Printed Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.47 Billion |

| Market Size (2031) | USD 8.91 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

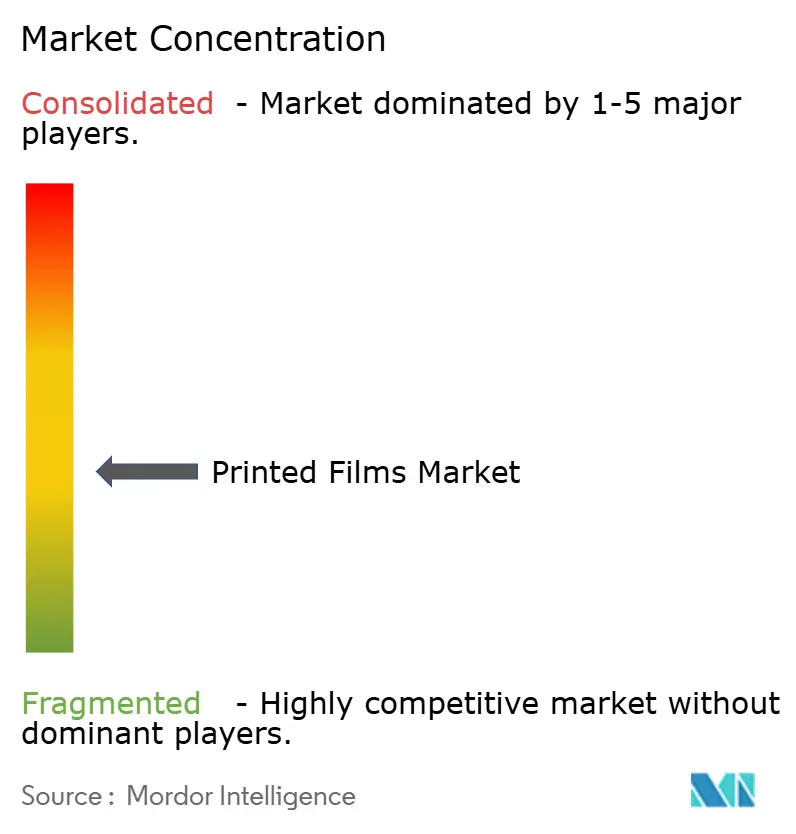

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printed Films Market Analysis by Mordor Intelligence

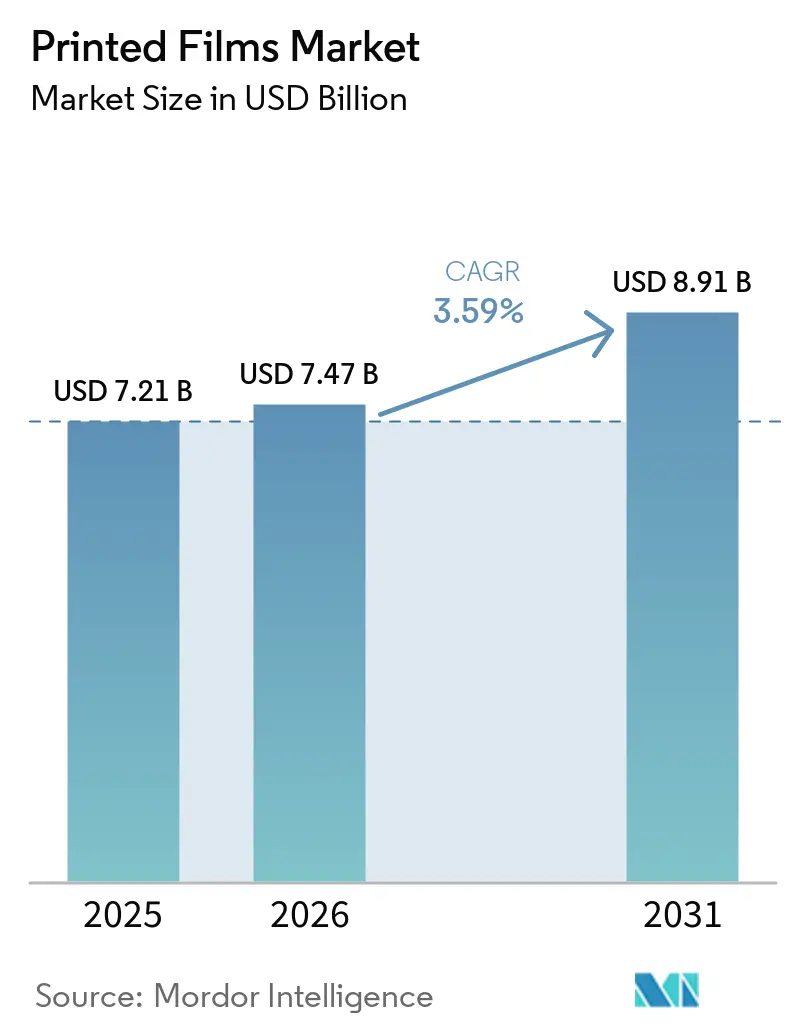

The printed films market size is projected to expand from USD 7.21 billion in 2025 and USD 7.47 billion in 2026 to USD 8.91 billion by 2031, registering a CAGR of 3.59% during the forecast period (2026 to 2031). Sustained e-commerce activity is keeping protective mailers and cushioned wraps in the spotlight, while growing legislative pressure in Europe and North America is steering brand owners toward compostable or recyclable film substrates. Polyethylene grades remain the volume mainstay owing to their cost positioning, yet polyester’s superior oxygen-barrier performance is pulling healthcare and premium food brands into new laminate structures. Print-service providers are investing in hybrid flexo-digital presses that shorten lead times and cut changeover waste, and ink manufacturers are accelerating the rollout of photoinitiator-free UV-curable systems that satisfy stricter migration limits. Regionally, rapid capacity additions in India and Saudi Arabia signal a shift in supply hubs, but North America and Europe still command higher average selling prices because of tighter compliance requirements.

Key Report Takeaways

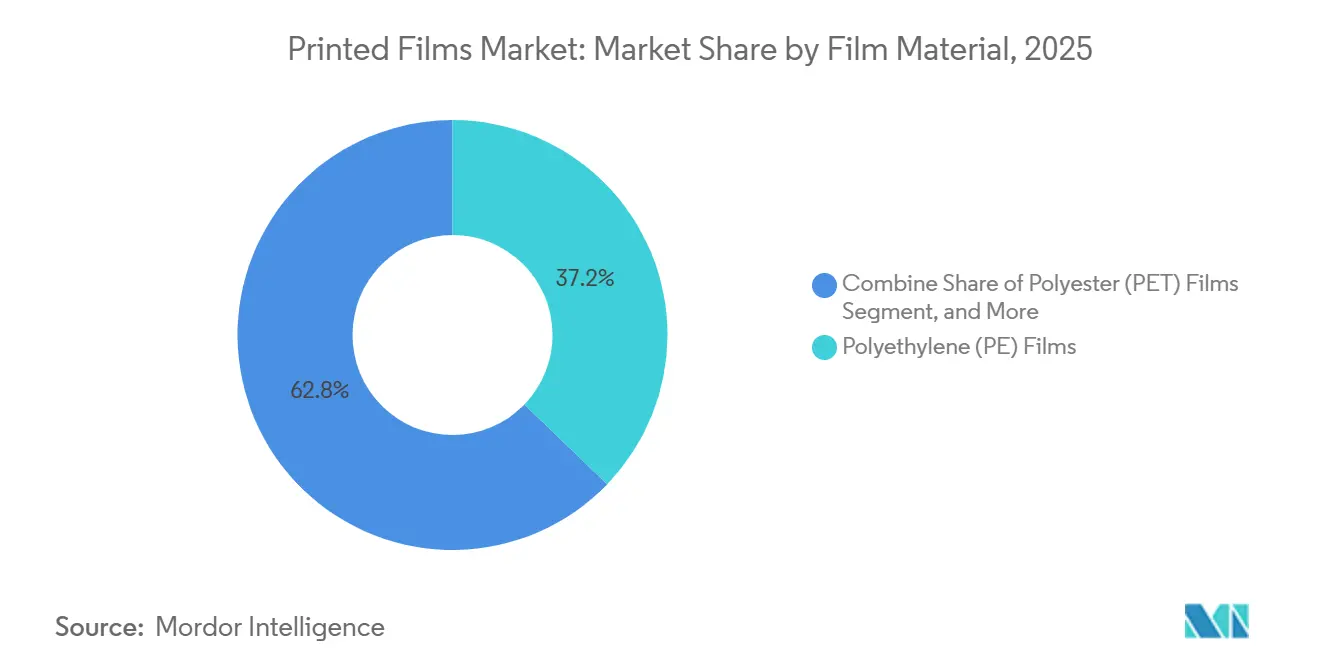

- By film material, polyethylene led with 37.22% of printed films market share in 2025, while polyester is forecast to grow at a 3.61% CAGR through 2031.

- By printing technology, flexographic printing accounted for 41.82% of printed films market share in 2025, whereas digital inkjet is projected to record the fastest 3.75% CAGR to 2031.

- By printing ink type, solvent-based inks retained 40.08% of printed films market share in 2025, and UV/EB-curable formulations are predicted to expand at a 4.01% CAGR over 2026-2031.

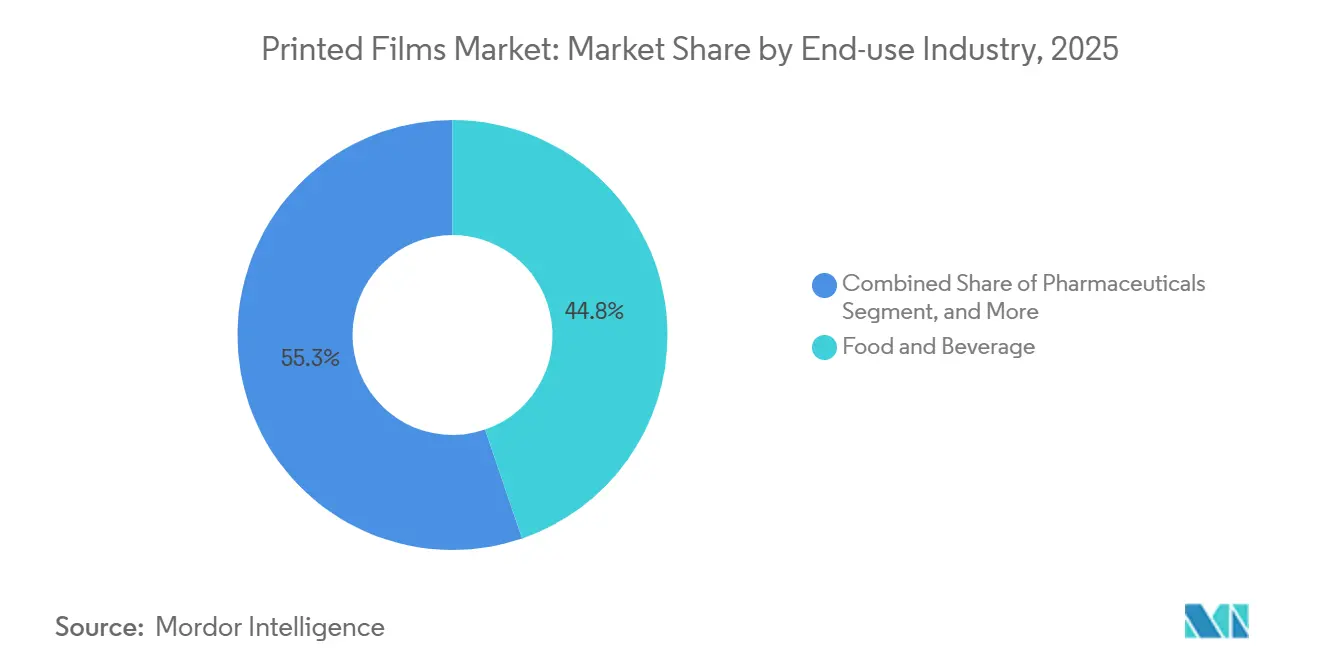

- By end-user industry, food and beverage held 44.75% of printed films market share in 2025, while pharmaceuticals are anticipated to post the highest 4.22% CAGR through 2031.

- By film thickness, the 25-50 µm range captured 39.54% of printed films market share in 2025, yet gauges below 25 µm should advance at a 3.85% CAGR during the forecast window.

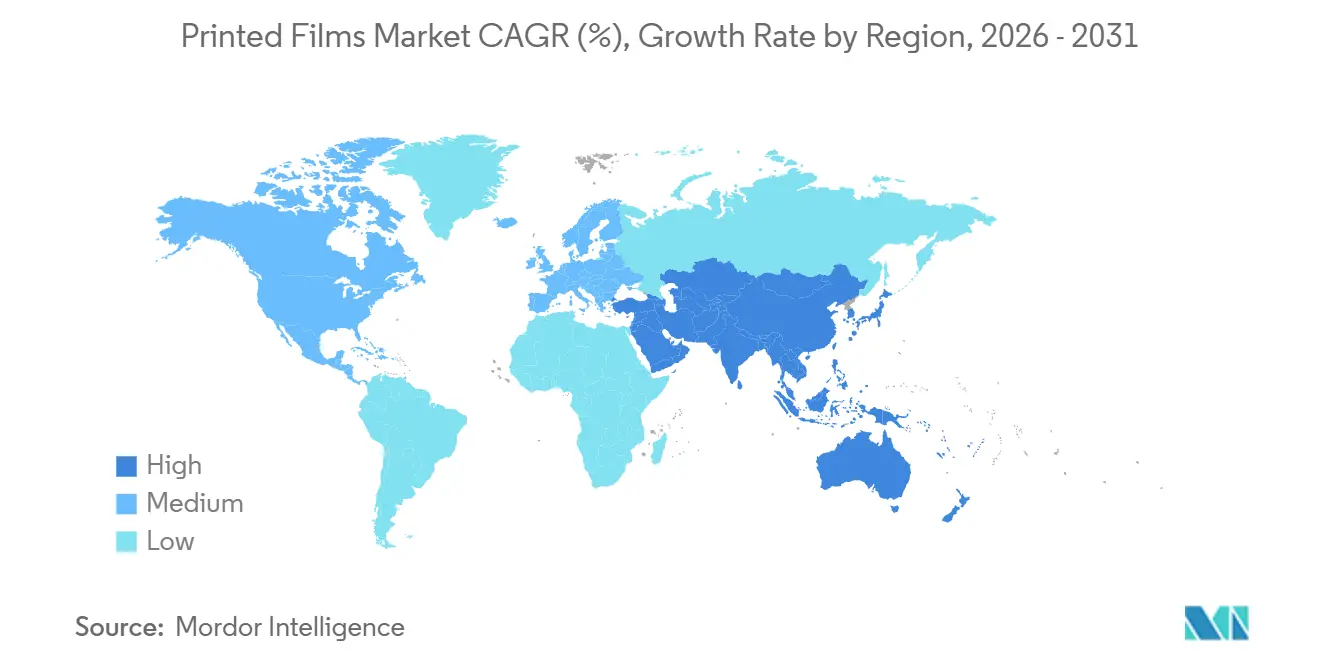

- By geography, Asia-Pacific generated 34.17% of printed films market share in 2025, and the Middle East is expected to be the fastest-growing region at a 3.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Printed Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Packaging Solutions | +1.2% | Global - strongest in Europe and North America | Medium term (2-4 yearss |

| Growth of E-Commerce Boosting Protective Printed Films | +0.9% | Global - urban corridors in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Advancements in High-Resolution Digital Printing Technologies | +0.7% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing Adoption of Smart and Interactive Packaging | +0.5% | Premium segments in North America and Europe | Long term (≥ 4 years) |

| Rapid Expansion of Printed Electronics on Flexible Substrates | +0.3% | Asia-Pacific manufacturing clusters | Long term (≥ 4 years) |

| Stringent Regulations Driving Biodegradable Printed Film Usage | +0.4% | Europe and selected North American states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Packaging Solutions

Brand procurement contracts now embed circularity clauses that oblige converters to certify bio-based content and recyclability. CARBIOS secured US food-contact clearance in 2025 for enzymatically recycled polylactic-acid films, enabling closed-loop recovery without downcycling.[1]CARBIOS, “FDA Food-Contact Clearance for Enzymatically Recycled PLA Film,” carbios.com Metalvuoto’s bio-based barrier coating on PLA substrates delivers oxygen transmission below 5 cc/m²/day and extends produce shelf life by 40%. The EU Packaging and Packaging Waste Regulation, effective in 2026, introduces monetary penalties for non-compliant flexibles, prompting rapid substrate reformulation and boosting the adoption of sustainable printed films.

Growth of E-Commerce Boosting Protective Printed Films

Global parcel volumes reached 150 billion in 2025, each typically wrapped in 1.8 layers of film. Converters answered with high-impact polyethylene mailers that withstand >400 g-force puncture tests yet accept water-based flexo inks. Automated fulfillment centers favor coextruded slip layers with a 0.18 coefficient of friction to enable sortation belts to move 8,000 parcels per hour. Digital presses that swap graphics within 10 minutes support small promotional batches, aligning with same-day-delivery demands and sustaining market penetration of printed films in logistics packaging.

Advancements in High-Resolution Digital Printing Technologies

Inkjet presses now run at 1,200 dpi and >100 m/min, removing the need for expensive rotogravure cylinders from the cost equation. HP Indigo’s 25K platform matches gravure’s optical density on metalized polyester while integrating inline corona treatment, and Konica Minolta’s 400 MHz piezo heads jet 12 pL drops of water-based ink to eliminate volatile solvents. Hybrid configurations, such as Windmoeller and Hoelscher’s Novoflex, apply flexo spot colors at 600 m/min and variable data at 150 m/min, balancing cost efficiency with the personalization needs that shape the printed films market.

Increasing Adoption of Smart and Interactive Packaging

NFC tags and RFID inlays embedded in film structures now authenticate goods, log cold-chain breaches, and unlock digital experiences. Avery Dennison shipped more than 10 billion RFID-enabled pouches in 2025, and Pragmatic Semiconductor’s sub-USD 0.01 FlexIC chips enable disposable tamper-evident seals. Wine brands deploying NFC shrink sleeves have seen counterfeit complaints drop and consumer engagement rise, reinforcing the printed films market’s move toward interactive formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices for Printing Inks and Films | -0.8% | Global - highest in import-dependent regions | Short term (≤ 2 years) |

| Environmental Concerns Regarding Plastic Waste Management | -0.5% | Global - acute in coastal Asia-Pacific and Europe | Medium term (2-4 years) |

| High Initial Capital Investment in Advanced Printing Presses | -0.3% | Emerging markets and SME converters | Long term (≥ 4 years) |

| Supply Chain Disruptions Affecting Specialty Substrates | -0.2% | Global - key Middle East and Asia-Pacific routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices for Printing Inks and Films

Polyethylene swung from USD 950/t to USD 1,320/t in 2025 on Middle East outages and China cracker shutdowns, slashing converter margins. Titanium dioxide climbed 18% YoY to USD 3,200/t in early 2026, inflating white-ink costs. Converters with captive resin or pigment facilities, such as Uflex, enjoy a 200-250 bp margin cushion, yet many independents are forced into quarterly repricing, limiting predictable investment in the printed films market.

Environmental Concerns Regarding Plastic Waste Management

Only 30% of waste systems in emerging economies can process compostable films, creating a gap between biodegradable claims and actual end-of-life outcomes. California’s SB 343 now bans recyclability symbols on flexibles lacking statewide collection, while the EU’s Single-Use Plastics Directive adds producer fees of EUR 0.50-1.20/kg for non-recyclables.[2]California Legislative Information, “SB 343 – Environmental Advertising: Recycling Symbol,” leginfo.legislature.ca.gov Rising scrutiny is nudging buyers toward mono-material designs, but infrastructure shortcomings still restrain the wider market uptake of advanced biopolymers in printed films.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Material: Polyester Gains on Barrier Performance

Polyethylene accounted for 37.22% of 2025 revenue, yet polyester is on track to outpace the printed films market at a 3.61% CAGR, buoyed by pharmaceutical and high-barrier food formats that demand oxygen levels below 3 cc/m²/day. Toray’s aluminum-oxide-coated PET delivers 0.8 cc/m²/day at 12 µm yet remains transparent, a specification low-density polyethylene cannot match without multilayer complexity. Polypropylene remains essential wherever heat-seal strength above 2.5 N/15 mm is required, while PVC’s share continues to erode in food-contact applications due to phthalate bans. Emerging biopolymers currently have only mid-single-digit value but serve as a testbed for circularity pilots and keep the printed films market narrative around sustainability alive.

Cost-effective downgauging strategies are reinforcing polyester uptake. Innovia’s nano-porous BOPP allows lettuce and berries to breathe without laser perforation, and Cosmo First’s anti-fog PET keeps refrigerated pouches clear for a three-week shelf life. With regulators capping overall migration at 10 mg/dm² in the EU, demand for food-grade resins with full traceability is increasing, positioning specialty PET grades as credible challengers to incumbent polyolefins within the printed films industry.

By Printing Technology: Digital Inkjet Erodes Flexo’s Volume Dominance

Flexo accounted for 41.82% share of 2025 revenue, but inkjet’s 3.75% CAGR signals an inflection. Digital presses eliminate plate-mount downtime and run 500-meter jobs profitably, making them perfect for regional promotions and SKU proliferation. Windmoeller and Hoelscher’s hybrid unit integrates flexo stations for static branding and inkjet heads for serialized QR codes, reducing cost per thousand impressions across mixed portfolios. Rotogravure remains relevant for snack and tobacco films exceeding 1 million meters, where cylinder costs amortize efficiently, and color variation must remain within ±1 ΔE.

Ongoing innovation keeps flexo competitive. Bobst’s M6 line automatically registers plates and curtails setup scrap by 40%, narrowing waste differentials versus digital. Meanwhile, the printed films market for screen and pad technologies remains niche, focusing on conductive tracks and specialized tamper seals. Across print platforms, converters are weighing capital outlay against run-length flexibility, a trade-off that shapes future equipment purchases throughout the printed films industry.

By Printing Ink Type: UV-Curable Formulations Capture Low-Migration Premium

Solvent inks dominated in 2025 with a 40.08% share, owing to their compatibility with legacy lines, yet UV/EB systems should eclipse the growth of the printed films market, advancing 4.01% annually. Flint Group’s dual-cure LED product cures PLA substrates at 150 m/min while trimming energy use 70%. Toyo Ink’s Swiss-compliant formulations keep residual photoinitiators below 5 ppb after 6 months, securing shelf-stable yogurt and confectionery contracts. Water-based inks are gaining ground in non-film laminates, and their <25% VOC profiles are also gaining traction as air-quality rules tighten.

Bio-based resin chemistries continue to emerge. Covestro’s 90%-renewable polyurethane binder matches the adhesion of fossil analogs at a surface tension of 42 dyn/cm. Electron-beam inks remain niche but critical for foil snack pouches that require total elimination of photoinitiators. Even so, solvent systems priced at USD 4.50-6.00/kg remain entrenched in agriculture and industrial films, where migration limits are less stringent, and the printed films market is driven by low cost.

By End-User Industry: Pharmaceutical Serialization Drives Above-Market Growth

Food and Beverages accounted for the largest market share of 44.75%, as printed films stand out as a cost-effective, functional, and marketing choice for packaging food products. Healthcare mandates under the EU Falsified Medicines Directive and U.S. DSCSA elevate high-resolution code requirements, propelling pharmaceuticals at a 4.22% CAGR. Vision systems now inspect 400 cartons per minute, rejecting packages with contrast below 1.5. Tamper-evident delamination films from Avery Dennison deter counterfeiters targeting a USD 200 billion black market.

In contrast, food and beverage retain bulk volume, demanding low-seal-initiation films for high-speed form-fill-seal lines and moisture barriers that keep bakery products crisp. Cosmetics rely on metalized holographic finishes to convey premium cues, and home care brands favor chemical-resistant polyethylene. Specialty niches, seed treatment pouches, static-dissipative electronics wraps, total single-digit share but offer double-digit margins, affirming the printed films market's diversity beyond mass consumer goods.

By Film Thickness: Ultra-Thin Gauges Enable Lightweighting

Standard 25-50 µm films with 39.54% market share, balance strength and economics, yet sub-25 µm gauges are growing faster at 3.85% CAGR as converters shave 15-20% resin per unit. Innovia’s 20 µm BOPP meets 450 g puncture tests, translating to USD 0.08-0.12/kg savings for high-volume snack programs. Toray’s 12 µm PET blister foil slashes the weight of the PVC-PVDC laminate while keeping oxygen below 1 cc/m²/day, satisfying ICH Q1A stability requirements.[3]California Legislative Information, “SB 343 – Environmental Advertising: Recycling Symbol,” leginfo.legislature.ca.gov

Ultra-thin webs raise run-ability challenges; presses now deploy real-time tension control and chill rolls to curb wrinkling at >300 m/min, allowing the printed films market to tap light-weighting benefits without sacrificing throughput. Heavier films remain indispensable for industrial sacks and retort pouches that must endure 121 °C sterilization. Agricultural silage wraps in the 50-100 µm bracket need UV stabilization for 2,000 h outdoor exposure, underscoring the breadth of mechanical demands that printed films must satisfy across end markets.

Geography Analysis

Asia-Pacific accounted for 34.17% of the printed films market, anchored by India’s 81,200 tpa line from Cosmo First and Jindal Poly Films’ INR 700 crore (USD 84 million) expansion, which together reinforce regional leadership in BOPP and BOPET supply. China’s domestic demand for e-commerce mailers grew at mid-single-digit rates despite resin shortages, while Japan’s converters focused on export-oriented pharmaceutical applications that require stringent migration controls.[4]Toray Industries, “High-Barrier PET Films with Aluminum-Oxide Vapor Deposition,” toray.com Southeast Asian nations captured follow-on investment in specialty laminates, adding to the depth of the printed films market across the region.

North America and Europe jointly captured nearly one-half of global value, driven by higher selling prices for low-migration and recyclability-compliant films. Amcor’s USD 24 billion revenue base after merging with Berry Global accentuates consolidation, and Mondi’s EUR 1.2 billion (USD 1.34 billion) capex program increases mono-material stand-up pouch output. The EU Packaging Regulation, taking effect in 2026, spurs redesigns toward recyclable structures, an imperative that sustains the printed films market size in mature economies.

The Middle East is expected to post the fastest CAGR of 3.96% through 2031, as GulfPack’s 135,000 tpa BOPP line positions Saudi Arabia as a re-export platform to Africa and South Asia. South America holds high potential but faces currency volatility that tempers capital spending, while Africa remains largely import-dependent, with South Africa and Egypt hosting regional hubs that serve basic flexible packaging needs.

Competitive Landscape

The market is moderately fragmented, with major players such as Amcor, Sealed Air, Mondi, Huhtamaki, and Constantia Flexibles holding a significant share of global capacity. This leaves considerable opportunities for regional specialists to establish their presence and compete effectively. Amcor’s USD 8.4 billion acquisition of Berry Global has led to some European divestitures, which were necessary to comply with regulatory requirements. However, this strategic move has strengthened Amcor’s global scale efficiencies, enabling the company to optimize its operations and expand its market reach.[5]Cosmo Films, “Shendra BOPP Capacity Expansion,” cosmofilms.com

Vertically integrated groups like Uflex, with captive resin, ink, and metallization capabilities, consistently outperform competitors on margins, particularly during periods of feedstock price volatility. These companies benefit from their ability to control multiple stages of the production process, ensuring cost efficiency and supply chain stability. Meanwhile, technology investments are creating a divide within the market. Players adopting hybrid flexo-digital printing lines and LED-UV curing technologies are gaining a competitive edge by meeting demand for short-run, high-margin stock-keeping units (SKUs). In contrast, gravure-centric shops are increasingly facing pricing pressures as brands prioritize agility and faster turnaround times.

Innovation pipelines across the industry remain robust, with companies actively pursuing advancements to maintain their competitive positioning. For instance, Toray filed 14 patents for high-barrier PET technologies in 2025, while Flint Group secured 9 patents for photoinitiator-free UV inks, demonstrating its commitment to developing cutting-edge solutions. Additionally, Pragmatic Semiconductor is commercializing printed silicon chips for smart seals priced at less than USD 0.01, which could revolutionize cost-effective smart packaging solutions. Sustainability remains a critical differentiator in the market. CARBIOS’s enzymatic PLA recycling loop, which meets stringent circularity key performance indicators (KPIs), is enabling converters to attract eco-conscious brands. As the printed films market increasingly shifts toward closed material cycles, such innovations are expected to play a pivotal role in shaping the industry's future.

Printed Films Industry Leaders

Sealed Air Corporation

Amcor plc

Huhtamaki Oyj

Mondi plc

Constantia Flexibles Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Innovia Films unveiled P2G, a recyclable BOPP film with high gas exchange for fresh produce, extending shelf life by 30%.

- November 2025: Uflex invested INR 700 crore (USD 84 million) in Dharwad for new BOPP and metallization capacity.

- September 2025: Konica Minolta released 12 pL water-based inkjet heads operating at 400 MHz, targeting flexible-packaging installations in Europe and North America.

- January 2025: American Packaging Corporation commissioned two HP Indigo 200K presses at its Wisconsin hub to meet demand for short-run, flexible packaging.

Global Printed Films Market Report Scope

The Printed Films Market encompasses the global industry that produces, prints, and distributes flexible films with printed graphics, text, and functional information for packaging, labeling, branding, and protective applications. These films are widely used across consumer goods and industrial sectors to enhance product visibility, communication, and shelf appeal while maintaining material performance and durability.

The Printed Films Market Report is Segmented by Film Material (Polyethylene Films, Polypropylene Films, Polyester Films, Polyvinyl Chloride Films, and Other Film Materials), Printing Technology (Flexographic Printing, Rotogravure Printing, Digital Inkjet Printing, and Other Printing Technologies), Printing Ink Type (Solvent-based Inks, Water-based Inks, UV/EB-curable Inks, and Other Printing Ink Types), End-user Industry (Food and Beverage, Personal Care and Cosmetics, Pharmaceuticals, Homecare and Cleaning, and Other End-user Industries), Film Thickness (Up to 25 µm, 25 - 50 µm, 50 - 100 µm, and Above 100 µm), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Polyethylene (PE) Films |

| Polypropylene (PP) Films |

| Polyester (PET) Films |

| Polyvinyl Chloride (PVC) Films |

| Other Film Materials |

| Flexographic Printing |

| Rotogravure Printing |

| Digital Inkjet Printing |

| Other Printing Technologies |

| Solvent-based Inks |

| Water-based Inks |

| UV/EB-curable Inks |

| Other Printing Ink Types |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Homecare and Cleaning |

| Other End-user Industries |

| Up to 25 µm |

| 25 - 50 µm |

| 50 -100 µm |

| Above 100 µm |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Film Material | Polyethylene (PE) Films | |

| Polypropylene (PP) Films | ||

| Polyester (PET) Films | ||

| Polyvinyl Chloride (PVC) Films | ||

| Other Film Materials | ||

| By Printing Technology | Flexographic Printing | |

| Rotogravure Printing | ||

| Digital Inkjet Printing | ||

| Other Printing Technologies | ||

| By Printing Ink Type | Solvent-based Inks | |

| Water-based Inks | ||

| UV/EB-curable Inks | ||

| Other Printing Ink Types | ||

| By End-user Industry | Food and Beverage | |

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| Homecare and Cleaning | ||

| Other End-user Industries | ||

| By Film Thickness | Up to 25 µm | |

| 25 - 50 µm | ||

| 50 -100 µm | ||

| Above 100 µm | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current printed films market size and where is it headed by 2031?

The printed films market size stands at USD 7.47 billion in 2026 and is projected to reach USD 8.91 billion by 2031, reflecting a 3.59% CAGR, according to Mordor Intelligence.

Which film material is expanding fastest within printed packaging?

Polyester films are forecast to register a 3.61% CAGR through 2031 on the back of superior oxygen-barrier performance, especially for pharmaceuticals and premium food.

How quickly is digital printing gaining share over flexo?

Digital inkjet printing is expected to grow at 3.75% annually during 2026-2031 as converters favor short-run agility and variable-data capability.

Why is the Middle East considered a high-growth regional market?

Capacity expansions such as GulfPack's 135,000 tpa BOPP line in Saudi Arabia enable re-exports into Africa and South Asia, driving a regional CAGR of 3.96% through 2031.

Which end-user industry is likely to outperform overall market growth?

Pharmaceuticals should grow at a 4.22% CAGR because global serialization mandates require high-resolution printed codes and tamper-evident films.

What factors most threaten printed film converters margins in the near term?

Volatile resin and pigment prices, alongside tightening environmental fees for non-recyclable films, compress operating margins unless converters hold captive raw-material capacity.

Page last updated on: