominance through cost advantages and established supply chains, though particle size innovations and compacting technologies address traditional functionality gaps. Liquid growth acceleration reflects industrial food processing trends toward precision ingredient delivery and automated manufacturing systems.

By Flavor: Flavored Variants Drive Premiumization

Plain substitutes retained 86.77% share during 2024, their neutral profile serving as a blank canvas for reformulation across hundreds of product categories. Flavored alternatives surge at 7.43% CAGR through 2030, capitalizing on consumer demand for variety and enhanced sensory experiences in sodium-reduced products. Tata Consumer Products' relaunch of Sendha+ rock salt in the mass premium segment demonstrates successful flavor differentiation strategies that command higher margins while addressing health concerns. The flavored segment benefits from clean-label positioning, incorporating herbs, spices, and natural flavor enhancers that mask potassium chloride's inherent bitterness. While plain variants will maintain volume leadership, sensory innovation is turning flavored options into income drivers, injecting price elasticity into what was once a commoditized corner of the Salt substitute market.

Innovation in enzyme-enhanced flavor production enables sophisticated taste profiles without artificial additives, supporting premium positioning strategies. Plain variants maintain market leadership through versatility across diverse food applications and lower production costs that enable mass market penetration. The flavor segment's growth trajectory reflects broader food industry premiumization trends and consumer willingness to pay higher prices for enhanced sensory experiences. Regulatory approval processes for flavored variants create barriers to entry that benefit established players with extensive R&D capabilities and regulatory expertise.

By Category: Organic Acceleration Reflects Clean-Label Trends

Conventional low sodium sea salt maintain 83.41% market share in 2024, supported by established manufacturing infrastructure and cost advantages that enable mass market accessibility. Organic variants accelerate at 8.39% CAGR through 2030, driven by premiumization trends and consumer preference for natural ingredients free from synthetic processing aids. The USDA's 2024 technical report on calcium chloride establishes organic certification pathways for non-sodium salt substitutes, expanding addressable market opportunities for certified producers. Tata Consumer Products' 31% growth in value-added salt portfolio demonstrates successful organic positioning strategies that capture premium pricing while addressing health and wellness trends.

European natural food additives market growth reflects regulatory preferences for organic alternatives and consumer willingness to pay premium prices for certified products according to the CBI. Conventional products retain dominance through price competitiveness and broader distribution reach, particularly in emerging markets where cost sensitivity limits organic adoption. The organic segment's acceleration reflects broader sustainability concerns and clean-label movement momentum across developed markets. Certification costs and supply chain complexity create barriers that favor larger manufacturers with integrated operations and regulatory expertise.

By Packaging Type: Stand-Up Pouches Transform Convenience

Bottles command 65.38% market share in 2024, leveraging consumer familiarity and established retail merchandising systems across global markets. Stand-up pouches accelerate at 7.24% CAGR through 2030, driven by convenience advantages and sustainability benefits that appeal to environmentally conscious consumers. Morton Salt's introduction of 20-pound standup pouches for water softener salt demonstrates successful packaging innovation that addresses consumer feedback regarding traditional bag handling difficulties. JOZO's 100% recyclable polypropylene salt shaker design reflects European regulatory requirements for packaging recyclability by 2030, creating competitive advantages for sustainable packaging solutions.

The stand-up pouch market projects growth, driven by food industry growth and consumer preference for convenient packaging formats. Jar packaging maintains steady market presence through premium positioning and reusability characteristics that appeal to quality-conscious consumers. Bottle dominance reflects established supply chains and cost advantages, though sustainability concerns increasingly favor alternative packaging formats. Innovation in flexible packaging technologies enables enhanced barrier properties and extended shelf life, supporting market expansion across diverse geographic regions.

By Distribution Channel: Foodservice Adoption Accelerates

Off-trade retail channels dominate with 70.46% market share in 2024, leveraging established consumer purchasing patterns and extensive distribution networks across global markets. On-trade foodservice adoption accelerates at 7.64% CAGR through 2030, driven by institutional sodium reduction policies and menu reformulation initiatives across restaurants and healthcare facilities. Amazon's achievement of over USD 100 billion in grocery sales demonstrates e-commerce expansion within retail channels, with everyday essentials representing one-third of units sold. Supermarkets and hypermarkets maintain distribution leadership through product visibility and consumer education opportunities at point of sale.

Convenience stores and online retail channels capture growing market share through accessibility advantages and subscription-based purchasing models that ensure consistent product availability. Foodservice growth acceleration reflects institutional procurement policies that prioritize health outcomes and regulatory compliance over cost considerations. The distribution landscape increasingly favors omnichannel strategies that integrate physical and digital touchpoints to maximize market reach. Supply chain optimization becomes critical as distribution channels diversify and consumer expectations for product availability and convenience continue to escalate across all market segments.

Geography Analysis

Asia-Pacific commands 35.63% market share in 2024, driven by high baseline sodium consumption patterns and government health initiatives that create substantial reformulation opportunities across the region's massive food processing industry. Indonesia's urgent sodium reduction needs, highlighted by Ajinomoto's advocacy for salt substitute adoption, demonstrate regional commitment to addressing cardiovascular disease burdens through dietary interventions. The region benefits from established manufacturing infrastructure and cost advantages that enable mass market penetration, while growing middle-class populations drive demand for health-oriented food products. Australia's stakeholder research reveals barriers to potassium-enriched salt scaling, including low consumer awareness and food industry hesitancy, suggesting significant untapped market potential once education and regulatory support improve. Vietnam's research on free L-glutamate demonstrates regional innovation in sodium reduction approaches that complement traditional salt substitute strategies.

North America emerges as the fastest-growing region at 6.82% CAGR through 2030, propelled by aggressive FDA sodium reduction initiatives and institutional foodservice adoption that creates scalable market opportunities. The FDA's Phase II voluntary targets aim to reduce average sodium intake to 2,750 mg daily, creating regulatory momentum that favors salt substitute adoption across 163 food categories. Morton Salt's USD 3.2 billion acquisition by Stone Canyon Industries Holdings reflects consolidation trends that enhance distribution capabilities and market penetration. The region's growth acceleration benefits from advanced food processing infrastructure and consumer willingness to pay premium prices for health-oriented products. E-commerce expansion, exemplified by Amazon's grocery dominance, creates new distribution pathways that bypass traditional retail limitations and enable direct-to-consumer marketing strategies.

Europe maintains steady market presence through established regulatory frameworks and consumer health consciousness that supports premium salt substitute adoption across diverse national markets. The European natural food additives market growth reflects regulatory preferences for natural alternatives and sustainability concerns that favor clean-label low sodium sea salt positioning according to the CBI. Portugal's successful implementation of mandatory salt targets for bread and voluntary food industry agreements provides replicable policy models for other European nations seeking sodium reduction outcomes according to the World Health Organization. The region's market development reflects mature regulatory environments and consumer sophistication that enables premium positioning strategies for innovative low sodium sea salt technologies.

Competitive Landscape

The low sodium sea salt market exhibits moderate concentration, characterized by established multinational players leveraging vertical integration advantages while emerging technology disruptors challenge traditional formulation approaches. Cargill dominates through comprehensive potassium chloride production capabilities and patent-pending compacting technologies that create differentiated product offerings like FlakeSelect® Potassium Chloride/Sea Salt blends. Technology-driven differentiation emerges as competitive advantage, with MicroSalt's patented microparticle technology delivering 50% sodium reduction without flavor compromise, securing GBP 3.1 million IPO funding for commercialization.

Leading brands such as Stone Canyon Industries, Selina Naturally, A&B Ingredients, Inc, Birdee Group, etc. dominate the market by offering premium, natural, and sustainably harvested low sodium sea salt products. These companies cater to a growing health-conscious consumer base seeking natural alternatives with reduced sodium content, often focusing on clean-label and mineral-enriched formulations to differentiate their offerings. Geographic diversity is notable, with strong market presences in North America, Europe, and Asia-Pacific, where a combination of rising health awareness and regulatory drivers supports demand growth.

These companies compete across various product types including granules, flakes, and sprays, as well as through multiple distribution channels such as supermarkets, specialty stores, and rapidly growing online retail platforms. Innovation, particularly around organic and seaweed-enriched variants, packaging convenience, and functional benefits, plays a critical role in maintaining competitive advantage. However, the market also faces competitive pressure from alternative salt substitutes like potassium chloride-based salts, which may offer cost or health benefits appealing to some consumers. Overall, the competitive landscape is dynamic, with ongoing product development, regional expansion, and marketing efforts shaping market leadership and growth trajectories in the coming years.

Low Sodium Sea Salt Industry Leaders

-

Tata Consumer Products Limited

-

Stone Canyon Industries

-

Selina Naturally

-

A&B Ingredients, Inc

-

Birdee Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Cornish Sea Salt rolled out its latest offering, TekSalt, enabling users to reduce sodium intake without sacrificing taste. TekSalt, crafted to help food manufacturers tackle the challenge of reducing sodium while enhancing flavor, is a minerally-balanced sea salt. Infused with Celtic sea minerals and electrolytes, TekSalt boasts a lower sodium content yet delivers a robust salty punch.

- January 2024: Tekcapital Plc, announced that MicroSalt Inc is successfully broadening its low-sodium offerings. MicroSalt shakers have now made their debut on Amazon UK. In a strategic move to support this regional growth, Reliable Express, based in Southampton, has been appointed for local distribution across the UK. Their role encompasses not just the distribution, but also the storage of its bulk-packed products, catering to the burgeoning B2B demand in both the UK's food distribution and manufacturing sectors, as well as extending their reach into the EU markets.

- February 2023: Tekcapital Plc announced that MicroSalt had entered into a strategic alliance with US Salt LLC (“US Salt”) for the distribution and delivery of MicroSalt’s low-sodium solutions. The alliance was anticipated to significantly impact both companies, bolstering their positions as leaders in the sodium reduction movement. Additionally, it aimed to expand MicroSalt's customer base and enhance US Salt's product offerings with healthier, lower-sodium alternatives.

Global Low Sodium Sea Salt Market Report Scope

| Powder |

| Liquid |

| Plain |

| Flavored |

| Organic |

| Conventional |

| Stand-Up Pouches |

| Bottles/Salt Sprinkler/Sprays |

| Jars |

| On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Form | Powder | |

| Liquid | ||

| By Flavor | Plain | |

| Flavored | ||

| By Category | Organic | |

| Conventional | ||

| By Packaging Type | Stand-Up Pouches | |

| Bottles/Salt Sprinkler/Sprays | ||

| Jars | ||

| By Distribution Channel | On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the low sodium se salt market?

The salt substitute market reached USD 242.63 million in 2025 and is projected to grow to USD 336.11 million by 2030, expanding at a 6.74% CAGR.

Which region dominates the low sodium se salt market?

Asia-Pacific commands the largest market share at 35.63% in 2024, driven by high baseline sodium consumption patterns and government health initiatives.

What are the main types of low sodium se salt available?

The market is segmented by form (powder and liquid), with powder forms dominating at 78.56% market share.

What's the outlook for organic salt substitutes?

Organic variants are accelerating at 8.39% CAGR through 2030, driven by premiumization trends and clean-label preferences.

Page last updated on: