Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

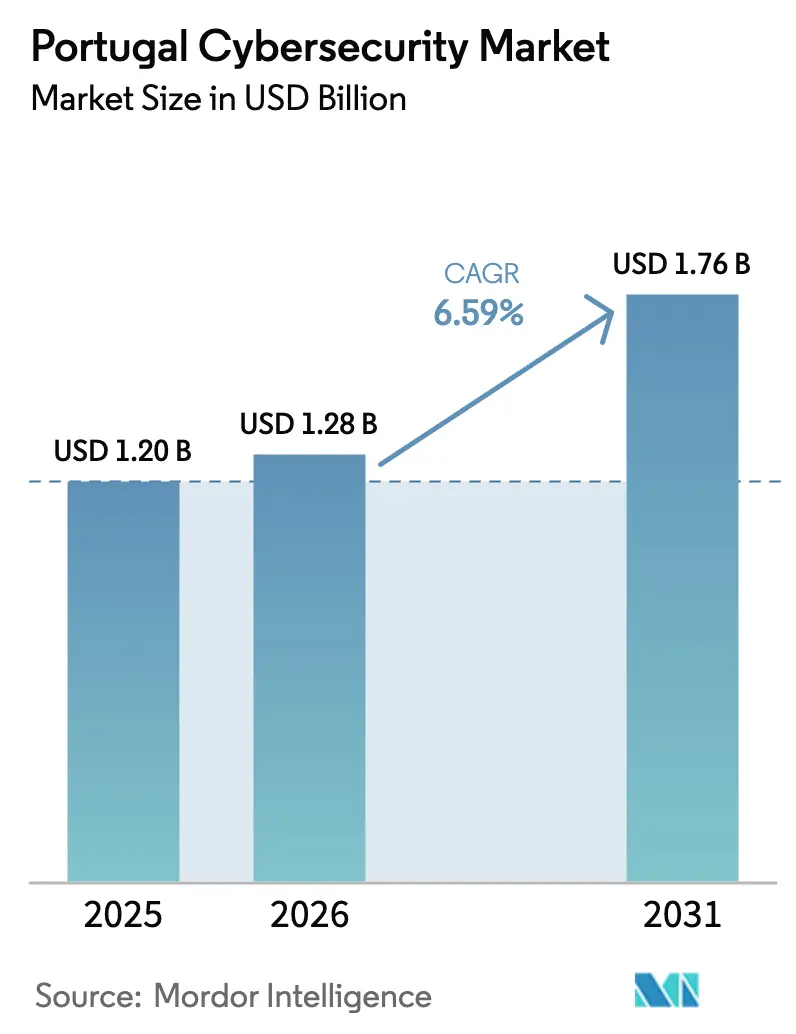

| Base Year Market Size (2025) | USD 1.20 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Cybersecurity Market Analysis by Mordor Intelligence

Portugal cybersecurity market size in 2026 is estimated at USD 1.28 billion, growing from 2025 value of USD 1.20 billion with 2031 projections showing USD 1.76 billion, growing at 6.59% CAGR over 2026-2031. Rising investment is anchored in the country’s role as a Southern-European data gateway and in strict implementation of the EU’s NIS2 Directive and the Digital Operational Resilience Act (DORA)[1]European Commission, “Directive (EU) 2022/2555 on Measures for High Common Level of Cybersecurity,” europa.eu. Continuous growth also stems from public-sector digital-transition funds, a heightened critical-infrastructure threat profile and aggressive cloud adoption. New hyperscale data-center campuses along the Sines-Lisboa-Porto corridor embed zero-trust baselines in supplier contracts, pushing enterprises toward identity-centric security controls. Large programmable grants aimed at small and mid-size companies require auditable cyber safeguards, creating fresh pockets of demand. Talent shortages and fragmented public procurement temper momentum yet they also redirect spending toward managed services and automation, thereby sustaining the upward trajectory of the Portugal cybersecurity market.

Key Report Takeaways

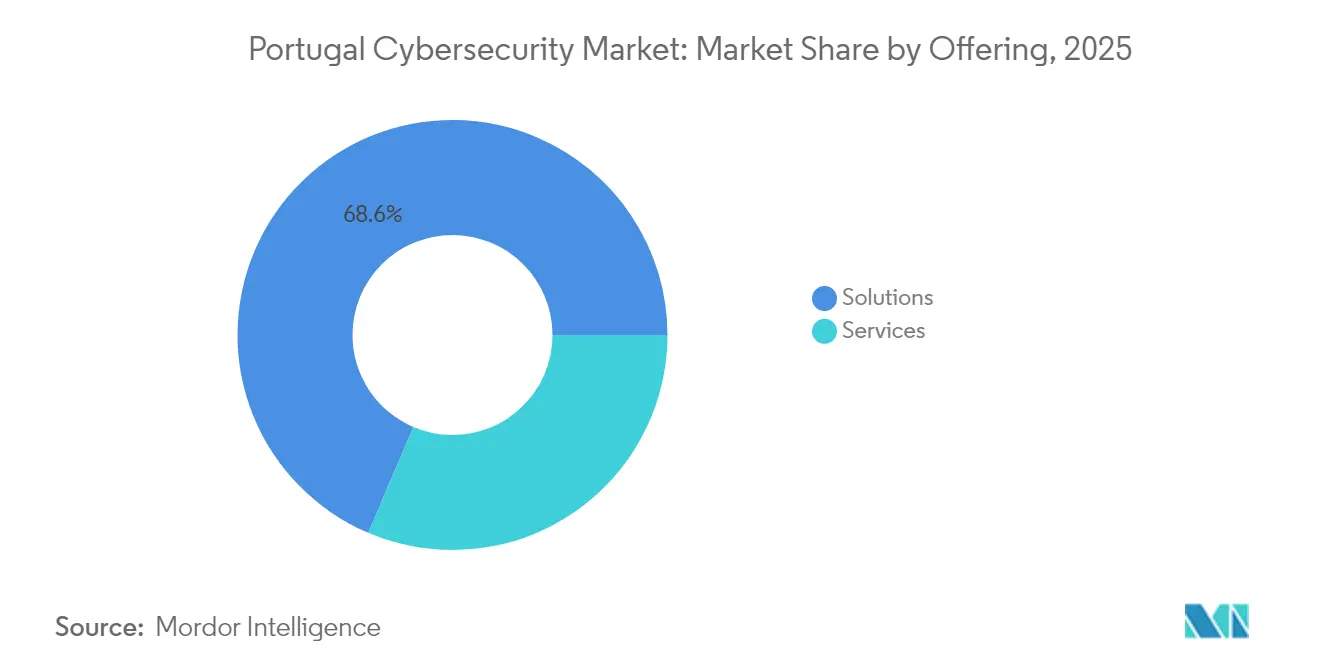

- By offering, solutions captured 68.60% Portugal cybersecurity market share in 2025; services are projected to grow fastest at an 8.05% CAGR through 2031.

- By deployment mode, on-premise represented 70.55% of the Portugal cybersecurity market size in 2025, while cloud deployments are forecast to climb at an 8.24% CAGR through 2031.

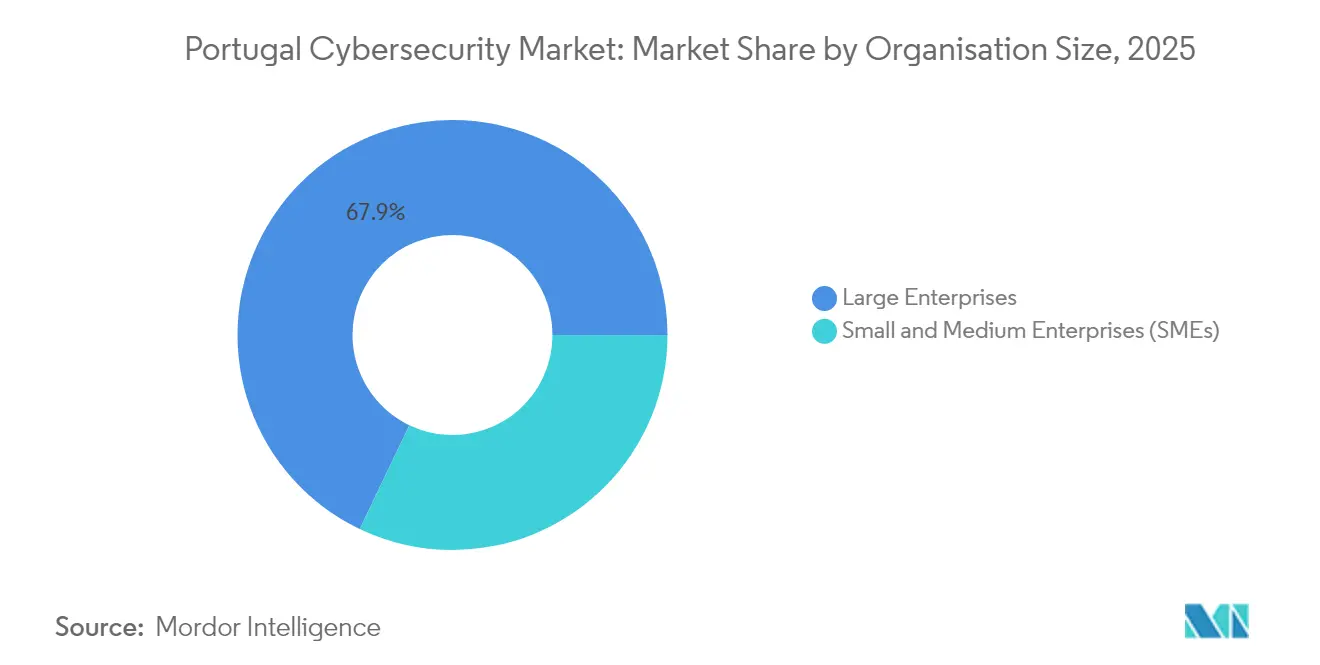

- By organisation size, large enterprises held 67.90% revenue in 2025; SMEs are expected to advance at a 7.63% CAGR by 2031.

- By end user, IT and telecom led with 22.50% revenue share in 2025; BFSI is projected to post the quickest growth at a 6.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Portugal Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU NIS2 compliance deadlines boosting spend | +1.8% | Global, with early gains in Norte, Centro, Lisboa | Medium term (2-4 years) |

| Remote-work and cloud adoption exposing attack-surface | +1.5% | National, concentrated in Lisboa and Porto tech hubs | Short term (≤ 2 years) |

| Spike in public-sector and banking cyber incidents | +1.2% | National, with spillover to critical infrastructure operators | Short term (≤ 2 years) |

| Hyperscale data-center build-outs requiring zero-trust architectures | +1.0% | Regional, concentrated in Sines, Lisboa, Porto corridors | Long term (≥ 4 years) |

| Portugal Tech II VC fund accelerating local cyber start-ups | +0.8% | National, with concentration in Lisboa, Porto, Coimbra | Medium term (2-4 years) |

| SME digitalization grants with mandatory cybersecurity outlays | +0.4% | National, with stronger uptake in Centro and Norte regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU NIS2 compliance deadlines boosting spend

Portugal is finalising the transposition of NIS2. Organisations now face compressed windows to map assets, perform risk assessments and report incidents. The National Cybersecurity Centre (CNCS) recommends integrated approaches instead of point solutions, raising demand for platform architectures that merge vulnerability management, threat intelligence and automated reporting.

Remote-work and cloud adoption expanding attack surface

More than 80 000 tech professionals work in Portugal; a remote-first culture widens perimeters far beyond corporate offices. Enterprises therefore move to zero-trust network access and strong identity controls, replacing VPN-centric approaches that struggled during pandemic shifts.

Spike in public-sector and banking cyber incidents

High-profile disruptions in the Iberian power grid and repeated phishing campaigns against national ministries raised awareness of cross-sector cyber dependencies. Banco de Portugal has issued circulars compelling financial institutions to formalise ICT-risk frameworks aligned with DORA, accelerating procurements of security-information-and-event-management (SIEM) upgrades and managed detection services.

Hyperscale data-center build-outs requiring zero-trust architectures

More than EUR 12 billion in confirmed data-center investment flows into Portugal, with projects such as the Start Campus complex specifying micro-segmented networks and post-quantum encryption for all suppliers. These requirements ripple through subcontractors and local managed-service providers, lifting total addressable demand in the Portugal cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cyber-talent shortage inflating salary costs | -1.2% | National, most severe in Lisboa and Porto tech hubs | Short term (≤ 2 years) |

| Legacy IT penetration and tight SME budgets | -0.8% | National, concentrated in traditional manufacturing regions | Medium term (2-4 years) |

| Fragmented public procurement restricting deal sizes | -0.6% | National, with spillover effects across all regions | Medium term (2-4 years) |

| In-house IT culture slowing MSSP uptake | -0.4% | National, strongest in large enterprises and government | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute cyber-talent shortage inflating salary costs

The ENISA “Cybersecurity Skills Shortage” report shows 65% of Portuguese entities struggling to fill defensive roles; salaries for senior architects now top EUR 100 000, more than double average IT wages[2]European Union Agency for Cybersecurity, “Cybersecurity Skills Shortage 2024,” enisa.europa.eu. Companies substitute with managed detection-and-response subscriptions and AI-driven monitoring, injecting momentum into the services segment of the Portugal cybersecurity market.

Legacy IT penetration and tight SME budgets

OECD surveys reveal 18% of Portuguese SMEs still deploy no dedicated security controls, while 44% rely only on basic antivirus software. Up-front hardware costs and limited in-house skills slow adoption, though EU-funded grant programmes increasingly condition payouts on verified cyber safeguards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services gain momentum as compliance complexity rises

Solutions accounted for 68.60% of Portugal cybersecurity market revenue in 2025. Integrated firewall, endpoint and identity platforms remain baseline purchases for regulated industries. Yet services outpace all other categories at an 8.05% CAGR as organisations seek external expertise to interpret NIS2, DORA and CNCS guidance. National service providers bundle incident-response retainers with 24 × 7 SOC staffing that many midsize firms cannot afford internally. Almost two-thirds of large buyers now require contracts to guarantee mean-time-to-detect below 15 minutes, a metric rarely achievable without specialised personnel.

By Deployment Mode: Cloud chips away at on-premise leadership

On-premise still held 70.55% Portugal cybersecurity market share in 2025, reflecting data-sovereignty sensitivities in energy and public administration. Cloud deployments, however, rise 8.24% annually, powered by EUR 2.46 billion in government digital-transition funds that showcase secure sovereign clouds for document management. Hybrid models now dominate new tenders: sensitive databases stay on dedicated hardware, while e-mail gateways and sandboxed analysis shift to SaaS.

By Organisation Size: SMEs accelerate under grant-linked mandates

Large enterprises commanded 67.90% of expenditure in 2025, driven by layered compliance obligations. Still, SMEs are on course for 7.63% CAGR because Portugal 2030 financing ties at least EUR 200 000 of every approved digital-transformation project to provable cybersecurity measures. Unified-threat-management appliances and subscription-based endpoint suites lower entry barriers, helping lift the Portugal cybersecurity market size attributable to small firms.

By End User: BFSI races ahead on regulatory urgency

IT and telecom providers led spending with 22.50% revenue in 2025. BFSI is projected to accelerate the fastest at 6.66% CAGR through 2031. DORA requires banks to catalogue critical ICT functions, test under severe-but-plausible scenarios and report major cyber incidents within strict timelines. Portuguese lenders therefore expand governance-risk-and-compliance suites and automated third-party monitoring, feeding fresh orders into the Portugal cybersecurity market.

Geography Analysis

The Norte region generated 36.72% of 2025 revenue. A dense manufacturing base around Porto and Braga prioritises industrial-control-system monitoring and secure remote maintenance to comply with IEC 62443 guidelines. Universities of Minho and Porto produce applied-research graduates who staff regional managed-service centres.

Centro is forecast to grow fastest at 7.05% CAGR. The Cybersecurity Competence Center – Central Region opened in Coimbra and runs joint research labs and certification facilities, lowering barriers for local SMEs to meet NIS2 benchmarks. Leiria hosts additive-manufacturing firms adopting secure digital-twins that rely on embedded encryption.

Lisboa and Tagus Valley remain the nation’s digital nucleus. Web Summit and three hyperscale cloud regions concentrate talent and venture funding, fuelling advanced use cases such as automated secure-software pipelines. Start Campus in Sines adds 495 MW of green-powered server capacity with a strict zero-trust blueprint, enforcing minimum-security requirements on every subcontractor and thus enlarging the Portugal cybersecurity market.

Algarve, Alentejo and the islands of Azores and Madeira adopt cybersecurity to protect smart-tourism platforms and micro-grid controllers that underpin renewable-energy self-sufficiency. These smaller territories leverage EU structural funds to co-finance vulnerability assessments and cyber-awareness training.

Competitive Landscape

The Portugal cybersecurity market is moderately fragmented. Global equipment suppliers—Cisco, Fortinet, Palo Alto Networks and Microsoft—deliver core platforms for firewalls, secure-access service edge and workload protection. National integrators such as Noesis and S21sec localise compliance playbooks, wrap managed detection services around leading platforms and translate EU legislation for Portuguese boards.

Innovation flourishes in niche segments. Ethiack commercialises continuous penetration testing with human-in-the-loop validation, serving over 50 domestic clients including the national airport operator. Probely, created in Porto and acquired by Snyk, exports automated web-vulnerability scanning built on machine-learning heuristics, demonstrating Portugal’s capacity to develop globally applicable security IP.

Foreign strategic buyers increase their presence to secure NIS2-related contracts. The scarcity of experienced SOC analysts raises acquisition multiples for mature service providers, while AI-rich start-ups attract venture capital for autonomous threat-detection engines. Together these dynamics enlarge the Portugal cybersecurity market while nudging it toward gradual consolidation.

Portugal Cybersecurity Industry Leaders

IBM Corporation

Dell Technologies Inc.

Fortinet Inc.

AVG Technologies

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NTT DATA deepened its alliance with CrowdStrike, launching 24 × 7 managed threat-hunting from Lisbon-based SOCs.

- March 2025: Ethiack secured EUR 4 million seed funding to enhance its AI-powered penetration-testing platform and expand across Europe.

- February 2025: The government launched a EUR 100 million deep-tech fund, half allocated to cybersecurity venture rounds.

- January 2025: DORA became effective across the EU, mandating ICT-risk management and incident reporting for Portuguese financial institutions, with enforcement by Banco de Portugal and the European Banking Authority.

Portugal Cybersecurity Market Report Scope

Cybersecurity solutions help a company to monitor, detect, report, and thwart cyber threats, which are internet-based attempts to compromise sensitive data via spyware, malware, and phishing and to disrupt or damage information systems.

The Portugal cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-premise |

| Cloud |

By Organization Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By End User

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Other End-Users |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End User | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Other End-Users | ||

Key Questions Answered in the Report

How big is the Portugal cybersecurity market today?

It stands at USD 1.28 billion in 2026 and is projected to reach USD 1.76 billion by 2031, reflecting a 6.59% CAGR.

Which segment is growing the fastest?

Professional and managed services rise at an 8.05% CAGR as firms outsource expertise to meet NIS2 and DORA obligations.

Why are SMEs increasing cybersecurity spending?

Portugal 2030 grants make cybersecurity investment a funding prerequisite, pushing smaller firms to adopt unified-threat-management and cloud-based protection suites.

What regulation most influences spending in Portuguese banks?

The Digital Operational Resilience Act obliges banks to test resilience and report incidents, driving significant upgrades in monitoring and incident-response tooling.

Which geographic area is forecast to grow fastest?

The Centro region leads with a projected 7.05% CAGR, supported by a new cybersecurity competence centre and fresh foreign investment.

How do hyperscale data-center projects affect the market?

They impose strict zero-trust and post-quantum standards on suppliers, expanding opportunities for identity-centric and cloud-workload security solutions across industries.

Page last updated on: