Flexographic Printing Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

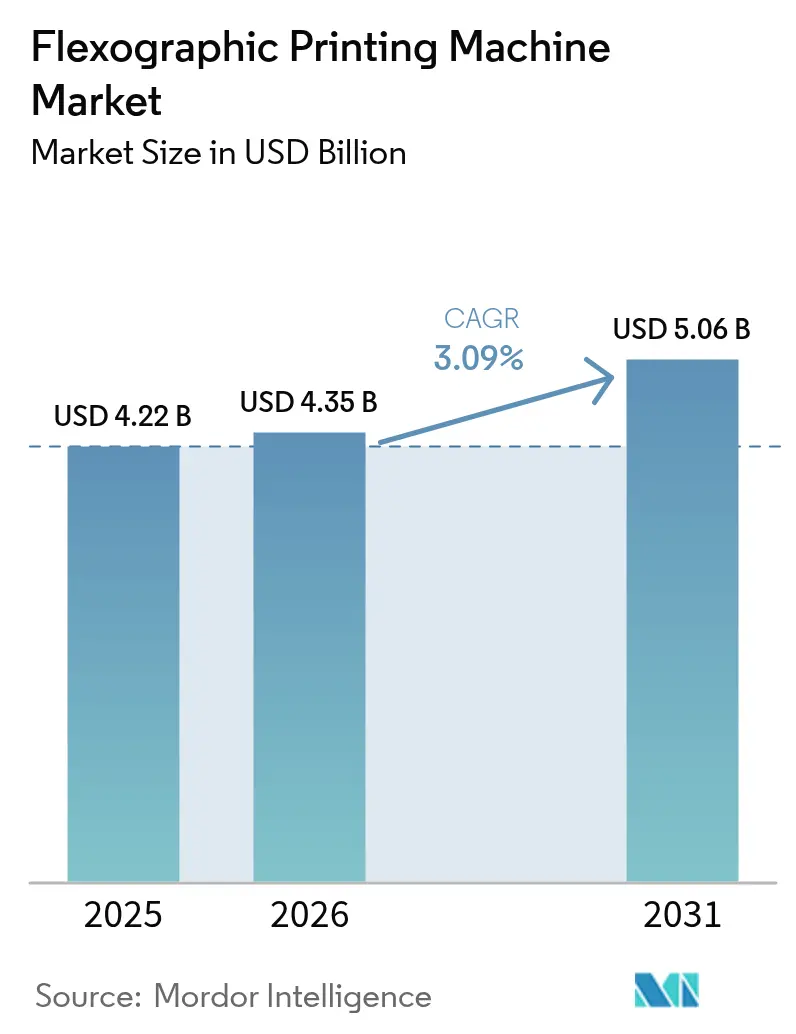

| Market Size (2026) | USD 4.35 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexographic Printing Machine Market Analysis by Mordor Intelligence

Flexographic printing machine market size in 2026 is estimated at USD 4.35 billion, growing from 2025 value of USD 4.22 billion with 2031 projections showing USD 5.06 billion, growing at 3.09% CAGR over 2026-2031. Investment priorities now revolve around automation, hybrid press capabilities, and compliance with tightening sustainability rules rather than simple capacity expansion. E-commerce-related short runs, water-based ink mandates, and digital-twin maintenance platforms are reshaping procurement criteria across converters. Suppliers that marry fast changeovers with low-VOC performance are gaining share, while regional subsidy programs, most notably China’s 2026 “Green Press” policy, are altering the competitive map. At the same time, mergers such as XSYS-MacDermid and INX-C&A illustrate how plate-making and ink specialists are consolidating to cut lead times and navigate PFAS restrictions.

Key Report Takeaways

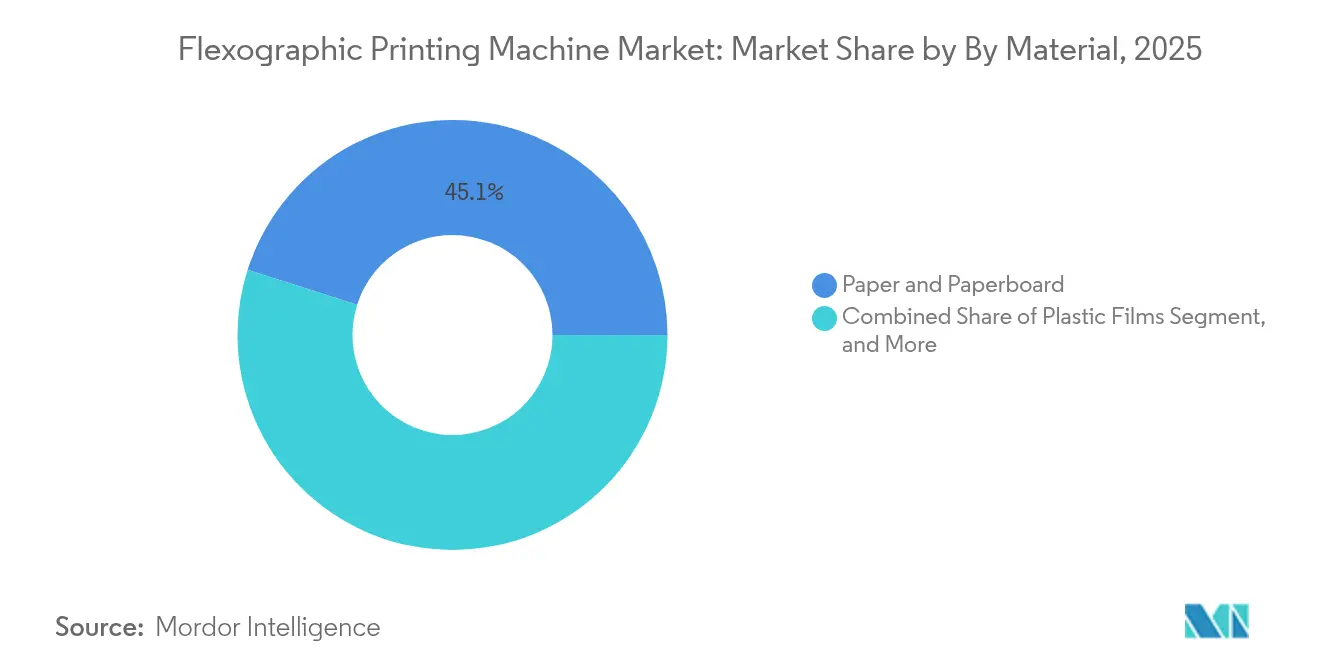

- By material, paper and paperboard led with 45.10% of the flexographic printing machine market share in 2025.

- By press type, in-line/modular systems held 39.00%of the flexographic printing machine market size in 2025.

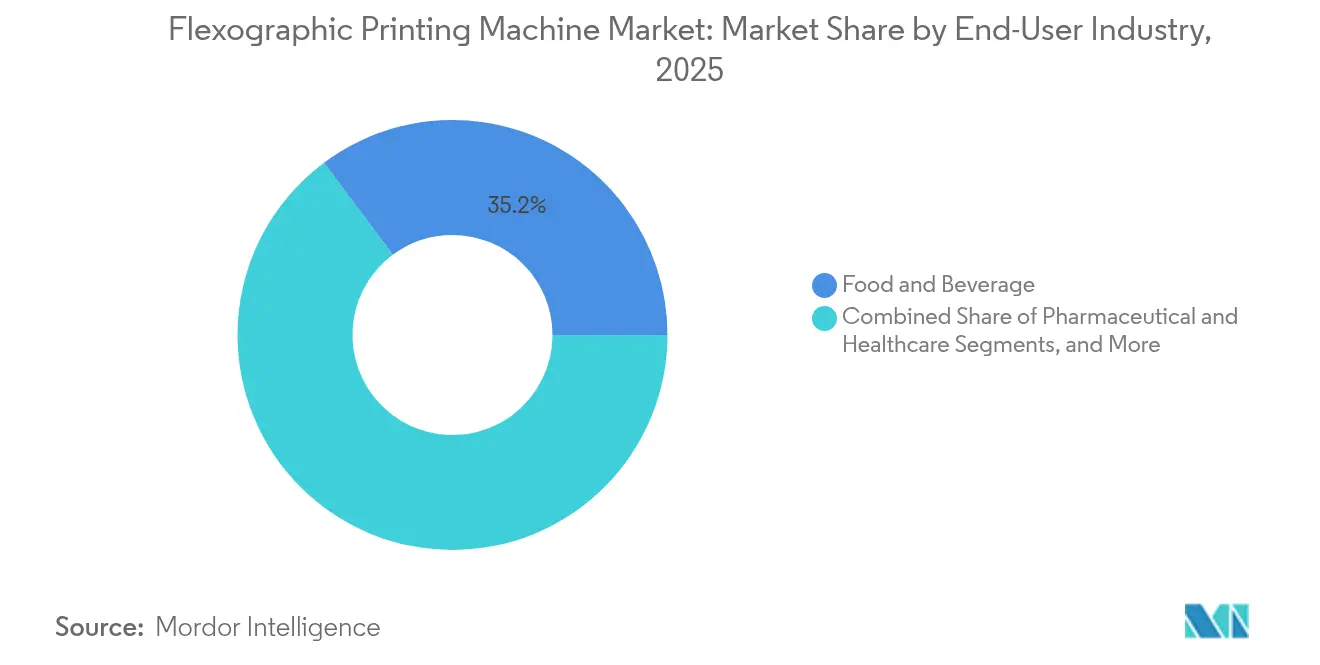

- By end-user industry, food and beverage accounted for 35.20% of the flexographic printing machine market share in 2025.

- By automation level, smart/IoT-enabled systems advance at a 7.08% CAGR between 2026-2031 for flexographic printing machine market size.

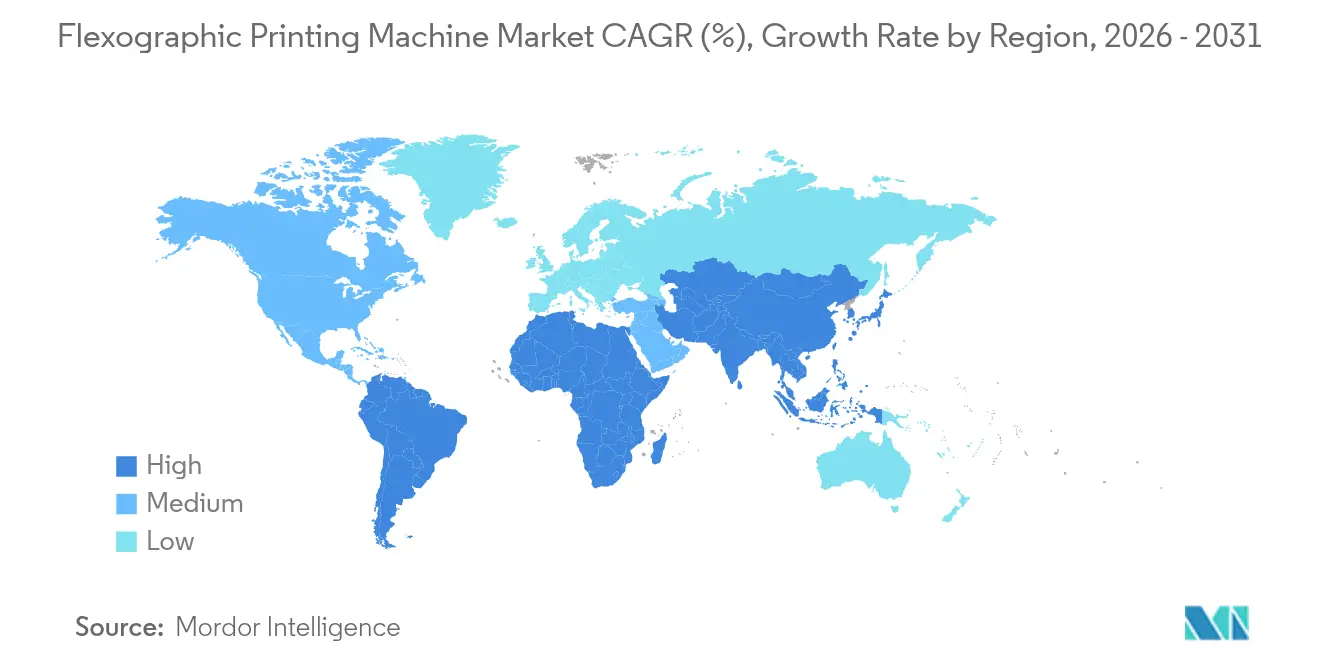

- By geography, Asia-Pacific captured 40.10% of the flexographic printing machine market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexographic Printing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective short-run packaging capability | +0.8% | North America & Europe | Medium term (2-4 years) |

| Food-grade sustainable flexible packaging surge | +0.7% | EU & North America | Long term (≥4 years) |

| Rapid corrugated capacity additions | +0.6% | Asia-Pacific core | Short term (≤2 years) |

| Water-based low-VOC ink mandates | +0.5% | North America & EU | Medium term (2-4 years) |

| Converting-line digital twin and AI predictive-maintenance adoption | +0.4% | Global, with early adoption in Germany, Japan, South Korea | Long term (≥ 4 years) |

| China's 2026 "Green Press" subsidy for CI-flexo equipment | +0.3% | China domestic market, competitive pressure globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost-effective short-run packaging capability

Flexographic press builders have slashed setup times, taking profitable minimum runs from 5,000 m to close to 500 m. Shorter cycles mean brands with seasonal or regional SKUs can deploy custom graphics without prohibitive costs. MacDermid’s LUX ITP plates now leave the plate room in eight hours, down from two days, which removes a key bottleneck for converters targeting next-day art changes. Together, faster plates and rapid changeovers allow flexography to reclaim work that once defaulted to digital presses. Converters are therefore investing in mid-range modular lines that balance speed with flexibility, underpinning equipment demand across the flexographic printing machine market.

Surge in food-grade sustainable flexible packaging

European and North American regulations are eliminating PFAS while demanding full recyclability. Saica Flex plans a 100% recyclable portfolio by 2030 with 5% PCR content, showcasing the pressure on converters to prove circularity[1]Source: Packaging Europe, “How Saica Flex Targets a Circular Future for Flexible Packaging,” packagingeurope.com. INX’s GelFlex EB inks remove lamination layers, cutting total pack weight yet maintaining barrier integrity inxinternational.com. Inline barrier-coating partnerships, such as Solenis-Heidelberg, further reduce secondary processes. As converters race to certify new chemistries before the EU’s August 2026 PFAS cap, demand crescendos for presses that can run water-based or EB curing inks at competitive speeds benefiting the flexographic printing machine market.

Rapid corrugated capacity additions in e-commerce fulfillment

Asia-Pacific corrugators are adding lines to meet package personalization tied to online retail. Over half of corrugated box graphics already use flexo, owing to its speed advantage on brown kraft liners. China’s express-packaging rule GB 43352-2023 imposes heavy-metal limits on inks, pushing converters toward compliant, water-based chemistries. In the United States, Atlantic Packaging’s plant expansion underscores a similar trend toward multi-SKU, high-mix corrugated fulfillment.

Mandates on water-based low-VOC inks

The US EPA now applies Significant New Use Rules to virtually every fresh ink chemistry, forcing formulators to document environmental impacts . Washington State is debating the most stringent ink ban yet, which would trigger wholesale reformulation. High-velocity water-based lines, such as OSP Group’s 100 m/min machine, prove that solvent-free performance is achievable at scale. The rulemaking reinforces water-based investment across the flexographic printing machine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cap-ex intensive multi-color CI presses | -0.6% | Global | Medium term (2-4 years) |

| Skilled press-operator shortage | -0.4% | Europe & Japan | Long term (≥4 years) |

| Plate-making lead-time bottlenecks for ultra-short runs | -0.3% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

| Tightening PFAS restrictions on barrier coating compatibility | -0.2% | North America & EU, extending to APAC regulatory zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cap-ex intensive multi-color CI presses

A fully optioned 1,300 mm CI line can command USD 4 million, well above modular alternatives. As a result, even global accounts deferred orders in 2024, cutting Bobst CI bookings by 24%. Mid-market converters hesitate to finance premium presses when average run lengths are shrinking, slowing replacement cycles in the flexographic printing machine market.

Skilled press-operator shortage in Europe and Japan

Complex registration and color management still require experienced crews, yet retirements are outpacing new entrants. The European Labour Authority lists skilled trade scarcity among the region’s top constraints. Japanese converters respond by deploying automated handling robots from Fujifilm Business Innovation to cut manual intervention . Nonetheless, labor gaps continue to cap throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Dominance Faces Plastic Innovation

Paper and paperboard led the flexographic printing machine market with 45.10% share in 2025, buoyed by retail e-commerce cartons and recycled kraft liners. Converters rely on paper’s easy recyclability to satisfy brand mandates, while improved coatings are extending shelf life for ambient foods. Plastic films, however, chart the fastest 6.33% CAGR as mono-material laminates and PCR blends solve circularity and barrier needs.

The substitution battle intensifies as INX’s EB inks allow film structures to drop a lamination layer, cutting gauge without compromising barrier. UFlex’s new PET resin capacity in Egypt reflects global resin self-sufficiency moves to shorten supply chains. Overall, paper converters expand corrugator fleets, whereas film suppliers chase high-barrier pouches together sustaining equipment demand across the flexographic printing machine market size for substrate-specific presses.

By Press Type: Modular Flexibility Versus CI Quality

In-line/modular systems held 39.00% revenue share in 2025 thanks to affordable acquisition costs and nimble job changes traits favored by private-label food and indie cosmetics. Central-impression presses, though capital-heavy, are gaining fastest at 5.28% CAGR, propelled by brand demands for tight color-to-color register on shrink sleeves and wide web snacks.

Hybrid designs blur former lines: Uteco’s OnyxOMNIA stitches inkjet heads onto an eight-color flexo deck, delivering 400 m/min while enabling variable data . As CI OEMs roll out automatic plate cylinders and digital-twin diagnostics, converters with 24/6 shifts migrate upscale, driving the flexographic printing machine market toward higher-spec platforms.

By End-User Industry: Food Leadership Meets E-Commerce Growth

Food and beverage sustained a 35.20% stake in 2025 because safety rules and retail presentation standards align naturally with flexography’s low-migration inks and quick color changes. Drake’s Brewing cut Scope 3 emissions by 4% after switching to recyclable cans, illustrating brand sustainability push-pull effects.

Logistics and e-commerce packaging, posting a 7.42% CAGR through 2031, is the standout growth engine. Corrugated plants embrace quick-setup modular presses to print batch-level QR codes, customizing every shipping box. The segment’s volume swing factor makes it an equipment demand bellwether, increasingly shaping capital budgets in the flexographic printing machine market.

By Automation Level: Smart Systems Drive Transformation

Conventional presses still form 57.90% of global installs, a legacy effect of earlier rollouts. Yet smart/IoT-enabled lines accelerate at 7.08% CAGR as AI diagnostics curb waste and downtime. SOMA’s bounce-control algorithms and Müller Martini’s connected bindery modules show how predictive analytics reduce operator touchpoints.

Real-time data platforms feed cloud dashboards where maintenance teams schedule bearing swaps before a defect surfaces, cutting typical stoppages by 10%. Automation upgrade paths thus underpin aftermarket retrofits and new-press sales alike, reinforcing momentum in the flexographic printing machine market.

Geography Analysis

Asia-Pacific accounted for 40.10% of global revenues in 2025, aided by China’s capacity expansions and subsidy-driven equipment renewals that favor CI presses meeting “green, intelligent” criteria. Japan’s high labor costs accelerate adoption of robotic material handling, while South Korean and ASEAN converters invest in flexible packaging lines to serve regional snack and personal-care brands.

Middle East & Africa is the fastest-growing territory at 5.96% CAGR. Population growth, cold-chain improvements, and rising FMCG penetration spur new flexible packaging plants, drawing investments like UFlex’s PET chip facility in Egypt which anchors local resin supply. Gulf States are also piloting water-based ink retrofits to meet circular-economy targets.

North America and Europe, though mature, remain technology pacesetters as PFAS and VOC regulations tighten. The EU’s 25 ppb PFAS ceiling effective August 2026 forces converters to overhaul barrier coatings. North American printers face similar pressure from state-level solvent rules, driving upgrades to enclosed-chamber doctor-blade systems and heat-set air management. Consequently, replacement demand keeps the flexographic printing machine market dynamic despite slower macro-volume growth in these regions.

Competitive Landscape

Market consolidation is advancing yet stops short of oligopoly. XSYS’s USD 325 million purchase of MacDermid Graphics Solutions builds a plate-making powerhouse that can shave hours off lead times. INX’s acquisition of Coatings & Adhesives strengthens low-VOC coating innovation pipelines.

Bobst, Windmöller & Hölscher, and Uteco race to embed IIoT dashboards and remote diagnostics. Bobst’s Florence competence center showcases inline digital-flexo hybrids, signaling where press portfolios are headed. Meanwhile, Komori and Koenig & Bauer restructure to streamline R&D around automation modules.

New entrants leverage niche strengths: Domino integrates inkjet bars into narrow-web flexo frames for variable data labels, and Xeikon’s tie-up with EFI builds a combined service footprint for legacy Jetrion users. All players focus on rapid-changeover, solvent-free production lines, and predictive maintenance to differentiate amid the evolving flexographic printing machine market.

Flexographic Printing Machine Industry Leaders

Bobst Group SA

Edale UK Limited

OMET

Koenig & Bauer AG

Mark Andy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Xeikon and EFI formed a strategic partnership for digital label printing, integrating Jetrion customers into Xeikon’s service network

- January 2025: Bobst opened a 1,200 sqm competence center in Florence featuring inline flexo and digital systems linked to the Bobst Connect platform.

- November 2024: Koenig & Bauer announced a group realignment to sharpen segment focus and reduce overhead.

- September 2024: XSYS agreed to acquire MacDermid Graphics Solutions in a USD 325 million deal pending approval.

Global Flexographic Printing Machine Market Report Scope

A flexographic printing machine is an equipment that can print high-quality prints on various types of flexible materials. It is commonly used in the packaging industry to print labels, tags, packaging materials, and flexible packaging products. Flexographic printing, which uses flexible printed plates made of rubber or photopolymer, is a process that can be used for various purposes, such as printing on any flat surface.

The Flexographic Printing Machine Market is segmented by material (paper, corrugated cardboard, plastic films, metallic films), end-user industry (pharmaceutical, food & beverage, cosmetics, consumer electronics, logistics, print media), and by geography (North America (United States, Canada), Europe (United Kingdom, France, Germany, Italy, Spain), Asia-Pacific (China, Japan, India, Australia) Latin America (Brazil, Argentina, Mexico), The Middle East, and Africa (Saudi Arabia, South Africa, Egypt)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Paper and Paperboard |

| Plastic Films |

| Metallic Films and Foils |

| Corrugated Board |

| Others Material (Bioplastics, Laminates) |

| Central-Impression (CI) |

| Stack |

| In-Line / Modular |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Personal-Care and Cosmetics |

| Consumer Electronics |

| Logistics and E-commerce |

| Other End-user Industry |

| Conventional |

| Smart / IoT-Enabled |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Material | Paper and Paperboard | ||

| Plastic Films | |||

| Metallic Films and Foils | |||

| Corrugated Board | |||

| Others Material (Bioplastics, Laminates) | |||

| By Press Type | Central-Impression (CI) | ||

| Stack | |||

| In-Line / Modular | |||

| By End-User Industry | Food and Beverage | ||

| Pharmaceutical and Healthcare | |||

| Personal-Care and Cosmetics | |||

| Consumer Electronics | |||

| Logistics and E-commerce | |||

| Other End-user Industry | |||

| By Automation Level | Conventional | ||

| Smart / IoT-Enabled | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| Italy | |||

| United Kingdom | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the flexographic printing machine market?

The flexographic printing machine market is valued at USD 4.35 billion in 2026.

How fast is the flexographic printing machine market growing?

The market is registering a 3.09% compound annual growth rate between 2026 and 2031.

Which region holds the largest share of the flexographic printing machine market?

Asia-Pacific leads with 40.10% revenue share as of 2025.

What is the fastest-growing application segment?

Logistics and e-commerce packaging is expanding at a 7.42% CAGR through 2031.

Why are water-based inks gaining traction in the flexographic printing machine industry?

Tighter VOC and PFAS regulations in North America and Europe are pushing converters toward solvent-free, low-migration ink systems that comply with new limits.

How are equipment makers addressing the labor shortage challenge?

Manufacturers are embedding IoT sensors, digital twins, and automated material-handling robots to reduce manual interventions and maintain consistent print quality.

Page last updated on: