Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.61 Billion |

| Market Size (2026) | USD 1.7 Billion |

| Market Size (2031) | USD 2.26 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

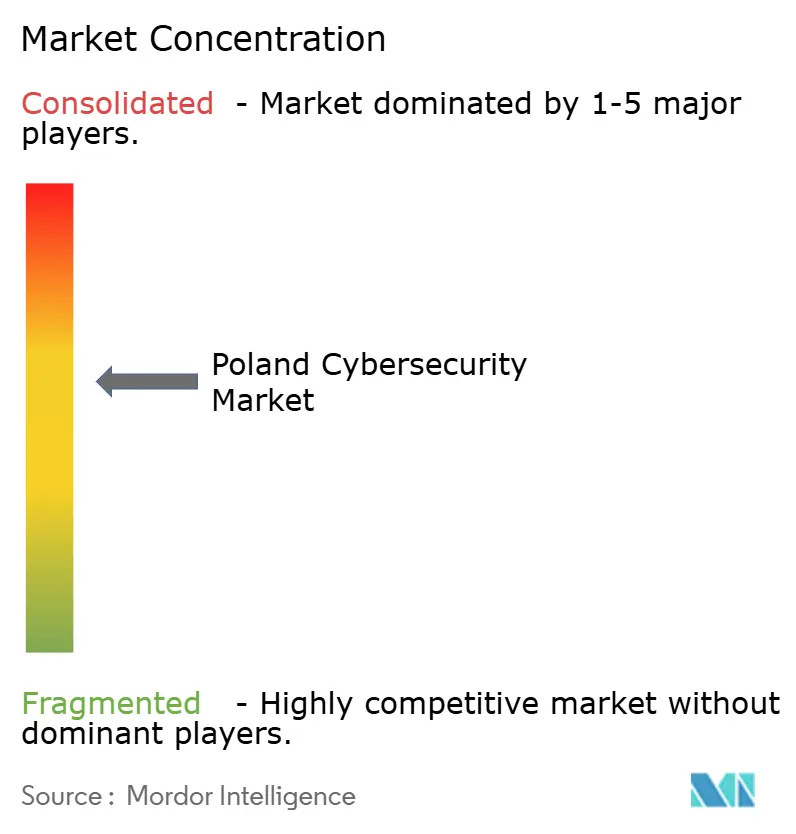

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Cybersecurity Market Analysis by Mordor Intelligence

The Poland cybersecurity market size is expected to grow from USD 1.61 billion in 2025 to USD 1.7 billion in 2026 and is forecast to reach USD 2.26 billion by 2031 at 5.80% CAGR over 2026-2031. Board-level acceptance of security as a core operational requirement, rather than a discretionary technology upgrade, is now common. Procurement teams routinely bundle threat-protection licences with every new cloud, 5G or artificial-intelligence rollout, creating a pace of repeat orders that points to deeply rooted structural demand. Geopolitical tension has sharpened this momentum by pulling forward public-sector spending on threat-intelligence platforms and secure government clouds. Local suppliers benefit because proximity to end users shortens incident-response times, while international vendors invest in Polish-language support and domestic data handling to satisfy compliance rules. Combined, these shifts suggest the Poland cybersecurity market is entering a phase in which subscription and managed-service contracts dominate cash flows, driving predictable, recurring revenue streams across the value chain.

Key Report Takeaways

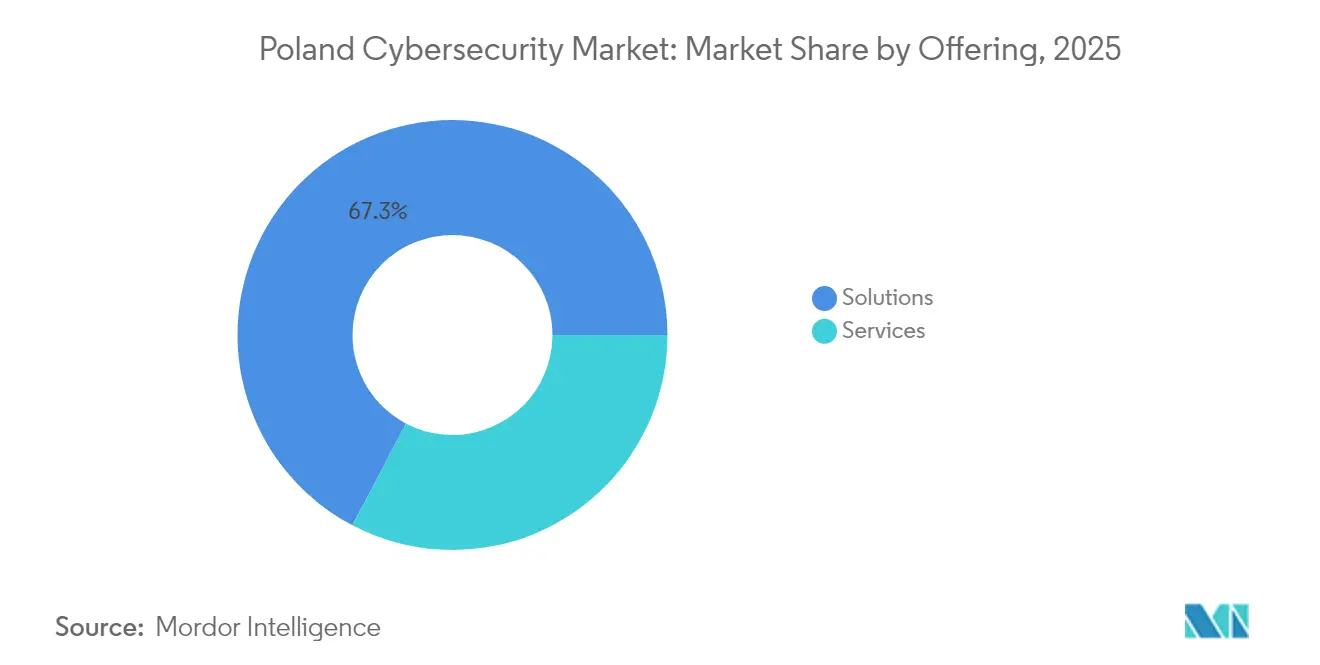

- By offering, solutions led with 67.30% Poland cybersecurity market share in 2025, while services are forecast to expand at a 15.05% CAGR through 2031.

- By deployment mode, on-premises retained 53.90% of Poland cybersecurity market size in 2025; cloud is projected to grow at an 18.15% CAGR between 2026 and 2031.

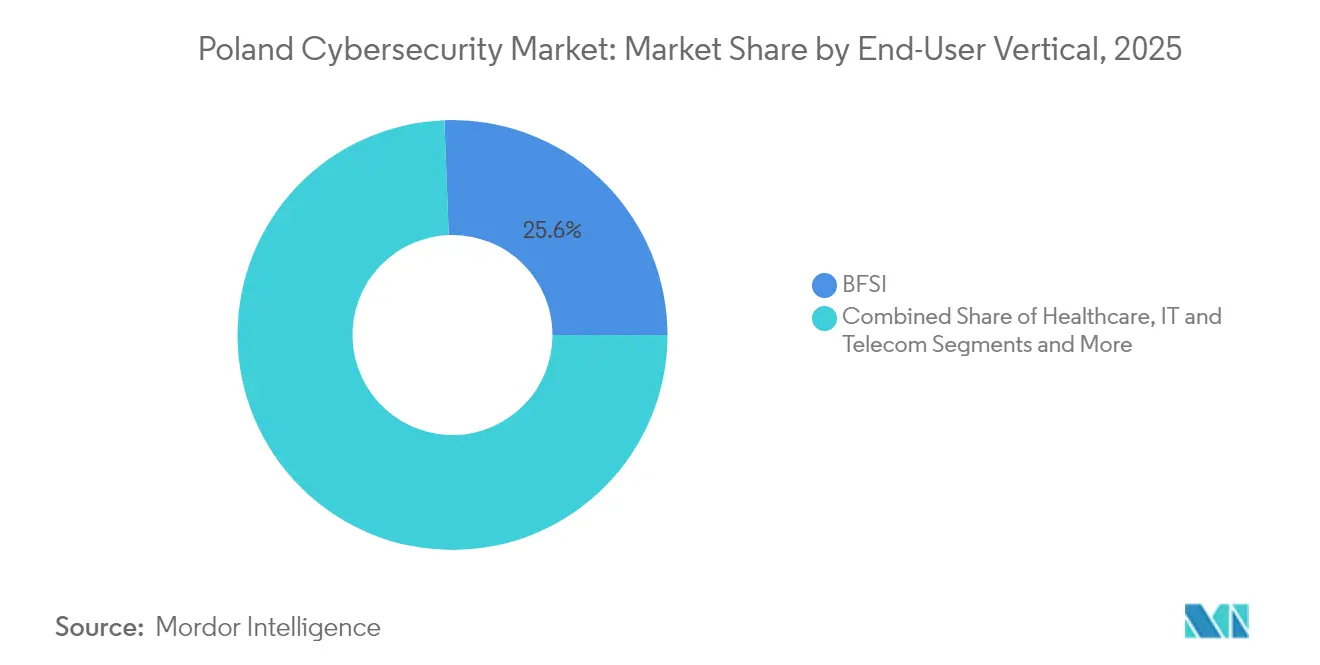

- By end-user vertical, BFSI commanded 25.60% of the Poland cybersecurity market share in 2025, whereas healthcare is advancing at a 18.55% CAGR through 2031.

- By end-user enterprise size, large enterprises held 70.80% share of the Poland cybersecurity market size in 2025, yet SMEs record the highest forecast CAGR at 16.75% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-cloud migration among mid-caps | +1.8% | National; Warsaw, Kraków, Wrocław | Medium term (2-4 years) |

| OT-focused attacks on manufacturing belt | +1.5% | Silesia, Wielkopolska | Short term (≤ 2 years) |

| SME managed-security adoption | +1.2% | National; secondary cities | Medium term (2-4 years) |

| Cyber-espionage-driven government spending | +2.0% | National; eastern regions | Short term (≤ 2 years) |

| Digital-banking expansion and zero-trust | +1.0% | National; urban centers | Medium term (2-4 years) |

| National investment in cloud, 5G and AI | +1.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acceleration of Public-Cloud Migration Among Polish Mid-Caps

Mid-sized companies that skipped large on-premises cycles are adopting public clouds as their first major infrastructure platform, accelerating initial outlays on cloud-native security controls. As usage bills rise, boards question whether built-in safeguards are sufficient, pushing specialised vendors into earlier procurement stages. The Poland cybersecurity market therefore gains a new pool of buyers whose adoption timelines are compressed relative to larger peers. Vendors offering simplified policy orchestration win because lean teams need tools that hide cloud complexity [1]Thales Group, “European Cloud Security Study 2024,” thalesgroup.com.

Sharp Rise in OT-Focused Attacks on Poland’s Manufacturing Belt

Automotive and heavy-machinery plants in Silesia and Wielkopolska face a growing number of OT incidents as attackers exploit converged factory and corporate networks. Each new robotic arm adds an ingress point, so plant managers now include segmentation and anomaly detection in retrofit budgets. Integrators opening local offices underline how manufacturing is becoming the next growth vertically after finance and telecoms. Annual reports that now disclose factory downtime underscore that cyber resilience has clear financial materiality.

Surge in SME Managed-Security Adoption Amid Talent Shortage

Small businesses struggle to recruit qualified security personnel, prompting a pivot toward managed detection, response and incident-handling services. Bundled contracts convert variable licence costs into predictable operating expenses and provide documented SLAs that auditors view favourably. Because SMEs account for a large share of national employment, subscription revenue from thousands of smaller clients adds breadth and stability to vendor portfolios.

Cyber-Espionage Concerns Elevating Government Spend

State-linked intrusion attempts have led Warsaw to earmark USD 760 million for cyber-defenses in the current budget cycle. Public tenders increasingly demand supply-chain transparency and knowledge-transfer clauses, raising entry barriers for black-box products and building a domestic pool of certified specialists. The direct injection of funds lifts short-term license volumes and indirectly boosts private sector hiring[3]U.S. Department of State, “U.S.–Poland Cybersecurity MoU,” state.gov .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented public-sector procurement cycles | −0.8% | National; all administrative levels | Long term (≥ 5 years) |

| Budget constraints among municipal bodies | −1.2% | Smaller municipalities; rural regions | Medium term (2-4 years) |

| Low cyber-insurance penetration | −0.5% | National; especially SMEs | Long term (≥ 5 years) |

| Integration complexity in multi-vendor environments | −0.7% | National; large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Public-Sector Procurement Cycles Slowing Deal Closure

Decentralized buying structures force vendors to navigate redundant legal reviews across ministries, agencies and councils. The resulting delays raise bid costs and can deter smaller suppliers, narrowing competitive diversity. Grassroots moves toward joint framework agreements have begun but adoption is uneven, so sales cycles remain protracted.

Budget Constraints Among Municipal Bodies Limiting Advanced Tool Adoption

Local authorities balance essential citizen services against the rising cost of security tooling. National grants often cover hardware but not operating expenses, so councils hesitate to commit to full deployments. This creates uneven protection across critical services, with advanced safeguards more common in cities than rural areas. Vendors offering usage-based pricing report shorter sales cycles in budget-constrained districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Security Solutions Remain the Revenue Anchor

Solutions captured 67.30% Poland cybersecurity market share in 2025, underlining the enduring dominance of licenses for network firewalls, endpoint suites and cloud access brokers. Enterprise-wide perimeter refreshes ahead of NIS2 compliance sustain order pipelines, prompting resellers to deepen technical-support capabilities. Because frameworks seldom replace every tool at once, incremental upgrades stabilize distributor revenue.

Services are forecast to expand at a 15.05% CAGR, outpacing overall Poland cybersecurity market size growth. Compliance consulting rises fastest as organizations seek external auditors versed in European directives. Managed detection and response attract mid-caps that want always-on coverage without building a 24-hour SOC. Clients now assess service partners by the maturity of their AI toolchains rather than headcount, reflecting a pronounced shift in perceived value.

By Deployment Mode: Cloud Trajectory Accelerates

On-premises deployments accounted for 53.90% of 2025 Poland cybersecurity market size. Sensitive data in defense and energy remains in private data centers, but every hardware refresh prompts architects to question another capital cycle, gradually eroding on-premises share even if absolute spending stays stable.

Cloud security enjoys an 18.15% CAGR outlook, the fastest among deployment models. Thales data showing 61% of European organizations classifying at least 40% of cloud data as sensitive accelerates board approval for advanced encryption and key-management services. Subscription licenses align with operating-expense budgets, reducing friction compared with capital-heavy appliances and speeding adoption.

By End-User Vertical: Healthcare Surges Ahead

The BFSI segment commanded 25.60% Poland cybersecurity market size share in 2025, underscoring its role as benchmark for best practice. PKO Bank Polski logged 8 million active mobile users in Q1-2024, driving adoption of identity-centric, zero-trust architectures that later spread to less regulated industries.

Healthcare is set to grow at a 18.55% CAGR through 2031. Telemedicine connected devices and electronic health records multiply exposure points, so hospital administrators allocate specific ransomware-mitigation budgets. The Polish Hospital Federation counts roughly 170 digital-health start-ups embedding security at design phase, promising a resilient pipeline of future clinical tools.

By End-User Enterprise Size: SMEs Show Rapid Upside

Large enterprises held 70.80% Poland cybersecurity market share in 2025, powered by complex attack surfaces and multi-year roadmaps in banking, telecom and energy. Integrated platforms that reduce alert fatigue give suite vendors leverage during renewals. Purchase decisions by blue-chip firms influence vendor credibility across smaller accounts.

SMEs are projected to grow at a 16.75% CAGR, signaling that security is now viewed as a business continuity essential. Scarce talent pushes owners toward turnkey managed services, freeing internal staff to work on core applications. Recurring revenue from thousands of small subscriptions can match large-enterprise contracts in aggregate, offering vendors a diversified income base.

Geography Analysis

Warsaw commands the largest share of spending, housing headquarters of major banks, telecoms and government agencies. International vendors base regional support centres in the capital, shortening response times and improving customer satisfaction. A dense network of universities supplies skilled graduates who feed a vibrant start-up scene targeting niche security gaps.

Kraków and Wrocław form Poland’s second-tier cybersecurity hubs. Shared-service centres for global technology companies pilot new tools here before worldwide rollouts, giving local teams influence over product roadmaps. Higher salary benchmarks encourage specialists to pursue advanced certifications, deepening the talent pool available to mid-caps in adjacent regions.

Industrial regions such as Silesia and Wielkopolska concentrate heavy-machinery and automotive plants that now demand OT-specific safeguards. Vendors that once served only IT networks partner with automation integrators to secure production lines. Regional development agencies offer grants for cyber-resilience audits, pushing suppliers to combine technology with workforce-training modules that raise overall maturity.

Competitive Landscape

Global suites and home-grown specialists compete intensely across sub-segments. Cisco, Check Point and Palo Alto Networks dominate large firewall and endpoint projects by leveraging economies of scale and established support structures. Local champions like Asseco and Comarch counter with Poland-specific compliance modules and bilingual support desks that resonate with public-sector buyers.

Strategic partnerships are a key growth tactic. Asseco’s acquisition of Infocomp expanded its healthcare footprint and opened cross-sell opportunities, while global vendors forge reseller alliances that embed their cloud-security offerings into telecom-operated managed-service bundles. The approach helps reach SMEs that rarely procure direct, blurring the line between competitor and partner.

Investment flows spotlight white-space potential. Venture capital targets start-ups in privileged-access management and deception technology, reflecting confidence in Polish engineering talent. International firms open threat-research labs to tap skilled labour at competitive costs, further enriching the local ecosystem and raising the sophistication of the Poland cybersecurity market.

Poland Cybersecurity Industry Leaders

TestArmy Group

RED TEAM Sp. z o.o. Sp.k.

TraceRoute42 sp. z o.o.

Framework Security

Cyberlands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Microsoft confirmed a USD 700 million investment in new data-centre capacity and security-training programmes in Poland.

- February 2025: Fudo Security secured 40 million PLN (USD 10.2 million) from bValue Fund to scale privileged-access-management solutions.

- January 2025: Inovo.vc led a USD 2 million seed round for SplxAI, a start-up designing security layers for AI applications.

- October 2024: The U.S. and Poland signed an MoU to strengthen joint cyber-defence initiatives.

Poland Cybersecurity Market Report Scope

Cybersecurity solutions help organizations monitor, report, and counter cyber threats to maintain data confidentiality. The adoption of cybersecurity solutions is expected to grow in line with the rising internet penetration among developing and developed countries. The need for cybersecurity has increased as every system in today's world is connected to the internet, making data more accessible to cybercriminals.

The Poland cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

Key Questions Answered in the Report

What is the projected Poland cybersecurity market size by 2031?

The market is forecast to reach USD 2.26 billion by 2031 on the back of cloud adoption, heightened public-sector investment and escalating threat levels.

Which segment grows fastest within the Poland cybersecurity industry?

Managed security services, particularly among SMEs, lead growth with a projected 15.05% CAGR as firms seek outsourced 24-hour monitoring and response.

Why is healthcare the fastest-expanding end-user vertical?

Telemedicine, connected devices and stringent data-privacy rules push hospitals to invest in ransomware mitigation and identity management, resulting in a 18.55% CAGR forecast.

How does geopolitical tension affect cybersecurity spending in Poland?

State-linked intrusion attempts have triggered USD 760 million in government allocations for threat intelligence, secure networks and specialist training, boosting license volumes.

Page last updated on: