Nigeria Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

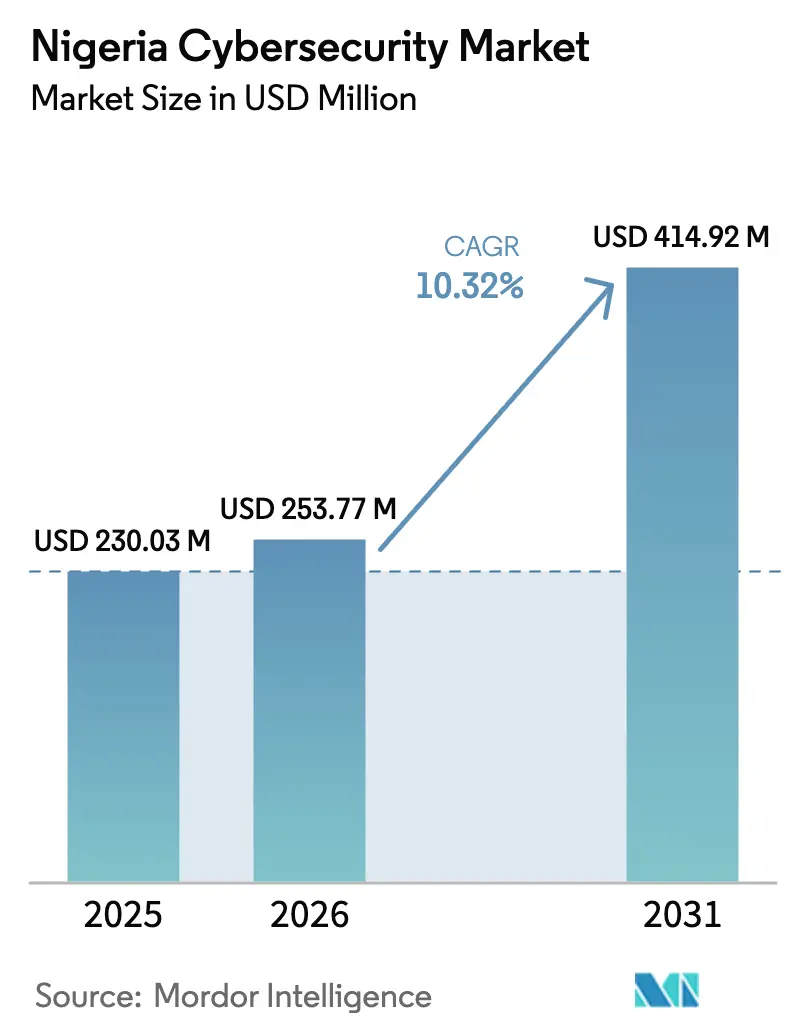

| Base Year Market Size (2025) | USD 230.03 Million |

| Market Size (2026) | USD 253.77 Million |

| Market Size (2031) | USD 414.92 Million |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Cybersecurity Market Analysis by Mordor Intelligence

The Nigeria cybersecurity market size was valued at USD 230.03 million in 2025 and estimated to grow from USD 253.77 million in 2026 to reach USD 414.92 million by 2031, at a CAGR of 10.32% during the forecast period (2026-2031). Widespread digital-payments adoption, the National Data Protection Act’s strict mandates, and an expanding cloud-centric IT environment collectively propel demand, while intermittent power supply and a shortage of certified professionals temper the pace. Accelerating 5G roll-outs in Lagos and Abuja broaden the attack surface, prompting enterprises to integrate cloud-native threat-detection, zero-trust frameworks, and AI-driven analytics. Competitive intensity is elevated: global vendors court large banks and telcos, whereas local specialists differentiate through regulatory expertise and niche managed services. A sustained venture-capital inflow into fintech and health-tech start-ups is enlarging the customer base for affordable, subscription-based security packages that cater to SMEs, reinforcing the Nigeria cybersecurity market’s medium-term momentum.

Key Report Takeaways

- By deployment mode, cloud-delivered security captured 57.20% of Nigeria cybersecurity market share in 2025 and is expanding at a 20.40% CAGR to 2031.

- By end-user industry, BFSI commanded 29.20% of the Nigeria cybersecurity market size in 2025, while healthcare is projected to register the fastest 21.90% CAGR through 2031.

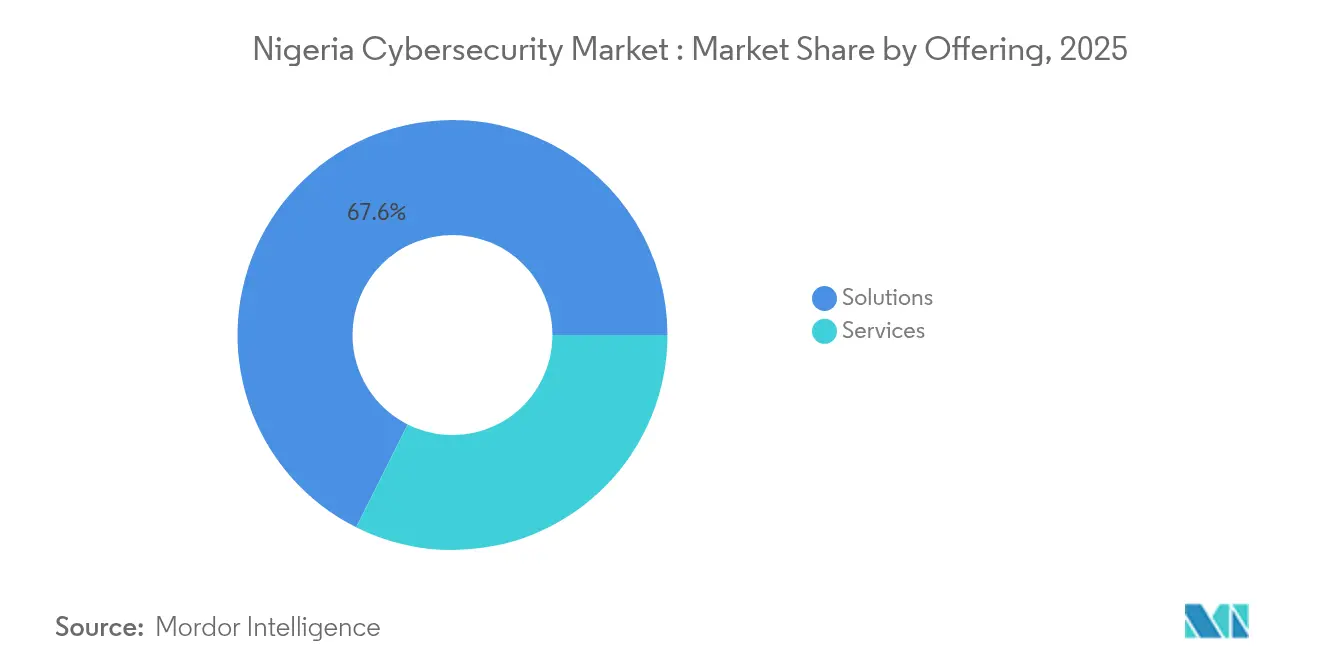

- By offering, solutions held 67.60% revenue share in 2025; managed services post the highest 17.20% CAGR to 2031.

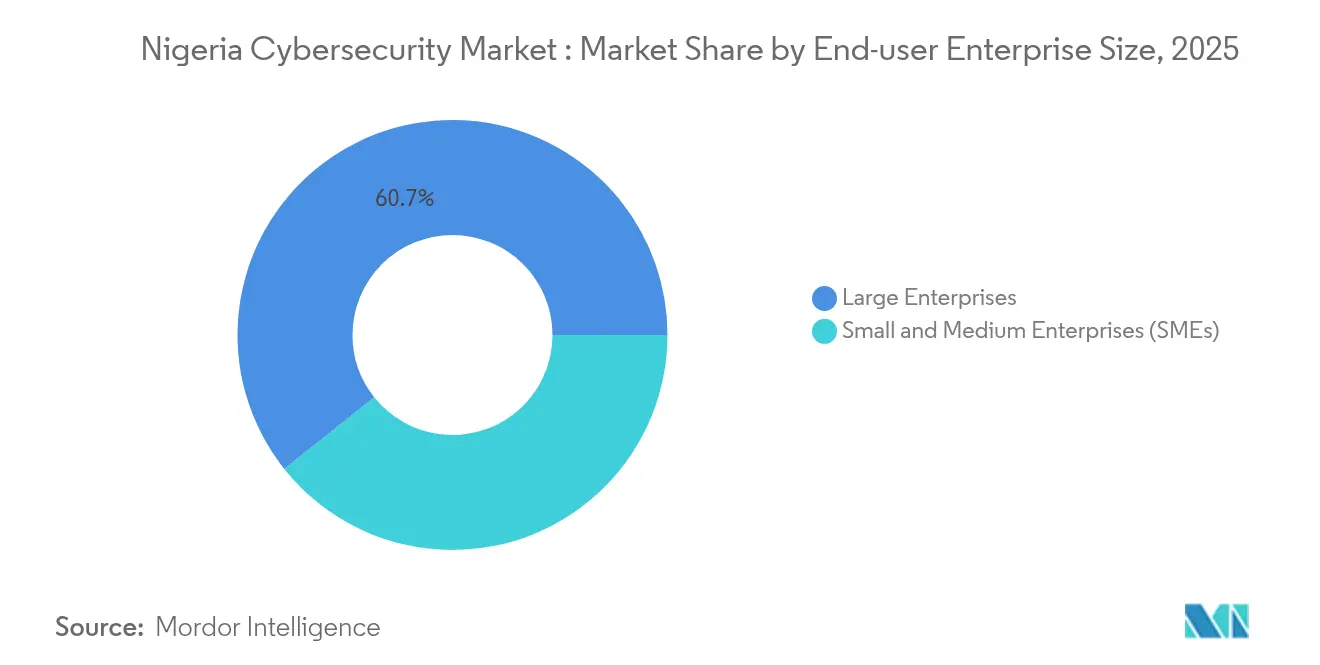

- By end-user enterprise size, large enterprises accounted for 60.70% share of the Nigeria cybersecurity market size in 2025, but SMEs are slated to grow at 18.60% CAGR between 2026-2031.

- Digital Encode, CyberSOC Africa, Microsoft, Cisco, Fortinet, and IBM jointly controlled an estimated 47.60% Nigeria cybersecurity market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cash-less economy policies | +2.1% | Lagos, Abuja, Port Harcourt | Short term (≤ 2 years) |

| Data-protection compliance | +1.8% | National | Medium term (2-4 years) |

| Ransomware in oil and gas | +1.2% | Niger Delta | Short term (≤ 2 years) |

| Cloud First Policy | +1.9% | National administrative centres | Medium term (2-4 years) |

| 5G expansion | +1.4% | Lagos and Abuja, national roll-out | Long term (≥ 4 years) |

| Fintech VC investments | +1.7% | Lagos, secondary effect in Abuja | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cash-less economy policies

Nigeria’s accelerated drive toward cash-less payments magnifies fraud-related risk exposure, compelling banks to spend on end-to-end transaction monitoring, multifactor authentication, and tokenization platforms. Fraud losses of NGN 9.75 billion in H1 2023 forced lenders to adopt shared-intelligence initiatives such as Operation Radar, which disseminates real-time threats across institutions. The Central Bank’s 2024 directive binding BVN to NIN for all Tier-1 accounts tightens identity checks and opens revenue streams for API-based verification providers that integrate seamlessly with core banking systems. Payment-fintechs embedding compliance features at the application layer gain a competitive edge, illustrating how regulation recasts security from a cost centre into a differentiation lever.[1]BusinessDay Staff, “Nigeria ranks 14th on global cyberattack risk index,” businessday.ng

Data-protection compliance

The Nigeria Data Protection Act mandates explicit consent, breach reporting, and registration for major data controllers. Penalties ranging from NGN 2 million to NGN 10 million elevate compliance from optional to essential. Licensing of Data Protection Compliance Organisations has already generated NGN 2 billion in fees, and more than 115,000 privacy professionals have been trained to fill advisory gaps. Demand for audit-ready encryption, data-loss-prevention, and rights-management tooling is rising across finance, healthcare, and e-commerce. Enterprises that align early convert compliance into trust capital, shortening sales cycles, especially in cross-border outsourcing deals. [2]Source: Nigerian Communications Commission, “Nigeria’s digital readiness climbs to 71%,” ncc.gov.ng

Ransomware in oil and gas

Sophisticated threat actors increasingly target drilling control systems, pipeline SCADA networks, and refinery automation. International operators exiting onshore assets leave transitional security gaps that local buyers scramble to close with OT-specific micro-segmentation, anomaly detection, and incident-response retainer services. Only 50% of energy firms carry cyber-insurance; premium hikes above 300% push the sector toward consequence-based risk modelling and network-isolation strategies. The Nigeria cybersecurity market benefits as OT-security vendors deliver ruggedised solutions capable of running despite fluctuating bandwidth or power outages.[3]Source: Dojah Research Team, “Bank fraud losses surge in cashless push,” dojah.io Source: Victor Esemosele, “CBN mandates BVN/NIN linkage,” businessday.ng

Cloud First Policy

Public-sector agencies adopt SaaS-delivered email, collaboration, and ERP platforms in line with the federal Cloud First Policy. Security controls must therefore satisfy data-sovereignty clauses, prompting the rise of hybrid architectures that store sensitive citizen records in in-country facilities while off-loading compute-intensive analytics to hyperscalers. Demand surges for cloud-workload-protection and posture-management offerings that automate compliance evidence. Skills shortages foster a parallel boom in managed detection and response (MDR) specialised for multi-tenant environments serving ministries and parastatals.[4]Source: BankInfoSecurity Editorial, “Cyber-insurance adoption in African oil sector,” bankinfosecurity.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low cyber-insurance uptake | -1.3% | National | Medium term (2-4 years) |

| Power-supply instability | -1.6% | National, greater outside megacities | Long term (≥ 4 years) |

| Certified-talent scarcity | -1.5% | Outside Lagos and Abuja | Medium term (2-4 years) |

| Fragmented NDPR enforcement | -1.1% | State-by-state variation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low cyber-insurance uptake

Inflated premiums and exclusions deter many firms from transferring residual risk to insurers. Without coverage that incentivises controls, especially in manufacturing and critical-infrastructure segments, boards sometimes postpone spending on advanced security analytics. Market education programs by brokers and government subsidies remain limited, thereby curbing addressable demand for incident-response retainers and breach-forensics engagements that insurers typically require.

Power-supply instability

Frequent grid outages inflate the total cost of ownership for on-premise appliances because organisations must invest in diesel generators and additional cooling to keep security operations centres online. SMEs in secondary cities often downsize or defer planned deployments. Although cloud solutions sidestep this barrier, local data-centres still rely on backup power, leaving the constraint only partially mitigated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Extend Value Beyond Technology

Services collectively accelerate at a 17.20% CAGR, outstripping the wider Nigeria cybersecurity market. Banks and insurers sign multi-year security-operations-centre outsourcing contracts to align with the Cybercrime Act’s 0.5% cybersecurity levy on electronic transfers, thereby moving from capital expenditure to predictable operational costs. Demand also grows for privacy-impact assessments and remediation road-maps that demonstrate NDPA compliance during regulator audits.

Technology solutions retain 67.60% revenue share, anchored by network firewalls, secure web gateways, and cloud-access security brokers. Yet margin pressure rises as hardware refresh cycles lengthen and open-source tools narrow functional gaps. Vendors bundling post-deployment tuning and threat-hunting services capture stickier revenue streams. Application security adoption gains momentum as DevSecOps principles mainstream within indigenous fintech and health-tech development teams.

By Deployment Mode: Cloud Intensity Shapes Procurement

Cloud-delivered controls represent 57.20% of 2025 spending and expand 20.40% annually, reinforcing the Nigeria cybersecurity market’s pivot toward elastic, subscription-based defences. Multinational payment processors, start-ups, and public agencies routinely select cloud-native SEIM, email-security, and zero-trust SASE platforms to minimise upfront expenditure and sidestep unreliable power grids.

On-premise solutions, now 42.80% of expenditure, linger in utilities and defence where latency, data-sovereignty, or air-gap mandates override cost advantages. The hybrid model gains favour: encryption keys and sensitive datasets remain in local Tier-III facilities, while behavioural analytics engines run in hyperscale environments, ensuring state-imposed residency rules are met without hampering analytic depth.

By End-user Enterprise Size: SMEs Fuel Next-Wave Expansion

Large organisations maintain control of 60.70% spending through integrated security architectures spanning headquarters, branch offices, and OT environments. Compliance reporting dashboards consolidate metrics for board-level visibility, reinforcing vendor lock-in to established suites.

SMEs, however, are forecast to grow at 18.60% CAGR, injecting dynamism into the Nigeria cybersecurity market. Turn-key bundles that combine endpoint detection, secure cloud storage, and 24×7 monitoring resonate with resource-constrained businesses. Fintech incubation hubs in Yaba and Victoria Island partner with MSSPs to embed security-by-design into minimum viable products, lowering future remediation costs and raising the baseline security posture across the start-up ecosystem.

By End-user Industry: Healthcare Accelerates

BFSI retains the highest share at 29.20%, driven by zero-trust adoption, PSD2-like open-banking frameworks, and real-time fraud prevention mandates. Enhanced transaction-charge-back rules push banks toward AI-enabled behavioural biometrics and risk-scoring engines that cut false positives and operational losses.

Healthcare posts a 21.90% CAGR as electronic health-record roll-outs, telemedicine, and IoMT devices expand. Hospitals procure immutable cloud backups and micro-segmentation to ensure patient-care continuity amid ransomware spikes. Data-residency laws oblige clinics to store biometrics within national borders, stimulating local-cloud investment. Energy, telecom, and retail follow, each embedding vertical-specific compliance overlays that shape solution design.

Geography Analysis

Lagos and Abuja jointly account for over 70% of Nigeria cybersecurity market spending, underpinned by data-centre density, fintech clusters, and proximity to regulators. Early 5G availability enables low-latency edge services, compelling telcos to secure distributed core and MEC nodes through AI-driven anomaly detection. Venture-backed start-ups co-locate within these hubs to access talent, funding, and accelerator programs.

The Niger Delta forms a specialised sub-market anchored in OT-security for oil-producing installations. Ownership transitions following divestments by global oil majors have introduced control-system visibility gaps; operators therefore prioritise passive network-monitoring and threat-intelligence feeds tailored to ICS protocols. Local-content rules further encourage procurement from domestic MSSPs versed in regional militant threat profiles.

Secondary cities such as Kano, Enugu, and Ibadan trail in adoption due to limited broadband, unstable electricity, and scarce cybersecurity curricula. The National Information Technology Development Agency’s plan to open research centres across all six geopolitical zones aims to reduce this digital divide, fostering local innovation pipelines and workforce development. Over the forecast horizon, improved fibre backbones and solar-powered micro-data-centres are expected to lift baseline readiness, gradually broadening the Nigeria cybersecurity market’s geographic dispersion.

Competitive Landscape

The vendor ecosystem blends multinational giants and agile local specialists. Microsoft Azure Sentinel, Cisco SecureX, and IBM QRadar dominate enterprise SIEM bids, leveraging global threat-intelligence and large partner networks. Yet localisation gaps in regulatory templates and NIN/BVN integration leave openings for Digital Encode and CyberSOC Africa, whose consultants craft compliance documentation aligned to NDPA and sector-specific guidelines.

Strategic alliances proliferate: Fortinet partners with local telcos to bundle SASE into SD-WAN offerings for SMEs, while AWS collaborates with training academies to certify cloud-security architects, mitigating talent bottlenecks. Service providers pivot to outcome-based pricing, assuring mean-time-to-detect metrics rather than selling hourly man-days.

Competitive intensity peaks in payments security, where startups offer AI-driven behavioural analytics at subscription fees suited to neo-banks and mobile-money operators. High churn risk drives both global and domestic vendors to invest in customer-success teams, regional SOC expansions, and co-innovation labs that produce threat-feeds specific to local dialect phishing lures.

Nigeria Cybersecurity Industry Leaders

IBM Corporation

Microsoft Corporation

Cisco Systems Inc.

Check Point Software Tech. Ltd.

Palo Alto Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Seamfix secured USD 4.5 million from Alitheia IDF to expand digital-identity services across Africa, enhancing Nigeria’s application-security and identity-management landscape.

- March 2024: Youverify raised USD 2.5 million to strengthen anti-money-laundering compliance platforms for Nigerian banks and fintechs.

- May 2024: The Central Bank introduced a 0.5% cybersecurity levy on electronic transfers covering GSM operators, ISPs, banks, insurers, and the Nigerian Stock Exchange to fund national cyber-defence programs.

- December 2024: The Nigeria Data Protection Commission intensified action against identity theft as NIN issuance hit 115 million, underscoring heightened safeguards for national identity databases.

Nigeria Cybersecurity Market Report Scope

The Nigerian cybersecurity market's scope encompasses revenues derived from solutions and services utilized across end-user industries. The analysis draws from a blend of secondary research and primary sources, providing a comprehensive view of the market. It also delves into the key drivers and restraints shaping its growth trajectory.

The Nigeria cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the projected size of the Nigeria cybersecurity market by 2031?

The Nigeria cybersecurity market size is expected to reach USD 414.92 million by 2031, growing at a 10.32% CAGR.

Which deployment mode is growing the fastest?

Cloud-delivered security leads with a 20.40% CAGR, reflecting strong uptake across public and private sectors.

Why is healthcare the fastest-growing vertical?

Rapid digitisation of patient records and stricter data-privacy oversight are driving healthcare to a 21.90% CAGR, the highest among end-user industries.

How do cash-less policies influence cybersecurity spending?

Mandatory BVN/NIN linkage and rising fraud losses force banks to enhance payment-security architectures, adding roughly 2.1 percentage points to market CAGR.

Page last updated on: