Squash Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 5.41 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

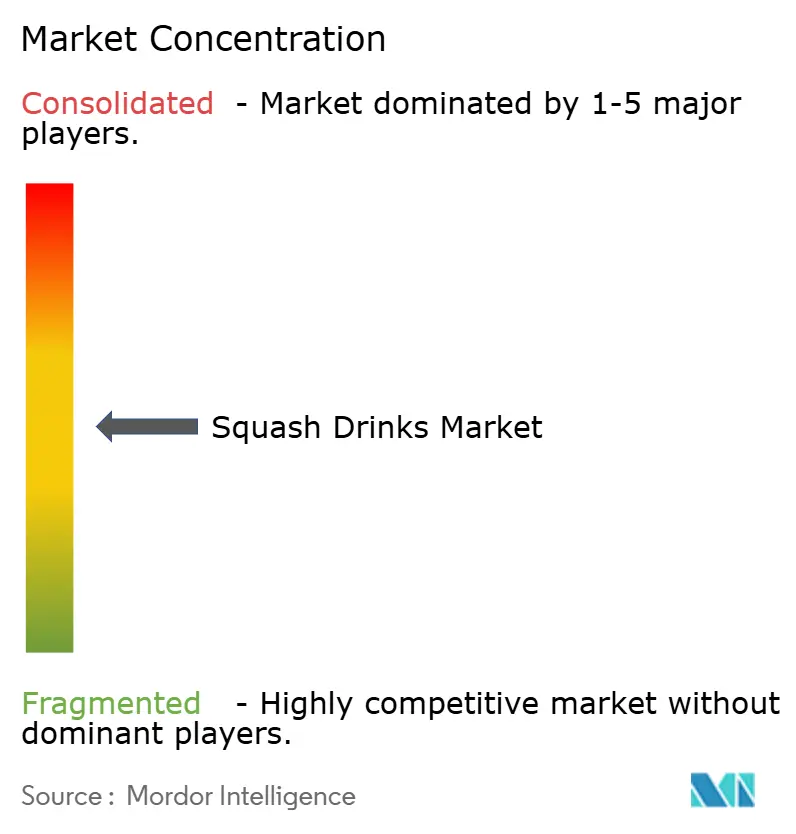

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Squash Drinks Market Analysis by Mordor Intelligence

The squash drinks market size was valued at USD 4.19 billion in 2025 and estimated to grow from USD 4.37 billion in 2026 to reach USD 5.41 billion by 2031, at a CAGR of 4.36% during the forecast period of 2026 to 2031. The market is growing as more people prepare beverages at home. Squash drinks, being concentrated, are more cost-effective per serving compared to many ready-to-drink options, making them a preferred choice for households looking to manage budgets effectively. Stricter regulations on sugar content are driving companies to reformulate their products with no-added-sugar options, improve transparency in ingredient labeling, and enhance their nutritional value. These changes are helping brands align with consumer demand for healthier beverage choices. Furthermore, the introduction of functional variants and recipes made with real fruit is expanding the appeal of squash drinks, attracting a broader range of consumers, including those who previously did not consider them part of their regular consumption. The market remains moderately consolidated, with key players such as Carlsberg Group (Britvic plc) and Suntory Holdings maintaining a significant presence.

Key Report Takeaways

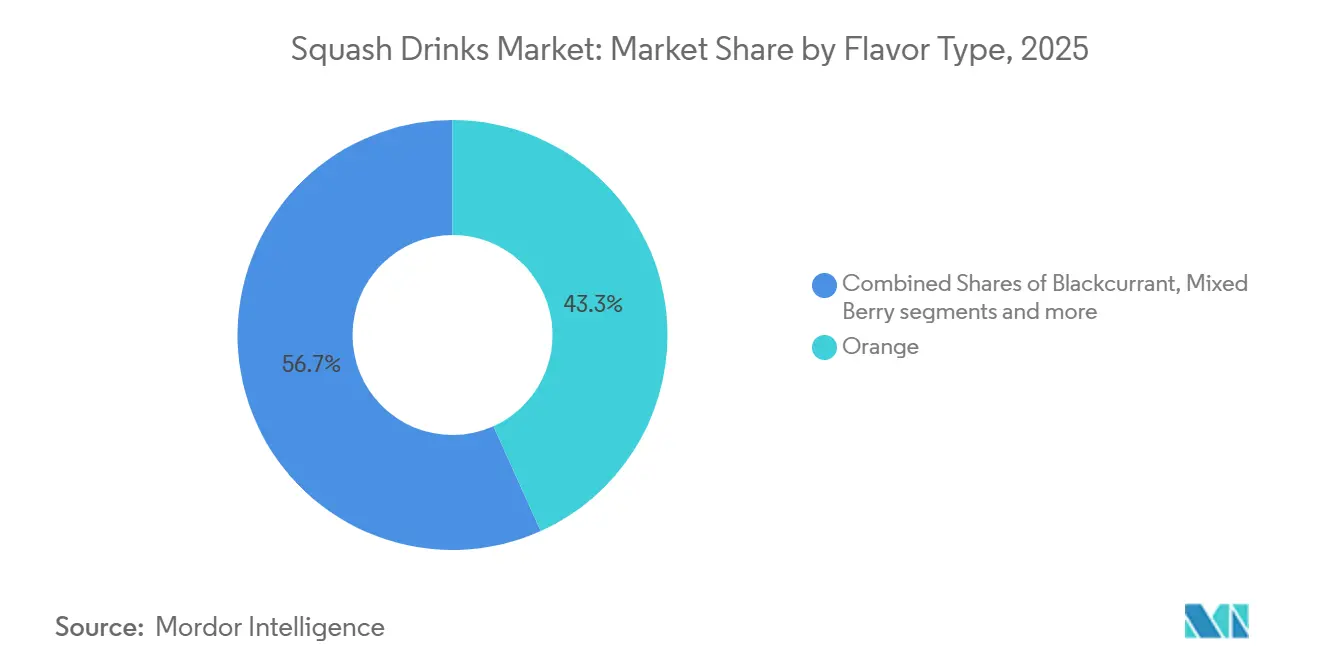

- By flavor type, orange held 43.26% revenue share in 2025, while mixed berry is forecast to expand at a 5.71% CAGR through 2031.

- By sugar content, added-sugar accounted for 76.15% of revenue in 2025, while no-added-sugar is projected to grow at a 5.27% CAGR through 2031.

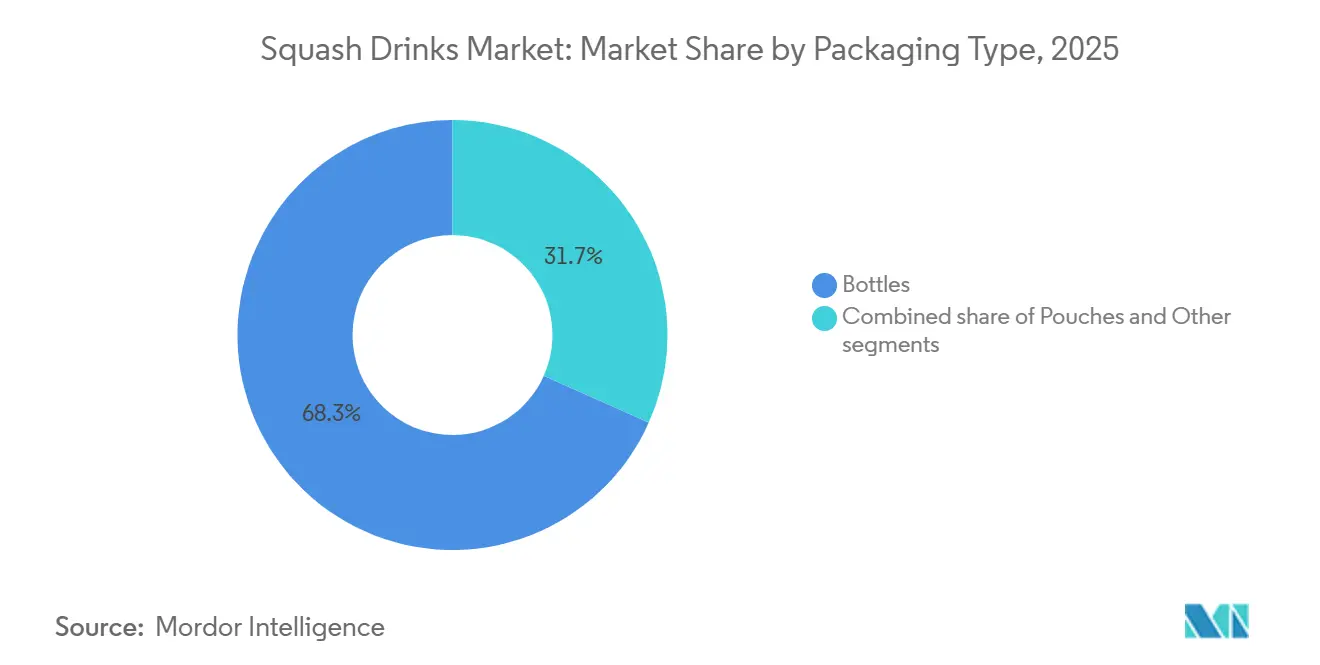

- By packaging type, bottles accounted for 68.32% of revenue in 2025, while pouches are expected to grow at a 6.33% CAGR through 2031.

- By distribution channel, off-trade represented 68.82% of revenue in 2025, while on-trade is forecast to grow at a 5.46% CAGR through 2031.

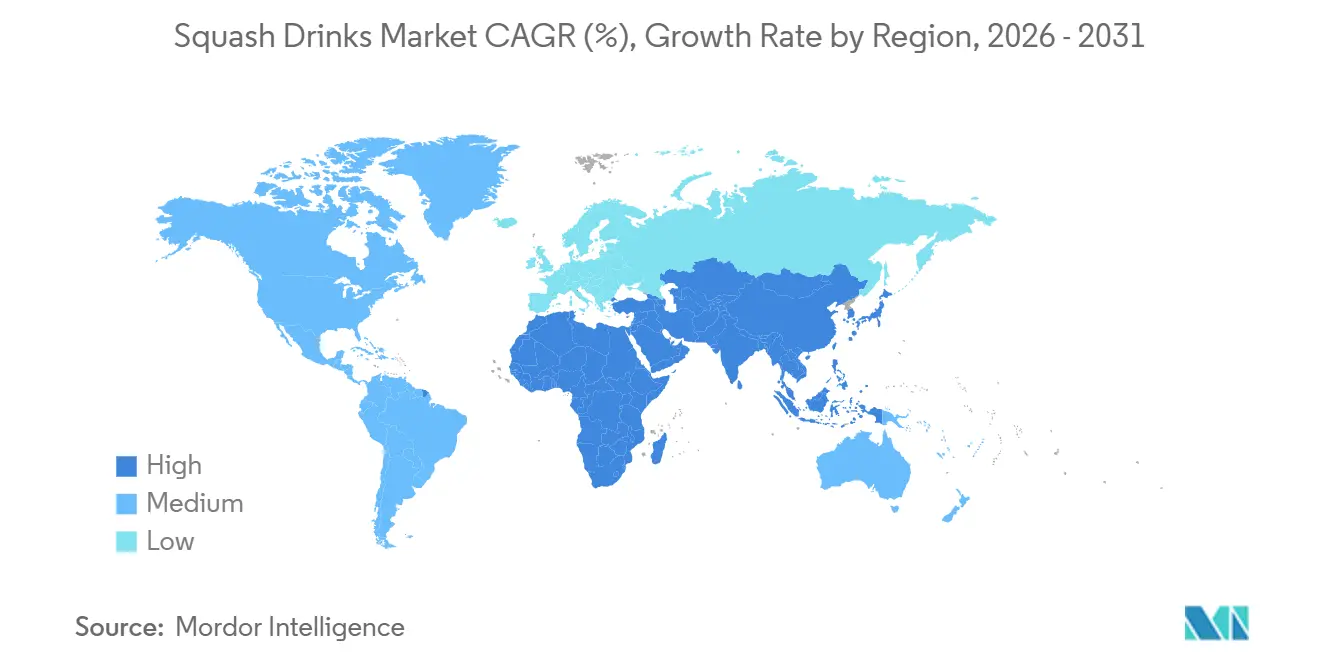

- By geography, North America led with 38.47% revenue share in 2025, while Asia-Pacific is projected to expand at a 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Squash Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of at-home beverage preparation | +1.0% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Seasonal demand for refreshing beverages during warmer weather conditions | +0.6% | Global, most acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Rising consumer preference for healthier and low-sugar beverage alternatives | +0.8% | Global, concentrated in North America and Europe | Medium term (2–4 years) |

| Product innovation in flavors and formulations | +0.7% | Global | Medium term (2–4 years) |

| Influence of health-conscious parenting trends | +0.5% | North America, Europe, Australia | Medium term (2–4 years) |

| Popularity of beverages with natural fruit ingredients | +0.6% | Global, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for healthier and low-sugar beverage alternatives

Consumers are increasingly seeking healthier, low-sugar beverage options, driving growth in the global squash drinks market. People are becoming more aware of the negative effects of high sugar consumption, such as obesity and other health issues, leading them to choose beverages that align with their wellness goals. For instance, a 2025 survey by the International Food Information Council (IFIC) revealed that 61% of Americans were actively trying to reduce their sugar intake[1]Source: International Food Information Council, "2025 IFIC Food and Health Survey", ific.org. This trend reflects a growing shift toward healthier consumption habits. In response, companies in the squash drinks market are focusing on creating products with no added sugar, reformulating existing offerings, and introducing innovative, health-focused options. These efforts aim to meet the changing demands of consumers who are prioritizing nutrition and healthier lifestyles.

Seasonal demand for refreshing beverages during warmer weather conditions

Hot weather significantly increases demand for refreshing beverages, making it a key driver of the global squash drinks market. During warmer months, consumers tend to prefer drinks that help them stay cool and hydrated, which increases the popularity of fruit-based and concentrated beverages like squash. This trend is especially pronounced in regions with high temperatures, where prolonged heatwaves directly affect drinking habits. For example, the Press Information Bureau (PIB) reported that in April 2026, temperatures in parts of India ranged from 40°C to 44°C, with Sri Ganganagar, Rajasthan, recording the highest temperature of 44.5°C[2]Source: Press Information Bureau, "IMD Issues Comprehensive Heatwave Guidance as Temperatures Rise Across Regions", pib.gov.in. Such extreme heat conditions lead to increased consumption of homemade drinks and fruit concentrates, as they are convenient and cost-effective ways to stay refreshed. This seasonal surge in demand plays a significant role in driving the growth of the squash drinks market, particularly in regions prone to high temperatures.

Popularity of beverages with natural fruit ingredients

The growing demand for beverages made with natural fruit ingredients is driving the global squash drinks market. Consumers are now looking for products with simpler, more transparent labels and ingredients they can trust. This shift in preference has pushed manufacturers to focus on using real fruit content, highlighting nutritional benefits, and sourcing high-quality ingredients. People are also drawn to beverages that promote health and authenticity, making fruit-based formulations more appealing. For example, in 2025, Rasna introduced its Rasna Rich range, offering multiple fruit flavors while emphasizing nutrition and family wellness. This launch reflects a broader market trend, where brands are innovating with fruit-based recipes and clear labeling to attract health-conscious buyers. These changes are helping companies differentiate their products and meet the growing demand for healthier beverage options.

Product innovation in flavors and formulations

Innovation in flavors and formulations is driving the growth of the global squash drinks market. Manufacturers are moving beyond traditional flavors and focusing on creating unique and appealing options to attract a wider range of consumers. These innovations include introducing premium flavor combinations, adding functional ingredients, and developing health-focused formulations. For example, in March 2026, Robinsons expanded its Fruit Creations range by launching a new Strawberry, Cherry and Lime flavor. This product was specifically designed to appeal to adults, offering a more sophisticated taste and creating opportunities for premium consumption occasions. Such efforts highlight how brands are leveraging new flavor profiles and improved product formulations to make squash drinks more appealing, engage consumers more effectively, and sustain market growth over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content concerns associated with traditional squash drinks | -0.4% | Global, highest in United Kingdom and North America | Short term (≤ 2 years) |

| Competition from ready-to-drink and functional beverage categories | -0.5% | Global | Medium term (2–4 years) |

| Increasing availability of homemade beverage alternatives | -0.3% | North America, Europe | Medium term (2–4 years) |

| Presence of artificial colors, preservatives, and additives | -0.2% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High sugar content concerns associated with traditional squash drinks

Concerns about the high sugar content in traditional squash drinks are becoming a significant challenge for the global squash drinks market. Consumers are increasingly aware of the negative health effects of consuming too much sugar, such as obesity, diabetes, and other related conditions. This growing awareness has led to greater scrutiny of the sugar levels in conventional beverage products. For instance, the National Health Service (NHS) in the United Kingdom advises that adults should limit their intake of free sugars to no more than 30 grams per day[3]Source: National Health Service (NHS), "Sugar: The Facts", nhs.uk. This recommendation reflects a broader trend of people prioritizing healthier eating habits and reducing sugar consumption. As a result, there is a rising demand for squash drinks with reduced sugar or no added sugar. Manufacturers are under pressure to reformulate their products to meet these preferences while maintaining an appealing taste for consumers. This shift is driving innovation in the market, as companies work to balance health-conscious formulations with flavor consistency to retain and attract customers.

Competition from ready-to-drink and functional beverage categories

The squash drinks market is facing growing competition from ready-to-drink and functional beverages, posing a major challenge to its growth. Consumers are increasingly opting for beverages that are easy to consume, require no preparation, and offer added benefits such as improved health, wellness, or enhanced performance. Products like functional waters, energy drinks, and other enhanced beverages are directly competing with squash drinks for daily consumption. This shift is particularly noticeable among younger consumers who value convenience, portability, and multi-functional options in their beverages. As a result, manufacturers of squash drinks are under pressure to innovate and diversify their offerings. They need to focus on creating products that not only appeal to traditional consumers but also attract new customers by addressing these evolving preferences. By introducing features such as improved nutritional benefits, unique flavors, and convenient packaging, squash drink producers can stay competitive in this increasingly crowded market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor Type: Orange Leads While Berry Profiles Advance Fastest

Orange flavor held the largest share in the global squash drinks market, accounting for 43.26% of the total market share in 2025. This dominance is attributed to its widespread popularity among consumers, appealing to a broad range of age groups and preferences. The refreshing orange flavor, combined with its availability across various product options, has solidified its position in the market. Its strong presence in both developed and emerging markets, supported by well-established brands, has further reinforced its leadership in the segment.

Mixed berry flavor is expected to experience the fastest growth in the squash drinks market, with a projected CAGR of 5.71% during the forecast period through 2031. This growth is driven by rising consumer interest in berry-based flavors, which are often associated with health benefits, such as antioxidants. The rising demand for clean-label products and beverages perceived as having nutritional value is also boosting the popularity of mixed berry flavors. Furthermore, innovations in product offerings and the growing trend toward premium and functional drinks are expected to significantly drive this segment's expansion.

By Sugar Content: Added Sugar Still Dominates While No-Added-Sugar Gains Momentum

Products with added sugar accounted for 76.15% of the global squash drinks market in 2025. This dominance is driven by long-standing consumer preferences for traditional flavors and the wide availability of these products across various retail channels. Their affordability and familiarity make them a popular choice among consumers of all age groups. Despite the growing focus on health and wellness, these products continue to enjoy steady demand due to their established market presence.

On the other hand, the no-added-sugar segment is expected to grow the fastest through 2031, with a projected CAGR of 5.27% during the forecast period. Increasing awareness about the health risks associated with high sugar consumption is pushing consumers toward healthier beverage options. The rising popularity of low-calorie and clean-label products is further boosting demand in this segment. To cater to these changing preferences, manufacturers are introducing naturally sweetened, health-focused squash drinks that are gaining traction among health-conscious buyers.

By Packaging Type: Bottles Stay Core While Pouches Expand Into New Use Cases

Bottles accounted for the largest share of the global squash drinks market in 2025, representing 68.32% of the total market size. This dominance is due to their convenience: bottles are easy to reseal, store, and reuse, making them ideal for households. Families and regular consumers prefer bottled packaging for its practicality in multi-serve usage. Additionally, bottles are widely available across retail channels, further boosting demand and solidifying their market position.

Pouches are projected to be the fastest-growing packaging format in the squash drinks market, with a CAGR of 6.33% during the forecast period of 2026 to 2031. The growing preference for lightweight, portable packaging is driving this growth. Pouches are convenient for on-the-go consumption and are easy to handle, making them popular among consumers. Moreover, the growing focus on sustainability and the reduced use of packaging materials are encouraging manufacturers to adopt pouch-based formats, which align with eco-friendly initiatives and consumer preferences for environmentally conscious products.

By Distribution Channel: Off-Trade Remains Largest While On-Trade Rebuilds

In 2025, the off-trade was the dominant distribution channel in the global squash drinks market, accounting for 68.82% of total revenue. This channel includes supermarkets, hypermarkets, convenience stores, and online platforms, all popular among consumers for their convenience and accessibility. The availability of a wide range of products, the option to buy in bulk, and frequent promotional offers have made off-trade the preferred choice for household purchases. Established retail networks and consistent marketing efforts have further strengthened its market position.

On the other hand, on-trade distribution is expected to grow faster, with a projected CAGR of 5.46% through 2031. This channel, which includes restaurants, cafés, hotels, and other foodservice establishments, is gaining traction as more consumers seek out-of-home beverage experiences. The rising demand for customized drink options and the growing popularity of dining out are key factors driving this growth. Moreover, the expansion of the hospitality and foodservice industries, particularly in emerging markets, is likely to boost the demand for squash drinks through on-trade channels in the coming years.

Geography Analysis

North America held 38.47% of the global squash drinks market share in 2025, making it the leading region by value. This dominance is due to the widespread use of squash drinks in households, especially in developed countries where these beverages are a common part of family purchases. Consumers in the region also have higher spending power, which drives demand for premium products, including healthier and enhanced formulations. However, the market faces growing competition from alternatives like flavored water and functional beverages, pushing manufacturers to innovate and stay competitive.

The Asia-Pacific region is expected to grow the fastest, with a projected CAGR of 5.74% through 2031. This growth is fueled by increasing demand for affordable beverage options, rapid urbanization, and a strong preference for fruit-based flavors that cater to local tastes. The region is also benefiting from improved retail distribution networks and manufacturers' expanded product portfolios. Additionally, the rising popularity of health-focused products and changing consumption habits are creating new opportunities in both emerging and developed markets within the region.

Europe represents a mature market where consistent consumption patterns continue to support steady demand. However, shifting consumer preferences are encouraging manufacturers to focus on healthier options, transparent ingredient labeling, and unique product offerings to differentiate themselves. In the Middle East and Africa, cultural traditions drive consistent demand for squash drinks, while South America is emerging as a promising market. In South America, value-conscious consumers and growing interest in fruit-based beverages are contributing to the market's gradual expansion.

Competitive Landscape

The squash drinks market is primarily led by major companies such as Carlsberg Group, Suntory Holdings, Dabur India Ltd, Unilever plc, and Nichols plc. These players dominate the market due to their strong brand presence and extensive distribution networks. However, the market also includes a variety of regional players and private-label manufacturers, which adds diversity and competition. Local brands are particularly important in regions where consumer preferences, pricing, and retailer relationships vary, as they can effectively cater to specific needs and preferences.

Competition in the squash drinks market is evolving, with companies focusing more on innovation and health-oriented products rather than just competing on price. Manufacturers are introducing options with functional ingredients, real-fruit content, and cleaner labels to meet the growing demand for healthier beverages. In mature markets, where private-label products are common, companies are also emphasizing premium offerings and engaging consumers more through targeted marketing. These strategies aim to keep their products relevant and appealing in a market that is becoming increasingly competitive.

Regional and local players are stepping up competition by offering affordable products, unique local flavors, and leveraging strong relationships with retailers. Private-label brands and contract manufacturers are also expanding their product ranges and improving their visibility on store shelves. In markets where flavor options are limited, companies are focusing on health claims, transparency, and targeted marketing to differentiate themselves. This ongoing competition between global brands and regional players continues to shape the growth and dynamics of the squash drinks market.

Squash Drinks Industry Leaders

-

Carlsberg Group (Britvic plc)

-

Suntory Holdings

-

Nichols plc

-

Dabur India Ltd

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Suntory Beverage and Food GB&I added a new Summer Fruits flavor to its Ribena range, available in both squash and ready-to-drink formats. This launch aimed to boost category growth and cater to changing consumer tastes.

- March 2026: Robinsons added a new Strawberry, Cherry, and Lime flavor to its Fruit Creations range. This move aims to strengthen its position in the adult squash segment by offering more premium, unique flavor options. The company plans to attract more consumers and expand usage occasions with this new flavor.

- April 2025: Capri-Sun expanded its beverage portfolio with the launch of a new Squash product range, including an enhanced formulation of its traditional Orange Squash and two innovative flavors: Monster Alarm and Jungle Drink.

- March 2025: Nichols introduced Vimto Wonderfuel, a functional squash variant of its Vimto brand, targeting the breakfast segment. The product contains high levels of vitamins B, C, and D, as well as iron and zinc supplements.

Global Squash Drinks Market Report Scope

Squash drinks are fruit-flavored concentrates that need to be mixed with water before drinking. They come in various flavors and types to suit different preferences. The global squash drinks market is classified into flavor type, sugar content, packaging type, distribution channel, and geography. Based on flavor type, the market is classified into orange, blackcurrant, mixed berry, mango, lemon/lime, and others. Based on sugar content, the market is classified into added-sugar and no-added-sugar. Based on packaging type, the market is classified into bottles, pouches, and other packaging types. Based on the distribution channel, the market is classified into on-trade and off-trade. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Orange |

| Blackcurrant |

| Mixed Berry |

| Mango |

| Lemon/Lime |

| Others |

| No-Added-Sugar |

| Added-Sugar |

| Bottles |

| Pouches |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Flavor Type | Orange | |

| Blackcurrant | ||

| Mixed Berry | ||

| Mango | ||

| Lemon/Lime | ||

| Others | ||

| By Sugar Content | No-Added-Sugar | |

| Added-Sugar | ||

| By Packaging Type | Bottles | |

| Pouches | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global squash drinks sector?

The squash drinks market was valued at USD 4.19 billion in 2025 and is estimated at USD 4.37 billion in 2026, with projected value reaching USD 5.41 billion by 2031.

What is driving growth in squash drinks through 2031?

The main growth drivers are at-home beverage preparation, rising demand for no-added-sugar products, and stronger innovation in functional and real-fruit formulations.

Which flavor segment is leading global demand?

Orange remained the leading flavor in 2025 with 43.26% share, while mixed berry is the fastest-growing flavor with a forecast 5.71% CAGR through 2031.

Which sales channel matters most for squash drinks?

Off-trade remains the core route to consumers, accounting for 68.82% of global revenue in 2025, supported by family shopping and bulk household purchases.

Page last updated on: