Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

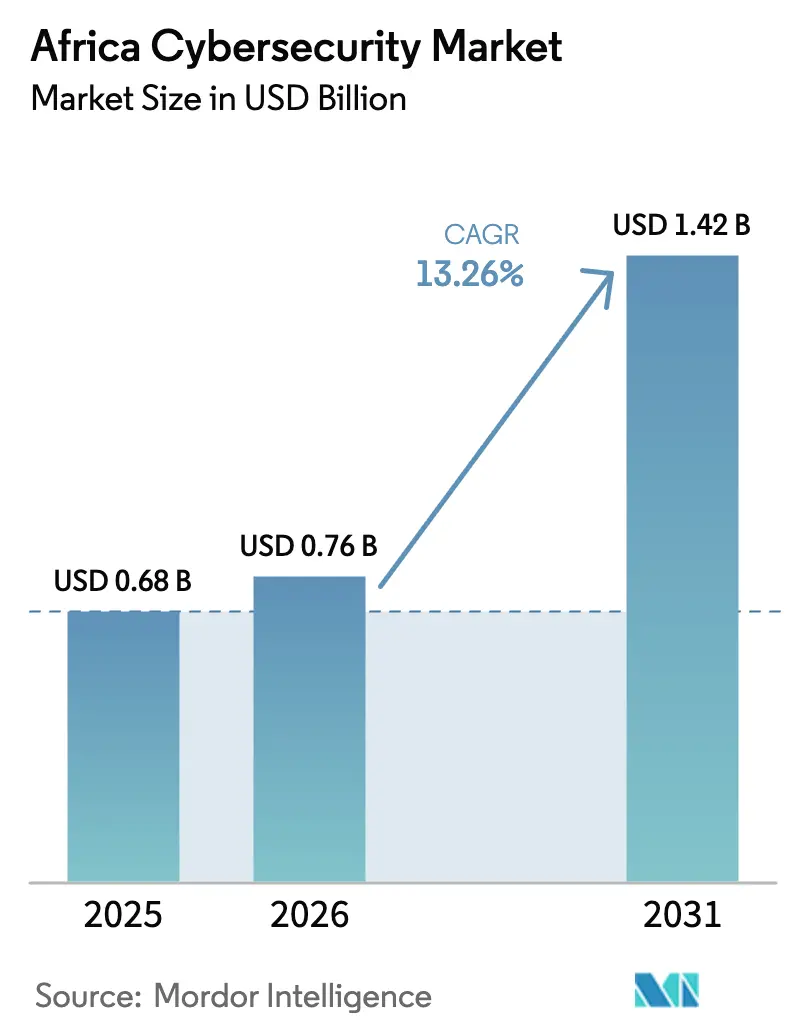

| Base Year Market Size (2025) | USD 0.68 Billion |

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 13.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Cybersecurity Market Analysis by Mordor Intelligence

The Africa cybersecurity market size is projected to expand from USD 0.68 billion in 2025 and USD 0.76 billion in 2026 to USD 1.42 billion by 2031, registering a CAGR of 13.26% between 2026 to 2031. Consistent digitalization of everyday commerce, the roll-out of hyperscaler data-center regions, and mandatory data-protection laws are the primary forces that keep capital flowing into the Africa cybersecurity market. Enterprises are modernizing their defenses to keep pace with 45 billion mobile-money transactions a year, while governments tighten procurement rules that now demand ISO-aligned audit trails. Vendor activity is intensifying as global players partner with regional systems integrators to navigate procurement complexity, and as local managed-security specialists use regulatory knowledge to win public-sector contracts. At the same time, inconsistent import duties and chronic power instability inflate operating costs, prompting buyers to favor elastic, cloud-delivered controls whenever connectivity allows.

Key Report Takeaways

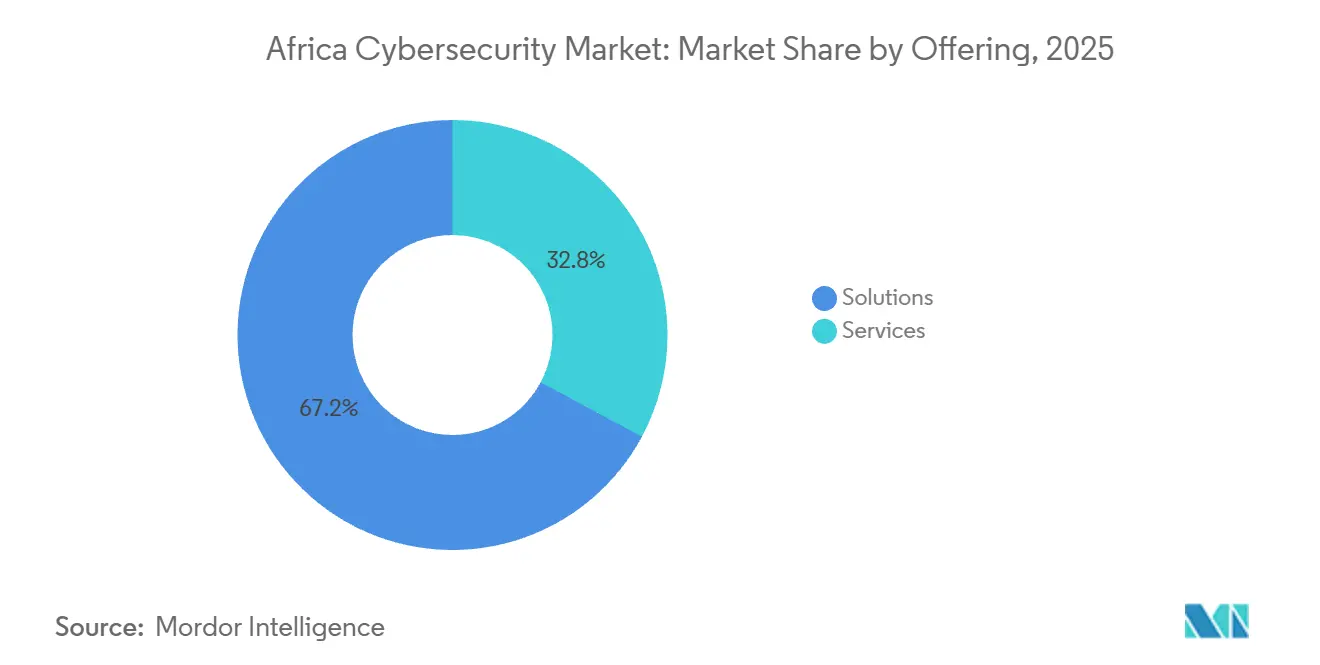

- By offering, solutions led with 67.16% of the Africa cybersecurity market share in 2025, while services are projected to advance at a 14.54% CAGR through 2031.

- By deployment mode, on-premises implementations accounted for 55.49% of the Africa cybersecurity market in 2025, yet cloud-based security is forecast to register the fastest 14.63% CAGR through 2031.

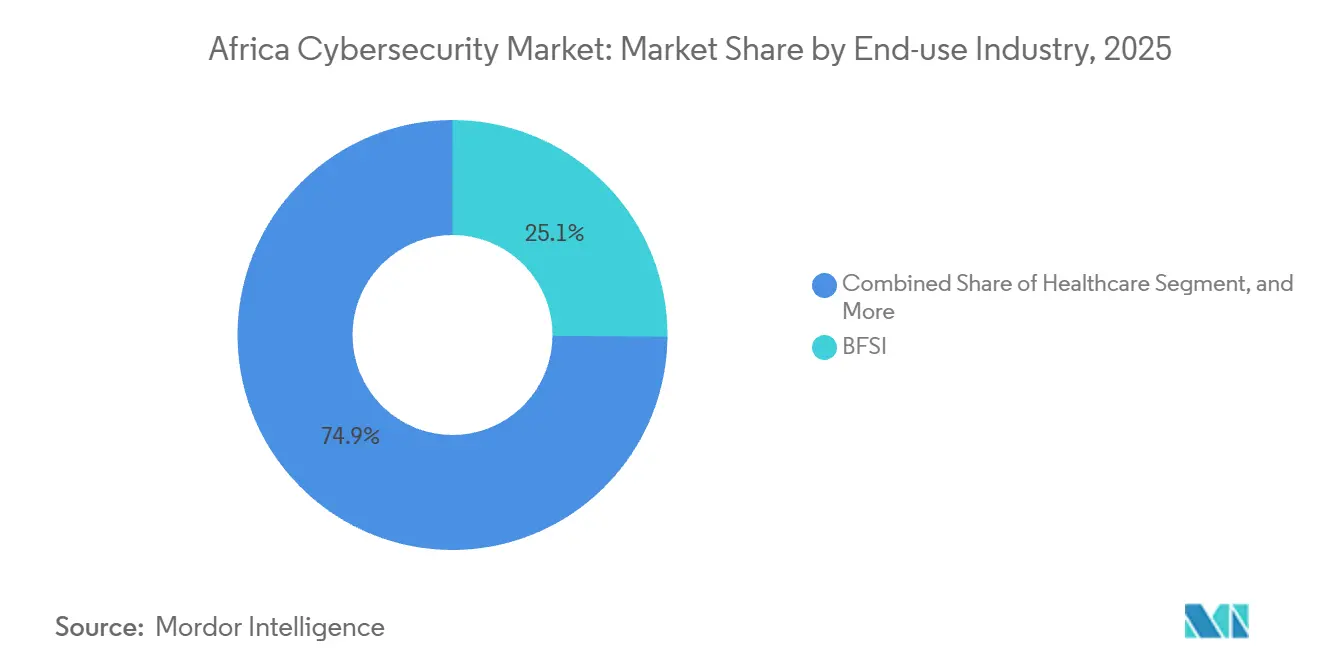

- By end-use industry, the BFSI segment accounted for 25.13% of the Africa cybersecurity market in 2025; healthcare is set to expand at a 15.13% CAGR through 2031.

- By enterprise size, large organizations commanded 70.69% of the market share in 2025, whereas SMEs are expected to post the highest CAGR of 14.87% through 2031.

- By country, South Africa accounted for 42.44% of the share in 2025, while Nigeria is projected to deliver the fastest 14.46% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Mobile-Money Platforms Across Sub-Saharan Africa | +2.5% | Sub-Saharan Africa, with concentration in Kenya, Nigeria, Ghana, Tanzania | Short term (≤ 2 years) |

| Expansion of National Data-Protection Regulations | +2.0% | South Africa, Nigeria, Egypt, Kenya; spillover to ECOWAS and SADC blocs | Medium term (2-4 years) |

| Hyperscaler Data-Center Roll-outs Driving Cloud-Native Security | +2.2% | South Africa, Kenya, Nigeria; indirect impact across Rest of Africa | Medium term (2-4 years) |

| OT Cybersecurity Demand in Gulf-of-Guinea Oil and Gas | +1.8% | Nigeria, Angola, Equatorial Guinea, Ghana offshore fields | Long term (≥ 4 years) |

| AfCFTA PAPSS Roll-out Creating Cross-Border Security Requirements | +1.5% | Pan-African, with early traction in West Africa and SADC corridors | Long term (≥ 4 years) |

| Generative-AI Enabled Financial-Services Fraud Accelerating Defense Spend | +2.3% | Global, with acute impact in Nigeria, Kenya, South Africa fintech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Mobile-Money Platforms Across Sub-Saharan Africa

Mobile-money traffic exceeded 45 billion transactions in 2025, and Kenya’s M-Pesa alone handled more than 25 million daily events, expanding the attack surface beyond traditional perimeter defenses.[1]Vodafone Group Plc, “Annual Report 2025,” vodafone.com Operators now invest in behavioral biometrics and real-time anomaly detection; MTN raised fraud-prevention budgets by 32% year-on-year across 19 markets in 2025. Cash-in and cash-out agents in rural areas share devices that often lack timely patches, making endpoint hygiene a pressing issue. Regulatory moves amplify urgency, with Nigeria’s central bank enforcing multi-factor authentication on wallet transactions above NGN 10,000 (USD 6.50) from January 2025.[2]Central Bank of Nigeria, “Guidelines on Mobile-Money Multi-Factor Authentication,” cbn.gov.ng Interoperability hubs such as Ghana’s instant-payment switch link multiple banks and mobile-money operators, pushing encryption and tokenization into settlement layers to block man-in-the-middle attacks.

Expansion of National Data-Protection Regulations

Enforcement of South Africa’s POPIA intensified after a ZAR 10 million (USD 0.55 million) fine levied in 2024, motivating enterprises to install data-loss-prevention and audit-trail tools. Nigeria’s Data Protection Act carries fines up to 2% of turnover and mirrors GDPR’s extraterritorial scope, compelling multinationals to standardize residency controls across the Africa cybersecurity market.[3]Nigeria Data Protection Commission, “Act Implementation Guidelines,” ndpc.gov.ng Egypt’s 2024 privacy law demands local storage of citizen records and explicit consent for biometric use, accelerating on-premise encryption sales. Kenya shortened breach-notification windows to 72 hours, spurring automated incident-response deployments. Across the continent, ISO 27001 certification has become a prerequisite for public contracts, with 92% of executives citing regulation as the chief budget driver in PwC’s 2025 East Africa survey.

Hyperscaler Data-Center Roll-Outs Driving Cloud-Native Security

Microsoft committed USD 1 billion to Azure regions in Kenya, Google expanded Johannesburg facilities, and AWS reported a 58% jump in security-service consumption in 2025, collectively redirecting design priorities toward cloud-native controls. Identity federation, secrets management, and continuous posture-management solutions are now baseline needs because the shared-responsibility model places application security squarely on the client. Deloitte found that 67% of African cloud users suffered at least one misconfiguration-related exposure during the prior year. Reduced latency from in-region compute lets banks score fraud in microseconds while sparing them international circuit costs, further boosting demand for cloud-delivered defenses.

OT Cybersecurity Demand in Gulf-of-Guinea Oil and Gas

Offshore production platforms in Nigeria, Angola, and Equatorial Guinea rely on programmable logic controllers that were never designed for hostile networks, yet they now connect to corporate IT estates for predictive maintenance. Ransomware attacks that lock supervisory control and data acquisition consoles can halt output worth millions of barrels, prompting operators to procure intrusion-detection sensors hardened for salt-spray environments. Regulatory attention is growing after a 2025 reconnaissance incident on a Nigerian substation triggered parliamentary hearings on energy security. Vendors with deep industrial-control expertise still scarce in the Africa cybersecurity market stand to capture contracts as upstream firms refresh defenses over multiyear cycles. Growing LNG export projects add urgency, because shipping insurers increasingly require proof of OT security before underwriting cargoes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Shortage of Certified Cybersecurity Talent | -2.8% | Pan-African, with acute gaps in Francophone West Africa and East Africa | Long term (≥ 4 years) |

| Fragmented Government Procurement and Long Sales Cycles | -1.9% | Nigeria, Kenya, Egypt; public-sector tenders across ECOWAS and SADC | Medium term (2-4 years) |

| Telecom Last-Mile Power Instability Hindering 24/7 SOC Operations | -1.2% | Nigeria, Ghana, Tanzania, Mozambique; rural and peri-urban areas | Short term (≤ 2 years) |

| Inconsistent Import Duties on Security Appliances Inflating CapEx | -1.0% | ECOWAS, SADC, EAC customs unions; fragmented tariff schedules | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Shortage of Certified Cybersecurity Talent

Only 20,000-30,000 certified practitioners serve more than 1.4 billion citizens, a ratio one-tenth of North America’s benchmark. Out-migration deepens the gap, with 40% of Kenyan graduates moving abroad within three years for salaries up to six times higher. Vendor academies from Cisco, Fortinet, and Huawei help, yet certification pass rates remain below 35% because hands-on labs and localized courseware are scarce. The shortage inflates managed-service pricing by 20%-30% over Asia-Pacific rates and extends median dwell time for advanced threats past 90 days versus a 21-day global norm. Without a concerted push to scale university programs, the talent deficit will continue to temper the growth potential of the Africa cybersecurity market.

Fragmented Government Procurement and Long Sales Cycles

Public-sector tenders take 18-36 months from request to signature, discouraging smaller integrators from dedicating bid teams. Nigeria’s IT agency, national security adviser, and line ministries each maintain separate technical specifications, forcing vendors through multiple approval paths. Mid-year budget cuts, such as Kenya’s 22% reduction to its national cyber center in fiscal 2025-2026, freeze procurement midway and erode vendor confidence. Corruption concerns rank 38 of 54 African states below the global median, triggering lengthy compliance checks by multinational bidders. Extended credit terms of up to 180 days strain the cash flow of regional partners, limiting participation and delaying the roll-out of urgently needed defenses across critical infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Rise As Scarce Skills Drive Outsourcing

Solutions secured 67.16% of Africa cybersecurity market share in 2025, underlining the preference for owning firewalls, endpoint licenses, and encryption tools. Services, however, are forecast to outpace with a 14.54% growth curve because the shortage of in-house talent forces enterprises to hire external specialists. Managed security operations centers delivering 24/7 monitoring, threat hunting, and incident response are the star performers, with global integrators such as Dimension Data and Liquid Intelligent Technologies winning multi-year contracts. Professional services covering penetration testing and compliance audits enjoy steady demand as data-protection authorities levy heftier penalties. Integrated risk-management platforms that pool vulnerability scanning, patch orchestration, and regulatory reporting into a single dashboard are gaining favor among banks juggling ISO 27001, PCI-DSS, and sector rules, pushing the Africa cybersecurity market toward unified architectures.

Spending patterns also reveal momentum in application-security tooling as fintech start-ups institutionalize DevSecOps pipelines. A 2025 survey recorded a 24-point leap to 52% in fintechs embedding code scans in continuous integration flows. Network and endpoint security together still claim more than half of solutions revenue, reflecting persistent bring-your-own-device and hybrid-work models. Data-security suites remain vital for sectors handling sensitive information, especially as telemedicine platforms encrypt consultations to satisfy cross-border privacy mandates. The pivot from capex to opex continues as cloud-based subscription bundles simplify budgeting, cementing services as a structural growth engine for the Africa cybersecurity market.

By Deployment Mode: Cloud Adoption Accelerates Despite Connectivity Gaps

On-premise implementations held 55.49% of the Africa cybersecurity market size in 2025 because data-residency mandates and legacy investments remain significant. Yet cloud security is projected to climb at a 14.63% CAGR thanks to local Azure, AWS, and Google zones that cut latency by up to 60% for security telemetry. Banks now run fraud-scoring algorithms in-region to avoid costly international backhaul, while retailers offload email security and web filtering to SaaS platforms that automatically update signatures. Hybrid arrangements dominate transitional years, with organizations maintaining on-premise appliances for core banking while migrating commodity workloads to the cloud.

Connectivity constraints still curb enthusiasm in secondary cities, where fiber penetration lags 15% and 4G coverage remains uneven. Telcos are closing the gap; MTN rolled out 5G in Johannesburg and Cape Town in 2024, and Safaricom activated Nairobi in 2025, enabling branch offices to stream logs to cloud SIEMs without saturating links. Regulatory considerations persist; Egypt’s privacy law and Nigeria’s act favor domestic storage but allow cloud use if encryption keys stay under enterprise control. Vendors entice customers with subscription prices up to 40% lower than the three-year total cost of ownership for on-premise hardware, ensuring that cloud will keep capturing share within the Africa cybersecurity market.

By End-Use Industry: Healthcare Leads Growth Under Telemedicine Encryption Rules

BFSI supplied 25.13% of Africa cybersecurity market size in 2025 as banks fortified against credential stuffing and SIM-swap fraud. Healthcare, however, is on track to deliver the highest 15.13% CAGR through 2031 after the World Health Organization urged cross-border encryption of patient data in 2024. Telemedicine platforms that proliferated during the pandemic now retrofit zero-trust access controls and endpoint-detection agents on medical devices. Ransomware incidents in hospitals during 2025 intensified board-level focus, driving procurement of immutable backups and privilege-access management. Telecom operators meanwhile face dual obligations: securing their own networks and reselling managed-security services to enterprise customers, expanding opportunity sets for multi-tenant SOC platforms.

Industrial manufacturing invests heavily in OT defenses to protect programmable controllers in automotive and cement plants. Deloitte listed OT/IT convergence among the top three risks for Nigerian factories in 2025. Retail chains such as Shoprite and Woolworths allocated more than ZAR 100 million (USD 5.5 million) in 2025 to encrypt point-of-sale terminals, illustrating compliance-driven momentum. Energy utilities add to demand because grid operators are hardening substations after reconnaissance attempts revealed systemic gaps. Collectively, these dynamics ensure broad-based expansion, with every vertical contributing to the Africa cybersecurity market.

By End-User Enterprise Size: SMEs Close The Protection Gap With SaaS Bundles

Large enterprises generated 70.69% of the market share in 2025, reflecting their complex estates and regulatory burdens. Yet SMEs will post a 14.87% CAGR up to 2031 as cloud bundles commoditize advanced defenses. An International Finance Corporation survey found that 34% of digitally active small businesses experienced a cyber incident in 2025, resulting in a median 8% loss of annual revenue. Solutions such as Microsoft 365 Business Premium, priced at USD 22 per user, combine email, endpoint, and identity protection, lowering adoption hurdles. Cisco’s pay-as-you-go Umbrella firewall follows seasonal cash flows, resonating with traders whose sales peak during harvest or holiday periods.

Government digital identity drives compliance; Kenya’s Huduma Namba and Nigeria’s NIMC enrollment push millions of traders into formal tax systems that now mandate basic security. SMEs prioritize quick wins such as multifactor authentication, automated patching, and phishing simulations over expensive SIEM deployments. Vendors that embed lightweight security inside accounting, point-of-sale, or inventory software at sub-USD 50 monthly price points stand to unlock latent demand, widening the customer base of the Africa cybersecurity market.

Geography Analysis

South Africa captured 42.44% of market share in 2025, thanks to POPIA enforcement, Johannesburg’s financial concentration, and early hyperscaler regions. Enterprises already run next-generation firewalls and SIEMs and are now piloting zero-trust architectures, yet rolling blackouts continue to divert budget to generator redundancy. Nigeria, by contrast, is forecast to expand at 14.46% CAGR as the 2024 Data Protection Act yields tangible fines, and Lagos fintechs process USD 150 billion in yearly payments that invite sophisticated fraud. Egypt’s USD 150 million cybersecurity strategy fuels public-sector tenders that bundle CERT-EG services with mandatory ISO 27001 certification.

Nigeria serves as the western pole of growth, with Lagos fintechs and state-backed digital-identity schemes setting aggressive security standards. The Data Protection Commission issued its first major fine in 2025, confirming regulatory teeth, and banks responded by tripling budgets for identity-and-access management alongside behavior analytics engines. Oil and gas majors headquartered in Abuja are modernizing OT defenses, raising demand for deep-packet inspection tools certified for industrial protocols.

East Africa’s momentum revolves around Kenya, where Microsoft’s USD 1 billion data-center build and Safaricom’s 5G network reduce latency, opening doors for SIEM-as-a-service even in peri-urban branches. Rwanda and Tanzania follow, leveraging regional fiber backbones to connect SMEs to cloud-delivered controls. North-African markets led by Egypt and Morocco emphasize sovereign-cloud and on-premise encryption appliances, reflecting strict residency clauses in newly minted privacy statutes. Collectively, these dynamics ensure that every sub-region contributes materially to the expansion of the Africa cybersecurity market.

Competitive Landscape

The Africa cybersecurity market is moderately fragmented, with players such as Cisco, Fortinet, Palo Alto Networks, Check Point, IBM, and others, leaving ample headroom for regional specialists and SaaS disruptors. Channel partnerships dominate go-to-market models, with over 120 African resellers carrying Cisco’s portfolio and 3,500 engineers newly certified in 2025. BCX and Silensec leverage local language skills and regulatory expertise to win government tenders that multinationals find arduous. White-space niches include OT security for Gulf-of-Guinea platforms and generative-AI fraud detection calibrated to mobile-money flows, areas where incumbent Western products trained on card-payment data misfire with high false positives.

Darktrace and CrowdStrike gain mindshare with autonomous response and cloud-native deployment that shrink the skills burden, though premium pricing caps penetration below tier-one enterprises. Huawei sustains strength in Francophone West Africa and Egypt via bundled network and security deals despite geopolitical wariness in Anglophone hubs. Vendors embed artificial-intelligence featuresautomated playbooks, predictive patching, and natural-language SOC interfaces to offset the talent shortage that constrains the Africa cybersecurity market. ISO 27001 certification plus alignment with the African Union cyber convention are now table stakes for any bidder chasing sovereign or critical-infrastructure contracts.

Liquid Intelligent Technologies and Dimension Data continue to enlarge their SOC footprints, trimming latency below 100 ms for customers in land-locked markets such as Zambia and Uganda. Mergers remain modest, yet Fortinet’s December 2025 integration with BCX to deliver secure-access-service-edge bundles signals a broader pivot toward converged networking and security stacks. Global suppliers increasingly localize product interfaces into Swahili, Hausa, and French to accelerate adoption among frontline analysts, a differentiator in competitive bids. Certification hurdles are rising, because Egypt and Kenya now demand ISO 27001 compliance and proof of local data residency before awarding public contracts, tilting advantage toward vendors that host cloud points of presence inside the continent. Pricing pressure persists as inconsistent import tariffs add up to 15% on hardware, prompting buyers to negotiate subscription discounts that smooth cash flow. Collectively these shifts keep rivalry intense and innovation continuous, yet fragmentation endures because no single provider controls more than 12% of the Africa cybersecurity market.

Africa Cybersecurity Industry Leaders

Dell Technologies Inc.

Fortinet, Inc.

Cisco Systems Inc.

IBM Corporation

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft began construction of its USD 1 billion Azure region in Kenya, pairing the build with programs to train 10,000 local security professionals over three years.

- January 2026: Liquid Intelligent Technologies secured a USD 180 million International Finance Corporation credit line aimed at scaling SOC-as-a-service across 13 countries.

- December 2025: Fortinet and BCX launched an integrated secure-access-service-edge bundle targeting 500 South African enterprises by end-2026.

- November 2025: Egypt’s telecom regulator awarded a USD 45 million monitoring-platform contract to a Cisco–Huawei consortium to integrate threat intelligence with CERT-EG.

Africa Cybersecurity Market Report Scope

Cybersecurity solutions help organizations monitor, report, and counter cyber threats to maintain data confidentiality. The adoption of cybersecurity solutions is expected to grow in line with the rising internet penetration among developing and developed countries. The need for cybersecurity has increased as every system in today's world is connected to the internet, making data more accessible to cybercriminals.

The Africa Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace Military and Defense, and Other End-use Industries), End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Country (South Africa, Egypt, Nigeria, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| Endpoint Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By Country

| South Africa |

| Egypt |

| Nigeria |

| Rest of Africa |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| Endpoint Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Country | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will Africa’s cybersecurity spending be by 2031?

The Africa cybersecurity market size is projected to reach USD 1.42 billion in 2031, expanding at 13.26% CAGR from 2026.

Which segment grows fastest across the region?

Cloud-based security shows the highest momentum, with a forecast 14.63% CAGR as enterprises migrate workloads to new regional data centers.

Why is healthcare security accelerating in Africa?

World Health Organization guidance that mandates encryption for cross-border patient data exchanges drives hospitals and telemedicine providers to boost cybersecurity budgets.

What restrains wider security adoption?

A severe shortage of certified professionals and elongated government procurement cycles slow implementation across critical infrastructure.

Which countries are setting the regulatory pace?

Nigeria, South Africa, Egypt, and Kenya lead with data-protection acts that impose hefty fines and enforce tight breach-notification windows.

Are SMEs finally investing in protection?

Yes, pay-as-you-go bundles from cloud providers and telcos enable small businesses to deploy multifactor authentication, endpoint security, and basic monitoring at affordable rates.

Page last updated on: