Large Format Printing Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

|---|---|

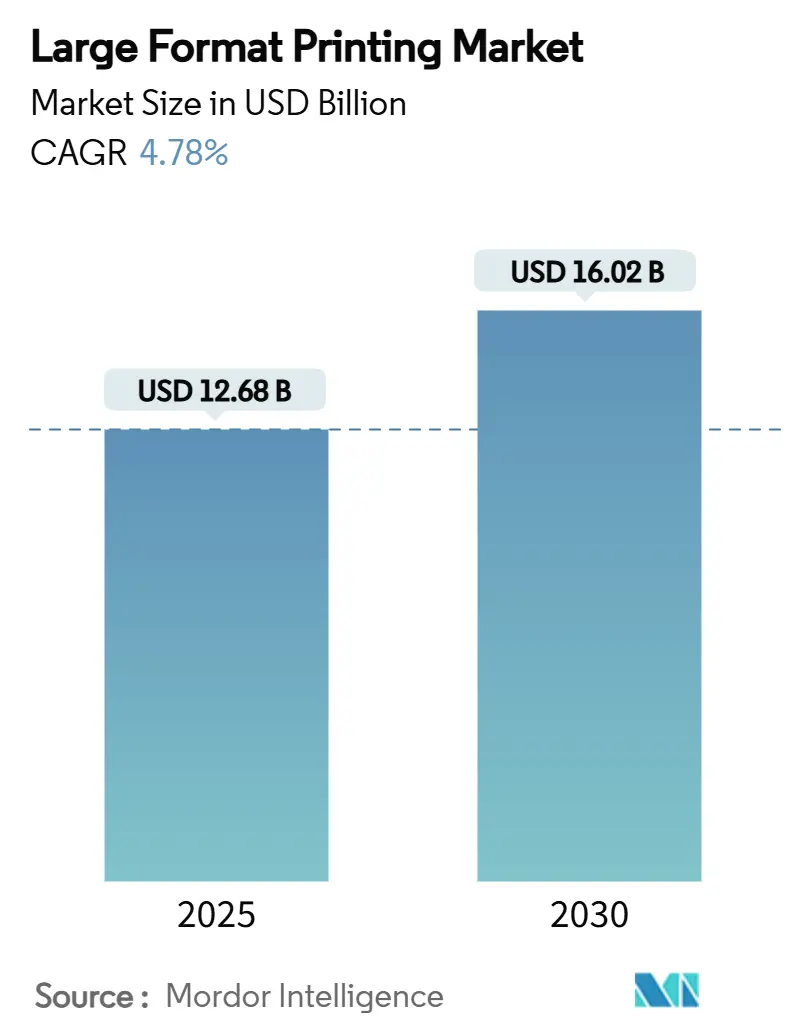

| Market Size (2025) | USD 12.68 Billion |

| Market Size (2030) | USD 16.02 Billion |

| Growth Rate (2025 - 2030) | 4.78% CAGR |

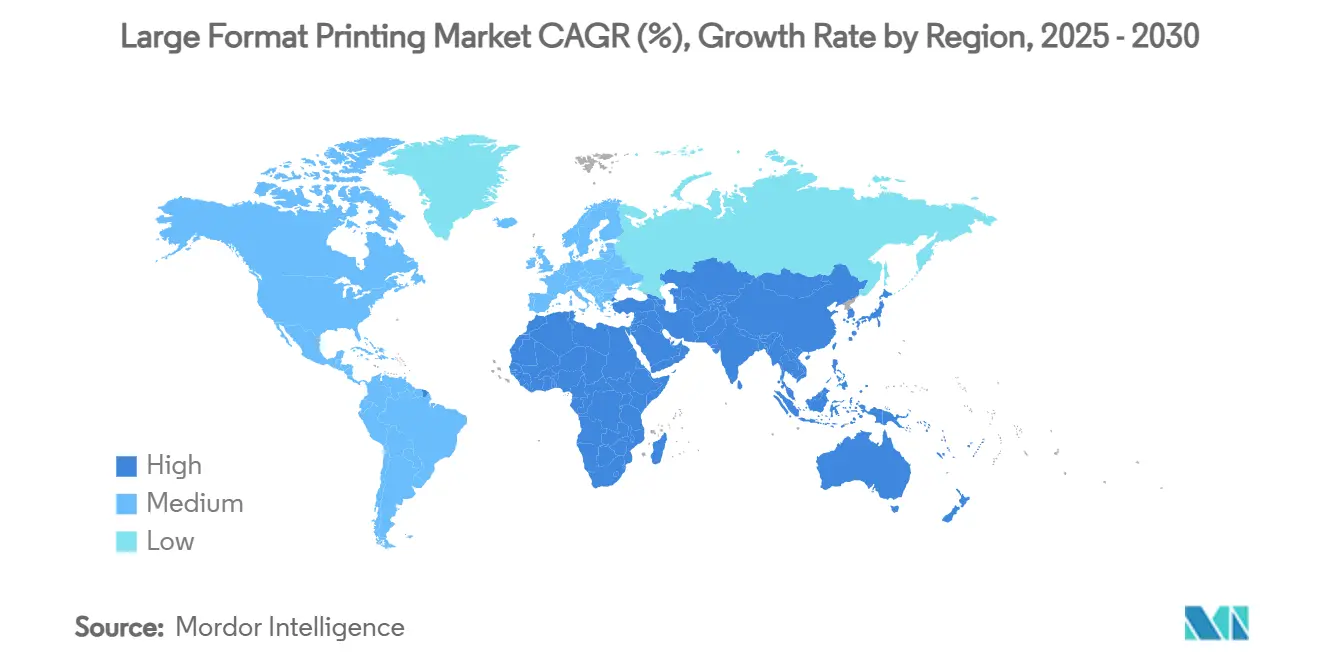

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

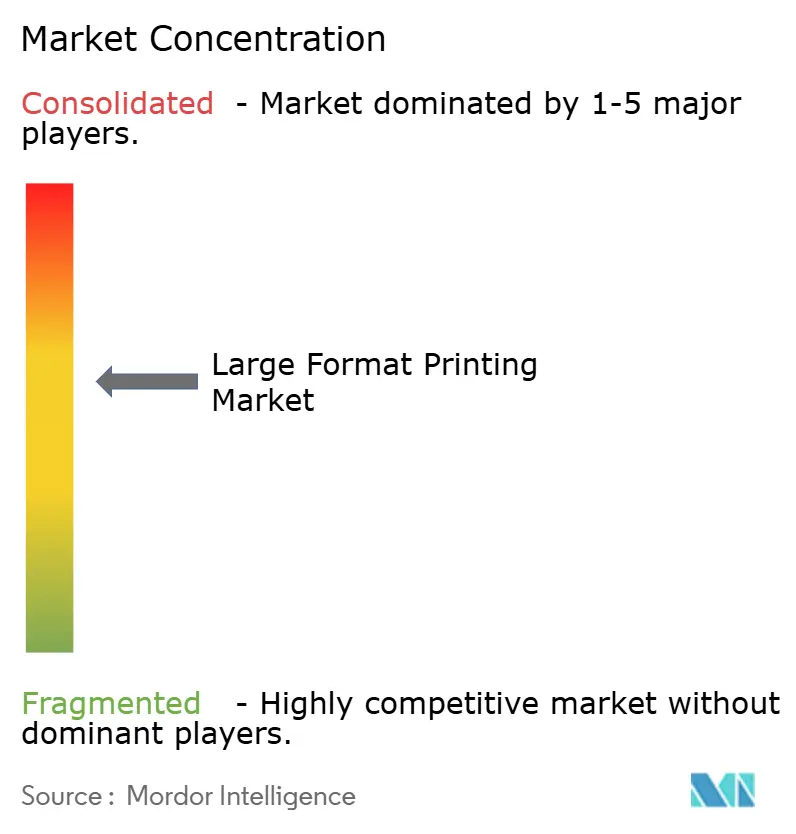

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Large Format Printing Market Analysis by Mordor Intelligence

The large format printing market stood at USD 12.68 billion in 2025 and is forecast to reach USD 16.02 billion by 2030 with a 4.78% CAGR, underscoring a solid growth runway despite tightening sustainability rules and rising capital costs. The market’s expansion rides on three structural shifts: global mandates that cap volatile-organic-compound emissions, rapid substitution of solvent systems by UV-curable and latex chemistries, and a wave of AI-enabled raster-image-processing tools that cut ink consumption and turnaround time. Brands now pair fleet electrification with vehicle-wrap campaigns, while web-to-print workflows push customized décor into mainstream retail. Supply chain shocks in specialty films and the ascent of digital-out-of-home LED panels temper near-term print volumes, yet broader demand for soft signage, wallcoverings, and textile prints keeps the large format printing market firmly on an upward trajectory.[1]European Union, “Reducing the Emissions of Volatile Organic Compounds (VOCs),” EUR-Lex, eur-lex.europa.eu

Key Report Takeaways

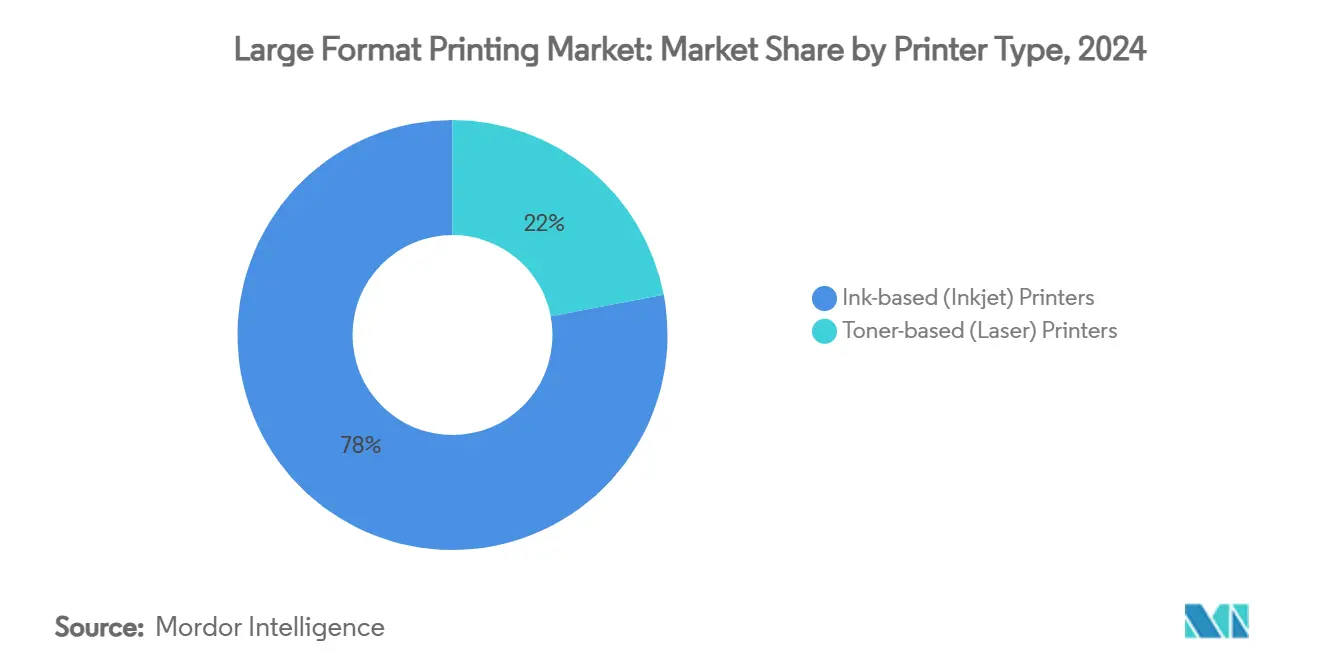

- By printer type, inkjet systems commanded 78% of the large format printing market share in 2024, while toner-based laser units are projected to expand at a 7.55% CAGR through 2030.

- By ink type, eco-solvent formulations held 32% share of the large format printing market size in 2024, whereas UV-curable inks are forecast to advance at a 7.90% CAGR to 2030.

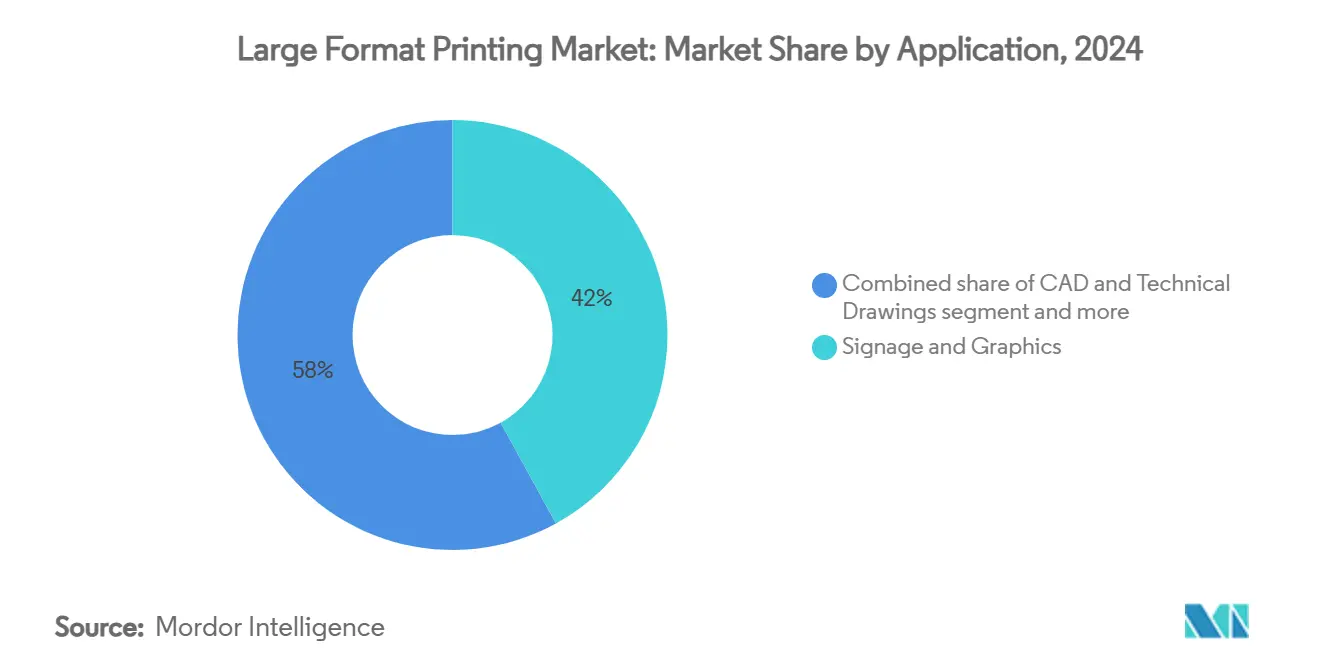

- By application, signage and graphics led with a 42% revenue share in 2024; textile and apparel printing is expected to post the fastest 8.60% CAGR during the outlook period.

- By print width, 44"–60" equipment accounted for 37% of the large format printing market size in 2024 and grand-format systems above 72" are set to accelerate at an 8.11% CAGR.

- By geography, North America contributed 34% market revenue in 2024, while Asia-Pacific is on track for a 6.50% CAGR through 2030.

Global Large Format Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand surge for soft signage and textile advertising | 1.20% | Global, with strong growth in APAC and North America | Medium term (2-4 years) |

| Shift toward UV-curable and latex, reducing VOCs | 0.90% | Europe & North America core, expanding to APAC | Long term (≥ 4 years) |

| Web-to-print mass-custom décor growth | 0.70% | North America & Europe, emerging in urban APAC | Medium term (2-4 years) |

| AI-driven RIP software for ink and workflow optimization | 0.50% | Global, led by technology-advanced markets | Short term (≤ 2 years) |

| Green-building VOC mandates boosting wallcovering prints | 0.40% | Europe & North America, selective APAC markets | Long term (≥ 4 years) |

| Fleet electrification expanding vehicle-wrap ad real-estate | 0.30% | Global, accelerated in EV-adoption regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Electrification Expanding Vehicle-Wrap Ad Real Estate

EV platforms eliminate tail-pipes and rooftop exhausts, giving designers uninterrupted surface real estate. Municipal bus agencies adopt full-body wraps that integrate QR codes for mobile engagement, and private fleets monetize vehicles as moving billboards. Complementary over-laminates extend graphic lifespan in harsh climates, which secures annuity orders for replacement wraps.

Shift Toward UV-Curable and Latex, Reducing VOCs

Europe’s enforcement of Directive 1999/13/EC forces print shops to retire legacy solvent lines, propelling UV and latex adoption. Instant curing eliminates idle drying racks, freeing floor space, while odor-free output meets indoor-air-quality codes in schools and hospitals. OEMs bundle low-energy LED lamps that extend bulb life and reduce heat, enabling prints on heat-sensitive films and recycled boards.[2]UV Printing Benefits and Applications,” American Printer, americanprinter.com

Web-to-Print Mass-Custom Décor Growth

E-commerce storefronts connect consumer uploads to automated RIP queues, enabling one-off wallpaper rolls, canvas art, and window films. HP forecasts digitally printed wallcoverings to exceed USD 10.4 billion by 2025 as 85% of service providers cite customer pressure for sustainable substrates. The model slashes dead stock and taps long-tail design demand, turning print runs of one into profitable orders.

AI-Driven RIP Software for Ink and Workflow Optimization

Artificial-intelligence modules in modern RIPs predict nozzle outages, balance CMYK loads, and arrange step-and-repeat impositions that shave media waste by double-digit percentages. Esko’s Phoenix engine analyses file geometry to pick the most efficient print-cut path, while Roland DG’s DIMENSE plug-in previews 3D textures before a single drop lands, compressing proof cycles and offsetting a 73% decline in skilled press operators since 2006.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership of industrial LFP systems | -0.80% | Global, particularly impacting SME adoption | Medium term (2-4 years) |

| Digital-out-of-home LED cannibalising banner demand | -0.60% | Global, accelerated in urban markets | Short term (≤ 2 years) |

| Supply-chain volatility of specialty PET back-lit films | -0.40% | Global, concentrated in Asia-Pacific production | Short term (≤ 2 years) |

| Data-privacy limits on personalised web-to-print campaigns | -0.20% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership of Industrial LFP Systems

Capital layouts for eight-color UV hybrids exceed USD 250,000, and ancillary costs pile on for chillers, exhaust systems, and technician training. Small firms struggle to secure financing, so consolidation accelerates as larger providers absorb independents. Ricoh notes that only 52% of commercial printers have completed digital upgrades, leaving a long tail that risks obsolescence within five years.

Supply-Chain Volatility of Specialty PET Back-Lit Films

Back-lit media relies on a narrow pool of Asian extrusion lines that experienced double-digit resin price spikes in 2024. Allocation quotas disrupt delivery schedules for transit-shelter posters, forcing service providers to carry costly buffer stock or substitute opaque films that alter color output. Currency swings further complicate landed costs for importers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printer Type: Inkjet Dominance Faces Laser Precision Challenge

Inkjet technology generated USD 9.9 billion in 2024 and retained 78% share of the large format printing market through superior colour gamut, substrate range, and evolving low-VOC chemistries. Multi-pass heads now spray at 2-picoliter drops, yielding photo-grade output for photographic and décor segments. In contrast, laser engines captured engineering clients that prize 0.1 mm line fidelity and water-fast blueprints. Toner device shipments are set to grow 7.55% annually to 2030 as architecture and construction firms migrate from monochrome LED plotters to colour laser platforms. The long-term outlook shows coexistence, with laser’s share inching upward while inkjet defends breadth of applications.

The consumables equation favours inkjet OEMs because specialized UV and latex inks command premium prices. Laser operators benefit from lower toner costs and predictable maintenance intervals. However, laser’s limited compatibility with thick or textured media constrains expansion into soft signage and décor. Inkjet vendors answer with predictive-maintenance firmware that reduces downtime and auto-cleans nozzles, mitigating earlier reliability issues in high-volume shops.

By Ink Type: Eco-Solvent Leadership Challenged by UV-Curable Innovation

Eco-solvent inks accounted for 32% revenue, but their share will erode as urban air-quality ordinances squeeze permissible VOC levels. UV-curable formulations grow 7.90% yearly thanks to instant cure, scratch resistance, and adhesion on rigid panels. Latex chemistries gain ground among print shops that prefer water-based systems, offering odour-free prints for sensitive interiors. Aqueous pigment lines serve indoor posters and fine art, whereas dye-sublimation inks dominate polyester fabric transfer. Innovation in bio-circular carbon black, such as Orion’s PRINTEX Nature 35, signals future convergence of sustainability and performance.

By Application: Signage Dominance Meets Textile Innovation

Signage and graphics delivered USD 5.3 billion in 2024, translating to 42% of overall revenue, yet textile and apparel will climb fastest at an 8.60% CAGR to 2030. Retailers adopt fabric lightboxes that fold into carry-ons and save freight. Brands pilot made-to-order apparel micro-factories that print, cut, and sew within city centers, reducing transit emissions. Vehicle wraps stay robust, helped by higher-capacity batteries in electric vans that present larger, uninterrupted surface areas for graphics. Packaging prototypes migrate to flatbed UV presses for full-colour comps that reach design reviews within hours.

By Print Width: Mid-Range Stability Versus Grand-Format Growth

Systems in the 44"–60" band generated 37% of 2024 revenue and remain the workhorse of general commercial work. Grand-format engines above 72" will rise 8.11% annually as architects specify single-piece building wraps and entertainment companies order stage backdrops exceeding 10 meters. Mid-range devices blend affordability with throughput, making them the entry point for shops upgrading from desktop plotters. Compact 17"–24" models serve design studios with space limits, while 60"–72" hybrids straddle volume needs of photo labs and short-run décor printers.

Geography Analysis

North America held 34% of the large format printing market in 2024, buoyed by deep advertising spend and early uptake of VOC-compliant inks. Corporate sustainability goals accelerate swap-outs of solvent machines for latex and UV-gel units. Fleet electrification drives a fresh cycle of vehicle-wrap graphics, notably on last-mile delivery vans. The region’s capital intensity encourages mergers, with networks scaling to amortize seven-figure investments in industrial hybrids.

Asia-Pacific will post a 6.50% CAGR through 2030 as textile clusters in China and India digitize to chase micro-lot fashion trends. Regional printing expos report record capital orders, led by Japanese and Korean OEM showcases that highlight inline quality automation. South-East Asian nations attract relocated electronics and consumer-goods factories that demand local packaging proofing services, adding incremental press capacity.

Europe balances mature installed bases with strict ecological legislation that punishes high-solvent emissions. German and Dutch printers trial bio-based substrates that support cradle-to-cradle certification. Italy and Spain tap fashion and décor niches, linking web-to-print storefronts to local production clusters. The European Union’s policy leadership nudges global vendors to embed VOC metrics in product datasheets, ensuring worldwide compliance from a single platform.[3]Rahul Kumar, “PrintPack to Be a Bigger Show Than Ever,” PrintWeek India, printweek.in

Competitive Landscape

The large format printing market shows moderate fragmentation. Tier-one vendors HP, Canon, and Epson leverage global channels and broad portfolios that cover aqueous, solvent, latex, and UV chemistries. Roland DG and Mimaki carve profitable niches in signage and textile segments with application-specific firmware and modular accessories. Durst competes on productivity, bundling robotics for non-stop board feeding. Competitive intensity pivots on sustainable inks, AI-driven workflow, and hybrid roll-to-board architecture.

Strategic alliances reshape sourcing and R&D economics. Konica Minolta and Fujifilm Business Innovation explore joint platforms to consolidate engine development and gain purchasing leverage on mechatronics. Epson’s acquisition of Fiery adds high-performance RIP expertise, tightening integration between printer hardware and colour management. Orion’s bio-circular pigment initiative signals upstream raw-material innovations that could cascade across competitive lines.

OEMs diversify into service models, bundling click-charge contracts that include remote diagnostics, consumables, and scheduled part swaps. Growing appetite for AI-assisted maintenance favours brands with extensive IoT telemetry and cloud security credentials.[4]Konica Minolta and Fujifilm Business Innovation Explore a Potential Strategic Alliance in Multifunction Printer and Printer Areas,” Konica Minolta, konicaminolta.com

Large Format Printing Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corporation

Roland DG Corporation

Mimaki Engineering Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Roland DG Corporation launched the DIMENSE Module for Roland DG Connect Designer, enabling 3D texture preview and automated pattern generation.

- June 2025: Roland DG introduced the VersaSTUDIO BN2-30 solvent inkjet and BD-12 UV flatbed printers, addressing entry-level professional demand.

- May 2025: Roland DG released the TrueVIS XG-640 print-and-cut model targeting 1,890 global unit sales within three years.

- April 2025: Mimaki Engineering unveiled the JV200 series eco-solvent roll printers featuring 40% odor reduction.

Global Large Format Printing Market Report Scope

| Ink-based (Inkjet) Printers |

| Toner-based (Laser) Printers |

| Hardware (Printers) |

| Software and RIP |

| Consumables (Inks, Media) |

| Aqueous |

| Solvent |

| UV-Curable |

| Latex / Resin |

| Dye-Sublimation |

| Aqueous Dye-Based |

| Aqueous Pigment |

| Eco-Solvent |

| UV-Curable |

| Latex |

| Sublimation |

| 17” - 24” |

| 24” - 44” |

| 44” - 60” |

| 60” - 72” |

| More than 72” (Grand-Format) |

| Signage and Graphics |

| CAD and Technical Drawings |

| Textile and Apparel Printing |

| Packaging and Labels |

| Decor and Wallpaper |

| Vehicle Wraps |

| Photographic and Fine-Art |

| Advertising and Marketing Service Providers |

| Textile and Apparel Manufacturers |

| Architecture, Engineering and Construction (AEC) Firms |

| Packaging Converters |

| Photographic Labs and Studios |

| Retail and POP Specialists |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Printer Type | Ink-based (Inkjet) Printers | ||

| Toner-based (Laser) Printers | |||

| By Component | Hardware (Printers) | ||

| Software and RIP | |||

| Consumables (Inks, Media) | |||

| By Print Technology | Aqueous | ||

| Solvent | |||

| UV-Curable | |||

| Latex / Resin | |||

| Dye-Sublimation | |||

| By Ink Type | Aqueous Dye-Based | ||

| Aqueous Pigment | |||

| Eco-Solvent | |||

| UV-Curable | |||

| Latex | |||

| Sublimation | |||

| By Print Width | 17” - 24” | ||

| 24” - 44” | |||

| 44” - 60” | |||

| 60” - 72” | |||

| More than 72” (Grand-Format) | |||

| By Application | Signage and Graphics | ||

| CAD and Technical Drawings | |||

| Textile and Apparel Printing | |||

| Packaging and Labels | |||

| Decor and Wallpaper | |||

| Vehicle Wraps | |||

| Photographic and Fine-Art | |||

| By End-user Industry | Advertising and Marketing Service Providers | ||

| Textile and Apparel Manufacturers | |||

| Architecture, Engineering and Construction (AEC) Firms | |||

| Packaging Converters | |||

| Photographic Labs and Studios | |||

| Retail and POP Specialists | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the large format printing market?

The large format printing market was valued at USD 12.68 billion in 2025.

How fast will the large format printing market grow?

The sector is projected to expand at a 4.78% CAGR, reaching USD 16.02 billion by 2030.

Which printer technology leads the market?

Inkjet systems dominate with 78% 2024 market share, although laser units are the fastest-growing at a 7.55% CAGR.

Why are UV-curable inks gaining popularity?

UV-curable inks meet strict VOC caps, cure instantly, and adhere to varied substrates, driving a 7.90% CAGR through 2030.

Which region will grow the quickest?

Asia-Pacific is forecast to register a 6.50% CAGR due to manufacturing growth and rising demand for customized décor.

What major restraint could limit adoption?

High total cost of ownership for industrial printers remains a key barrier, especially for small and medium enterprises.

Page last updated on: