Security Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

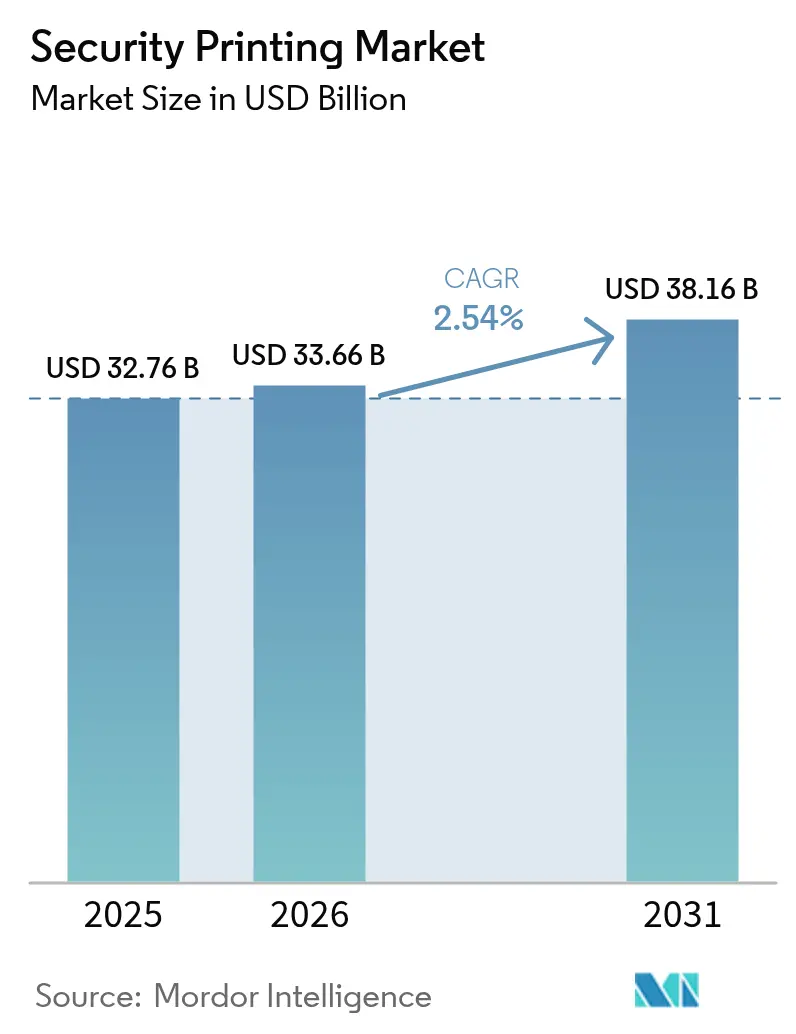

| Market Size (2026) | USD 33.66 Billion |

| Market Size (2031) | USD 38.16 Billion |

| Growth Rate (2026 - 2031) | 2.54% CAGR |

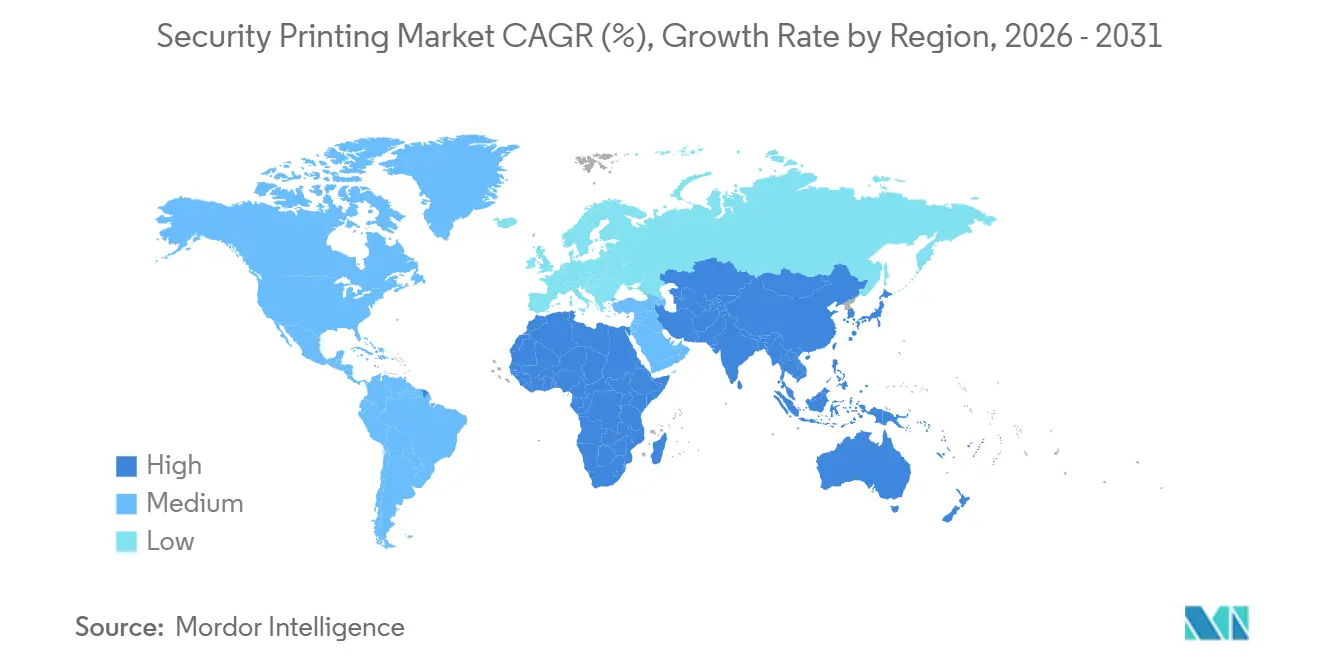

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Printing Market Analysis by Mordor Intelligence

The security printing market size was valued at USD 32.76 billion in 2025 and estimated to grow from USD 33.66 billion in 2026 to reach USD 38.16 billion by 2031, at a CAGR of 2.54% during the forecast period (2026-2031). Persistent counterfeiting pressure on banknotes, passports and tax banderoles is compelling issuers to layer multiple overt, covert and forensic features. Personal identification documents are advancing more quickly than cash, helped by biometric-passport rollouts and national digital-ID programs. Polymer substrates are gaining traction because they last 2.5-4 times longer than cotton paper, trimming lifecycle costs even after factoring in their 30-40% price premium. Contactless authentication via RFID and NFC tags is now a mainstream requirement in passports and secure ID cards, creating fresh demand for inline digital-inkjet personalization. Meanwhile, central-bank “green banknote” policies are nudging suppliers toward recycled cotton, lower-emission inks and solvent-free varnishes, opening a sustainability-linked product niche within the security printing market.

Key Report Takeaways

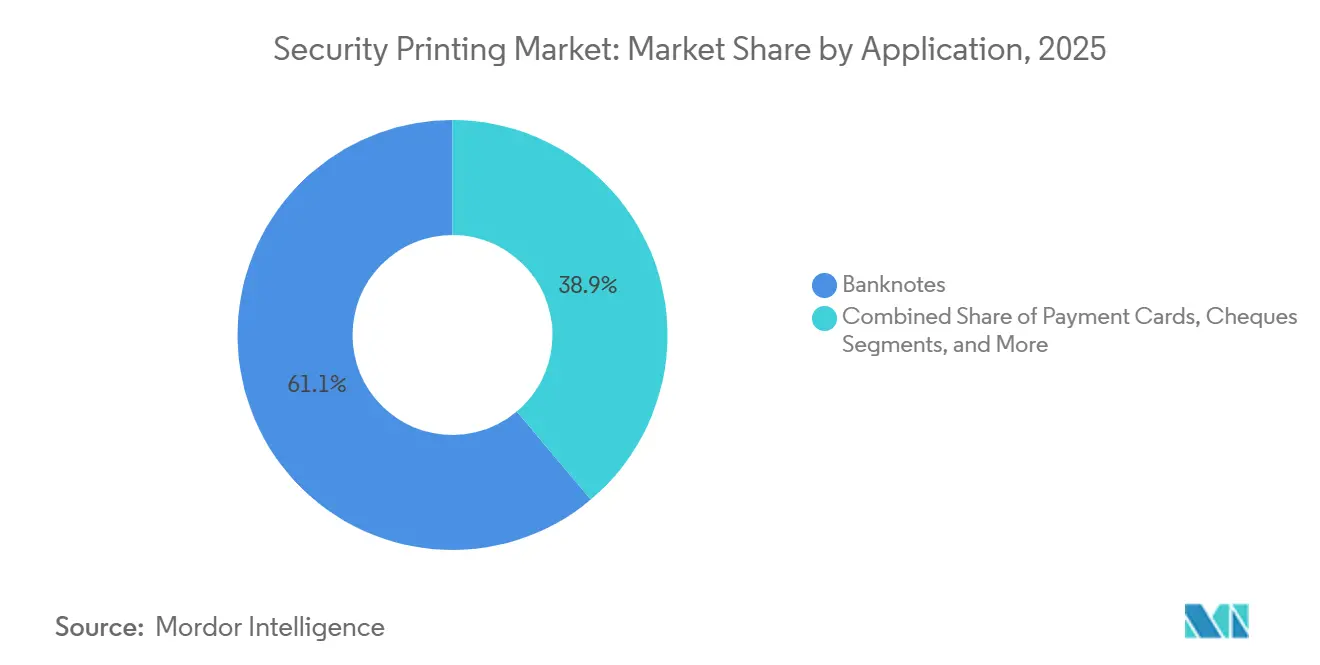

- By application, banknotes led with 61.12% revenue share in 2025, while personal identification documents posted the fastest growth at a 3.88% CAGR through 2031.

- By security feature, security inks commanded 37.21% of the security printing market share in 2025, whereas RFID and NFC tags are projected to expand at a 3.49% CAGR to 2031.

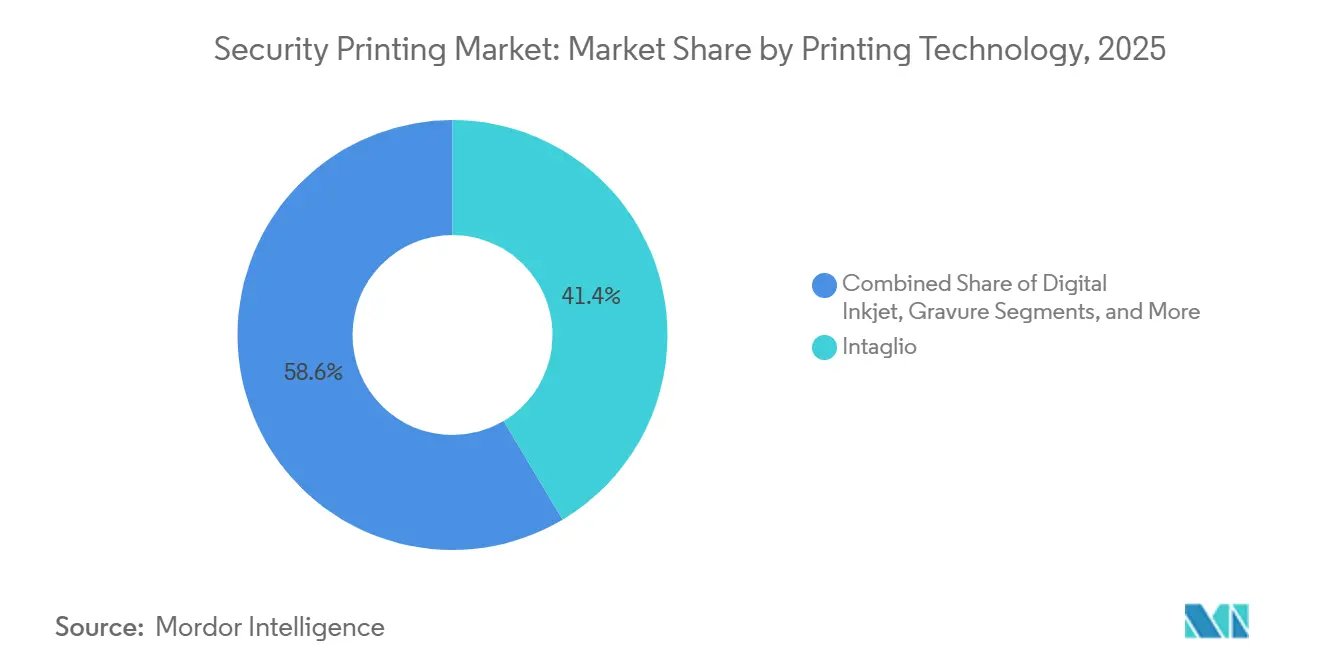

- By printing technology, intaglio accounted for 41.44% of the security printing market size in 2025, yet digital inkjet is forecast to accelerate at a 3.51% CAGR between 2026-2031.

- By substrate, cotton paper retained 47.86% share of the security printing market size in 2025, while polymer substrates are advancing at a 3.29% CAGR through 2031.

- By geography, Asia-Pacific generated 33.12% of 2025 revenue, but Africa is anticipated to be the fastest-growing region at a 3.46% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Forgery and Counterfeiting | +0.8% | Global, acute in Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Government Mandates for Secure IDs and E-Passports | +0.7% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Adoption of Polymer Banknote Substrates | +0.5% | Australia, Canada, United Kingdom, Middle East | Medium term (2-4 years) |

| Growing Circulation of High-Denomination Notes | +0.3% | Asia-Pacific, Middle East, Africa, South America | Long term (≥ 4 years) |

| AI-Enabled Inline Inspection Reduces Spoilage | +0.2% | North America, Europe, advanced Asia-Pacific hubs | Short term (≤ 2 years) |

| Central-Bank “Green Banknote” Programs | +0.2% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Forgery and Counterfeiting

Counterfeit seizures are climbing, spurring faster adoption of optically variable inks, 3D security ribbons and micro-optic threads. The European Central Bank withdrew 554,000 fake euro notes in 2024, equivalent to 18 counterfeits per million genuine notes.[1]European Central Bank, “ECB Reports 554,000 Counterfeit Euro Notes Withdrawn in 2024,” ECB.EUROPA.EU Germany’s Bundesbank registered a 28% annual rise in counterfeits, while the U.S. USD 100 note remains the world’s most forged series.[2]Deutsche Bundesbank, “Counterfeit Detection Statistics 2024,” BUNDESBANK.DE Passport fraud is also persistent, even after the introduction of ICAO-compliant RFID chips, driving continued demand for holographic overlays and laser engraving. Higher-value notes in emerging markets enlarge the payoff for counterfeiters, reinforcing the security-feature arms race.

Government Mandates for Secure IDs and E-Passports

National programs are boosting volume demand for secure polycarbonate data pages, laser engraving and contactless smart-card inlays. India began issuing biometric chip passports in November 2025 with the goal of producing 10 million units per year by 2027.[3]Government of India, “Launch of Biometric Chip Passports,” MEA.GOV.IN The European Union’s eIDAS 2.0 framework obliges member states to deploy digital-ID wallets tied to secure element chips, catalyzing equipment upgrades across 27 authorities. Indonesia’s Home Affairs Ministry selected IDEMIA for a high-volume NIK card contract, while the United States REAL ID deadline of May 2025 kept state driver-license bureaus on a sustained procurement cycle. Mandatory features differ by income tier, splitting the supplier landscape between premium biometric offerings and cost-optimized fraud deterrence.

Adoption of Polymer Banknote Substrates for Durability and Security

Seventy-six countries had shifted to polymer notes by 2025. Australia alone saved USD 1 billion over 25 years through longer note life and fewer replacements. The UAE’s Dh500 polymer note introduced transparent windows with holographic foils, while Canada confirmed it will migrate the CAD 20 note to polymer in 2027. Higher substrate costs and the need for specialized presses temper the speed of adoption, but total cost of ownership still favors polymer in high-circulation markets.

Growing Circulation of High-Denomination Banknotes in Emerging Markets

Cash-intensive economies continue to issue larger-value notes as digital infrastructure lags. Nigeria had 2.7 trillion naira in circulation by 2024 despite a mobile-money surge. India counted 140 billion notes outstanding in 2025, while China prints more than 90 billion notes annually. New issues in Somalia and the BEAC region reflect a broader pattern of redesigns aimed at shoring up public trust. Developed markets show the opposite trend, with Sweden’s cash transactions now below 10% of retail payments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Cashless Payments and CBDCs | -0.6% | Europe, North America, urban Asia-Pacific | Medium term (2-4 years) |

| High Capex for Next-Gen Security Presses | -0.4% | Africa, South America, smaller central banks | Long term (≥ 4 years) |

| Shortages of Specialty Inks and Substrates | -0.3% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Carbon-Footprint Scrutiny of Currency Production | -0.2% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Cashless Payments and CBDCs

Digital alternatives are eroding long-run demand for physical currency in high-income markets. Ninety-four percent of central banks surveyed by the BIS were researching CBDCs in 2024, with retail launches expected within six years. Sweden’s e-krona tests and the European Central Bank’s digital euro project foreshadow double-digit contractions in banknote volumes by 2035. China’s e-CNY has amassed 260 million wallets, although rural cash reliance tempers the impact. Everywhere that contactless payments take hold, paper tickets and cheques disappear, forcing printers to pivot toward identity documents and brand-protection labels.

High Capex for Next-Gen Security Presses

A single Komori Chambon S-6 intaglio press costs USD 15-25 million, with 18-36 month lead times. Koenig and Bauer’s NotaSys systems range from EUR 20-30 million (USD 22-33 million) once inspection modules are included. These outlays strain smaller central banks; Ethiopia’s 2025 e-passport plant required concessional financing to proceed. Digital inkjet equipment is cheaper but often fails to deliver the tactile depth or chemical durability that regulators demand for banknotes, slowing technology diffusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Personal-ID Momentum Offsets Slower Cash

Banknotes generated the largest slice of the security printing market in 2025, yet personal identification documents are growing faster and reshaping capital investment priorities. Large passport tenders in India, France and the United Kingdom locked in multi-year demand for chip-inlay assembly lines, laser engraving and polycarbonate lamination. The security printing market size for ID documents is benefiting from eIDAS 2.0 in Europe and rising KYC requirements in Asia, encouraging suppliers to expand regional card-personalization hubs. Meanwhile, cheque printing is in structural decline after volumes in the United Kingdom dropped from 3.9 billion in 1990 to 219 million in 2023. Transit ticketing is migrating to NFC-enabled smartphones, but brand-protection banderoles for tobacco and alcohol are expanding as regulators impose serialization. Tax-stamp tenders under the EU Tobacco Products Directive illustrate how secure print volumes can grow even as traditional cash instruments stagnate.

In cash-centric regions, high-denomination banknotes keep intaglio press lines running near capacity, preserving the security printing market share of legacy equipment suppliers. Nigeria, India and the BEAC bloc collectively issued more than 250 billion notes in 2025, underlining the resilience of physical currency outside the OECD. However, retender cycles are getting longer and order sizes more variable because central banks anticipate eventual CBDC substitution. Suppliers are therefore diversifying into ID documents and track-and-trace labels, which require similar covert features but carry higher margins per square meter of substrate.

By Security Feature: RFID Tags Challenge Ink Hegemony

Security inks still anchor more than one-third of feature revenues, but electronic components are climbing the value stack. RFID and NFC tags, each costing USD 2-4 in a passport versus about USD 0.30 for a hologram, now dominate the bill of materials for e-passports. Chip shortages in 2024 exposed supply-chain fragility, pushing issuers to dual-source between NXP, Infineon and domestic fabs in India and China. Optically variable devices such as Surys kinegrams remain critical for first-line verification, yet covert taggants and machine-readable elements drive bulk profitability. Stegano varnish, introduced by Koenig and Bauer in 2025, embeds covert spectra that are invisible to the naked eye but detectable under defined wavelengths, enabling press-side application without an extra finishing step. This convergence of overt, covert and forensic features is standard practice as central banks layer 10-15 distinct elements on each denomination to frustrate counterfeiters.

Serialisation systems meeting GS1 and EU Tobacco Products Directive standards are the fastest-growing micro-segment. Each cigarette pack in the European Union now carries a unique identifier, generating demand for inline digital printheads capable of 600-dpi microtext at 120 meters per minute. Domino and Videojet have captured early share in this niche, while Memjet and Xaar pitch higher-resolution alternatives for premium tax stamps and pharmaceuticals. These trends are gradually eroding the dominance of analog security inks and tilting future growth toward hybrid electronic-print feature sets.

By Printing Technology: Digital Inkjet Carves a Niche

Intaglio presses remain indispensable for tactile depth and raised-ink perception, preserving a 41.44% revenue contribution in 2025. Hybrid lines that combine intaglio, offset and screen in a single pass maximize substrate handling efficiency and allow up to eight colors for complex guilloche patterns. Komori delivered its 200th intaglio press by mid-2025, underscoring stickiness in sovereign contracts. Nevertheless, serialization mandates for tax stamps and regulated packaging are accelerating digital inkjet adoption. Koenig and Bauer’s RotaJET platform, leveraging Memjet DuraLink heads, supports variable-data layouts at industrial throughput, enabling security printers to overlay unique identifiers without interrupting offset sequences. Gravure retains a niche for long-run fiscal stamps and lottery tickets where cylinder costs amortize over billions of impressions, but its share is slipping as regulatory cycles shorten.

Screen and flexographic presses thrive in low-security, high-volume applications such as parking permits and event badges. They are also being retrofitted with stochastic screening to apply UV-reactive patterns invisible under daylight. Intaglio’s dominance will persist until digital-inkjet chemistry improves durability and central banks validate its counterfeit resistance, yet hybrid workflows illustrate how new technology can coexist with legacy infrastructure inside the security printing market.

By Substrate: Polymer Gains but Cotton Holds Volume

Cotton-based paper, embedded with watermarks and partially embedded security threads, still accounts for 47.86% of revenue because of entrenched supply chains in the United States, Eurozone and Japan. However, polymer substrates are outpacing overall sector growth due to two key advantages: lifespan and environmental profile. Australia, Canada and the United Kingdom report 2.5-4× note life extensions after full polymer conversion, shaving replacement and transport costs despite the higher ex-works price. Africa and Southeast Asia view polymer as a leapfrog option to cut wear-related losses in hot, humid climates. CCL Secure’s Guardian substrate dominates the landscape, followed by Innovia’s Clarity C. Hybrid paper-polymer laminates are emerging as a transitional format for issuers unwilling to overhaul press lines, blending cotton’s familiarity with polymer’s strength.

Sustainability criteria are influencing substrate selection. The European Central Bank committed to sourcing 100% sustainable cotton from certified farms by 2025, but lifecycle analyses show polymer’s carbon footprint per year-in-circulation can be lower once transport and destruction emissions are counted. These findings will likely sway additional central banks toward polymer as recycling infrastructure matures. Until major economies make the switch, though, cotton paper will continue to underpin bulk tonnage in the security printing market.

Geography Analysis

Asia-Pacific remains the revenue anchor for the security printing market, reflecting China’s output above 90 billion banknotes per year and India’s 140 billion notes in circulation. Growth is helped by Indonesia’s plan to raise banknote volumes 3% annually through 2030 and by Japan’s new series introduced in 2024, which were 30% distributed by mid-2025. Suppliers benefit from a dense ecosystem of substrate mills, intaglio press assembly plants and semiconductor fabs, allowing regional sourcing of RFID chips and optically variable pigments.

Africa is predicted to outpace every other region at a 3.46% CAGR to 2031. Kenya’s five-year contract with Giesecke+Devrient and Ethiopia’s e-passport joint venture with Toppan show a push for sovereign autonomy in currency and ID document manufacture. Nigeria’s redesign, Somalia’s new 1,000-shilling notes and the BEAC bloc’s “type 2020” series bolster regional press utilization rates. Upfront capex remains a hurdle, but multilateral lenders and export-credit agencies are underwriting several turnkey plants, accelerating technology transfer into the continent.

Europe illustrates the digital transition. Despite a robust base of 12 national euro printers, cash usage in Sweden and Norway is near single digits, and the ECB’s digital euro pilot may curb circulation after 2028. Nevertheless, the region will sustain demand for biometric passports, tax stamps compliant with the Tobacco Products Directive and serialized pharmaceutical labels, allowing the security printing market to pivot from cash to secure civil documents. North America mirrors this dual track: the United States Bureau of Engraving and Printing still turns out 7.6 billion notes annually, but brand-protection labels and high-security driving licenses are rising fastest.

South America faces currency volatility that complicates forecast volumes. Brazil’s Casa da Moeda has halted some export contracts to prioritize domestic hyperinflation mitigation, while Argentina’s peso collapse widened tender gaps for polymer note trials. The Middle East is upgrading its own plants; the UAE’s recyclable polymer Dh500 note and Saudi Arabia’s capacity expansion aim to cut dependence on European suppliers. Each geography thus exhibits a unique mix of growth drivers and structural drag, reinforcing the need for diversified product portfolios within the security printing market.

Competitive Landscape

The top five vendors—Giesecke+Devrient, De La Rue, SICPA, Koenig and Bauer and CCL Secure—collectively controlled roughly 40-45% of revenue in 2025, a profile that places the security printing market in the moderately consolidated category. Giesecke+Devrient’s KES 14.5 billion Kenyan contract and Komori’s sole-supplier status at the Bank of England show how incumbent relationships defend share. De La Rue’s takeover by Atlas Holdings and its sale of the Authentication arm to Crane Currency betray mounting margin pressure that encourages consolidation among Western incumbents.

Technology is the primary differentiator. SICPA’s rare-earth pigmented optically variable inks power most Type-III currency series, with replacement risk low because color-shift recipes are trade secrets. CCL Secure enjoys a near-monopoly on polymer substrate, strengthened by 20-year supply contracts with Australia, the United Kingdom and Canada. Koenig and Bauer’s ISO 14298 certification and its “protected at print” varnish extension underline how equipment suppliers use security feature integration to lock in press upgrades.

State-owned printers in China, India, South Korea and Russia contribute significant output, but their business is largely captive, limiting competitive threat abroad. New entrants focus on digital inkjet serialization niches, where capital requirements are lower and switching costs minimal. Memjet and Xaar have placed printheads on hybrid lines that overlay serialized identifiers on tax stamps and pharmaceutical cartons, but their share remains in single digits. Overall, the competitive theatre is defined by long sovereign contracts, high press capex and proprietary chemistry—factors that collectively sustain mid-level concentration in the security printing market.

Security Printing Industry Leaders

Giesecke+Devrient GmbH

De La Rue plc

SICPA Holding SA

Koenig and Bauer AG

CCL Secure Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Koenig and Bauer completed the first commercial run of its Stegano varnish on a European tax-stamp line, claiming a spoilage reduction of 10%.

- September 2025: Koenig and Bauer introduced the “protected at print” workflow, embedding covert Stegano varnish directly on offset presses, trimming post-press steps.

- May 2025: Crane Currency bought De La Rue’s Authentication division for USD 300 million, adding holographic foil and track-and-trace capability.

- April 2025: Atlas Holdings finalized its USD 330 million acquisition of De La Rue, intending to streamline unprofitable contracts.

Global Security Printing Market Report Scope

Security printing encompasses the production of tamper-proof and counterfeit-resistant printed materials, including currency, identification cards, passports, certificates, and official documents. The industry incorporates advanced security features such as holograms, UV inks, microprinting, RFID tags, and watermarks to prevent forgery, duplication, and alteration. The market provides solutions for governments, banks, healthcare institutions, and packaging companies in response to increasing global requirements for secure and authenticated documentation.

The Security Printing Market Report is Segmented by Application (Banknotes, Payment Cards, Cheques, Personal Identification Documents, Ticketing and Transit Passes, Postage and Fiscal Stamps, Brand-Protection and Tax Banderoles), Security Feature (Security Inks, Holograms and DOVIDs, Watermarks and Security Threads, RFID and NFC Tags, Track-and-Trace Serialisation), Printing Technology (Intaglio, Offset/Lithography, Screen and Flexo, Digital Inkjet, Gravure), Substrate (Cotton-Based Paper, Polymer, Hybrid Paper-Polymer, Synthetic and Composite Films), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Banknotes |

| Payment Cards |

| Cheques |

| Personal Identification Documents |

| Ticketing and Transit Passes |

| Postage and Fiscal Stamps |

| Brand-Protection and Tax Banderoles |

| Security Inks (UV, OVI, Optically Variable) |

| Holograms and DOVIDs |

| Watermarks and Security Threads |

| RFID and NFC Tags |

| Track-and-Trace Serialisation |

| Intaglio |

| Offset/Lithography |

| Screen and Flexo |

| Digital Inkjet |

| Gravure |

| Cotton-Based Paper |

| Polymer |

| Hybrid Paper-Polymer |

| Synthetic and Composite Films |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia and New Zealand | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Application | Banknotes | |

| Payment Cards | ||

| Cheques | ||

| Personal Identification Documents | ||

| Ticketing and Transit Passes | ||

| Postage and Fiscal Stamps | ||

| Brand-Protection and Tax Banderoles | ||

| By Security Feature | Security Inks (UV, OVI, Optically Variable) | |

| Holograms and DOVIDs | ||

| Watermarks and Security Threads | ||

| RFID and NFC Tags | ||

| Track-and-Trace Serialisation | ||

| By Printing Technology | Intaglio | |

| Offset/Lithography | ||

| Screen and Flexo | ||

| Digital Inkjet | ||

| Gravure | ||

| By Substrate | Cotton-Based Paper | |

| Polymer | ||

| Hybrid Paper-Polymer | ||

| Synthetic and Composite Films | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia and New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the security printing market in 2026 and at what CAGR is it growing?

It is estimated at USD 33.66 billion in 2026 and is forecast to reach USD 38.16 billion by 2031, registering a 2.54% CAGR over 2026-2031.

Which segment is expanding fastest inside the security printing market?

Personal identification documents are advancing at a 3.88% CAGR through 2031 as governments mandate biometric passports and digital IDs.

Why are polymer banknotes gaining popularity?

Polymer lasts 2.5-4 times longer than cotton paper, lowers replacement costs and enables advanced transparent security windows, offsetting its 30-40% higher material price.

How are RFID tags affecting security-feature spending?

RFID and NFC components, required in e-passports and many national ID cards, are growing at a 3.49% CAGR and raising the average feature cost per document.

What is the biggest restraint on long-term growth?

The shift toward cashless payments and the development of CBDCs could cut physical banknote demand in developed markets, subtracting an estimated 0.6 percentage points from forecast CAGR.

Who leads the polymer substrate niche?

CCL Secure’s Guardian film supplies 76 central banks and effectively dominates global polymer banknote production contracts.

Page last updated on: