Romania Cybersecurity Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

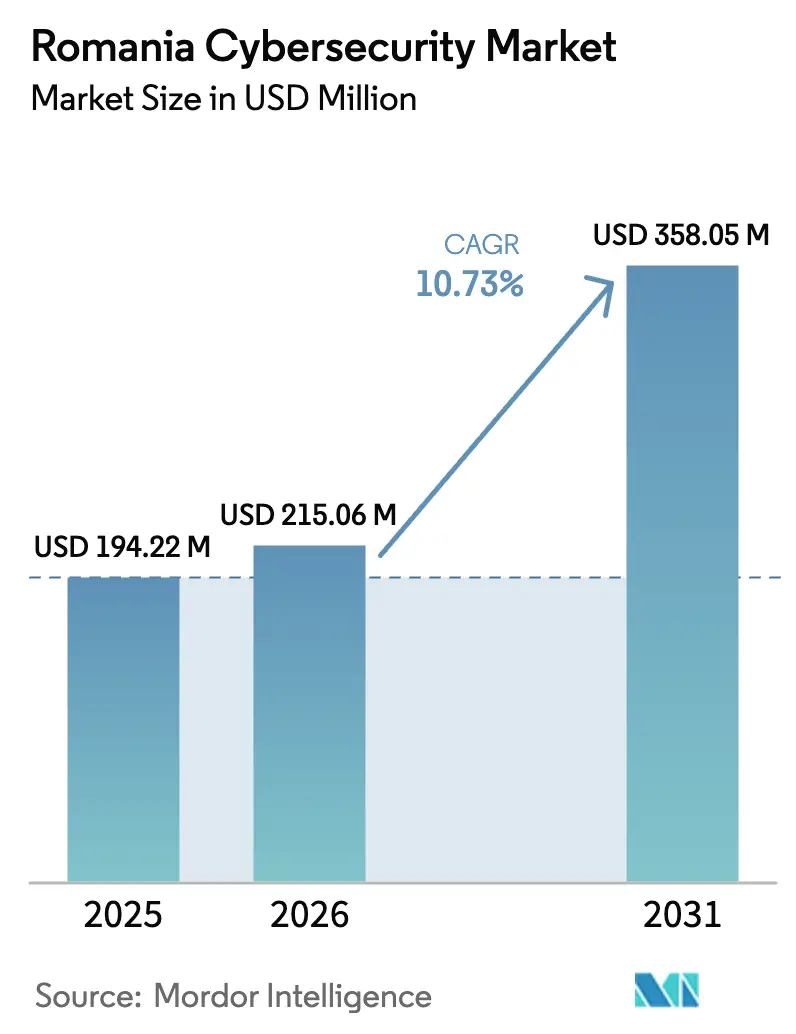

| Base Year Market Size (2025) | USD 194.22 Million |

| Market Size (2026) | USD 215.06 Million |

| Market Size (2031) | USD 358.05 Million |

| Growth Rate (2026 - 2031) | 10.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Cybersecurity Market Analysis by Mordor Intelligence

The Romania cybersecurity market size is expected to grow from USD 194.22 million in 2025 to USD 215.06 million in 2026 and is forecast to reach USD 358.05 million by 2031 at 10.73% CAGR over 2026-2031. Demand is moving decisively from tactical, compliance-led spending toward holistic resilience frameworks that combine cloud workload protection, managed detection and response, and identity governance. Accelerated cloud migration of public portals, the mandatory NIS2 regime, and a sharp rise in double-extortion ransomware are prompting boards to approve multiyear security budgets up front. Buyers now favour outcome-based contracts that guarantee reductions in mean-time-to-detect, signalling an emerging value-pricing model. Parallel near-shoring of Security Operations Center (SOC) services from Western Europe positions local providers as both domestic protectors and regional exporters of expertise, further lifting the Romania cybersecurity market.

Key Report Takeaways

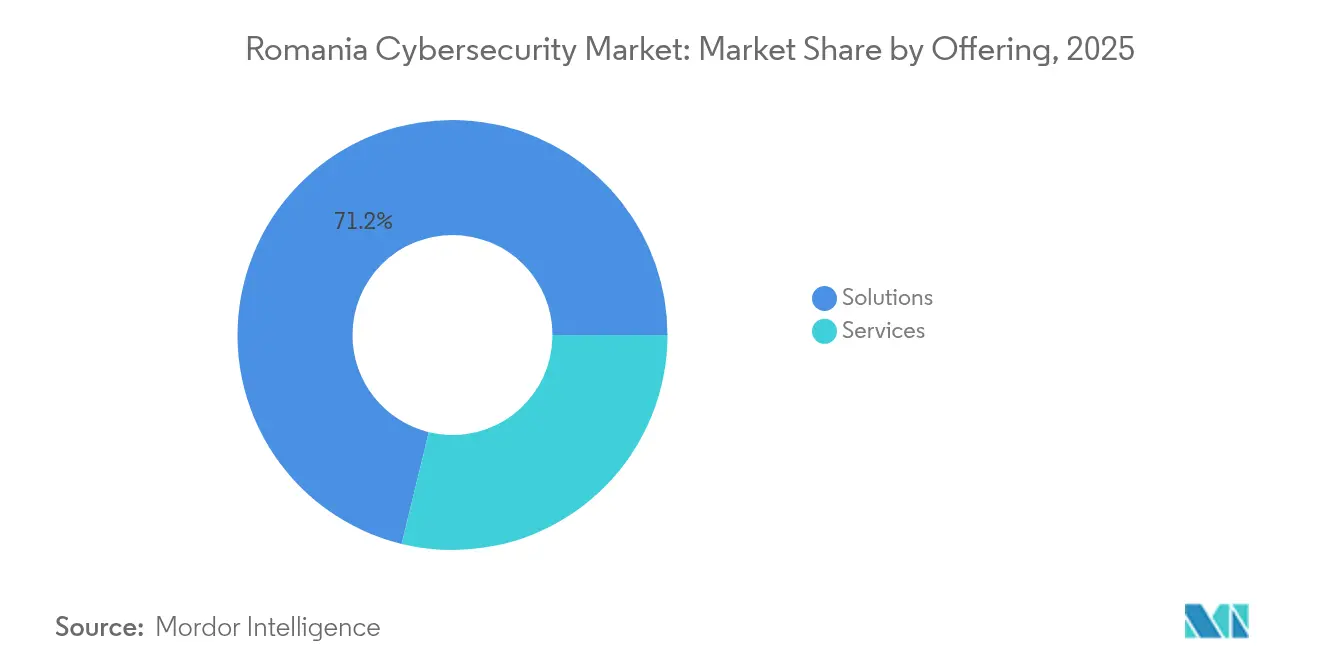

- By offering, solutions dominated with 71.20% of Romania cybersecurity market share in 2025, while services are projected to expand at a 15.32% CAGR to 2031.

- By deployment, cloud models accounted for 58.00% of Romania cybersecurity market size in 2025; hybrid cloud security is forecast to rise at a 14.41% CAGR through 2031.

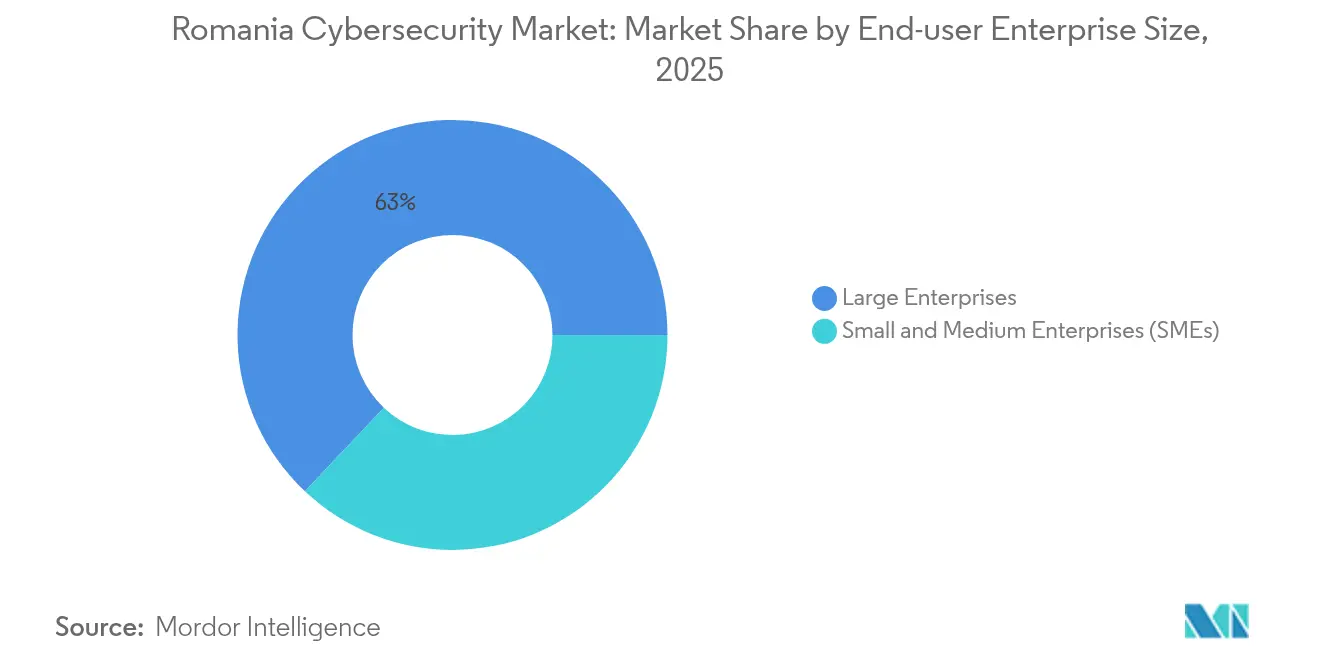

- By end-user enterprise size, large enterprises controlled 62.96% of Romania cybersecurity market share in 2025, whereas SMEs are set to post a 16.62% CAGR between 2026-2031.

- By end user, BFSI led with 22.18% revenue share in 2025; healthcare is on track for a 15.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digitalisation grants for SMEs (POCIDIF) | +2.1% | National; strongest in Cluj-Napoca, Timișoara, Iași | Medium term (2-4 yrs) |

| Ransomware surge on critical infrastructure | +1.8% | Nationwide; major urban hospitals and utilities | Short term (≤ 2 yrs) |

| EU-funded RoEduNet cloud overhaul | +1.2% | University hubs | Medium term (2-4 yrs) |

| Near-shoring of SOC services | +1.5% | Bucharest, Cluj-Napoca, Timișoara | Medium term (2-4 yrs) |

| Mandatory NIS2 transposition | +2.3% | National; critical-infrastructure entities | Short term (≤ 2 yrs) |

| Accelerated cloud adoption in public services | +1.4% | National; government agencies | Medium term (2-4 yrs) |

| Source: Mordor Intelligence | |||

Government-backed digitalisation grants for SMEs (POCIDIF)

Targeted public funding is rewriting SME risk appetites. The POCIDIF programme allocates EUR 160 million for RandD and an additional EUR 150 million for advanced digital tools, covering up to 70% of eligible cybersecurity costs.[1]Ministerul Investițiilor și Proiectelor Europene, “POCIDIF Program Details,” mfe.gov.ro Beneficiaries frequently bundle grants with bank credit, stretching subsidies across licence renewals and multi-year services. As award rounds occur each quarter, integrators enjoy a predictable pipeline, fuelling above-market growth for endpoint detection, MFA, and zero-trust access solutions across the Romania cybersecurity market.

Surge in ransomware targeting critical infrastructure

Incidents that crippled 100 hospitals in February 2024 and disrupted Electrica Group in December 2024 jolted executive boards into action.[2]Huawei Technologies, “Ultra-Broadband RoEduNet Upgrade,” huawei.com Procurement priorities shifted from theoretical breach prevention to provable containment and recovery, boosting demand for immutable backups, network segmentation, and incident-response retainers. Suppliers able to showcase sub-four-hour restoration times now command premium pricing, indicating ransomware continues to expand the Romania cybersecurity market size at the high-end solution tier.

EU-funded RoEduNet cloud overhaul driving network-security spend

The EU-financed overhaul of RoEduNet deploys 14.4 Tbit/s routers and elastic cloud nodes, earmarking roughly 20% of project value for security appliances.[3]BBC News, “Romanian Hospitals Hit by Ransomware Attack,” bbc.com Universities require deep packet inspection, SASE gateways, and automated compliance reporting, all of which are supplied by local integrators partnering with global OEMs. Because many campuses double as municipal e-service hubs, these elevated baselines cascade into surrounding smart-city projects, indirectly enlarging the Romania cybersecurity market share in the public sector.

Near-shoring of SOC services from Western Europe

Western European firms are relocating SOC workloads to Romanian MSSPs that operate at 30-40% lower cost yet meet EU data-residency rules.[4]Romania Insider, “Stefanini Names Romania Main Delivery Hub,” romania-insider.com Providers advertise bilingual analysts and ISO 27035-aligned playbooks, winning multiyear contracts whose exports already exceed half of total SOC revenue. This flow injects foreign exchange, accelerates skills transfer, and underpins a specialised services ecosystem that magnifies Romania cybersecurity market revenue beyond domestic demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent migration to Western EU | −1.7% | Nation-wide; acute in mid-size cities | Long term (≥ 5 yrs) |

| Low municipal cybersecurity budgets | −1.0% | Smaller towns | Medium term (2-4 yrs) |

| Fragmented legacy OT in utilities | −0.9% | Energy and industrial belts | Long term (≥ 5 yrs) |

| Limited cyber-insurance penetration | −0.4% | National | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Talent migration to Western EU creating skills gaps

Over 5.7 million Romanians now work abroad, draining senior cyber talent and stretching vacancies past six months. Salaries escalate, pushing firms toward automation and retention bonuses indexed to recruitment costs. While fast-track bootcamps fill entry-level posts, the scarcity of architects and threat hunters remains a brake on complex project roll-outs, shaving 1.7 percentage points from forecast CAGR across the Romania cybersecurity market.

Low cybersecurity budgets among municipal administrations

An audit of 103 municipalities exposed wide disparities in e-service quality and sparse security allocations. Although the DigiLocal programme sets aside 200 million lei for 2024-2025, first-come-first-served applications favour larger towns with professional grant writers. Smaller councils remain under-protected, holding sensitive citizen data yet lacking threat-monitoring capacity, a gap that depresses overall Romania cybersecurity market penetration in the local-government vertical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions remain dominant while services accelerate

Solutions held 71.20% of Romania cybersecurity market share in 2025 as enterprises built base-line controls. Services, however, will surge at a 15.32% CAGR through 2031, driven by SOC near-shoring and 24×7 monitoring mandates. Identity-and-access management and next-gen network firewalls top procurement lists owing to NIS2 inspection readiness. Vendors offering open APIs for rapid ecosystem integration are poised to capture incremental Romania cybersecurity market size from consolidating buyers.

Demand inside the services bundle is evolving from installation support to continuous threat hunting and incident response. MSSPs such as Stefanini and Zitec add DevSecOps, cloud posture management, and purple-team simulation, locking clients into multiyear retainers. As subscription jackets replace perpetual licences, annual recurring revenue could eclipse one-time sales before 2028, reshaping revenue recognition norms across the Romania cybersecurity industry.

By Deployment Mode: Cloud adoption reshapes architectures

Cloud security tools captured 58.00% of Romania cybersecurity market size in 2025 and will expand at a 14.41% CAGR through 2031 as e-government portals, digital banking, and e-health records migrate to hyperscale clouds. Compliance dashboards, workload-protection agents, and CASB layers now appear as mandatory tender requirements. Integrators note that attach rates for cloud-security add-ons can double total contract value once continuous controls monitoring is included.

On-premise and hybrid deployments persist in defence, energy, and select healthcare environments needing low-latency or sovereign data handling. Hybrid models split analytics in cloud SIEMs while retaining local packet capture, prompting demand for orchestration overlays that normalise policy. Appliance vendors embedding secure elements to meet air-gapped mandates continue to hold ground, ensuring diversified opportunity across the Romania cybersecurity market.

By End-user Enterprise Size: Large enterprises lead while SMEs surge

Large corporations generated 62.96% of Romania cybersecurity market share in 2025 thanks to multi-layer budgets and regulatory scrutiny. Banks routinely allocate 8-10% of IT spend to security and now mentor supply-chain partners, multiplying overall market demand. Pilot programmes for AI-driven threat analytics in telecom and utilities will propagate best practices downstream, reinforcing the enterprise segment’s benchmark role.

SMEs are forecast to grow at 16.62% CAGR through 2031 as POCIDIF subsidies and NIS2 thresholds broaden coverage. Fintech start-ups embed security testing in agile sprints, while manufacturers adopt pay-as-you-go penetration tests to win export contracts. Vendors with modular, consumption-based pricing stand to expand Romania cybersecurity market penetration among the long-tail of 500k+ registered SMEs.

By End User: BFSI leads while healthcare accelerates

BFSI retained 22.18% share in 2025, underpinned by Digital Operational Resilience Act readiness, customer-facing MFA, and venture investments in security start-ups. Banks now request real-time fraud-scoring engines, opening lane for behavioural biometrics and machine-learning-based anomaly detection.

Healthcare is projected to grow at 15.88% CAGR as February 2024 ransomware fallout drives segmentation, secure email gateways, and automated backup orchestration. Telemedicine platforms flag security architecture reviews as sprint deliverables, making resilience intrinsic to go-live decisions. Energy, telecom, and public administration complete the demand mix, each pushing sector-specific compliance overlays that widen Romania cybersecurity market opportunities.

Geography Analysis

Bucharest accounts for roughly 62.70% of national cybersecurity revenue, reflecting its density of headquarters, data centres, and government ministries. Superior fibre backbones, proximity to regulators, and an international airport that eases audits enhance vendor win rates. University-to-vendor pipelines generate professional interns each semester, replenishing human capital even amid outward migration and reinforcing the Budapest-style cluster in the Romania cybersecurity market.

Cluj-Napoca, Timișoara, and Iași are fast-rising nodes, buoyed by university partnerships and cost advantages of up to 20% against the capital. The 88 million RON Artificial Intelligence Research Institute under construction in Cluj-Napoca positions the city as an RandD nucleus for machine-learning-driven security. Multinationals locate L2 SOC teams here to exploit a multilingual talent base and round-the-clock support. This decentralisation enhances national resilience by diffusing capability beyond one metropolitan area.

Small municipalities struggle to fund even baseline controls, widening the urban-rural digital divide. DigiLocal grants promise 200 million lei, yet competitive submissions marginalise less-resourced towns. Pilot cross-county SOCs and public-private partnerships are emerging as pragmatic solutions, pooling budgets for shared incident response. Over time, regional collaboration could unlock overlooked Romania cybersecurity market share while raising the national security posture.

Competitive Landscape

Romania’s cybersecurity arena couples global incumbents with agile local innovators. Bitdefender, posting USD 459.7 million revenue, analyses 30 billion threat queries daily, anchoring domestic credibility while selling globally. International players such as Eviden (Atos), Orange Cyberdefense, and Fortinet blend EU compliance advisory with on-shore engineering, securing regulated sectors and elevating baseline expectations in the Romania cybersecurity market.

Local firms like Safetech Innovations deliver threat-intelligence-centred services, leveraging proprietary honeypot grids to detect regional attacker tactics. MSSPs including Stefanini and Zitec export 24×7 SOC monitoring, now contributing more than half of their revenue, demonstrating that Romania is not merely a consumer but a net security service exporter. Their ISO 27035-aligned processes and bilingual analysts attract Western European clients seeking cost-efficient resilience.

Strategic alliances drive differentiation. Telcos embed Bitdefender engines in customer routers, delivering mass-market protection baked into connectivity packages. Venture capital, exemplified by Early Game Ventures’ EUR 500k infusion into Zero Code and Pentest Copilot, fuels niche automation start-ups. Such partnerships accelerate time-to-market and diversify solution stacks, steering competition toward ecosystem orchestration rather than price wars in the Romania cybersecurity market.

Romania Cybersecurity Industry Leaders

Atos Group

Bitdefender SA

Cisco Systems Inc.

Check Point Software Technologies Ltd.

CoSoSys Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Edenred Digital Center exceeded 300 employees, adding platform-level security services to support 60 million global users.

- January 2025: Bitdefender acquired part of Bitshield Data Defense, integrating new IP into its endpoint stack.

- May 2024: Early Game Ventures funded penetration-testing automation start-ups, signalling investor appetite.

- December 2024: Electrica Group reported ransomware breach, accelerating OT segmentation plans.

Romania Cybersecurity Market Report Scope

The Romania cybersecurity market's scope encompasses the revenues derived from solutions and services utilized across end-user industries. The analysis draws from a blend of secondary research and primary sources, providing a comprehensive view of the market. The market also covers the major factors impacting its growth in terms of drivers and restraints.

The Romania cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the projected Romania cybersecurity market size by 2031?

The market is expected to reach USD 358.05 million by 2031, reflecting a 10.73% CAGR.

Which vertical will grow the fastest?

Healthcare is forecast to expand at 15.88% CAGR as ransomware incidents propel urgent security upgrades.

How does NIS2 influence spending?

NIS2 widens compliance to firms with 50-plus staff or EUR 10 million turnover, driving identity governance, logging, and managed detection purchases.

Why are MSSPs thriving in Romania?

Near-shoring from Western Europe, 30-40% cost savings, and EU data-sovereignty adherence make Romanian SOCs attractive.

Page last updated on: