Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.02 Billion |

| Market Size (2026) | USD 15.55 Billion |

| Market Size (2031) | USD 26.23 Billion |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Cybersecurity Market Analysis by Mordor Intelligence

The Germany cybersecurity market size is projected to expand from USD 14.02 billion in 2025 and USD 15.55 billion in 2026 to USD 26.23 billion by 2031, registering a CAGR of 11.02% between 2026 to 2031. Heightened regulatory scrutiny, rapid cloud migration within public services, and accelerating Industrie 4.0 investments are reinforcing demand resilience across network, endpoint, and cloud-native controls. The Germany cybersecurity market is also benefiting from the mid-decade convergence of NIS2, DORA, and the Cyber Resilience Act, which collectively extend mandatory security obligations to tens of thousands of entities. Vendor competition remains vibrant because federal and Länder frameworks favor multi-vendor architectures that safeguard interoperability. In parallel, sovereign-cloud preferences are redirecting workloads toward domestic providers, entrenching data-residency as a critical purchase criterion and shaping the strategic roadmaps of both incumbents and challengers within the Germany cybersecurity market.

Key Report Takeaways

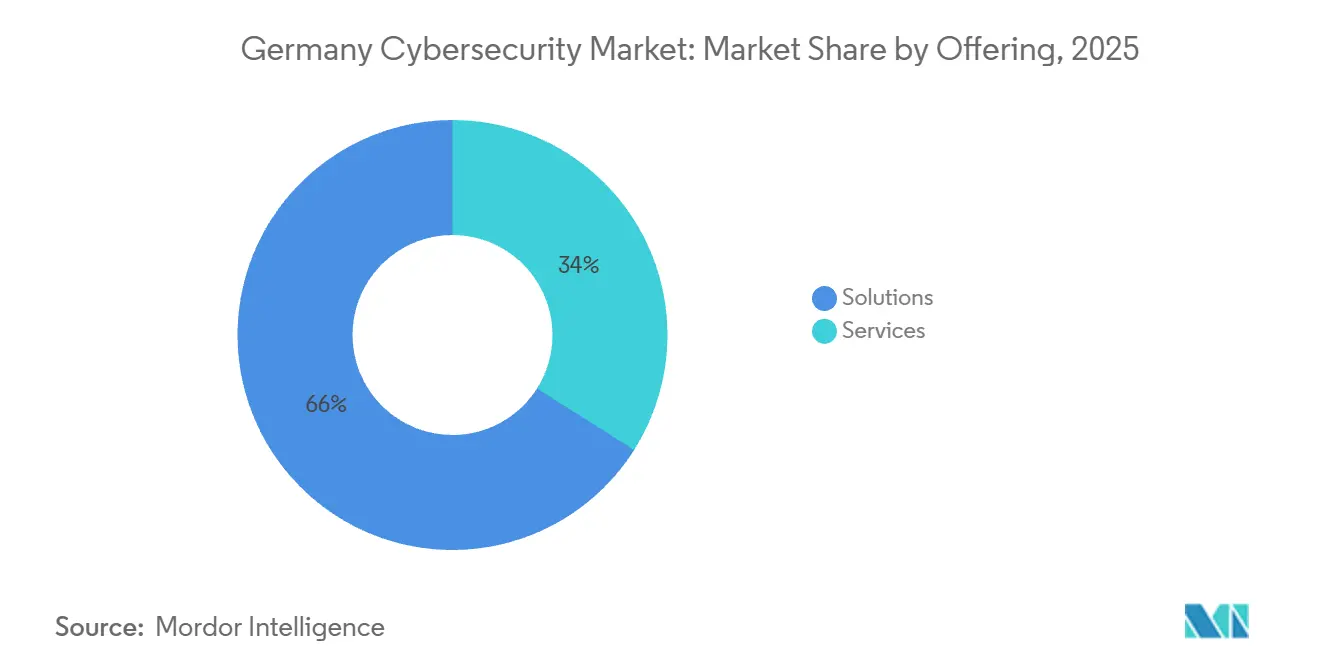

- By offering, solutions led with 66.02% of the Germany cybersecurity market share in 2025, while services are advancing at a 12.43% CAGR through 2031.

- By deployment mode, on-premise installations represented 52.77% of the Germany cybersecurity market size in 2025 and cloud deployments are expanding at a 12.84% CAGR to 2031.

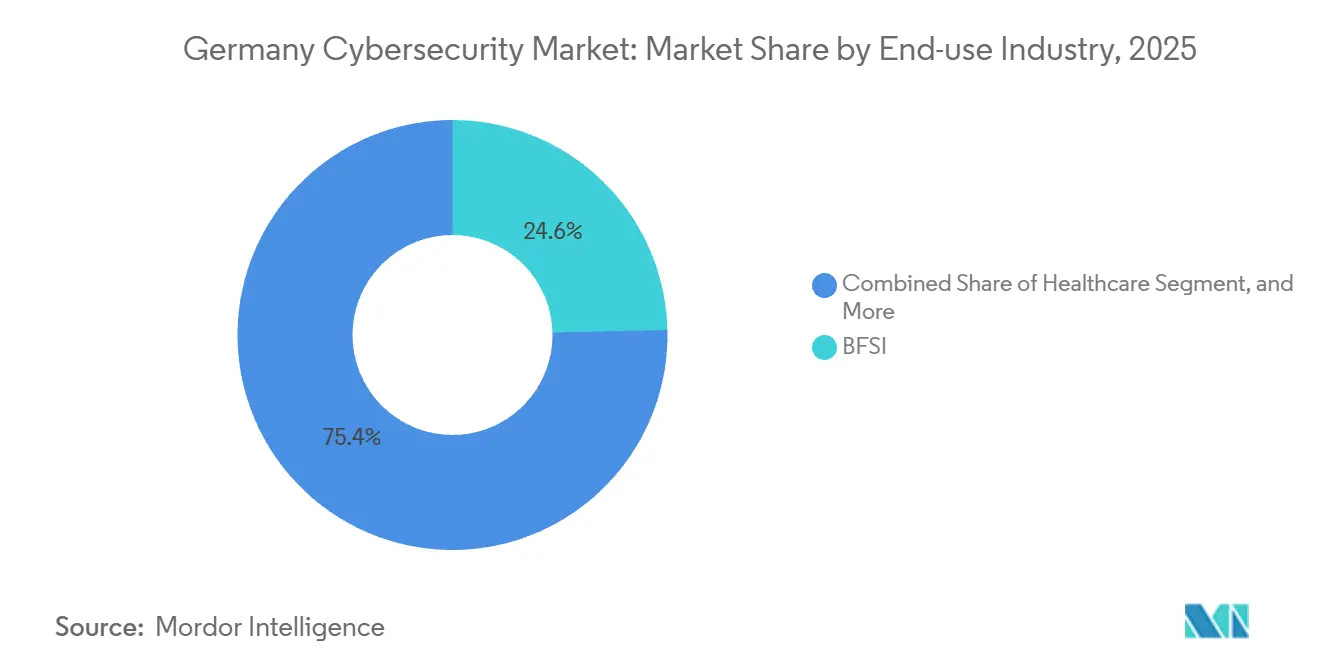

- By end-use industry, BFSI accounted for 24.62% of the Germany cybersecurity market size in 2025 and healthcare is rising at a 13.01% CAGR through 2031.

- By end-user enterprise size, large enterprises held 71.27% of the Germany cybersecurity market share in 2025, whereas small and medium enterprises are accelerating at a 12.56% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance Mandates (NIS2, DORA, BaFin IT Rules) | +2.8% | National with EU spillover | Short term (≤ 2 years) |

| OT/ICS Security Urgency amid Industrie 4.0 Roll-Outs | +2.3% | Baden-Württemberg, North Rhine-Westphalia | Medium term (2-4 years) |

| Cloud-Native Application Growth in Public Sector and Healthcare | +1.9% | Berlin, Hamburg, Bavaria | Medium term (2-4 years) |

| Expansion of 5G and Connected Mobility Infrastructure | +1.6% | Bavaria, Lower Saxony | Long term (≥ 4 years) |

| Rise of Cyber-Insurance Requirements Driving Security Spending | +1.2% | BFSI and manufacturing hubs | Short term (≤ 2 years) |

| AI-Driven Threat Detection and Response Automation | +1.0% | Large enterprise clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance Mandates (NIS2, DORA, BaFin IT Rules)

The combined transposition of NIS2 and the enforcement of DORA enlarged the pool of German entities subject to binding audits from roughly 2,000 to almost 30,000 between 2024 and 2025, imposing four-hour incident reporting, quarterly vulnerability scans, and third-party risk dashboards.[1]Bundesamt für Sicherheit in der Informationstechnik, “NIS2 Implementation in Germany,” bsi.bund.de Financial institutions face parallel scrutiny under BaFin’s MaRisk, which mandates zero-trust segmentation of critical payment systems. Enterprises that deferred upgrades suddenly faced simultaneous regulator visits, triggering a surge in managed detection and response contracts that explains why Services now outpace Solutions in the Germany cybersecurity market.

OT/ICS Security Urgency amid Industrie 4.0 Roll-Outs

Connecting legacy programmable logic controllers to enterprise networks widened the industrial attack surface, a risk underscored when a Tier-1 automotive supplier halted output following ransomware-induced downtime.[2]Siemens, “Annual Report 2025,” siemens.com The Cyber Resilience Act’s product-liability clauses, effective January 2026, push manufacturers to embed secure boot and remote-update features across equipment fleets. Consequently, automotive and chemical clusters in Baden-Württemberg and North Rhine-Westphalia are driving double-digit spending on industrial firewalls, anomaly detection and threat analytics.

Cloud-Native Application Growth in Public Sector and Healthcare

Hospital Future Act grants made reimbursement conditional on encrypted electronic health records and real-time monitoring, requirements most efficiently met via cloud security posture management. Deutsche Telekom’s T Cloud keeps workloads under German jurisdiction, removing CLOUD-Act exposure and attracting hundreds of public-sector and hospital tenants within months of launch.[3]Deutsche Telekom, “T Cloud Public Launch,” telekom.com Demand growth is therefore strongest for identity governance, data-loss prevention, and workload-encryption modules that integrate natively with sovereign cloud platforms.

Expansion of 5G and Connected Mobility Infrastructure

National 5G coverage exceeded 94% of residents by end-2025, creating the backbone for over-the-air vehicle updates. UNECE WP.29 turned cybersecurity into a type-approval prerequisite, prompting BMW, Mercedes-Benz, and Volkswagen to open 24-hour vehicle-security operations centers that ingest telematics telemetry at millisecond latency. Edge firewalls, automotive intrusion detection, and secure software update frameworks are therefore accelerating, especially across Bavaria and Lower Saxony’s R&D clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Shortage of German-Speaking Cybersecurity Professionals | -1.4% | National, acute outside metros | Long term (≥ 4 years) |

| Budget Limitations across SME-Dominated Mittelstand | -1.1% | Small manufacturing towns | Medium term (2-4 years) |

| Procurement Fragmentation across 16 Länder | -1.0% | All Länder agencies | Short term (≤ 2 years) |

| Data-Sovereignty Concerns Limiting Cloud Adoption | -0.9% | Nationwide, SaaS workloads | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Shortage of German-Speaking Cybersecurity Professionals

Germany recorded a gap of about 96,000 practitioners in 2025 because university curricula emphasize theory over hands-on incident response, leaving graduates ill-prepared for real-time SOC roles. Salaries for certified analysts rose 14% in Frankfurt and Munich, crimping margins for managed service providers that operate on fixed-price contracts. BSI apprenticeships aim to add 5,000 learners yearly, but relief will not materialize before 2028.

Budget Limitations across SME-Dominated Mittelstand

Mittelstand firms allocate only 4.2% of IT budgets to security, well below the 12% benchmark at large corporations. NIS2 gap assessments can cost EUR 50,000-200,000 (USD 56,000-224,000), a heavy lift for companies whose profit margins average 6-8% in precision engineering. Patchy subsidies across Länder compound disparities, slowing adoption of subscription-based tools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Compliance Outsourcing Accelerates

Solutions accounted for 66.02% of the Germany cybersecurity market size in 2025, reflecting entrenched firewalls, intrusion-prevention systems and endpoint agents. Yet Services are growing at 12.43% because NIS2 and DORA impose continuous monitoring and four-hour reporting that in-house teams cannot sustain. Managed security service providers, including T-Systems and Atos Eviden, now bundle SOC monitoring, quarterly scans and annual penetration tests into predictable operating budgets. Within Solutions, network and endpoint security combined for nearly 40% of revenue in 2025 thanks to zero-trust segmentation that BaFin guidance effectively mandates.

Cloud security and identity management are the fastest-growing solution families, each posting CAGRs above 13%, fueled by sovereign-cloud migrations and strict access-control rules for healthcare data. Application security also accelerated after high-profile supply-chain exploits nudged enterprises to embed composition analysis in CI/CD pipelines. Professional services clock higher percentage growth than managed services because many firms commission one-time zero-trust blueprints before committing to multi-year outsourcing.

By Deployment Mode: Sovereign Cloud Mandates Reshape Preferences

On-Premise deployments held 52.77% of the Germany cybersecurity market share in 2025 as KRITIS operators and defense contractors maintain air-gapped environments for classified workloads. Cloud configurations are nonetheless expanding at 12.84% because sovereign options from Deutsche Telekom, IONOS, and Open Telekom Cloud meet data-residency expectations that U.S. Cloud Act exposure jeopardizes. Schrems II continues to color buying decisions after regulators cautioned in 2024 that standard contractual clauses may not suffice.

Hybrid strategies now pair plant-floor control systems with cloud-based analytics in automotive and industrial facilities, balancing latency needs with elastic processing power. The Cyber Resilience Act further tilts software vendors toward cloud-native patch orchestration, reinforcing upward momentum in the Germany cybersecurity market. Additionally, the increasing adoption of IoT devices is driving the demand for robust cybersecurity solutions in the region.

By End-Use Industry: Healthcare Surges on Digitalization Mandates

BFSI captured 24.62% of the Germany cybersecurity market size in 2025, propelled by MaRisk updates that require annual penetration tests and strict network segmentation. DORA’s four-hour incident-notice window forced banks to automate response playbooks. Healthcare logs the fastest expansion, rising at a 13.01% CAGR, because the Hospital Future Act ties EUR 4.3 billion (USD 4.8 billion) in funding to encryption, role-based access control and audit logging implementations. Ransomware attacks that shut a Berlin clinic in 2024 further cemented security as a patient-safety priority.

Industrial manufacturing follows, driven by Industrie 4.0 retrofits that expose OT assets to internet vectors. Retail and e-commerce accelerate under PCI DSS 4.0, while energy utilities reinforce controls to meet KRITIS audits. Aerospace and defense remain niche yet command premium project pricing owing to classified-network requirements.

By End-User Enterprise Size: SMEs Accelerate Under Insurance Pressure

Large Enterprises held 71.27% of the Germany cybersecurity market share in 2025, buoyed by larger budgets, deeper regulatory oversight, and global footprint exposures. Yet SMEs are expanding at 12.56% because insurers will not underwrite policies without foundational controls such as multi-factor authentication and endpoint detection. The new underwriting stance converts optional safeguards into commercial prerequisites. Managed service providers responded with turnkey bundles that cost EUR 500-2,000 (USD 560-2,240) per month, making baseline protection achievable without full-time staff.

Small and Medium Enterprises are also leveraging security-as-a-service bundles that include managed endpoint agents, automated patching, and phishing-simulation training, allowing firms with limited headcount to meet insurer checklists without hiring full-time analysts. Adoption is supported by BSI’s “IT-Grundschutz kompakt” templates, which reduce policy drafting time and lower audit costs for companies entering the NIS2 compliance queue in 2026. Even so, the talent deficit remains acute: 72% of SMEs surveyed by Bitkom in late 2025 reported that open cyber roles remain vacant for more than 6 months, pushing them toward greater reliance on automation and external incident response retainers. Over the forecast horizon, this mix of regulatory pressure, insurance incentives and managed-service availability is expected to narrow but not fully close the maturity gap between large enterprises and SMEs within the Germany cybersecurity market.

Geography Analysis

Southern Germany, led by Bavaria and Baden-Württemberg, contributes a disproportionate share of the Germany cybersecurity market because automotive and machinery clusters navigate UNECE WP.29 and Industrie 4.0 deadlines that mandate real-time threat monitoring. Munich and Stuttgart also favor sovereign-cloud deployments for sensitive design files, stimulating local uptake of identity governance solutions. Lower Saxony adds momentum as Wolfsburg’s connected-vehicle R&D pipeline expands, demanding low-latency intrusion detection across 5G corridors.

In the north, Hamburg’s port economy and Bremen’s aerospace hubs channel spending toward maritime and satellite cybersecurity platforms. Berlin’s tech ecosystem accelerates SaaS usage, yet city agencies insist on domestic data residency, reinforcing demand for compliant cloud posture controls. North Rhine-Westphalia, Germany’s most populous Land, blends steel, chemicals and financial services, making it fertile ground for managed detection and response engagements.

Eastern Länder such as Saxony and Thuringia trail in absolute spend. However, local subsidy programs narrow the gap by underwriting up to 50% of qualified security investments. Cloud adoption grows once sovereign providers extend availability zones eastward, enabling SMEs in Chemnitz and Jena to offload log analytics and vulnerability scanning to hosted platforms with acceptable latency and cost profiles.

Competitive Landscape

The Germany cybersecurity market remains moderately fragmented. Deutsche Telekom leverages sovereign-cloud exclusivity to bundle managed detection and response into public contracts containing strict data-residency clauses. Rheinmetall and Rohde and Schwarz exploit defense clearances to secure KRITIS engagements that demand vetted personnel and air-gapped engineering.

International vendors localize to overcome language and latency hurdles; CrowdStrike and Arctic Wolf opened Frankfurt SOCs staffed with German speakers, easing Mittelstand adoption barriers. Startups such as genua and PHYSEC craft quantum-resistant encryption and physical-layer security, positioning for BSI’s post-quantum roadmap starting 2027. Mergers remain sparse because antitrust authorities scrutinize deals that could reduce competition in critical infrastructure sectors.

Sustainable differentiation now hinges on compliance mapping, sovereignty guarantees and protocol specialization. Suppliers embedding point-and-click regulatory dashboards, hosting data under German jurisdiction, or mastering OT protocols outperform peers focused solely on horizontal threat detection, shaping the trajectory of the Germany cybersecurity market.

Germany Cybersecurity Industry Leaders

IBM Deutschland GmbH

Cisco Systems Germany

Fortinet Germany GmbH

Deutsche Telekom (T-Systems)

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Deutsche Telekom augmented its T Cloud Public footprint with new availability zones in Frankfurt, Munich and Hamburg and opened a Cybersecurity Innovation Center in Bonn.

- February 2026: Deutsche Telekom confirmed full production at its AI factory equipped with 10,000 NVIDIA H100 GPUs to enable domestic training of large language models for threat analytics.

- December 2025: Rheinmetall and ICEYE created a venture to deploy a 20-satellite SAR constellation under a EUR 1.7 billion (USD 1.9 billion) defense contract for critical-infrastructure monitoring.

- December 2025: Deutsche Telekom invested in Quantum Systems to accelerate migration toward lattice-based encryption ahead of post-quantum deadlines.

Germany Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware, malware, and phishing.

The Germany Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace Military and Defense, and Other End-use Industries), End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| Endpoint Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| Endpoint Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Germany cybersecurity market today?

The market reached USD 15.55 billion in 2026 and is forecast to hit USD 26.23 billion by 2031.

What CAGR is projected for German cybersecurity spending?

A compound annual growth rate of 11.02% is expected from 2026 to 2031.

Which deployment option is expanding fastest?

Cloud installations on sovereign platforms are growing at a 12.84% CAGR.

Why is healthcare leading growth among verticals?

Hospital Future Act funding ties reimbursements to encryption and monitoring, driving a 13.01% CAGR.

How are insurance rules shaping SME security spending?

Underwriters now demand ISO 27001 controls and multi-factor authentication, spurring SMEs to adopt managed service bundles and fueling a 12.56% CAGR.

What is the biggest drag on market expansion?

A shortage of roughly 96,000 qualified professionals adds cost and delays, trimming growth by an estimated 1.4 percentage points.

Page last updated on: