Egypt Cybersecurity Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

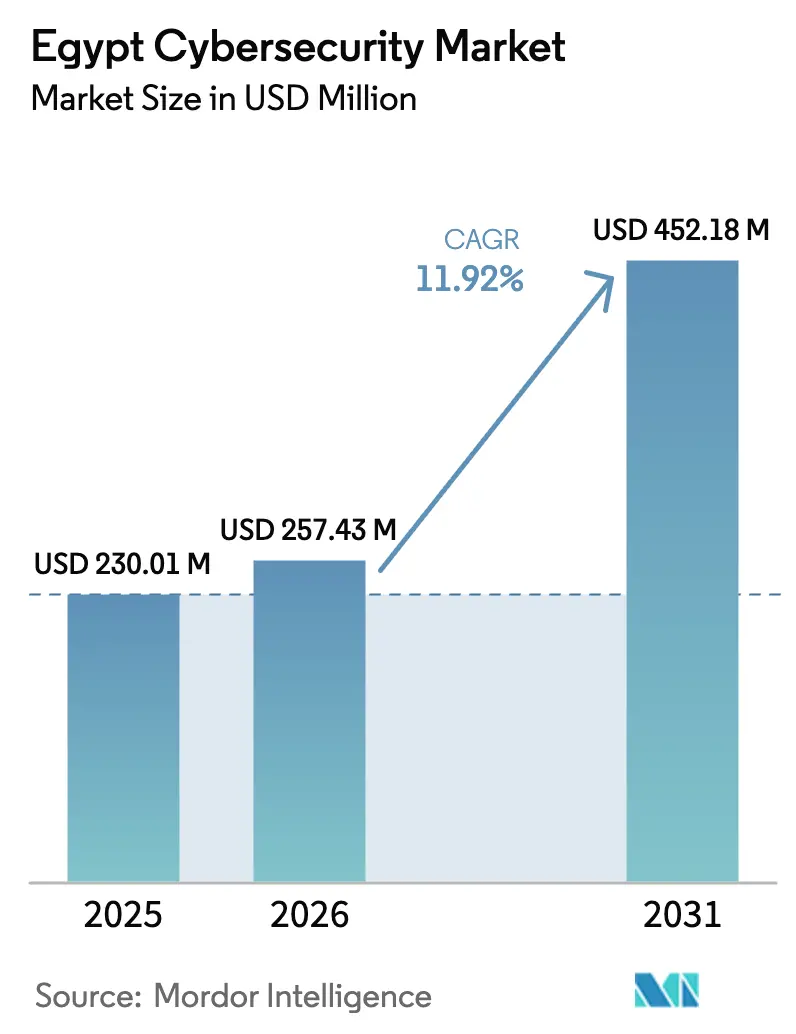

| Base Year Market Size (2025) | USD 230.01 Million |

| Market Size (2026) | USD 257.43 Million |

| Market Size (2031) | USD 452.18 Million |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

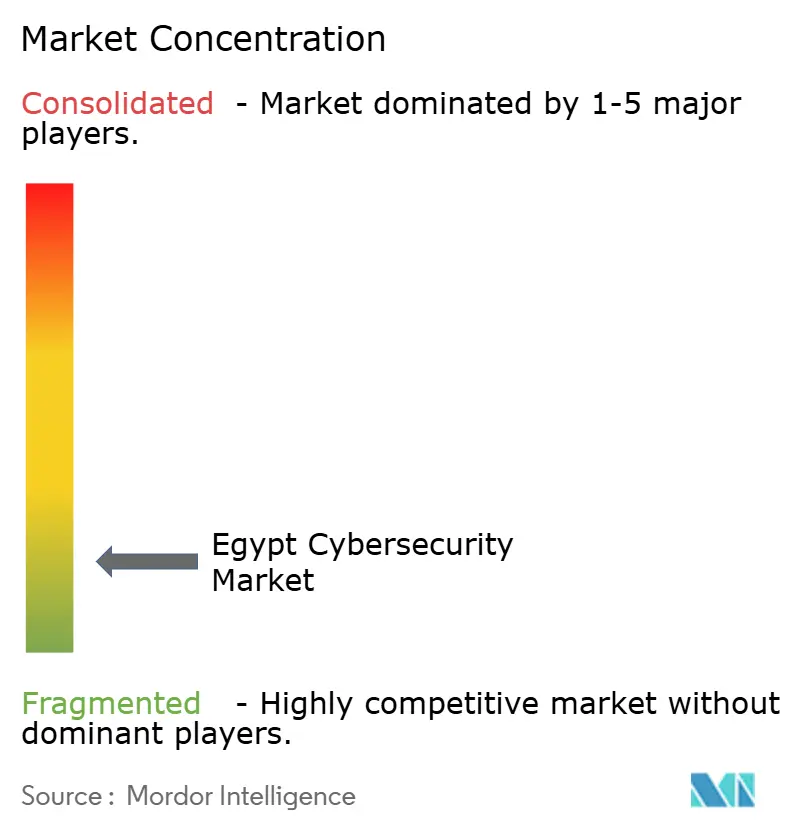

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Cybersecurity Market Analysis by Mordor Intelligence

The Egypt Cybersecurity market size is expected to grow from USD 230.01 million in 2025 to USD 257.43 million in 2026 and is forecast to reach USD 452.18 million by 2031 at 11.92% CAGR over 2026-2031.

Egypt’s rising status as a regional digital hub, major broadband upgrades worth EGP 150 billion since 2018, and the government’s Digital Egypt agenda underpin this growth. Heightened cyber-attack exposure—13% of total incidents recorded across Africa—has made proactive security investments a board-level imperative for enterprises and public agencies. Rapid fintech adoption, the rollout of smart-city projects such as the New Administrative Capital, and the launch of the first Government Data and Cloud Computing Center are broadening threat surfaces and intensifying demand for end-to-end protection. Parallel regulatory milestones—the National Cybersecurity Strategy (2023-2027) and Personal Data Protection Law 151—are pushing companies toward certified frameworks, thus amplifying market opportunity. Intensified competitive activity from IBM, Microsoft, Cisco, Orange Cyberdefense, and home-grown Secure Misr keeps solution breadth high and prices keen, even as acute talent shortages present implementation bottlenecks.

Key Report Takeaways

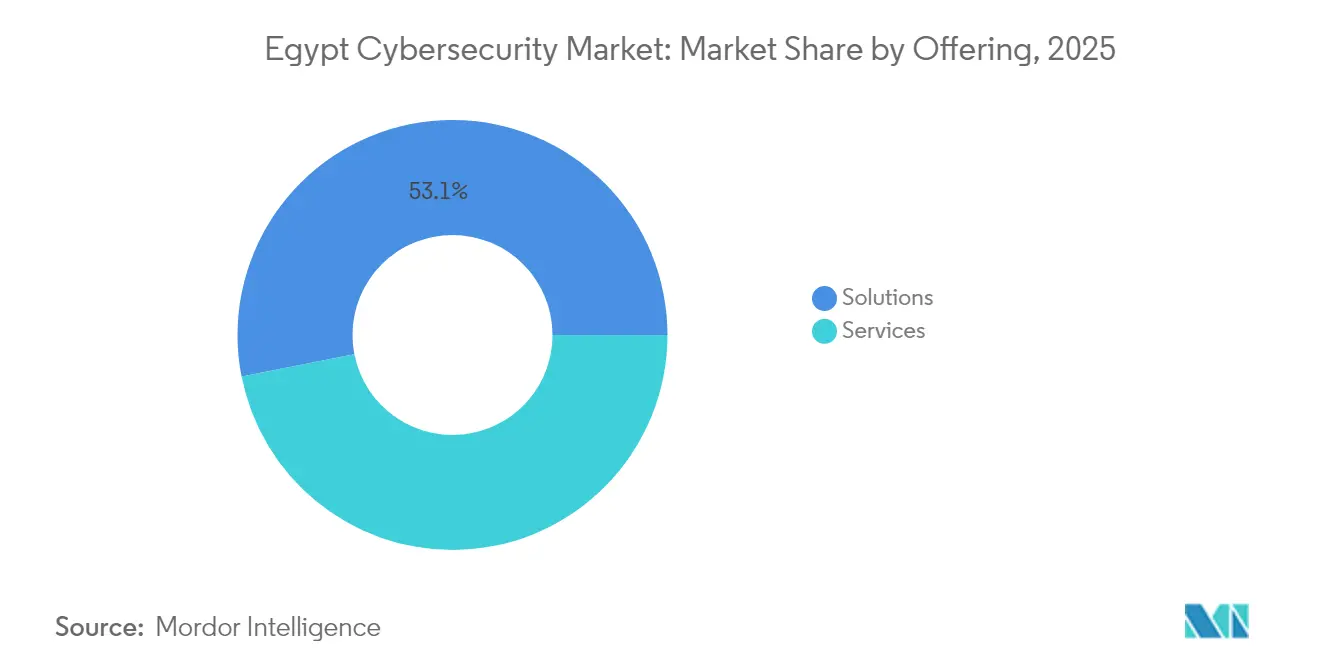

- By offering, solutions retained 53.10% revenue share in 2025 while managed services are projected to grow at a 13.25% CAGR to 2031

- By deployment mode, on-premise systems held 58.15% of Egypt cybersecurity market share in 2025, whereas cloud security is expected to expand at a 14.35% CAGR through 2031

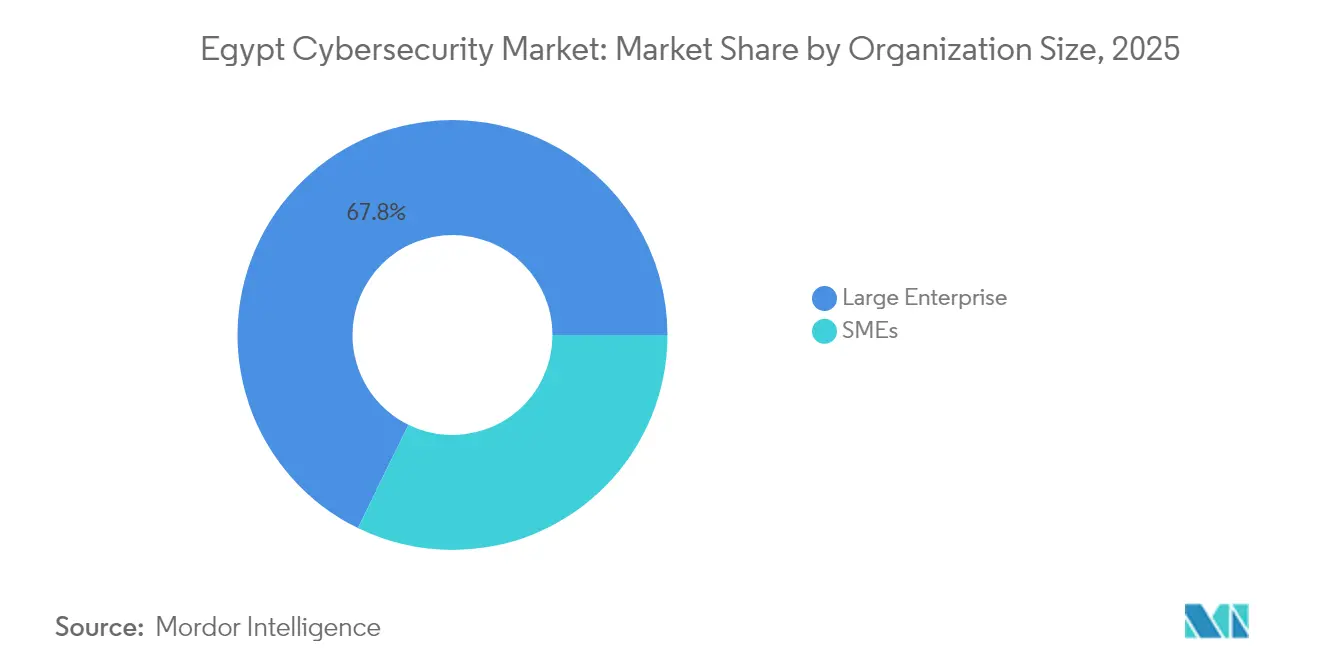

- By organization size, large enterprises commanded 67.75% of Egypt cybersecurity market size in 2025, yet SMEs are slated to post a 13.62% CAGR over the same period

- By end user, BFSI led with 31.10% revenue share in 2025; healthcare is forecast to increase at a 14.05% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cybersecurity Strategy accelerating public-sector spend | +2.8% | Cairo and New Administrative Capital | Medium term (2-4 years) |

| Fintech and mobile payments elevating threat surface | +2.1% | Urban centers nationwide | Short term (≤2 years) |

| Smart-city and mega-infrastructure projects | +1.9% | New Administrative Capital, Alexandria, Suez Canal Zone | Long term (≥4 years) |

| Personal Data Protection Law 151 compliance | +1.6% | Nationwide; early BFSI and healthcare uptake | Medium term (2-4 years) |

| Cloud adoption under Digital Egypt | +1.4% | Government and enterprise | Medium term (2-4 years) |

| OT digitalisation in oil-and-gas/Suez Canal | +1.2% | Energy corridors, industrial zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government’s National Cybersecurity Strategy (2023-2027) Accelerating Public-Sector Spend

The strategy sets clear metrics for local industry GDP contribution, research output, and talent pipelines. Its rollout coincided with the April 2024 commissioning of a 130,000-m² Government Data and Cloud Computing Center featuring 1,327 main servers and 120 petabytes of storage, connecting 33,000 government buildings via fiber. Ministries that once operated siloed defenses are now centralising operations, catalysing orders for integrated risk-management and infrastructure-security suites.

Proliferation of Fintech and Mobile Payments Elevating Threat Surface

Mobile-wallet transaction value hit EGP 268 billion and active users surpassed 26 million, while 88% of citizens used at least one emerging payment method in 2024. New tokenisation rules from the Central Bank mandate enhanced fraud controls, leading banks to prioritise application security and identity-access management. Annual cybercrime losses of USD 4 billion reinforce urgency for multilayered defenses, as illustrated by Banque Misr’s maintenance of PCI-DSS certification for the 12th year.

Smart-City and Mega-Infrastructure Projects Requiring End-to-End Security

Partnerships such as Honeywell-Etisalat Misr have embedded cyber-proof IoT frameworks into the New Administrative Capital’s command-and-control centre, integrating traffic, utilities, and emergency systems. USD 2.5 billion invested in backbone internet upgrades since 2018 amplifies data flows and attack vectors across connected lighting, smart parking, and industrial IoT sites[1]Honeywell, “Honeywell and Etisalat Misr to Secure New Administrative Capital,” honeywell.com.

Enforcement of Personal Data Protection Law Driving Compliance Investments

Law 151 imposes 72-hour breach-notification rules, Data Protection Officer requirements, and fines of up to EGP 5 million. The Personal Data Protection Centre launched in 2024 now licenses data processors, pushing firms to deploy encryption, data-classification, and rights-management tools that map to GDPR-inspired mandates.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Cyber-Talent Shortage within Egypt | -2.3% | National, with acute impact in specialized sectors | Medium term (2-4 years) |

| Budgetary Constraints among SOEs & SMEs | -1.8% | National, with higher impact in rural and industrial areas | Short term (≤ 2 years) |

| Legacy OT Limiting Modern Security Deployment | -1.4% | Regional, concentrated in oil & gas, manufacturing, and Suez Canal operations | Long term (≥ 4 years) |

| Fragmented Regulatory Enforcement Delaying Procurement Cycles | -1.1% | National, with particular impact on government and public sector procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Cyber-Talent Shortage Within Egypt

Government scholarships and the Cyber Talents program aim to graduate 1,000 specialists a year, yet market demand for SOC analysts and ICS engineers far outpaces supply. Average cyber-security salaries have climbed to USD 98,497, intensifying competition between multinationals and local providers and delaying some projects. IBM’s pledge to upskill 100,000 Egyptians via its SkillsBuild program offers long-term relief but cannot solve immediate capacity gaps.

Budgetary Constraints Among SOEs and SMEs

Currency depreciation and inflation pressures limit discretionary IT budgets, particularly for state-owned utilities and family-owned firms outside Greater Cairo. Compliance outlays for Law 151—such as breach-notification platforms—strain SME resources, although “Micro-SOC” subscription bundles from Orange Cyberdefense are easing entry barriers for smaller organisations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Speed While Solutions Keep Scale

Solutions retained the lion’s share at 53.10% in 2025, led by network-security equipment and endpoint protection across critical ministries and financial institutions. Managed services, however, are on course for a 13.25% CAGR to 2031, underscoring a pivot toward outsourced monitoring as companies grapple with talent gaps. Egypt cybersecurity market size for managed services is expected to rise in tandem with the expansion of local Security Operations Centers built by telecom carriers.

Cloud, application, and identity-access-management stacks saw the steepest year-on-year growth as fintech platforms multiplied. Egypt cybersecurity market continues to benefit from Orange Cyberdefense’s micro-SOC, IBM’s X-Force threat-intelligence feed, and Secure Misr’s Arabic language adversary-simulation service portfolio. Integrated risk-management suites now bundle policy, audit, and incident-response modules to streamline Law 151 compliance.

By Deployment Mode: Cloud Momentum Builds Despite On-Premise Dominance

On-premise controls still account for 58.15% of 2025 spend, a figure rooted in data-sovereignty priorities at banks and defense operators. Egypt cybersecurity market size for on-premise deployments will nevertheless cede ground as the public sector shifts workloads into the national cloud complex with 120 petabytes of capacity. Cloud-native security is racing ahead at a 14.35% CAGR to 2031, powered by 5G network prep and the attraction of consumption-based pricing.

Hybrid patterns are gaining favour: state agencies keep citizen records on site but adopt cloud-delivered SIEM analytics for faster threat correlation. The new Government Data Center’s common-controls framework is setting interoperability norms, encouraging suppliers to certify solutions under regional cloud-security standards.

By Organization Size: SME Uptake Accelerates

Large enterprises held 67.75% revenue share last year, yet SMEs will clock the highest 13.62% CAGR through 2031. Public incentives under the ICT 2030 blueprint include subsidised training vouchers and tax relief on security hardware, prompting micro-retailers to secure e-commerce payment links. Egypt cybersecurity market size devoted to SME protection is therefore poised for double-digit expansion as managed-service bundles bring enterprise-grade defence within smaller budgets.

Conversely, conglomerates in energy, telecom, and banking are expanding in-house SOCs equipped with AI-driven threat hunting. Several now subscribe to regional cyber-range platforms that simulate attacks on OT networks, reinforcing the continuous-learning culture demanded by evolving threats.

By End User: Healthcare Outpaces Other Verticals

BFSI kept pole position with 31.10% spend in 2025, reflecting continuous PCI-DSS recertification cycles and aggressive fraud-prevention roadmaps. Healthcare, however, is forecast to surge ahead at a 14.05% CAGR to 2031 as nationwide e-health insurance, connected medical devices, and tele-consult platforms generate sensitive patient data. Egypt cybersecurity market share for healthcare solutions is set to widen once the Digital Egypt Platform integrates medical records across public and private providers.

Industrial and defense segments are intensifying procurement of ICS security for oil-and-gas pipelines and Suez Canal automation. Retailers, utilities, and manufacturing firms face mounting ransomware campaigns, triggering demand for zero-trust network segmentation and legacy-system patch orchestration.

Geography Analysis

Greater Cairo anchors demand, hosting IBM’s Client Engineering hub, Commvault’s Center of Excellence, and Konecta’s USD 100 million regional headquarters. Abundant multilingual talent and fibre backbones make the capital the epicentre for threat-intelligence services and managed-security exports across Africa and the Middle East. Egypt cybersecurity market revenues generated in Cairo continue to dominate national totals.

The New Administrative Capital exemplifies green-field build-outs where security is hard-wired from the ground up: every streetlight, sensor, and public-safety feed feeds a unified command platform hardened with Honeywell cyber-proof protocols. Alexandria and the Suez Canal Zone form the industrial flank, where port digitalisation and petrochemical upgrades are sparking orders for maritime and OT-focused controls.

Beyond metropolitan clusters, six regional technology parks, supported by the Ministry of Communications, extend training and incubation programs into secondary cities. This decentralisation strategy both grows local job pools and opens fresh sales lanes for mid-tier integrators. The government also views Egypt as a continental data corridor; new submarine-cable landing stations on the Red Sea and Mediterranean coasts entail multilayer security for cross-border traffic.

Competitive Landscape

Competition is moderate, with global majors, regional telecom affiliates, and domestic boutiques sharing wallet. IBM, Microsoft, Cisco, and Palo Alto Networks bundle hardware, software, and managed detection layers, often through government framework contracts. Orange Cyberdefense, Vodafone Egypt, and Etisalat Misr leverage network reach to sell integrated connectivity-plus-security packs to SMEs and remote-office clients.

Local pure-plays—Secure Misr, Absega, and Niotek—differentiate through Arabic-language threat-intel feeds, tailored Law 151 compliance modules, and flexible pricing. Market fragmentation persists because no single vendor controls more than 10% of bookings; however, joint ventures and capacity-building pledges (e.g., IBM’s 100,000-person upskilling plan) are likely to reshape share dynamics. Industrial cybersecurity is an under-served niche that new entrants are targeting with IEC-62443-certified gateways and SOC-as-a-service packages[3]IBM, “IBM SkillsBuild to Train 100,000 Egyptians in AI,” ibm.com.

Acquisition activity remains muted, but technology partnerships are multiplying. Commvault’s Cairo centre uses local engineers to support backup-and-recovery clients across EMEA, while Trend Micro collaborates with ed-tech platform Nafham on nationwide cyber-awareness campaigns. Vendors able to supply holistic, compliance-ready stacks stand to gain as procurement cycles grow more sophisticated.

Egypt Cybersecurity Industry Leaders

IBM Corporation

Palo Alto Networks, Inc.

Absega Egypt Technology Services

Fortinet Inc.

Cyberteq

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBM partnered with the ministry to train 100,000 Egyptians in AI skills under the SkillsBuild program.

- March 2025: Government unveiled plans to train 30,000 AI specialists and support 250 AI-driven firms under a new national AI strategy.

- February 2025: Nafham teamed with Trend Micro on the #Akhberna_bkesetek internet-safety contest for students.

- January 2025: Konecta and the Information Technology Industry Development Agency signed a USD 100 million MoU to open a regional HQ in New Cairo that will provide cybersecurity and AI services.

Egypt Cybersecurity Market Report Scope

Cybersecurity involves safeguarding a business's data and digital infrastructure against cyber attacks and breaches. Companies offer services aimed at shielding data and services from potential breaches. The specific protection measures employed depend on the organization's internal structure and the technologies it utilizes.

The Egypt cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

| On-Premise |

| Cloud |

| SMEs |

| Large Enterprises |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the current size of the Egypt cybersecurity market?

The market is valued at USD 257.43 million in 2026.

How fast is the Egypt cybersecurity market expected to grow?

It is set to register a 11.92% CAGR, reaching USD 452.18 million by 2031.

Which segment will expand the quickest?

Cloud-based security is projected to grow at 14.35% CAGR through 2031.

Why is healthcare becoming a priority for cybersecurity vendors in Egypt?

Digital health platforms and new patient-data regulations are driving a 14.05% CAGR for healthcare-focused security solutions.

What are the main barriers to wider cybersecurity adoption in Egypt?

A shortage of specialised talent and tight IT budgets at SOEs and SMEs are the two most significant restraints.

Which cities outside Cairo are emerging hotspots for cybersecurity spending?

The New Administrative Capital, Alexandria, and the Suez Canal Zone are all witnessing rapid growth due to smart-city and industrial-digitalisation projects.

Page last updated on: