Paper Printing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

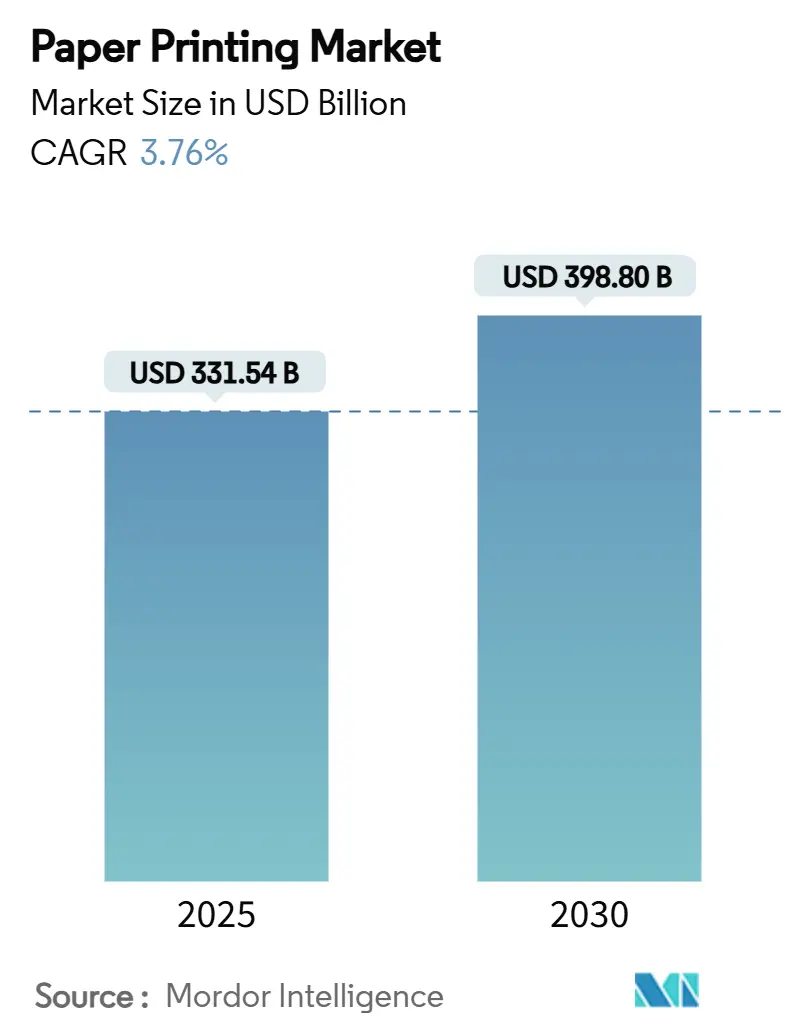

| Market Size (2025) | USD 331.54 Billion |

| Market Size (2030) | USD 398.80 Billion |

| Growth Rate (2025 - 2030) | 3.76% CAGR |

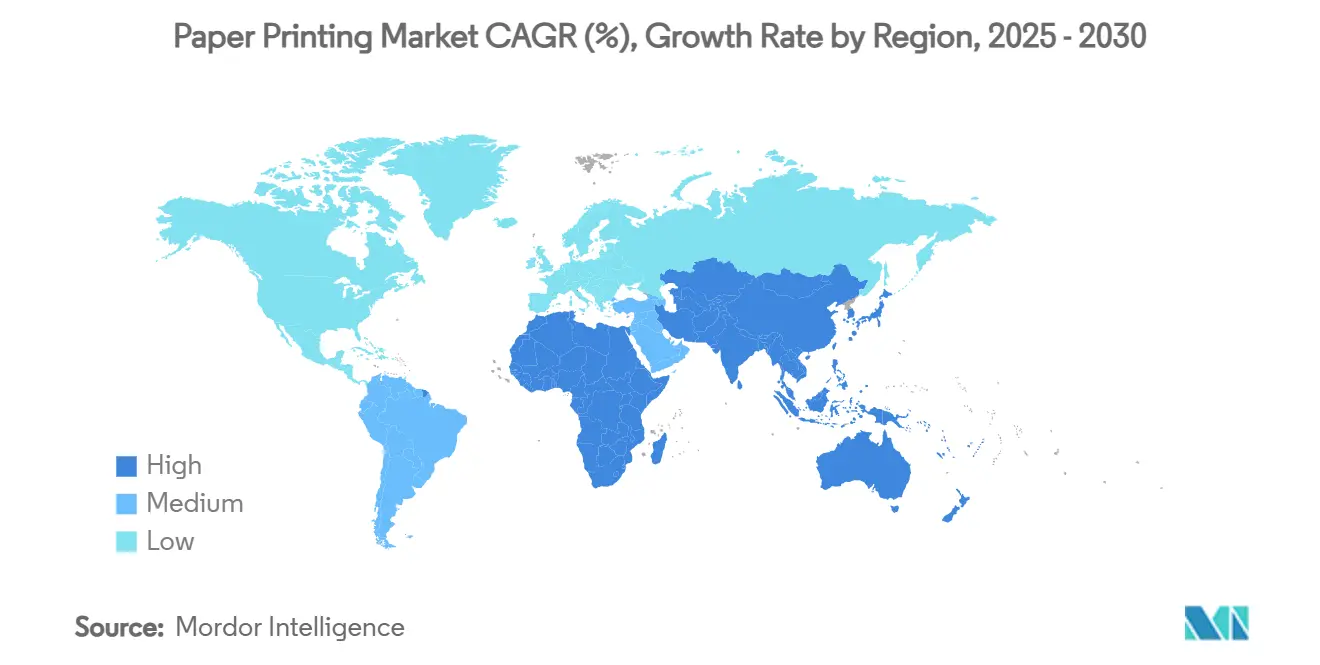

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

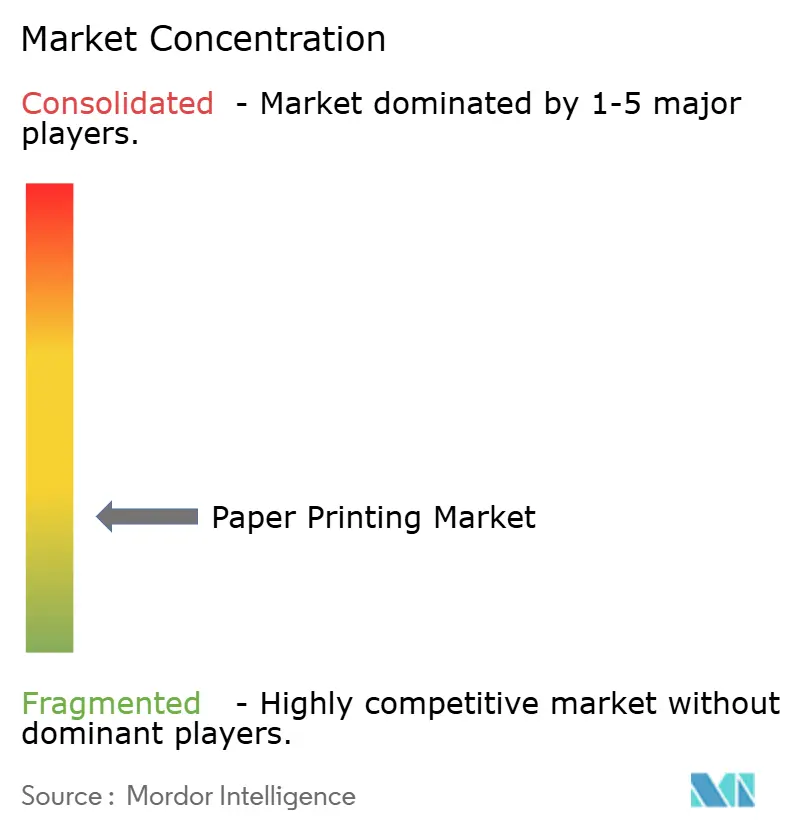

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Printing Market Analysis by Mordor Intelligence

The paper printing market size stands at USD 331.54 billion in 2025 and is forecast to reach USD 398.80 billion by 2030, expanding at a 3.76% CAGR. A surge in e-commerce packaging, regulatory preference for fiber-based substrates, and steady demand for secure documents underpin this growth. Packaging applications dominate the paper printing market because online retail needs branded corrugated boxes that double as marketing displays. At the same time, high-speed inkjet presses cut waste and turn conventional print runs into on-demand workflows that appeal to cost-sensitive publishers and advertisers. Asia-Pacific’s manufacturing momentum, coupled with government incentives for domestic pulp capacity, keeps the region at the forefront of new press installations. Consolidation among converters, such as Xerox’s Lexmark takeover, shows how incumbents are strengthening digital capabilities to serve evolving brand requirements.

Key Report Takeaways

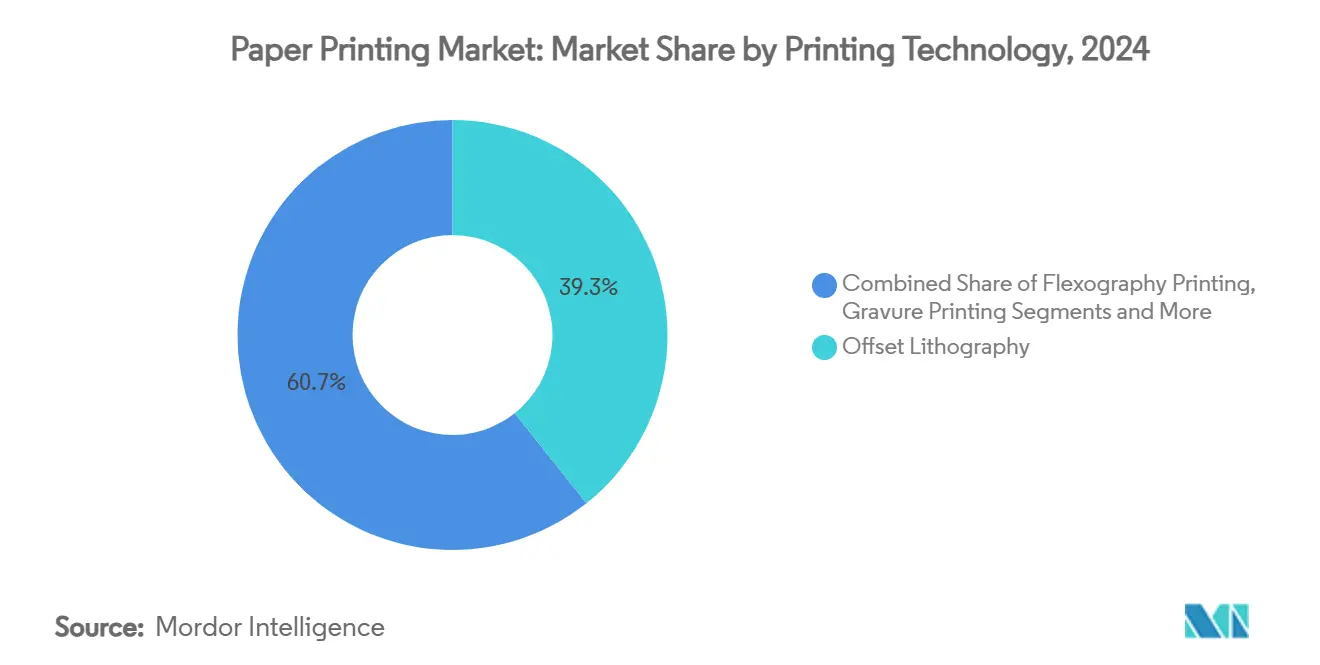

- By printing technology, offset lithography led with 39.3% of the paper printing market share in 2024, while inkjet digital printing is projected to grow at 4.7% CAGR through 2030.

- By application, packaging printing commanded 58.1% revenue share in 2024; textile transfer printing is forecast to advance at 4.8% CAGR to 2030.

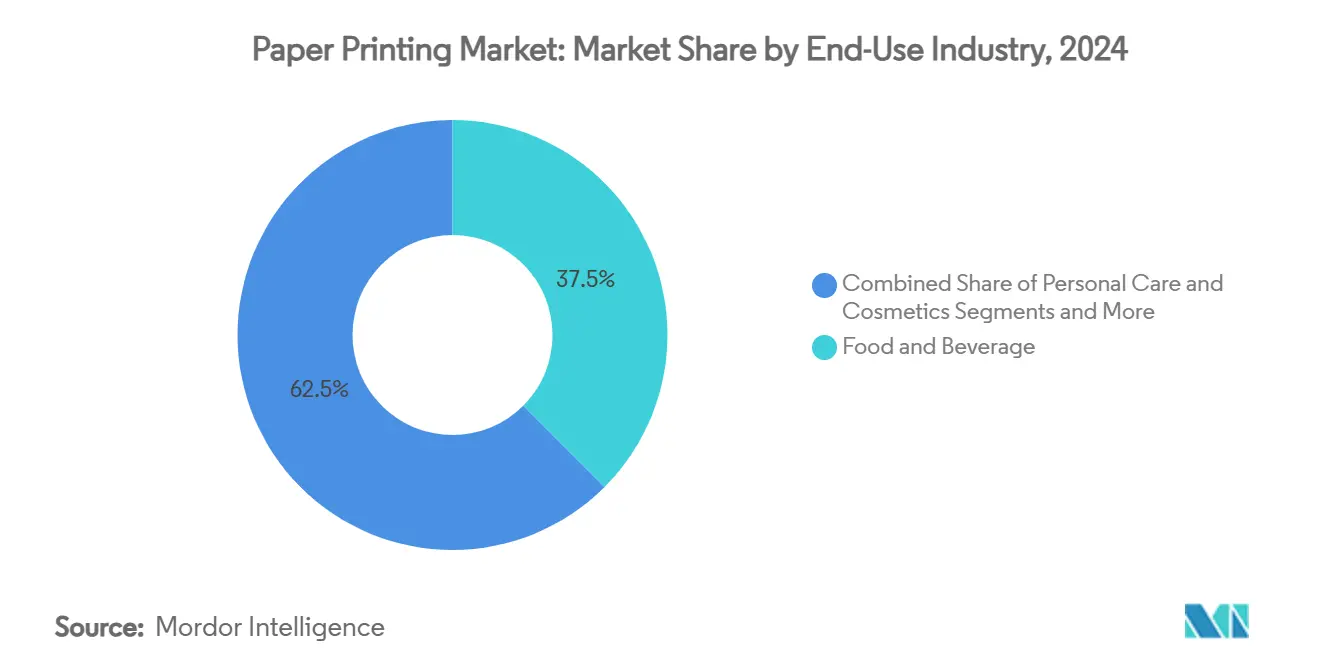

- By end-use industry, food and beverage held 37.5% share of the paper printing market size in 2024, while e-commerce and retail will expand at 5.3% CAGR through 2030.

- By substrate, coated paper and paperboard captured 48.2% share in 2024; specialty and barrier papers are set to grow at 5.2% CAGR through 2030.

- By geography, Asia-Pacific accounted for 44.3% share in 2024 and is projected to post the fastest 5.8% CAGR to 2030.

Global Paper Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of e-commerce packaging print | +0.6% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Sustainability shift from plastic to paperboard | +0.5% | Global, led by Europe and North America | Long term (≥ 4 years) |

| High-speed inkjet lowers commercial print costs | +0.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Variable-data print for brand engagement | +0.3% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Functional printing on paper | +0.2% | APAC core, spill-over worldwide | Long term (≥ 4 years) |

| Election-grade secure document demand surge | +0.2% | Global democratic regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid growth of e-commerce packaging print

Online sellers rely on corrugated cartons that carry high-resolution brand graphics and authentication marks, driving the paper printing market toward flexible runs that follow seasonal launches. Digital presses let converters merge shipping protection and shelf display into one unit, cutting inventory and eliminating double packaging. Large platforms such as Amazon now set material specifications that favor easy-recycle paperboard, lifting demand for barrier-coated liners that resist moisture. Corrugated converters upgrade to inline inkjet heads, reducing setup times that weighed on traditional offset. As fit-to-product packaging gains traction, brands capitalize on unboxing experiences to spur social media engagement, reinforcing the shift toward short runs and high graphics. Enhanced workflows shorten delivery windows, making speed a decisive differentiator.

Sustainability shift from plastic to paperboard

Regulators exempt fiber-based packs from several recycled-content mandates, giving paper an edge over single-use plastics.[1] Packaging Europe, “The packaging stories and trends to follow in 2025,” packagingeurope.comConsumer polls show 66% preference for paper packs, prompting brand owners like Nestlé to switch to high-barrier paper sleeves that match metalized film performance. Suppliers respond with coatings that keep recyclability above 80% fiber while granting grease resistance for snack foods. Novel substrates such as stone paper cut lifecycle emissions by 39% compared with legacy materials. Printers that install curtain coaters and closed-loop recovery lines secure early-mover pricing power. Over time, retailer private-label specifications will likely tighten, embedding sustainability as a non-negotiable requirement across the paper printing market.

High-speed inkjet lowers commercial print costs

Next-generation inkjet presses such as HP Indigo 120K merge analog-grade image quality with digital agility, eliminating plate changes and trimming overruns to near zero. Publishers note that 25% of book pages already move through inkjet, a share projected to climb to 39% by 2028. The cost curve flattens as heads last longer and inks run on offset papers, removing the substrate premium that once restricted digital rollouts. Automation cuts labor touchpoints by 85%, letting plants operate multiple shifts with lean crews. Energy usage drops due to simpler workflows, supporting corporate decarbonization targets. These economics accelerate the adoption of inkjet across catalogs, direct mail, and transactional print, reshaping the competitive cost base of the paper printing market.

Variable-data print for brand engagement

Personalized mail pieces lift campaign response rates to a median 29% when they carry unique images or messages. Coca-Cola’s named bottle labels and Nutella’s custom jars showcase how scalable variable-data applications build emotional resonance at shelf. Software plug-ins now auto-populate variable fields across text, color, and imagery, enabling marketers to run thousands of micro-segments with minimal operator input. Secure digital asset management ensures regulatory compliance for sensitive data while feeding press queues in real time. Integration with QR codes and augmented reality extends print into omnichannel activations. As brands chase measurable returns, variable-data print keeps the paper printing market relevant within broader customer journey strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital substitution in publishing and transaction | -0.3% | Global, most pronounced in developed markets | Long term (≥ 4 years) |

| Print-buyer consolidation squeezes margins | -0.2% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Pulp and paper price volatility | -0.2% | Global, with regional variations | Short term (≤ 2 years) |

| Stricter VOC limits on solvent inks | -0.2% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital substitution in publishing and transaction

Graphic paper demand fell 19% in 2024 as readers consumed news and statements online.[2]Hammond Paper Company, “Challenges and Opportunities for the Paper and Pulp Industry,” hammondpaper.com Banks migrate to mobile notifications, eroding statement volumes that once provided stable work for offset plants. Hybrid models soften the decline: publishers keep backlists alive through print-on-demand, which lowers warehousing. Transaction printers pivot to secure direct mail for regulated notices, retaining a niche within data-sensitive communications. The overall effect still subtracts 0.3 percentage points from the paper printing market CAGR.

Print-buyer consolidation squeezes margins

Retailers and brand groups centralize procurement, demanding multiyear contracts that push prices down. Converters in North America and Europe report narrower spreads between input pulp costs and selling prices, prompting mergers aimed at volume leverage. Some independents counter by specializing in short-run high-graphics SKUs, yet buyer power remains a structural headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Digital inkjet drives flexible production

Offset lithography still delivers the lowest unit cost on million-sheet campaigns, cementing its 39.3% share of the paper printing market in 2024. However, the segment’s growth plateaus as brands favor micro-targeted releases that suit digital workflows. Inkjet presses, expanding at 4.7% CAGR, eliminate plate fees and let converters batch orders by substrate rather than customer, increasing press uptime. The paper printing market size attributed to digital presses is projected to reach USD 129 billion by 2030, reflecting sustained capex in roll-fed lines. Hybrid sites blend offset and inkjet, enabling printers to match run length with optimal economics during the same shift. Flexography keeps a foothold in corrugated and flexible packs where fast-dry inks and wide webs shine. Gravure’s niche narrows to long-run catalogs and décor laminates, while toner devices migrate to office equipment and photo prints.

Advancements in ink chemistry now bond with standard gloss and matte stocks, removing pre-treated paper premiums and widening addressable applications. Automated color-profile engines drive consistent output across shifts, reducing rejects. Predictive maintenance platforms feed sensor data into cloud dashboards, slashing unexpected downtime. These capabilities enhance the competitiveness of digital lines and keep capital flowing into software as much as hardware.

By Application: Packaging maintains scale as textiles rise

Packaging occupied 58.1% of the paper printing market size in 2024, propelled by e-commerce volumes that need outer cartons and protective inserts. Corrugated’s double-digit unit growth offsets declines in legacy folding cartons tied to in-store displays. Textile transfer printing progresses at 4.8% CAGR, underpinned by fashion’s pivot to mass customization. Direct-to-film technology reduces water use and supports on-shore production runs of limited editions. Publishing output contracts but stabilizes through short-run educational titles printed only after orders arrive. Commercial advertising repositions around data-driven direct mail, allowing marketers to break through digital ad fatigue using tactile engagement.

Security and transaction work holds steady because elections, tax notifications, and authentication features resist digitization. Functional and smart packaging emerges as a frontier segment, turning boxes into marketing analytics endpoints. As a result, printers that diversify across multiple applications mitigate exposure to any single demand swing in the paper printing market.

By End-Use Industry: Food & beverage dictates volume

Food and beverage customers consumed 37.5% of the paper printing market share in 2024, with barrier-lined cartons protecting snacks, dairy, and ready meals. Brands demand grease and moisture barriers free of PFAS chemicals, creating specification hurdles that reward technical competence. E-commerce and retail segments, growing at 5.3% CAGR, transform shipper boxes into billboard spaces, with unboxing aesthetics ranking high in DTC channel priorities. Personal care firms request metallic accents and tactile varnishes that differentiate on crowded shelves.

Pharmaceutical companies lock in multiyear contracts for serialized folding cartons that track drugs through supply chains. Industrial buyers focus on durable labels and manuals that withstand harsh conditions. Government agencies procure secure passports and tax stamps, ensuring a steady baseline. The diversity of end users spreads risk and sustains the paper printing market across economic cycles.

By Print Substrate: Barrier paper innovations accelerate adoption

Coated paperboard claimed 48.2% of 2024 revenue thanks to its printability and structural strength. Developments in aqueous coatings now meet grease-proof standards for quick-service meals, broadening use cases. Specialty barrier grades, climbing at 5.2% CAGR, integrate bio-based layers that deliver oxygen and moisture protection while remaining repulpable. Corrugated board benefits from double-digit e-commerce expansion, reinforced by algorithms that design right-sized boxes to cut void fill. Uncoated papers stay relevant for financial mailers and books where glare reduction matters.

Conductive polymer coatings turn ordinary liners into smart surfaces able to sense temperature or track freshness. Label stock evolves toward thinner facestocks combined with wash-off adhesives that improve recycling yields. Substrate development therefore plays a direct role in how the paper printing market captures new value pools beyond traditional graphics.

Geography Analysis

Asia-Pacific generated 44.3% of 2024 revenue and shows the fastest 5.8% CAGR to 2030. China’s box demand slackened amid macro headwinds, yet investments in digital press hubs and textile transfer clusters keep regional momentum high. India’s print export incentives and growing middle class spur capacity in corrugated and folding cartons, while Vietnam and Indonesia attract multinational apparel firms that need rapid-turnaround labels. Technology suppliers in Japan and South Korea pioneer inkjet heads and process automation that diffuse globally.

North America benefits from reshoring trends and infrastructure spending that require construction document sets, plus a relentless e-commerce sector driving corrugated volumes. Investments such as International Paper’s USD 260 million Iowa plant and Georgia-Pacific’s USD 550 million Green Bay expansion add box converting lines with 85% automation. These upgrades boost capacity while embedding robotics, sharpening the region’s competitiveness within the global paper printing market.

Europe balances stringent environmental policy with a high-value luxury goods sector. The EU’s STS directive raises compliance costs, but printers that adopt activated-carbon systems win preferred-supplier status among brand owners who market sustainability transparency. Italy and France see demand for short-run cosmetics cartons, while Germany focuses on industrial labels for machinery exports. Eastern European sites secure outsourced jobs from Western brand owners seeking cost efficiency inside the EU trade zone.

Competitive Landscape

The paper printing market remains moderately fragmented. The top five converters control less than 30% of global revenue, leaving room for regional specialists and digital disruptors. Traditional offset houses face margin erosion as inkjet entrants promise faster turnarounds and variable content. Consequently, strategic acquisitions accelerate: Xerox bought Lexmark for USD 1.5 billion to widen managed-print services coverage across 170 countries. Toppan paid USD 1.8 billion for Sonoco’s thermoformed and flexible packaging assets, creating an integrated fiber-to-package platform.

Competitive edges shift toward automation, sustainability credentials, and smart-packaging know-how. HP leverages AI-driven predictive maintenance that cuts downtime and calibrates color in real time, lowering cost per print and boosting consistency.[3]HP Inc., “HP Sets New Industry Standard in Digital Printing,” hp.com Amcor and Metsä Board differentiate with proprietary barrier coatings that remove PFAS chemicals while retaining performance. Patent filings in conductive inks signal convergence between printing and electronics sectors, foreshadowing future alliances or rivalries.

Smaller converters carve niches in luxury embellishment, tactile varnishes, or sustainable substrate consulting. Some sites adopt subscription-based press models where OEMs monitor performance remotely and bill by printed square meter, easing capex burdens. Price pressure from consolidated buyers persists, but printers that package high-margin services—such as design, logistics, and data analytics—mitigate commoditization. The overall trajectory sees incremental consolidation balanced by nimble entrants exploiting technology gaps, keeping rivalry active across the paper printing market.

Paper Printing Industry Leaders

Dai Nippon Printing Co., Ltd.

Toppan Inc.

Quad/Graphics, Inc.

RR Donnelley & Sons Company

Cimpress plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kimberly-Clark announced a USD 2 billion five-year investment to expand North American manufacturing, including a new plant in Warren, Ohio and an expansion in Beech Island, South Carolina, creating over 900 skilled jobs.

- January 2025: International Paper announced plans to build a USD 260 million corrugated packaging plant in Waterloo, Iowa, replacing its existing facility with a 900,000-square-foot site that will create 90 jobs.

- December 2024: Toppan Holdings agreed to acquire Sonoco's Thermoformed & Flexible Packaging business for about USD 1.8 billion, enhancing sustainable packaging in the Americas.

- December 2024: Xerox announced acquisition of Lexmark for USD 1.5 billion, establishing a consolidated presence in 170 countries and targeting USD 200 million in synergies.

Global Paper Printing Market Report Scope

| Offset Lithography Printing | |

| Flexography Printing | |

| Gravure Printing | |

| Screen Printing | |

| Digital Printing | Inkjet Digital Printing |

| Toner Digital Printing |

| Packaging Printing |

| Commercial and Advertising Printing |

| Publishing Printing |

| Security and Transaction Printing |

| Textile Transfer Printing |

| Other Specialty Prints |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceutical and Healthcare |

| E-commerce and Retail |

| Government and Institutional |

| Industrial and Manufacturing |

| Uncoated Paper |

| Coated Paper and Paperboard |

| Corrugated Board |

| Specialty / Barrier Papers |

| Labels and PSA Stock |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Printing Technology | Offset Lithography Printing | ||

| Flexography Printing | |||

| Gravure Printing | |||

| Screen Printing | |||

| Digital Printing | Inkjet Digital Printing | ||

| Toner Digital Printing | |||

| By Application | Packaging Printing | ||

| Commercial and Advertising Printing | |||

| Publishing Printing | |||

| Security and Transaction Printing | |||

| Textile Transfer Printing | |||

| Other Specialty Prints | |||

| By End-Use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceutical and Healthcare | |||

| E-commerce and Retail | |||

| Government and Institutional | |||

| Industrial and Manufacturing | |||

| By Print Substrate | Uncoated Paper | ||

| Coated Paper and Paperboard | |||

| Corrugated Board | |||

| Specialty / Barrier Papers | |||

| Labels and PSA Stock | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the paper printing market?

The paper printing market size stands at USD 331.54 billion in 2025 and is projected to grow to USD 398.80 billion by 2030.

Which region leads the paper printing market?

Asia-Pacific leads with 44% revenue share in 2024 and is expected to post the fastest 5.80% CAGR through 2030.

Why is packaging printing so important?

Packaging accounted for 58% of 2024 revenue because e-commerce demands branded, sustainable boxes that double as marketing displays, driving continuous press investment.

How is digital inkjet affecting traditional printing?

Inkjet presses grow at 4.70% CAGR by removing plate costs and enabling variable data, eroding offset’s dominance in medium runs.

What regulations are influencing market growth?

Stricter VOC caps and plastic-reduction policies push converters toward paperboard and water-based inks, boosting demand for sustainable substrates and clean technologies.

Who are the notable recent investors?

Firms such as Kimberly-Clark, International Paper, and Georgia-Pacific each committed over USD 200 million to new or expanded North American facilities since late 2024, underscoring confidence in long-term growth.

Page last updated on: