Screen Printing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

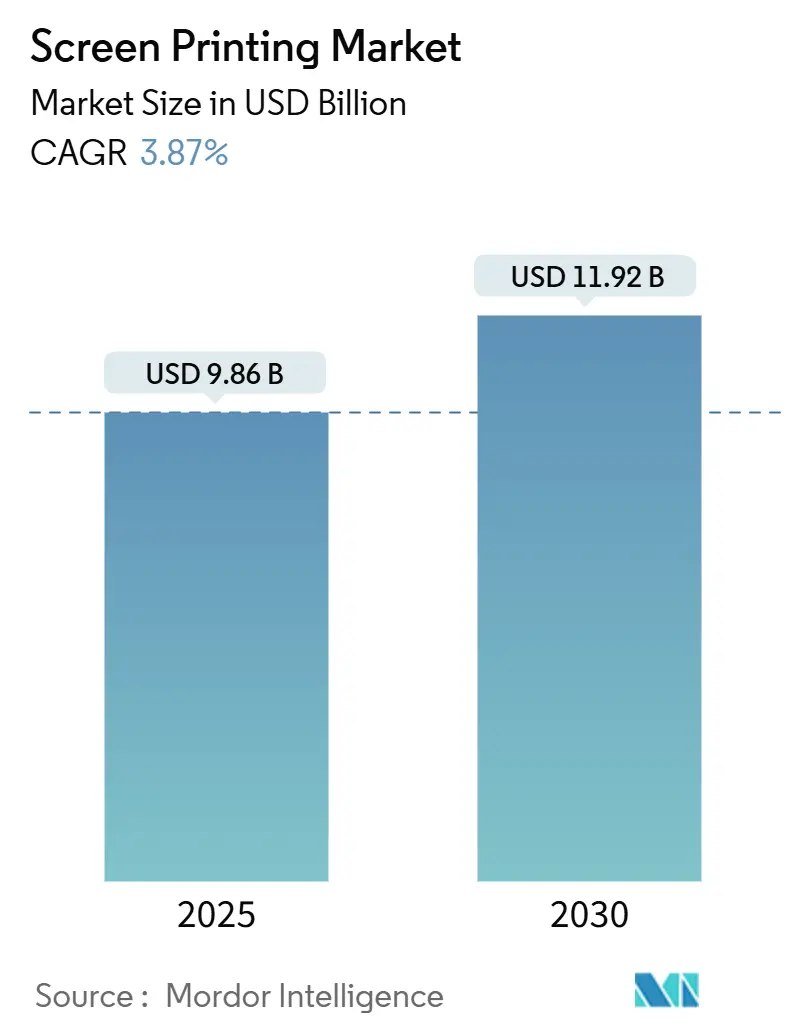

| Market Size (2025) | USD 9.86 Billion |

| Market Size (2030) | USD 11.92 Billion |

| Growth Rate (2025 - 2030) | 3.87% CAGR |

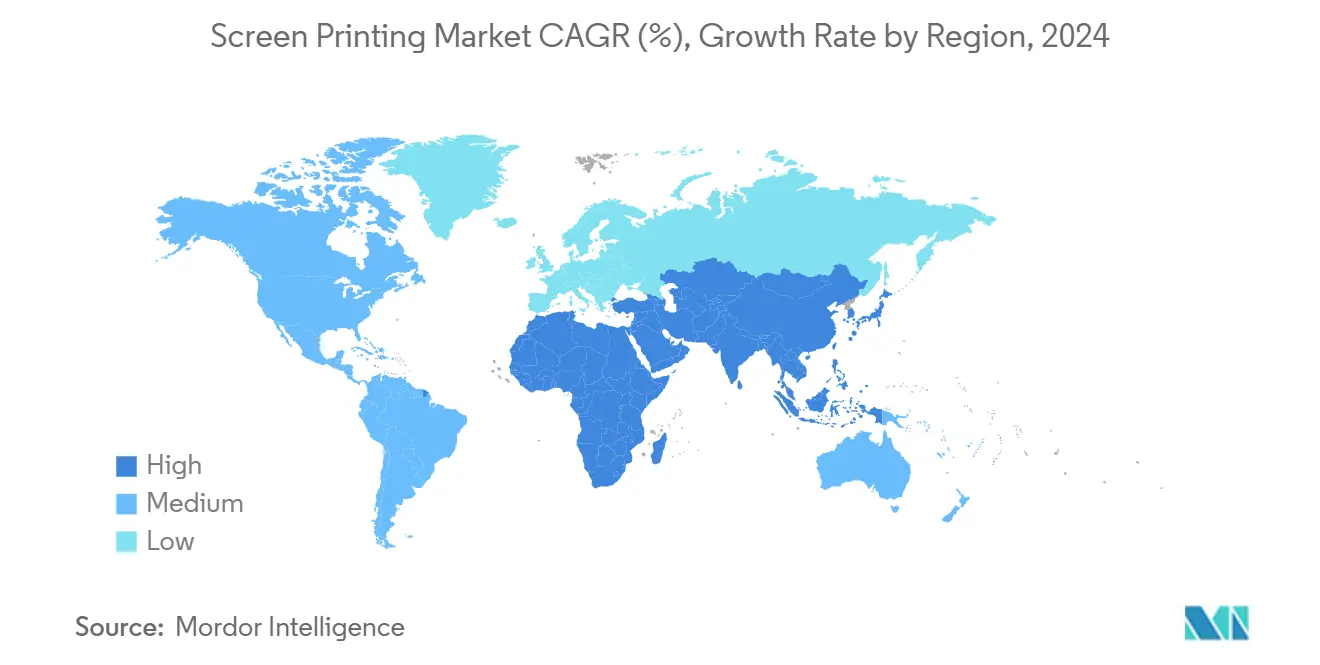

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Screen Printing Market Analysis by Mordor Intelligence

The screen printing market size reached USD 9.86 billion in 2025 and is forecast to rise to USD 11.92 billion by 2030 at a 3.87% CAGR, reflecting steady demand across textiles, packaging, and functional electronics applications. Traditional garment decoration is yielding margin to conductive-trace deposition for printed electronics, where screen technology supplies superior film thickness, adhesion, and material latitude relative to inkjet. Asia Pacific anchors growth as Chinese textile exports climb and Indian electronics assembly expands under incentive schemes, while North American converters commit multi-year capacity to e-commerce labels requiring thick, durable inks. In Europe, stricter volatile-organic-compound (VOC) thresholds under REACH and the Ecodesign Directive accelerate the shift to water-based chemistries, bolstering capital spending on closed-loop wash systems. Simultaneously, private-equity groups are targeting the screen printing market for its predictable cash flows, catalysing acquisitions that bundle prepress, printing, and fulfilment services.

Key Report Takeaways

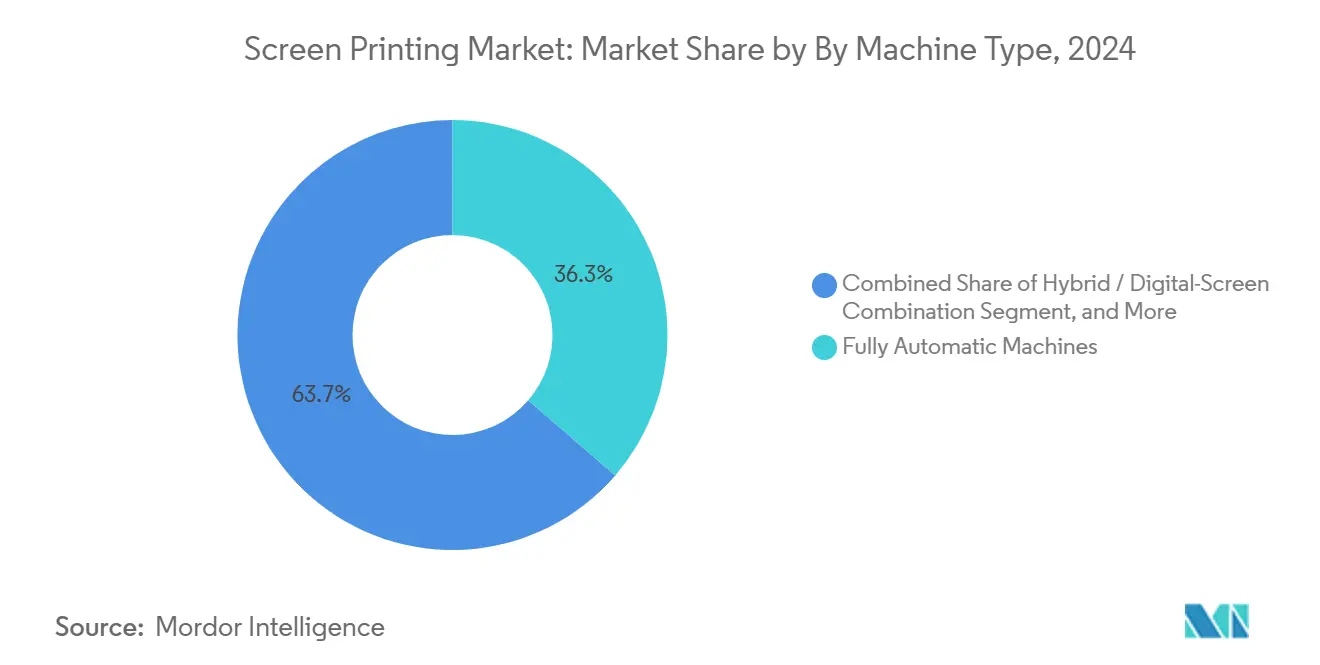

- By machine type, fully automatic presses led with 36.33% revenue share in 2024, whereas hybrid digital-screen systems are projected to expand at a 5.10% CAGR through 2030.

- By substrate, textiles accounted for 48.16% of 2024 sales, while conductive films are set to grow at 5.60% CAGR to 2030.

- By ink chemistry, plastisol posted 39.61% share in 2024; conductive formulations are expected to register a 6.30% CAGR through 2030.

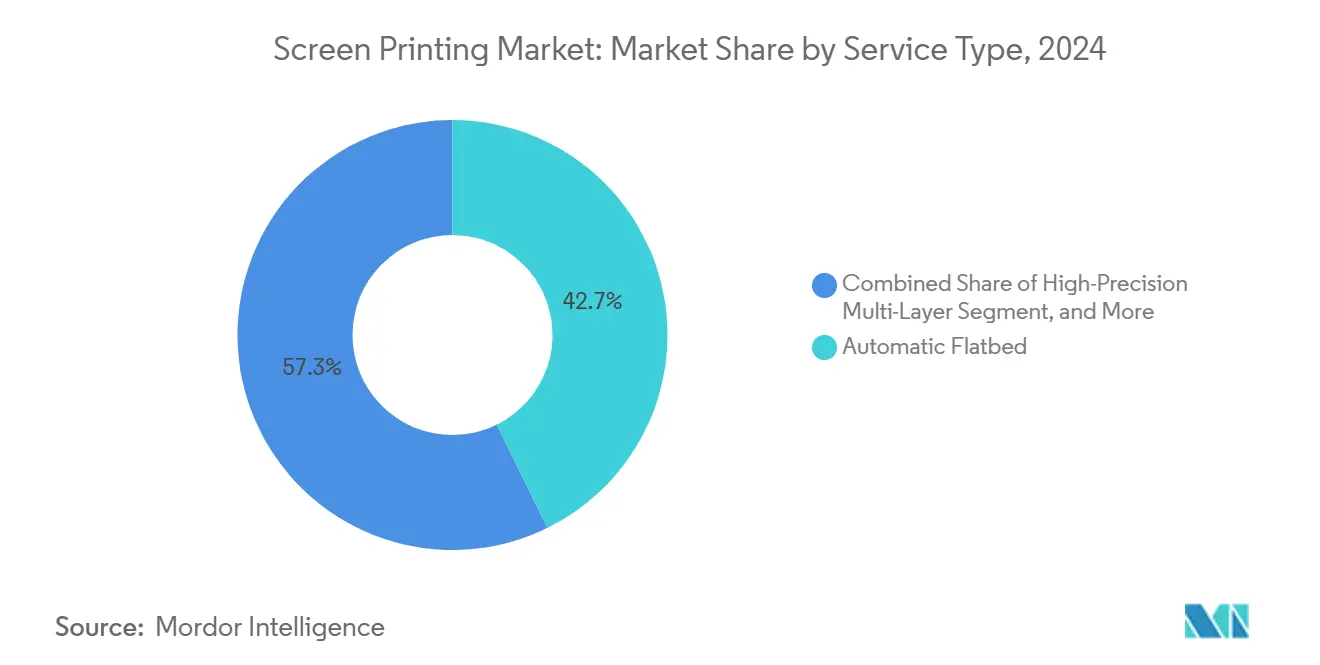

- By service type, automatic flatbed printing contributed 42.71% of 2024 revenue; precision multilayer services will advance at a 5.40% CAGR during the outlook period.

- By end-user, apparel and fashion captured 40.07% revenue in 2024, yet electronics applications are forecast to rise at a 6.00% CAGR to 2030.

- By geography, Asia Pacific held 34.55% of 2024 turnover and is poised for the fastest regional expansion at 4.80% CAGR through 2030.

Global Screen Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Custom Apparel and Promotional Merchandise | +0.80% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of Packaging and Label Printing for E-Commerce Logistics | +0.70% | Global, led by North America and Asia Pacific | Short term (≤ 2 years) |

| Adoption of Water-Based and Eco-Friendly Inks Under Tightening Regulations | +0.60% | Europe and North America, emerging in Asia Pacific | Long term (≥ 4 years) |

| Emergence of Screen-Printed Conductive Traces for Printed Electronics and IoT Devices | +0.90% | Asia Pacific, North America and Europe | Long term (≥ 4 years) |

| Automotive Interiors' Shift Toward Screen-Printed HMI Films and Sensors | +0.50% | Europe and Asia Pacific, selective North America | Medium term (2-4 years) |

| On-Demand Mass-Customisation Enabled by Web-to-Print Platforms | +0.40% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Emergence of Screen printed Conductive Traces for Printed Electronics and IoT Devices

Screen printing deposits metal layers between 5 µm and 25 µm, delivering low sheet resistance essential for flexible circuits used in battery monitoring, LiDAR heaters, and in-Mold switches. Automotive suppliers specify silver or copper pastes on polyimide and PET because the process pairs throughput with adhesion on heat-stable films. Asia Pacific research hubs are standardizing test protocols within IEC 62899, granting procurement teams the confidence to release volume contracts.[1]Source: International Electrotechnical Commission, “IEC 62899 Series on Printed Electronics,” iec.ch As smartphones, wearables, and smart tags proliferate, in-region fabs are scaling rotary lines that marry rotary tension control with micron-level registration. The technology also serves textile-integrated sensors, bridging rigid boards and fully printed flexible hybrids.

Adoption of Water-Based and Eco-Friendly Inks Under Tightening Regulations

REACH phthalate limits and the EU Ecodesign Regulation are accelerating the phase-out of plastisol’s in Europe, prompting converters to install closed-loop wash bays and reclaim units. Germany’s Federal Environment Agency reported water-based systems on over 40% of new textile lines in 2024, up from 28% four years earlier.[2]German Federal Environment Agency, “Water-Based Ink Adoption in Textile Screen Printing 2024,” umweltbundesamt.de Brands complying with France’s AGEC law favour water-borne barrier coatings that adhere to recycled paperboard without delamination. North American printers echo the shift to satisfy retailer scorecards and municipal VOC caps, adopting UV-LED lines that slash curing energy while eliminating dryer ovens. Mesh suppliers now coat with silicone repellents optimized for low-viscosity inks, further shrinking press downtime.

Expansion of Packaging and Label Printing for E-Commerce Logistics

Parcel volumes demand durable, variable-data labels able to endure abrasion and thermal swings across distribution centers. North America’s flexible-packaging sector was valued at USD 38.6 billion in 2024 and grows 3.9% annually, with screen printers serving metallized snack films and tamper-proof seals.[3]Flexible Packaging Association, “North America Flexible Packaging Market 2024,” flexpack.org Flatbed presses handling corrugated sheets now integrate vision cameras that register microtext and QR codes at 3,000 impressions per hour. Pharmaceutical brands leverage multilayer passes to embed UV-reactive pigments and holographic foils for serialization compliance. Europe’s 2025 Packaging and Packaging Waste Regulation pushes converters toward water-based adhesives that do not foul polyethylene recycling streams.[4]European Commission, “Packaging and Packaging Waste Regulation 2025,” ec.europa.eu

Rising Demand for Custom Apparel and Promotional Merchandise

Web-to-print platforms route time-sensitive orders to regional screen shops equipped with automatic carousels, preserving cost efficiency above 50-unit runs. Screen technology still leads on dark garments thanks to its opaque whites and specialty effects such as puff and reflective layers. China exported USD 109.04 billion in textiles during 2024, a 5.04% year-on-year increase, feeding Western distributors that value screen printed activewear and workwear. Extended Producer Responsibility rules in Europe emphasize graphics that withstand 50-plus industrial washes, reinforcing demand for robust plastisol and silicone formulations. North American collegiate sports licensing likewise sustains multi-colour, multi-layer carousel capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cannibalisation from Digital, DTG and DTF Printing Technologies | -0.60% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Volatile Prices of Specialty Meshes, Emulsions and Plastisol Raw Materials | -0.40% | Global, with pronounced impact in Asia Pacific and North America | Short term (≤ 2 years) |

| Skilled Labour Shortage for Multilayer and High-Precision Screen Printing | -0.30% | North America and Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| Capital Intensity of Automated Carousel and Rotary Presses for SMEs | -0.30% | Global, particularly acute for SMEs in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cannibalization from Digital, DTG, and DTF Printing Technologies

Direct-to-garment and direct-to-film systems erase setup and permit unlimited colours, drawing micro-brand runs below 100 pieces away from carousel presses. Equipment builders now bundle inkjet heads with rotary stations so that variable data prints digitally while base coats and tactile varnishes remain analog. Label converters report rising quotations featuring hybrid footprints as procurement teams hedge risk between cost per print and turnaround speed. The asymmetry persists: digital triumphs at design complexity; screen excels at opacity, durability, and unit economics above break-even volumes. Consequently, training programs emphasize cross-skilling operators to queue digital and screen jobs interchangeably.

Volatile Prices of Specialty Meshes, Emulsions, and Plastisol Raw Materials

Polyvinyl-chloride resin averaged CNY 5,700–5,850 per tonne during 2024 as crude swings and chlor-alkali outages ricocheted through supply chains. Polyester monofilament mesh lead times extended to 12 weeks after supplier consolidation, leaving contract printers vulnerable to price-locked agreements. Emulsion polymers tracking naphtha rose 15% through 2024, squeezing margins for small and medium shops lacking hedging tools. Some converters counter by standardizing mesh counts to pool purchasing, while others negotiate cost-escalator clauses tied to energy indices. Capital budgeting for automation slows when raw-material volatility clouds pay-back assumptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Hybrid Systems Bridge Analog and Digital Workflows

Fully automatic units generated 36.33% of 2024 revenue, reflecting apparel decorators’ priority on throughput, multicolour alignment, and in-line curing. Hybrid digital-screen presses, though smaller in installed base, will record the segment’s highest 5.10% CAGR as converters defend mid-length runs where customers still demand raised varnish, metallics, or opaque whites. These platforms place piezoelectric heads ahead of rotary or carousel stations, enabling versioned graphics without stopping the press.

Manual tables persist in artisan studios and emerging economies where labour costs undercut automation amortization. Rotary cylinder systems remain indispensable for seamless wallpaper and continuous textile yardage at speeds exceeding 100 meters per minute, while flatbeds dominate rigid panels for electronics and appliance overlays. SPGPrints widened the technology envelope in December 2025 with its Basalt RSI rotary line tailored for conductive films up to 508 millimetres wide.

By Substrate: Conductive Films Outpace Legacy Categories

Textiles supplied 48.16% of 2024 turnover thanks to athletic apparel, promotional tees, and workwear. Yet conductive films on polyimide and PET will log a leading 5.60% CAGR as automotive interiors specify touch-sensor layers and battery heaters. Plastics, encompassing bottles and moulded parts, rely on screen’s adhesion and colour density, particularly for opaque whites and metallics that injection moulding cannot replicate.

Paper and paperboard capture e-commerce labels and corrugated displays, where dense ink builds guarantee barcode legibility and abrasion resistance. Glass serves appliances, smart mirrors, and architectural panels. Ceramics and metals occupy niche segments, ranging from tile decoration to industrial nameplates, where high-temperature curing and chemical resistance are paramount.

By Ink Type: Conductive Chemistries Lead Innovation

Plastisol retained 39.61% of 2024 sales due to its stretch, opacity, and forgiving shear profile. Conductive pastes, though smaller in volume, are forecast at a 6.30% CAGR as automotive and IoT projects scale. Water-based inks are gaining share in textiles and paperboard packaging to meet VOC caps, encouraged by Germany’s carbon-pricing framework. UV-LED systems, while beyond the scope of market-research estimates, attract label printers for instant curing and lower energy bills.

Solvent formulations linger in outdoor graphics, but air-quality rules in California and across the EU are narrowing their window. Emerging silver-flake blends achieve resistances below 50 mΩ/□ suitable for RFID antennas, and ongoing R&D targets copper and carbon formulations with improved oxidation stability.

By Service Type: Precision Multilayer Printing Captures High-Value Niches

Automatic flatbed lines held 42.71% revenue share in 2024 by serving packaging converters who need rigid-substrate throughput at high registration accuracy. High-precision multilayer services will outpace the category at a 5.40% CAGR, driven by pharmaceutical serialization and flexible-circuit value-adds that stack six-plus layers with <50 µm tolerance. Rotary lines dominate endless webs textile yardage, wallpaper, and flexible packaging while cylinder presses address ceramic decals and extra-large signage.

Manual work persists for bespoke runs that prize craft aesthetics over volume efficiency. Equipment vendors are rolling out laser-to-screen imagers that cut masking steps, shrink chemical waste, and lift resolution to 5,080 dpi, pushing screen printing closer to photolithographic quality.

By End-User Industry: Electronics Segment Drives Functional Printing Pivot

Apparel and fashion commanded 40.07% of 2024 income, but electronics clients ranging from vehicle OEMs to sensor start-ups will chart the swiftest 6.00% CAGR through 2030 as flex circuits and capacitive films move from lab to line. Packaging and labels inherit e-commerce volume, marrying screen’s ink build with digital variable data. Advertising and large-format signage rely on thick ink layers for UV durability.

Automotive interiors integrate screen printed graphics on trim and overlays, embedding touch keys and backlit icons. Industrial components, from control panels to appliance fronts, specify screen inks for chemical and abrasion resistance, sustaining a resilient baseline of demand.

Geography Analysis

Asia Pacific generated 34.55% of global revenue in 2024 and will advance at a 4.80% CAGR to 2030. China dominates textiles on the strength of USD 109.04 billion in 2024 exports, aided by domestic supply chains that weave mesh, formulate inks, and assemble automatic carousels at cost advantages surpassing 15% over Western peers. India’s production-linked incentive program is spawning greenfield electronics fabs that contract local screen shops for sensor prototypes, while Japan’s press builders pivot to printed-electronics lines capable of 60 m/min label output. Vietnam and Bangladesh expand apparel decoration as brands pursue China-plus-one sourcing, though infrastructure gaps limit automation depth.

Europe’s screen printing market is bifurcating under environmental regulation. Textile and packaging houses shift to water-based or UV-LED lines to avoid REACH penalties and the EUR 50–150 per-tonne carbon levy expected under the EU Emissions Trading System enlargement. Automotive suppliers add conductive layer capacity for human-machine interface films. Italy and Spain retain artisanal houses that serve luxury fashion and ceramics at premium prices, whereas Eastern Europe competes on labor costs for export-oriented apparel printing. The United Kingdom navigates post-Brexit compliance divergence yet leverages flexible ink-switching to serve EU clients without duplicate tooling.

North America is consolidating as investors seek predictable margins: Brookfield completed a USD 2.2 billion take-private of Quad Graphics in 2024 and CCL Industries paid USD 1.1 billion for Checkpoint Systems the same year. Flexible packaging hit USD 38.6 billion in 2024, rising 3.9% annually, with screen printers capturing metallized films and track-and-trace tags. U.S. decorators adopt hybrid presses that pair inkjet heads with rotary stations to blend personalization and tactile varnishes, while Canada and Mexico target niche industrial and automotive components. Middle Eastern demand clusters in packaging and out-of-home advertising; South Africa, Nigeria, and Egypt form Africa’s main textile-print hubs despite limited access to specialty inks.

Competitive Landscape

The screen printing market shows moderate concentration; the top ten firms hold a significant share of global revenue, leaving regional players room to specialize in local substrates or value-added services. Private-equity activity accelerated in 2024 as asset managers pursued recurring cash flows: Brookfield acquired Quad Graphics, while CCL Industries folded Checkpoint Systems into its label empire.

Equipment builders differentiate through automation and hybrid capability. SPGPrints’ Basalt RSI rotary line offers widths up to 508 mm for conductive films, aimed at electronics assemblers pivoting from photolithography. M&R’s partnership with Xaar integrates piezoelectric heads on rotary stations for packaging converters needing variable data without sacrificing thick-film whites. Dai Nippon Printing’s acquisition of HK Holding deepens its automotive trim portfolio, illustrating how conglomerates knit screen printed components into broader surface-treatment strategies.

Innovation white-space concentrates on on-demand mass customization and conductive-trace sensor tags. Hybrid machines that queue digital layers before analog varnish preserve margins on mid-length runs threatened by fully digital workflows. Large converters invest in laser-to-screen lines to slash exposure times and eliminate hazardous chemicals, while small shops defer capital spending amid raw-material volatility. Adoption of IEC 62899 unlocks larger purchase orders from automotive and medical buyers, tilting competitive advantage toward plants boasting ISO 9001 procedures and documented process control.

Screen Printing Industry Leaders

Toppan Inc.

Dai Nippon Printing Co., Ltd.

CCL Industries Inc.

Quad/Graphics, Inc.

RR Donnelley and Sons Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: M&R Companies partnered with Xaar to embed piezoelectric inkjet heads into M&R rotary platforms, enabling hybrid workflows for packaging converters.

- February 2025: Dai Nippon Printing acquired HK Holding, owner of Hikari Metal Industry, adding metallized and textured screen-printing capabilities for automotive trim.

- January 2024: Dai Nippon Printing began operating a 2,500 mm coating line at its Mihara Plant, expanding optical-film capacity by 15% to meet display and automotive HMI demand.

- December 2024: SPGPrints released the Basalt RSI rotary system for printed electronics at widths up to 508 mm, targeting flexible-circuit scale-up.

Global Screen Printing Market Report Scope

The Screen Printing Market Report is Segmented by Machine Type (Manual, Semi-Automatic, Fully Automatic, Rotary, Flatbed, Cylinder, Hybrid/Digital-Screen Combination), Substrate (Textiles, Plastics, Glass, Paper and Paperboard, Conductive Films, Other Substrates), Service Type (Manual, Automatic Flatbed, Rotary, Cylinder, High-Precision Multi-Layer), Ink Type (Plastisol, Water-Based, UV-Curable, Solvent-Based, Conductive), End-User Industry (Apparel and Fashion, Packaging and Labels, Advertising and Signage, Electronics and Printed Electronics, Automotive and Transportation, Industrial Components, Other End-User Industries), and Geography (North America, Europe, Asia Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Manual Screen Printing Machines |

| Semi-Automatic Screen Printing Machines |

| Fully Automatic Screen Printing Machines |

| Rotary Screen Printing Machines |

| Flatbed Screen Printing Machines |

| Cylinder Screen Printing Machines |

| Hybrid / Digital-Screen Combination Machines |

| Textiles |

| Plastics |

| Glass |

| Paper and Paperboard |

| Conductive Films |

| Other Substrates |

| Manual Screen Printing |

| Automatic Flatbed Screen Printing |

| Rotary Screen Printing |

| Cylinder Screen Printing |

| High-Precision Multi-Layer Screen Printing |

| Plastisol Inks |

| Water-Based Inks |

| UV-Curable Inks |

| Solvent-Based Inks |

| Conductive Inks |

| Apparel and Fashion |

| Packaging and Labels |

| Advertising and Signage |

| Electronics and Printed Electronics |

| Automotive and Transportation |

| Industrial Components |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Qatar | |

| Kuwait | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Kenya | |

| Morocco | |

| Rest of Africa |

| By Machine Type | Manual Screen Printing Machines | |

| Semi-Automatic Screen Printing Machines | ||

| Fully Automatic Screen Printing Machines | ||

| Rotary Screen Printing Machines | ||

| Flatbed Screen Printing Machines | ||

| Cylinder Screen Printing Machines | ||

| Hybrid / Digital-Screen Combination Machines | ||

| By Substrate | Textiles | |

| Plastics | ||

| Glass | ||

| Paper and Paperboard | ||

| Conductive Films | ||

| Other Substrates | ||

| By Service Type | Manual Screen Printing | |

| Automatic Flatbed Screen Printing | ||

| Rotary Screen Printing | ||

| Cylinder Screen Printing | ||

| High-Precision Multi-Layer Screen Printing | ||

| By Ink Type | Plastisol Inks | |

| Water-Based Inks | ||

| UV-Curable Inks | ||

| Solvent-Based Inks | ||

| Conductive Inks | ||

| By End-User Industry | Apparel and Fashion | |

| Packaging and Labels | ||

| Advertising and Signage | ||

| Electronics and Printed Electronics | ||

| Automotive and Transportation | ||

| Industrial Components | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Qatar | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the screen printing market?

The screen printing market size stands at USD 9.86 billion in 2025.

How fast will global demand grow over the next five years?

Revenue is projected to rise at a 3.87% CAGR, reaching USD 11.92 billion by 2030.

Which region is expanding the quickest?

Asia Pacific leads with a forecast 4.80% CAGR, powered by Chinese textiles and Indian electronics programs.

Which segment shows the most upside beyond textiles?

Conductive-film applications for automotive and IoT devices are expected to record the highest 5.60% CAGR among substrates.

How are regulations shaping ink choices?

Tightening VOC limits under REACH and similar rules push European and North American printers toward water-based and UV-LED chemistries.

Are hybrid presses worth the investment?

For mid-length runs, hybrid digital-screen machines defend margins by combining variable data with the opacity and tactile effects unique to screen prints.

Page last updated on: