Screen Printing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

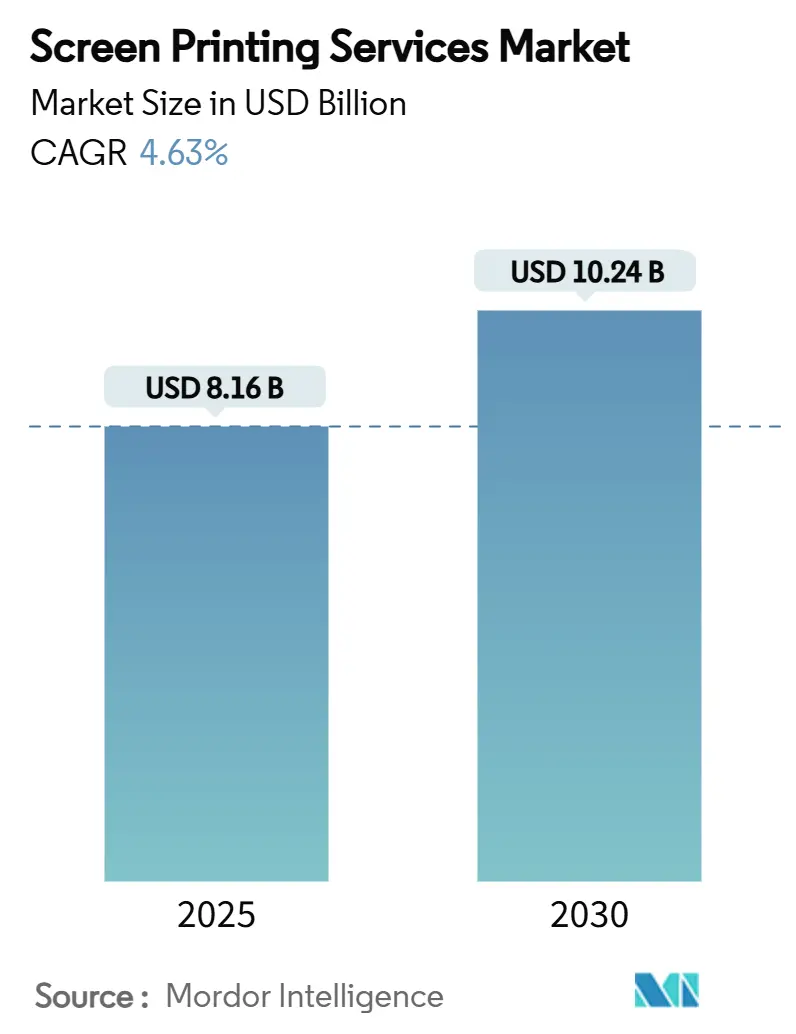

| Market Size (2025) | USD 8.16 Billion |

| Market Size (2030) | USD 10.24 Billion |

| Growth Rate (2025 - 2030) | 4.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

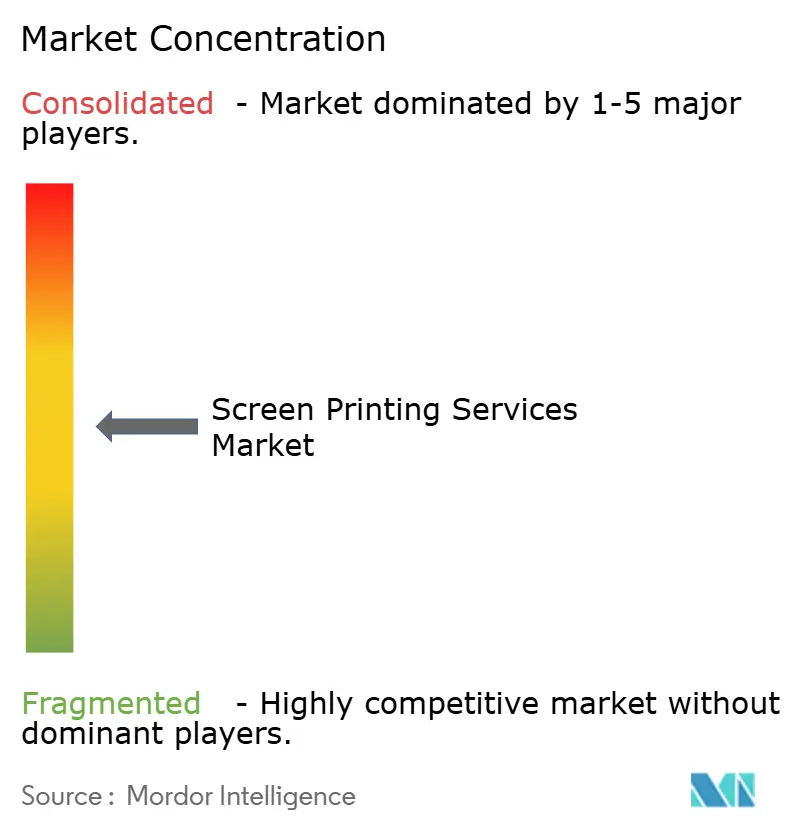

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Screen Printing Services Market Analysis by Mordor Intelligence

The screen printing services market size is estimated at USD 8.16 billion in 2025 and is forecast to reach USD 10.24 billion by 2030, reflecting a 4.63% CAGR over the period. Demand remains anchored in apparel decoration, packaging and signage, yet new revenue streams in printed electronics and automotive human-machine interfaces widen the opportunity set for service providers. Thick-film capability, superior durability and the option to deposit functional inks keep screen printing competitive when digital processes fall short on opacity, stretch or conductivity.[1]Fraunhofer ISE, “High-speed Rotary Screen Printing Technology,” fraunhofer.de Asia-Pacific drives global volume, while sustainability rules in Europe and North America accelerate migration toward water-based formulations. Automation raises throughput and consistency, prompting mid-sized firms to invest in rotary and carousel presses, and recent mergers such as the Printful-Printify tie-up underscore the sector’s move toward scale economics.

Key Report Takeaways

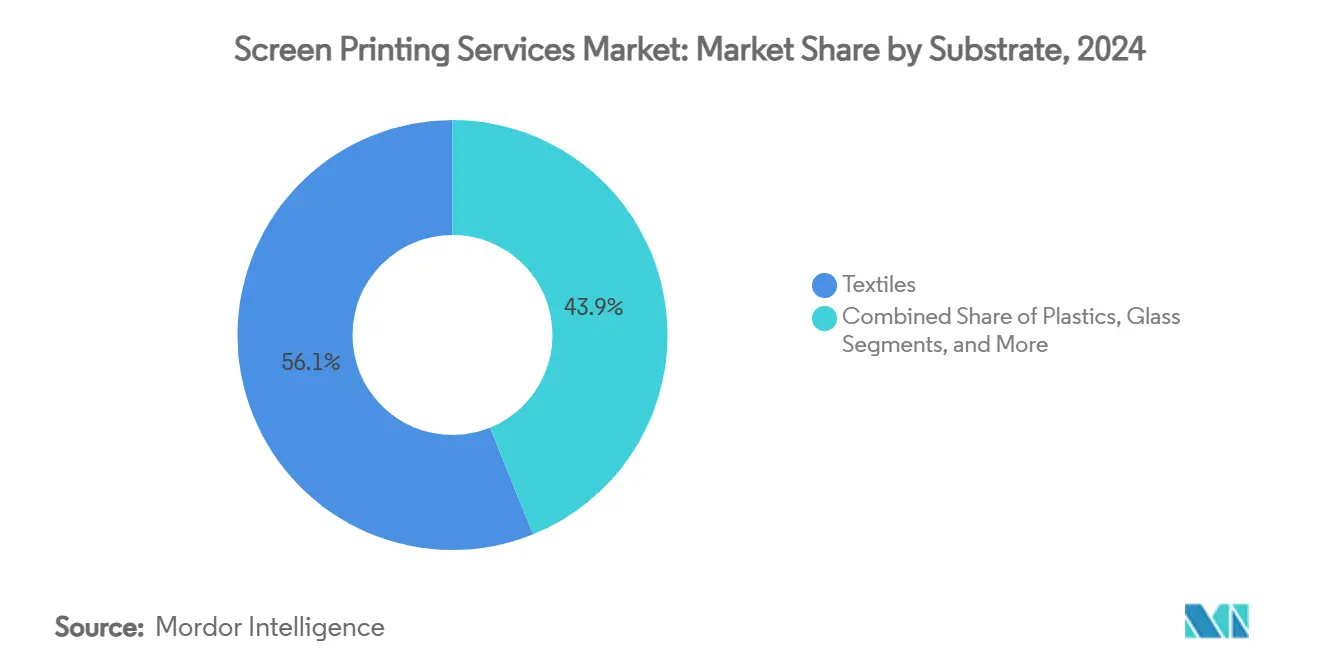

- By substrate, Textiles led with 56.12% of the screen printing services market share in 2024; conductive films are poised to grow at an 8.21% CAGR to 2030.

- By service type, Automatic flatbed systems commanded 42.12% of the screen printing services market size in 2024, while rotary solutions are forecast to expand at a 9.25% CAGR through 2030.

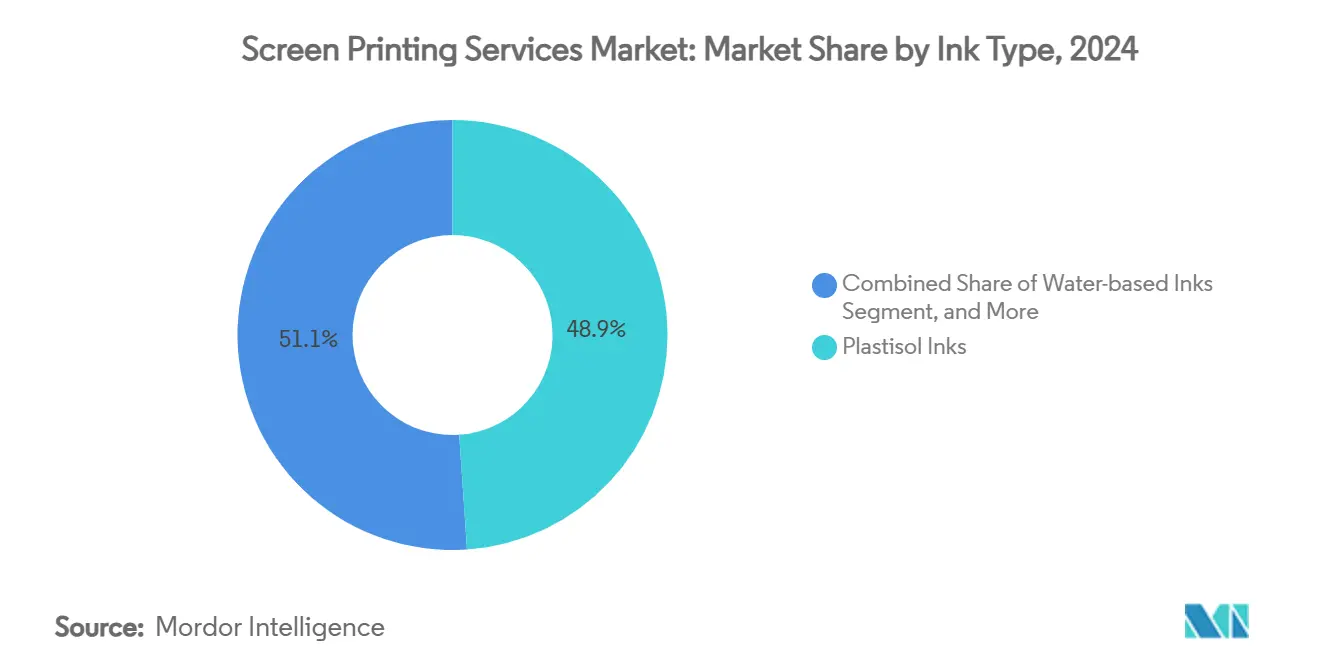

- By ink type, Plastisol retained 51.07% share in 2024; water-based inks represent the fastest category, advancing at a 7.05% CAGR through 2030.

- By end-user industry, Apparel and fashion accounted for 35.24% of the screen printing services market size in 2024, whereas electronics and printed electronics are growing at a 9.25% CAGR to 2030.

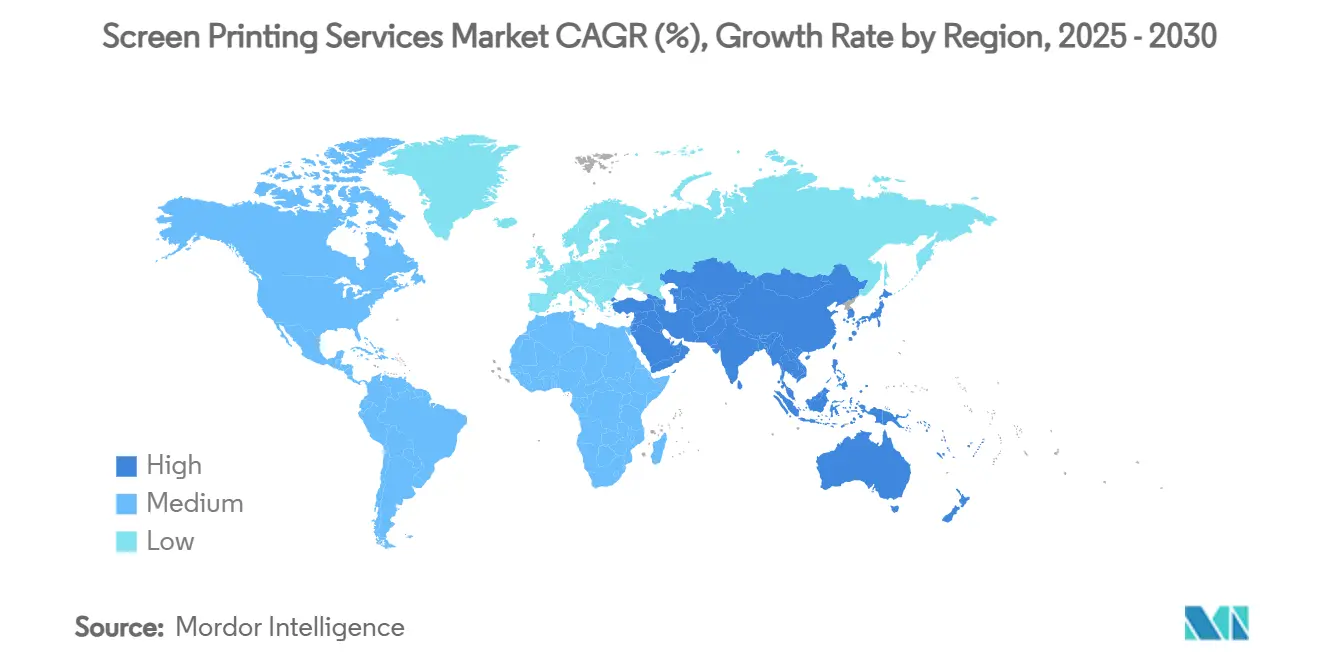

- By geography, Asia-Pacific held 36.37% revenue share in 2024 and is expected to post a region-leading 10.85% CAGR over the forecast period.

Global Screen Printing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of custom apparel & promotional-merchandise demand | +1.5% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of packaging & label printing for e-commerce logistics | +1.2% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Adoption of water-based & eco-friendly inks under tightening regulations | +1.0% | Europe & North America primary, expanding to APAC | Medium term (2-4 years) |

| Emergence of screen-printed conductive traces for printed electronics & IoT | +0.8% | Global, with early adoption in Asia-Pacific & North America | Long term (≥ 4 years) |

| Automotive interiors' shift toward screen-printed HMI films & sensors | +0.7% | Europe & North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| On-demand mass-customisation enabled by web-to-print platforms | +0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Custom Apparel & Promotional-Merchandise Demand

Corporate branding, influencer marketing and web-to-print storefronts fuel small-batch orders that favor the durability, opacity and tactile finishes obtainable only through screen printing. Fashion labels use the process for premium placements that align with direct-to-consumer drop strategies, while promotional-item buyers opt for higher-value garments that reinforce sustainability pledges. Workflow automation lets mid-volume printers achieve variable designs without sacrificing margin, positioning the screen printing services market as a resilient supplier to brand owners seeking long-lasting impressions.[2]Indian Retailer, “How Personalization Is Reshaping Fashion,” indianretailer.com

Expansion of Packaging & Label Printing for E-commerce Logistics

Online retail lifts demand for corrugated boxes, mailers and security labels that must survive automated fulfillment, transport and returns. Screen-printed tactile warnings, RFID antennas and high-opacity brand colors differentiate premium shipments, and the European RFID label market’s move toward EUR 2.5 billion (USD 2.71 billion) by 2027 underlines scale potential. China’s rebound in corrugated paper usage further magnifies volume requirements for specialty inks on paper substrates.[3]SunSirs, “China Corrugated Paper Price Trend,” sunsirs.com

Adoption of Water-based & Eco-friendly Inks Under Tightening Regulations

REACH in Europe and evolving TSCA rules in the United States compel printers to lower volatile organic compound output. Mature suppliers leverage compliance expertise to release low-VOC blends, evidenced by Avient’s bio-based plastisol portfolio, which balances sustainability and opacity. Early adopters absorb short-term curing-equipment upgrades yet benefit from preferred supplier status with global brands committed to environmental benchmarks.

Emergence of Screen-Printed Conductive Traces for Printed Electronics & IoT

Stretchable silver-based pastes achieving 6.02 × 10^6 S m-1 conductivity expand screen printing into flexible circuits, wearable sensors and automotive touch modules. Roll-to-roll lines delivering 30 m²/h throughput make the process cost-competitive against etched copper when application volumes scale, broadening the screen printing services market addressable share in the electronics supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cannibalisation from digital/DTG and DTF printing technologies | -1.1% | Global, most pronounced in North America & Europe | Short term (≤ 2 years) |

| Volatile prices of specialty meshes, emulsions & plastisol raw materials | -0.9% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Skilled labour shortage for multilayer/high-precision screen printing | -0.7% | Developed markets, particularly North America & Europe | Medium term (2-4 years) |

| Capital intensity of automated carousel & rotary presses for SMEs | -0.5% | Global, disproportionately affecting emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cannibalisation from Digital/DTG and DTF Printing Technologies

Direct-to-garment engines now exceed 400 garments per hour and skip screen prep, eroding cost advantages for runs below 100 units. Hybrid presses such as the DS-4000 allow incumbents to blend digital imagery with opaque screen whites, yet market share loss persists where variable data and rapid turnarounds outweigh longevity requirements.

Volatile Prices of Specialty Meshes, Emulsions & Plastisol Raw Materials

PVC, plasticizer and polyester yarn swings tighten gross margins, especially for small workshops that lack hedging mechanisms. Concentrated mesh output in East Asia magnifies exposure to port congestion and energy price spikes, prompting printers to test alternative suppliers, renegotiate terms and shorten quote validity periods, actions that add administrative overhead and strain customer relations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Textiles Dominate While Conductive Films Accelerate

Textiles retained 56.12% of screen printing services market share in 2024, reinforcing the process’s centrality to fashion, workwear and home textiles. The segment benefits from China’s USD 301.1 billion export engine and India’s trajectory toward USD 350 billion by 2030, ensuring a steady order pipeline. These volumes anchor the screen printing services market size, though margin pressure persists as large buyers push for greener inks and water stewardship credentials.

Conductive films carved the fastest-growing niche with an 8.21% CAGR outlook. Automotive dashboards and flexible wearables require transparent, stretchable substrates able to host silver or graphene inks without delamination. Printers expanding into this space invest in clean-room handling and multi-layer registration, diversifying revenue beyond cyclical apparel cycles. Mixed-material competence positions these operators for long-run contracts in IoT and medical monitoring.

By Service Type: Automation Lifts Output and Consistency

Automatic flatbed lines delivered 42.12% of the screen printing services market size in 2024, illustrating the shift to higher uptime, precision flood bars and reduced setup waste. Mid-tier providers deploy camera-guided repeats to cut spoilage, freeing human staff for quality inspection tasks.

Rotary printing, forecast to advance at 9.25% CAGR, outperforms on cylindrical packaging, tubing and high-speed label work. Fraunhofer’s 0.6-second stroke innovation multiplied unit throughput by 1.5x and lowered ink pick-up variance, making the technique attractive for converters chasing e-commerce demand spikes. Manual and cylinder presses survive in artisanal shops and specialty graphics where tactile finishes justify slower cycles.

By Ink Type: Plastisol Holds Ground as Water-based Variants Gain

Plastisol’s 51.07% command of the screen printing services market share in 2024 reflects its forgiving viscosity, broad color gamut and resistance to dye migration. Large apparel contractors trust the chemistry to achieve uniform hand feel across poly-cotton blends. Still, sustainability audits by global retailers accelerate water-based adoption, now growing 7.05% annually. Early movers upgrade dryers to reach moisture-removal temperatures while preserving low shrinkage targets.

UV-curable and solvent systems serve niche industrial uses requiring impact resistance or outdoor stability, whereas conductive formulations open fresh avenues in sensors and antenna arrays. Silver ink pricing tracks bullion markets, prompting R&D on carbon-silver hybrids and doped copper as cost mitigation measures.

By End-user Industry: Electronics Re-shapes Demand Mix

Apparel remained the anchor at 35.24% of screen printing services market size in 2024, but runaway 9.25% CAGR growth in electronics is re-allocating capex plans across the sector. Automotive tier-1 suppliers specify screen-printed ITO or PEDOT electrodes for touch-enabled center stacks, while wearable brands commission flexible ECG and temperature patches.

Packaging and labels prosper from direct-to-consumer shipping volumes, yet digital signage and OLED price declines temper traditional poster turnover. Industrial components for renewable energy, medical devices and aerospace heat shields demand multilayer builds, pushing printers toward class-100 clean-room upgrades and statistical process control certifications.

Geography Analysis

Asia-Pacific anchored 36.37% of 2024 revenue and headlines the growth curve with a forecast 10.85% CAGR, propelled by integrated supply chains, competitive labor and rising domestic consumption. China’s textile export engine and India’s broad technical-textile program attract continued foreign investment, deepening regional dominance. Vietnam, Bangladesh and Indonesia supply volume apparel orders, while Japan and South Korea emphasize printed electronics know-how, elevating value density per square meter.

North America commands premium niches such as performance sportswear, automotive HMI films and printed sensors. Proximity to brand owners enables design iterations under 48 hours, mitigating freight delays. Environmental oversight rewards early adoption of water-based systems, granting compliant firms access to corporate sustainability programs. Government incentives for reshoring electronics accelerate domestic conductive-ink capacity, reinforcing the screen printing services market in high-value verticals.

Europe balances legacy textile clusters in Portugal, Spain and Turkey with innovation labs in Germany’s NRW and Bavaria. REACH and the Packaging Waste Directive drive process audits, spurring capital upgrades to closed-loop washout booths and energy-efficient dryers. Eastern European facilities bridge cost gaps, supplying automotive and appliance brands based in Germany and Italy. South America and the Middle East & Africa remain emerging contributors, yet rising disposable incomes and industrial diversification attract gradual capacity additions in Brazil, Mexico, the UAE and Saudi Arabia.

Competitive Landscape

The screen printing services market hosts hundreds of regional operators, yet consolidation signals mounting scale efficiencies. Avient’s takeover of Magna Colours integrates eco-friendly pigments into an established distribution network, enabling cross-selling and faster regulatory clearance. The Printful-Printify merger aggregates on-demand volumes, improving negotiation leverage with blank-garment suppliers and logistics partners.

Equipment vendors M&R, MHM and Vastex differentiate on automation modules, IoT-enabled press diagnostics and operator ergonomics, winning loyalty through financing packages and remote maintenance portals. Ink formulators Nazdar, Fujifilm Sericol and Avient pursue low-VOC and bio-based skus, anticipating stricter chemical audits by fashion conglomerates.

Competitive intensity varies by application. Commodity tees push margin compression below 15%, while printed electronics jobs command gross margins above 40% due to specialized registration and clean-room requirements. Firms investing in R&D collaborations with universities and material-science centers position for defensible niches and longer-term contracts, mitigating commoditization risk.

Screen Printing Services Industry Leaders

Toppan Inc.

Dai Nippon Printing Co., Ltd.

CCL Industries Inc.

Quad/Graphics, Inc.

RR Donnelley & Sons Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Specialty Printing secured USD 11.5 million from Advantage Capital to hire 50 staff and add pressure-sensitive label lines, reinforcing a diversified label offering to grocery and healthcare customers.

- January 2025: Reflex Labels installed its third Screen brand press, signaling confidence in demand for high-resolution label work and boosting redundancy for just-in-time orders.

- December 2024: Kornit Digital expanded its executive bench to accelerate hybrid digital-screen technology rollouts, aiming to capture sustainability-oriented mid-volume garment printers.

- April 2024: Lawson Screen & Digital Products celebrated 75 years in business, showcasing updated manual presses that target entry-level entrepreneurs in the decorated-apparel sector.

Global Screen Printing Services Market Report Scope

| Textiles |

| Plastics |

| Glass |

| Paper and Paperboard |

| Conductive Films |

| Other Substrates |

| Manual Screen Printing |

| Automatic Flatbed Screen Printing |

| Rotary Screen Printing |

| Cylinder Screen Printing |

| High-precision Multi-layer Screen Printing |

| Plastisol Inks |

| Water-based Inks |

| UV-curable Inks |

| Solvent-based Inks |

| Conductive Inks |

| Apparel and Fashion |

| Packaging and Labels |

| Advertising and Signage |

| Electronics and Printed Electronics |

| Automotive and Transportation |

| Industrial Components |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Qatar | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

| By Substrate | Textiles | ||

| Plastics | |||

| Glass | |||

| Paper and Paperboard | |||

| Conductive Films | |||

| Other Substrates | |||

| By Service Type | Manual Screen Printing | ||

| Automatic Flatbed Screen Printing | |||

| Rotary Screen Printing | |||

| Cylinder Screen Printing | |||

| High-precision Multi-layer Screen Printing | |||

| By Ink Type | Plastisol Inks | ||

| Water-based Inks | |||

| UV-curable Inks | |||

| Solvent-based Inks | |||

| Conductive Inks | |||

| By End-user Industry | Apparel and Fashion | ||

| Packaging and Labels | |||

| Advertising and Signage | |||

| Electronics and Printed Electronics | |||

| Automotive and Transportation | |||

| Industrial Components | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Israel | |||

| Qatar | |||

| Kuwait | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Kenya | |||

| Morocco | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the screen printing services market?

The screen printing services market size stands at USD 8.16 billion in 2025 and is on track to reach USD 10.24 billion by 2030

Which substrate accounts for the largest share of screen printing demand?

Textiles dominate with 56% of screen printing services market share, driven by apparel and workwear orders.

Which region is growing the fastest?

Asia-Pacific leads growth with a projected 10.85% CAGR thanks to integrated supply chains and rising domestic consumption.

Why are water-based inks gaining popularity?

Tightening environmental regulations in Europe and North America and corporate sustainability targets encourage adoption of low-VOC water-based alternatives, which are growing at a 7.05% CAGR.

How is screen printing positioned in the electronics sector?

Screen-printed conductive traces enable flexible circuits for wearables, IoT sensors and automotive HMIs, spurring a 9.25% CAGR in the electronics end-use segment.

What strategic moves are shaping industry consolidation?

M&A activity such as Avient’s ink-technology acquisitions and the Printful-Printify merger aim to achieve scale, broaden product lines and secure supply-chain efficiencies across high-growth niches.

Page last updated on: