Saudi Arabia Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

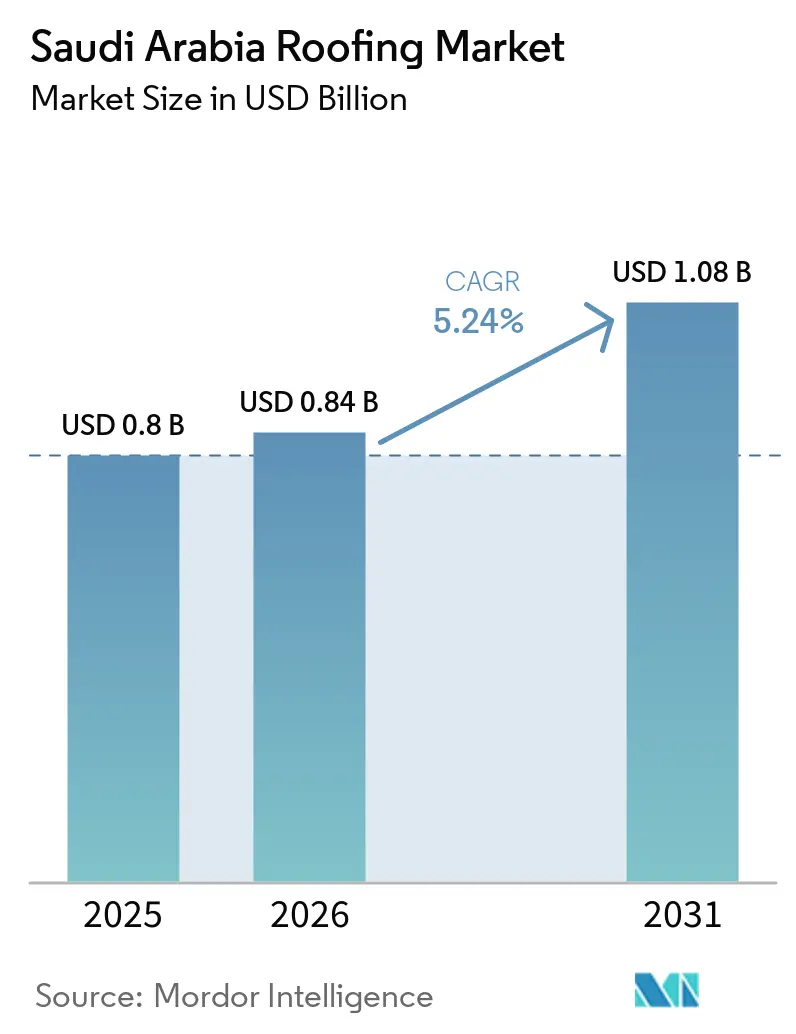

| Base Year Market Size (2025) | USD 0.8 Billion |

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Roofing Market Analysis by Mordor Intelligence

The Saudi Arabia Roofing Market size is expected to increase from USD 0.8 billion in 2025 to USD 0.84 billion in 2026 and reach USD 1.08 billion by 2031, growing at a CAGR of 5.24% over 2026-2031. Robust public spending tied to Vision 2030 giga-projects is decoupling demand from cyclical housing starts, pushing suppliers to scale capacity for climate-rated, energy-efficient systems. Procurement decisions favor membranes and insulated metal panels that withstand 45 °C summer temperatures, sandstorms, and longer design lives demanded by sovereign owners. Local investors are consolidating distribution and production to curb import exposure, while foreign brands deepen in-kingdom manufacturing through acquisitions and joint ventures. At the same time, tighter energy-efficiency codes and rooftop-solar incentives are accelerating the shift toward reflective, PV-ready assemblies with lower life-cycle costs[1]Construction Briefing, “Sindalah Island Opens,” constructionbriefing.com.

Key Report Takeaways

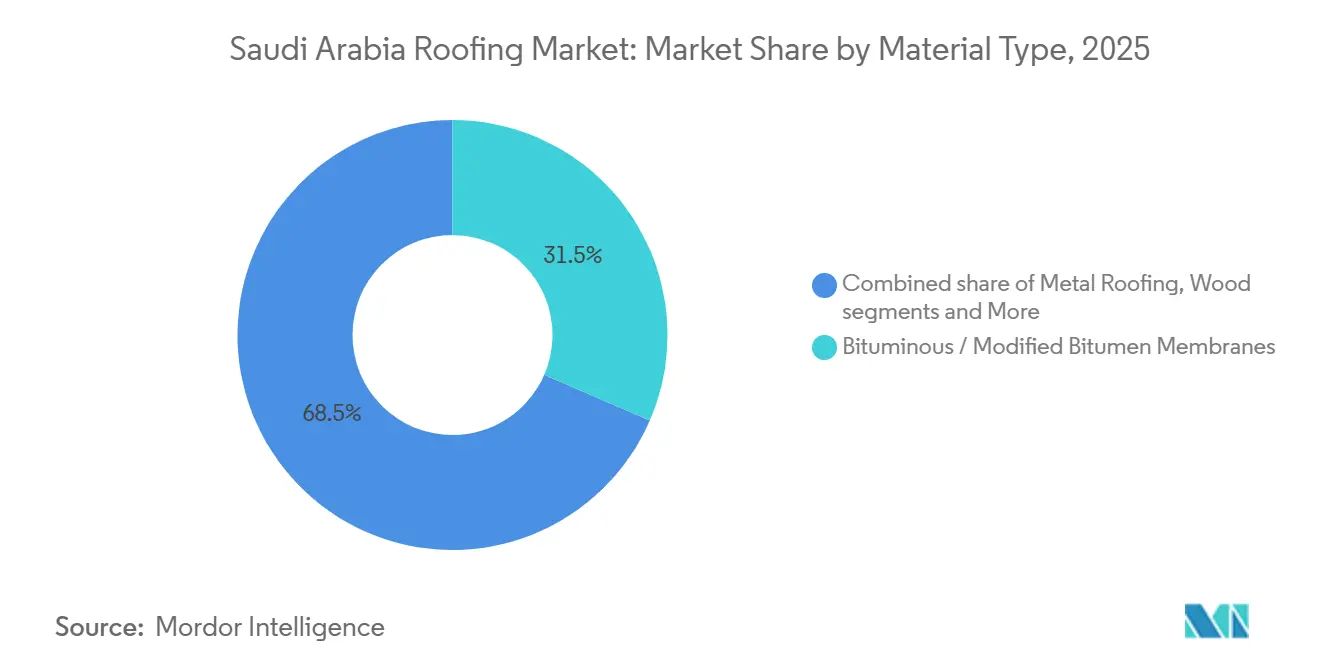

- By material type, bituminous and modified bitumen membranes held 31.5% of the Saudi Arabia roofing market share in 2025, while metal roofing is forecast to expand at a 6.71% CAGR through 2031.

- By construction type, new construction accounted for 76.0% of the Saudi Arabia roofing market size in 2025, while reroofing and replacement are projected to grow at a 6.08% CAGR through 2031.

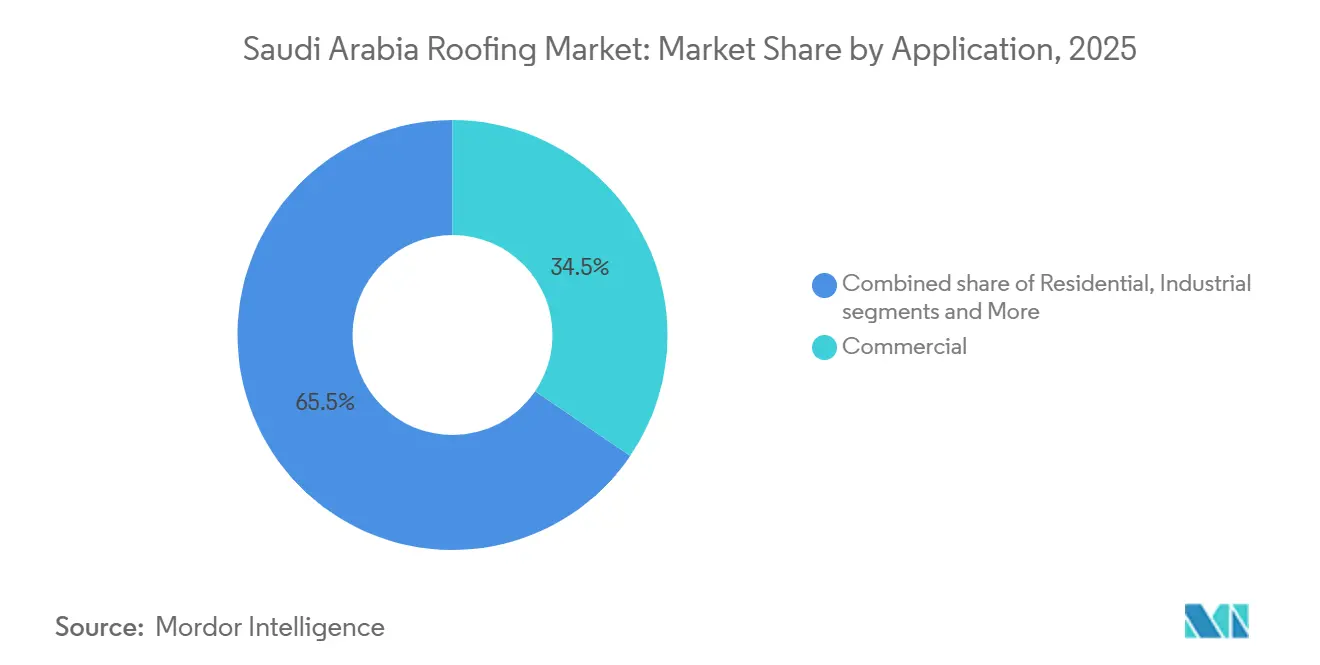

- By application, commercial accounted for 34.5% of the Saudi Arabia roofing market size in 2025, while industrial is advancing at a 7.02% CAGR through 2031.

- By city, Riyadh held 31.0% of the Saudi Arabia roofing market share in 2025, while the Dammam Metropolitan Area is forecast to grow at a 6.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-projects and housing programs generating large, sustained roofing demand across segments | 1.8% | National, concentrated in NEOM, Red Sea, Qiddiya, Riyadh, Jeddah | Long term (≥ 4 years) |

| Harsh climate pushing demand for durable, insulated, reflective roofing systems | 1.2% | National, with acute relevance in Riyadh, Dammam, and northern industrial zones | Medium term (2-4 years) |

| Industrial/logistics expansion favoring metal and single-ply membranes | 1.0% | National, early gains in Jeddah port zones, Dammam logistics corridors, NEOM Oxagon | Medium term (2-4 years) |

| Rooftop solar momentum and energy-efficiency codes encouraging cool roofs and PV-ready assemblies | 0.7% | National, led by Riyadh, Jeddah, and NEOM renewable-energy mandates | Long term (≥ 4 years) |

| Replacement/retrofit cycle on aging public and commercial stock boosting re-roofing volumes | 0.6% | Riyadh, Jeddah, Dammam metropolitan cores with 1980s–2000s building stock | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Projects and Housing Programs Generating Large, Sustained Roofing Demand Across Segments

The Public Investment Fund is allocating at least USD 40 billion annually to domestic mega-developments, supporting a long-term pipeline of projects covering hundreds of millions of square meters. The opening of Sindalah Island in 2024 highlights the transition of giga-projects from planning to execution, increasing demand for premium membranes and metal panels. Projects such as NEOM, Red Sea Global, and Qiddiya require high-reflectance surfaces and PV integration, favoring suppliers with proven climate-rated systems and strong local manufacturing capabilities. The scale and technical requirements create challenges for smaller fabricators, pushing the Saudi Arabian roofing market toward higher concentration. NEOM’s 100-year development timeline further ensures demand visibility beyond 2030.

Harsh Climate Pushing Demand for Durable, Insulated, Reflective Roofing Systems

Saudi Arabia's summer temperatures, often exceeding 45 °C, along with intense UV rays and frequent dust events, continue to challenge conventional bitumen products. The Saudi Energy Efficiency Center has introduced sixteen new insulation regulations, increasing envelope R-values and setting higher reflectance standards. Major infrastructures, such as King Abdulaziz International Airport, have adopted PVDF-coated aluminum to meet durability and low-maintenance requirements. Specifiers are now focusing on life-cycle thermal savings over initial costs, favoring single-ply TPO and PVC membranes over traditional dark bitumen in most commercial projects. These climate challenges are driving demand for the premium segment of Saudi Arabia's roofing market, leading to higher average selling prices and increased adoption of warranty-backed service contracts.

Industrial and Logistics Expansion Favoring Metal and Single-Ply Membranes

Saudi Arabia's diversification efforts are driving the growth of e-commerce fulfillment centers, bonded warehouses, and manufacturing lines for wind-turbine blades. These structures primarily feature long-span, low-slope roofs. The need for faster construction has increased the use of factory-finished steel panels and mechanically attached membranes. The announcement of Carrier and Alat’s HVAC plant in 2024 highlights the industrial demand for durable roofing that can support heavy rooftop equipment. In the Saudi Arabian roofing market, metal profiles and reflective synthetics are prioritized over tiles and shingles due to their ability to reduce construction time, lower structural steel weight, and enable future solar retrofits.

Rooftop Solar Momentum and Energy-Efficiency Codes Encouraging Cool Roofs and PV-Ready Assemblies

Saudi Arabia's renewable energy target of 58.7 GW and net-metering incentives priced at USD 0.019 per kWh are encouraging property owners to install PV arrays. Building codes now include solar-ready guidelines, requiring white membranes and high-puncture resistance to support ballasted racking systems. Sika's Sarnafil and Sikaplan lines reflect this shift with features like weldable seams and a 20-year reflectance warranty. Financing terms now favor green roofs by offering lower borrowing costs, increasing the adoption of reflective single-ply and insulated metal solutions in commercial and institutional projects. This trend is expected to boost the long-term CAGR for suppliers providing integrated cool-roof and PV-ready packages in Saudi Arabia's roofing market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile material costs and FX/import exposure squeezing contractor margins and bid certainty | -0.7% | National, with acute impact on import-dependent membrane and specialty-metal suppliers | Short term (≤ 2 years) |

| Execution constraints—skilled applicator shortages, extreme weather windows, and HSE compliance | -0.6% | National, concentrated in Riyadh, Jeddah, Dammam, and NEOM construction zones | Medium term (2-4 years) |

| Fragmented supply base and price-led tendering intensifying competition and quality variance | -0.5% | National, with heightened pressure in government procurement and mega-project bidding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Material Costs and FX/Import Exposure Squeezing Contractor Margins

Steel and bitumen prices fluctuate with global commodity trends, reducing the reliability of fixed-price contracts. PIF invested USD 3.33 billion in Saudi Iron & Steel to strengthen domestic supply, but many specialty membranes are still imported from Europe or Asia. Import tariffs and currency fluctuations increase costs, which mid-tier contractors find difficult to manage. Public Works contracts allow adjustments for tax or customs changes, but do not provide relief for commodity price increases. Since tenders are price-driven, some bidders lower the quality or delay projects when material costs rise, negatively affecting the CAGR of Saudi Arabia's roofing market[2]Ministry of Finance, “Public Works Contract Form,” mof.gov.sa.

Execution Constraints—Skilled Applicator Shortages, Extreme Weather Windows, and HSE Compliance

As giga-projects in Saudi Arabia increased, a shortage of certified installers occurred due to Saudization quotas and pandemic-related attrition. Temperatures above 45 °C reduced daytime workability for torch-applied membranes, limiting safe installation to night shifts during summer. Stricter HSE protocols now require additional inspections, insurance coverage, and performance bonds, increasing costs and timelines. Additionally, the requirement to subcontract at least 30% of work to local Saudi firms complicates coordination on large roofs with tight schedules. These challenges delay project deliveries and increase risk premiums, partially offsetting the growth in Saudi Arabia's roofing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Modified Bitumen Retains Leadership as Metal Systems Gain Industrial Ground

Bituminous and modified bitumen membranes accounted for 31.5% of the Saudi Arabia roofing market in 2025, maintaining their leading position, as flat commercial and public roofs still dominate building design across the Kingdom. That position reflects long-standing confidence in their use on concrete roof decks and the support of SASO 1505 performance benchmarks for APP and SBS systems under Saudi climate conditions. In the Saudi Arabia roofing industry, APP variants are gaining preference on exposed roofs because higher heat resistance matters more where thermal cycling is severe and UV exposure is persistent. Single-ply products such as TPO, ethylene propylene diene monomer, or EPDM, and polyvinyl chloride, or PVC, are also gaining ground on commercial cool-roof projects where energy compliance and reflectivity are part of the specification.

Metal roofing is the fastest-growing material group and is projected to advance at a 6.71% CAGR from 2026 to 2031, supported by warehouses, factories, and data centers that prefer pre-engineered steel structures with insulated panels. A December 2025 study in Results in Engineering found that composite roof systems using high-density insulation, such as PIR boards with reflective outer layers, delivered the strongest energy-reduction benefits, supporting the move toward higher-performance metal assemblies. Clay and concrete tiles still appear in heritage and Najdi-style projects. Still, their role stays limited in the mainstream Saudi Arabia roofing market because flat roof forms dominate both residential and commercial stock. Asphalt shingles and wood remain niche materials, while spray foam, cementitious waterproofing, and reflective coatings continue to serve retrofit situations where existing substrate conditions make torch-applied systems less suitable.

By Construction Type: New Build Holds the Volume Base While Retrofit Gains Speed

New construction accounted for 76.0% of the Saudi Arabia roofing market in 2025, underscoring the continued strength of demand tied to the Kingdom’s large project pipeline. That volume base is supported by ROSHN’s housing rollout, Red Sea Global hospitality assets, Qiddiya development, and the ongoing build-out at Diriyah. The Royal Commission for Riyadh City awarded USD 637 million in residential infrastructure contracts in May 2026 for Al Qirawan, Al Narjis, and Namar, confirming that greenfield supply in the capital is still moving from planning to execution. In the Saudi Arabia roofing industry, this keeps large volumes attached to new slabs and decks, and supports standard installation methods that fit fresh construction schedules.

Reroofing and replacement are the fastest-growing construction types. They are expected to expand at a 6.08% CAGR through 2031 as older public and commercial buildings reach the end of their waterproofing life. That segment has a different product mix because repair work often requires substrate preparation, layer removal, overlays, or non-flame systems for occupied buildings. Self-adhered SBS, liquid-applied polyurethane, and elastomeric acrylic coatings therefore have a stronger place in retrofit work than in commodity new-build supply. Public-sector maintenance spending may also pick up before Expo 2030 activity intensifies, keeping reroofing demand alongside the much larger new-build base rather than competing with it.

By Application: Commercial Leads Revenue While Industrial Sets the Growth Pace

Commercial accounted for 34.5% of the Saudi Arabia roofing market in 2025, making it the largest application, as malls, hotels, office complexes, airports, and mixed-use podium developments generate large, contiguous roof areas. Projects such as Diriyah Square and high-profile urban mixed-use schemes continue to support premium waterproofing demand where performance warranties and project image matter. Saudi Real Estate Company, or Al Akaria, awarded a USD 123.5 million contract in May 2026 for Package One of Porta Jeddah, while Riyad Capital’s Dar Al Salam mixed-use development added another major commercial reference point in the pipeline. This keeps the Saudi Arabia roofing market tied to a steady stream of commercial work even when some prestige projects are rescaled or rephased.

Industrial is the fastest-growing application and is forecast to rise at a 7.02% CAGR through 2031, supported by manufacturing localization, logistics build-out, and the growing data center base. ASMO’s 1.4 million-square-meter SPARK logistics hub and Khazna’s 200-megawatt Dammam campus illustrate the type of industrial asset that requires insulated metal roofing or reflective single-ply systems with higher service performance. Residential demand remains important through ROSHN communities and National Housing Company-linked programs, including the USD 880 million Noor Khuzam project and other large north Riyadh schemes. Institutional and niche leisure assets also contribute, but the strongest growth signal in the Saudi Arabia roofing market is still coming from industrial roofs that combine weather protection, insulation, and long-life service needs in one system.

Geography Analysis

Riyadh accounted for 31.0% of Saudi Arabia's roofing market share in 2025, making it the largest demand center across the Kingdom. The city’s strength comes from range as much as scale, because housing, mixed-use, civic projects, and logistics facilities are all moving at once. RCRC awarded USD 637 million in infrastructure contracts in May 2026 for 3 major residential land plots, which confirms continued activation of new roofing demand in Riyadh’s northern and southern corridors. King Salman Park and New Murabba also maintain commercial and institutional specifications, while airport-linked logistics development adds a parallel industrial requirement. Riyadh, therefore, anchors the Saudi Arabia roofing market with a pipeline broad enough that no single project reset is likely to remove its leadership position.

Jeddah’s role is different because reroofing is a larger part of the local mix, especially across older commercial and industrial stock near legacy business and port districts. At the same time, new logistics and hospitality projects keep fresh installation demand visible across the city. Mawani signed a USD 66.7 million contract in March 2026 with Sultan Logistics for a 200,000-square-meter integrated logistics zone at Jeddah Islamic Port, adding further demand for large-span industrial roofing in the port corridor. Premium hotel and mixed-use developments also support higher-value waterproofing systems where appearance, warranty length, and operating performance matter more than the lowest installed cost. Jeddah’s coastal climate and its larger stock of aging assets together keep both premium new build and replacement work active in the Saudi Arabia roofing market.

The Dammam Metropolitan Area is projected to grow at a 6.34% CAGR through 2031, which makes it the fastest-expanding geography in the Saudi Arabia roofing market. Its advantage is the breadth of industrial demand across petrochemicals, manufacturing, logistics, and data centers, rather than reliance on a single high-visibility giga-project. ASMO started work on its 1.4 million-square-meter SPARK hub in May 2026, and MEDLOG 1 was inaugurated at King Abdulaziz Port in February 2026 as another large industrial roofing reference. The rest of the country still matters because Makkah, Madinah, Yanbu, and other cities are adding residential, tourism, and industrial assets that provide a meaningful volume floor outside the 3 main metropolitan nodes.

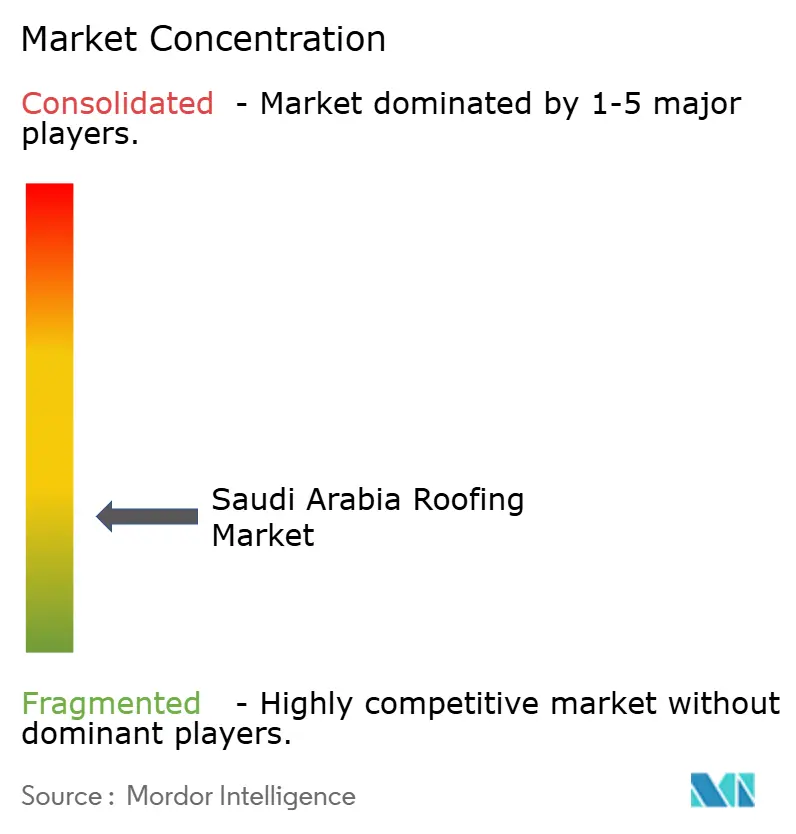

Competitive Landscape

Local fabricators, regional importers, and global system integrators compete in a fragmented field where government tenders prioritize price yet demand stringent technical compliance. PIF’s 30% equity entry into Masdar for Building Materials arms a domestic distributor with fresh capital for digital platforms and inventory expansion, potentially reshaping supply reliability. At the same time, foreign incumbents pivot to in-kingdom manufacturing to secure local-content credits.

Sika’s November 2025 purchase of Gulf Seal adds bituminous sheets to its Saudi portfolio and secures a Riyadh plant capable of reaching GCC export markets. Aramco’s materials alliance with CNBM signals a move toward non-metallic composite roofs aligned with decarbonization goals, hinting at future competitive entries that combine low-carbon materials with megaproject access. Meanwhile, construction-chemical suppliers push warranty-backed integrated systems that bundle membranes, insulation, and edge-metal in a single vendor contract, lowering risk for project owners.

Digital procurement and building information modeling are now differentiators. Vendors providing BIM-ready roof libraries gain specification priority on LEED-targeted towers. Local SMEs respond by partnering with global brands to access technology and training, meeting a 30% subcontracting rule within public contracts. Overall, the Saudi Arabia roofing market is bifurcating into premium integrators that address giga-projects and commodity suppliers serving villa and small-commercial segments, with middle-tier players squeezed by code escalation.

Saudi Arabia Roofing Industry Leaders

Saudi Basic Industries Corporation (SABIC)

Saudi Ceramic Company

Saudi Bitumen Industries Co. Ltd (SABIT)

Saint-Gobain

Owens Corning

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ASMO, a joint venture between Saudi Aramco and DHL, and Arcapita commenced construction of a 1.4 million square meter logistics hub at King Salman Energy Park in Dammam. The facility targets LEED Gold certification, generating sustained demand for reflective single-ply roofing membranes across a flagship industrial footprint that directly supports Saudi Arabia’s Vision 2030 logistics strategy.

- May 2026: The Royal Commission for Riyadh City awarded USD 637 million in infrastructure contracts for 3 residential land plots in Al Qirawan, 3.6 million square meters, Al Narjis, 87,000 square meters, and Namar, 570,000 square meters, unlocking substantial greenfield roofing demand in Riyadh’s northern and southern corridors ahead of housing-unit construction.

- March 2026: Mawani signed a USD 66.7 million contract with Sultan Logistics to develop a 200,000 square meter integrated logistics zone at Jeddah Islamic Port in the Al-Khumra area, adding large-span industrial roofing demand to Jeddah’s port corridor.

- February 2024: MEDLOG 1, an MSC-operated integrated logistics park of more than 100,000 square meters with annual handling capacity exceeding 300,000 twenty-foot equivalent units, was inaugurated at King Abdulaziz Port in Dammam, marking another large-span industrial roofing delivery in the Dammam Metropolitan Area.

Saudi Arabia Roofing Market Report Scope

The roofing market involves the manufacturing, distribution, installation, and maintenance of roofing materials and systems. Roofing is an essential part of construction and architecture, as it provides protection and shelter for buildings and their occupants from various weather conditions, including rain, snow, wind, and sunlight.

The Saudi Arabian roofing market is segmented by roofing material (bituminous roofing, metal roofing, tile roofing, and others), roofing type (flat roof and slope roof), and application (residential, commercial, and industrial). The report offers market sizes and forecasts in value (USD) for all the above segments.

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Cities | Riyadh |

| Jeddah | |

| DMA (Dammam Metropolitan Area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the current size of Saudi Arabia roofing demand?

The Saudi Arabia roofing market size stood at USD 802.4 million in 2025 and is projected to reach USD 1,088.47 million by 2031 at a 5.24% CAGR.

Which material category leads roofing demand in Saudi Arabia?

Bituminous and modified bitumen membranes accounted for 31.5% of the market in 2025, as flat roof construction remains the dominant building form across commercial and public assets.

Which roofing material is growing the fastest in Saudi Arabia?

Metal roofing is the fastest-growing material segment with a 6.71% CAGR through 2031, supported by warehouses, factories, and data centers.

Why is industrial roofing growing faster than other applications?

Industrial roofing is projected to expand at a 7.02% CAGR as Saudi Arabia adds logistics hubs, manufacturing capacity, and data centers that require large-span, insulated, and durable roof systems.

Which city leads roofing demand in the Kingdom?

Riyadh led with 31.0% share in 2025 due to the breadth of its housing, mixed-use, infrastructure, and logistics pipeline.

What is the main opportunity in replacement roofing across Saudi Arabia?

Reroofing and replacement are expected to grow at a 6.08% CAGR as older public and commercial buildings reach the end of their waterproofing life and require repair-friendly systems, such as self-adhered membranes and liquid coatings.

Page last updated on: