Finland Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

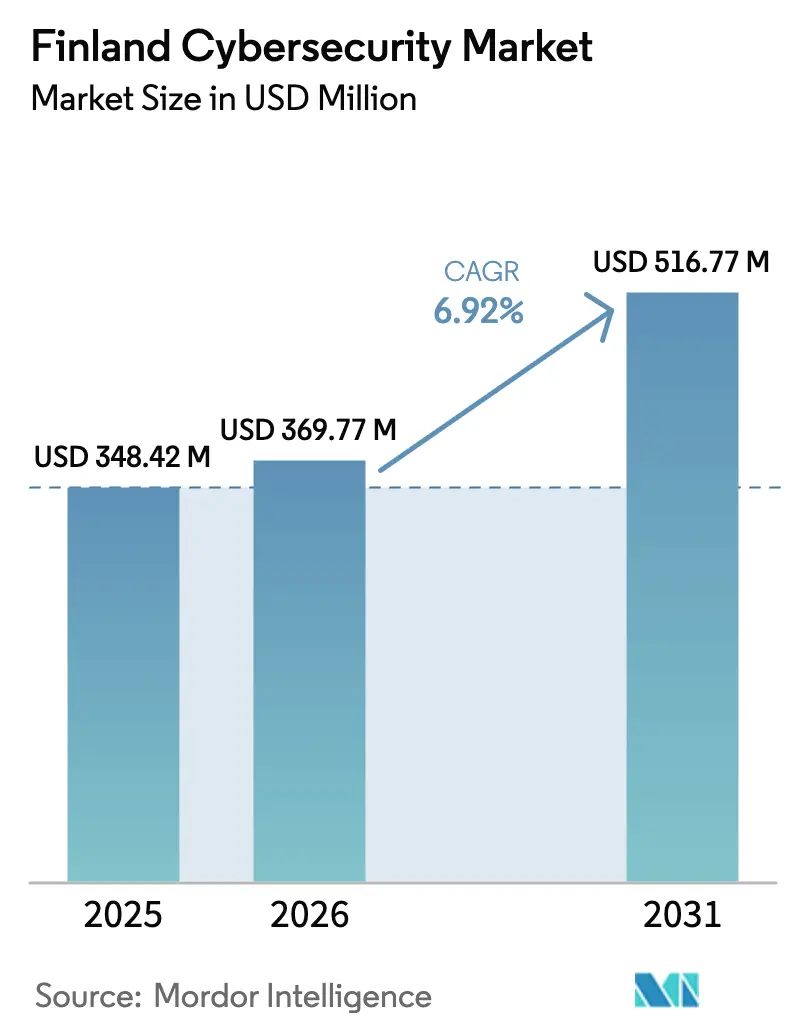

| Base Year Market Size (2025) | USD 348.42 Million |

| Market Size (2026) | USD 369.77 Million |

| Market Size (2031) | USD 516.77 Million |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Cybersecurity Market Analysis by Mordor Intelligence

The Finland cybersecurity market size is projected to expand from USD 348.42 million in 2025 and USD 369.77 million in 2026 to USD 516.77 million by 2031, registering a CAGR of 6.92% between 2026 to 2031. The Finland cybersecurity market is shifting from reactive defenses toward proactive resilience as NATO obligations, NIS2 compliance, and rapid digitization of public services converge. Large-scale funding directed at critical-infrastructure protection, combined with a 99% online-banking penetration rate, amplifies demand for fraud-prevention, identity governance, and managed detection capabilities. Service providers gain traction because a shortfall of 3,000 Finnish-speaking analysts constrains in-house security operations, while cloud-centred architectures expand the need for unified security across multi-cloud estates. Competition remains moderate, with global vendors leveraging channel alliances and Finnish specialists differentiating through local language support and regulatory expertise.

Key Report Takeaways

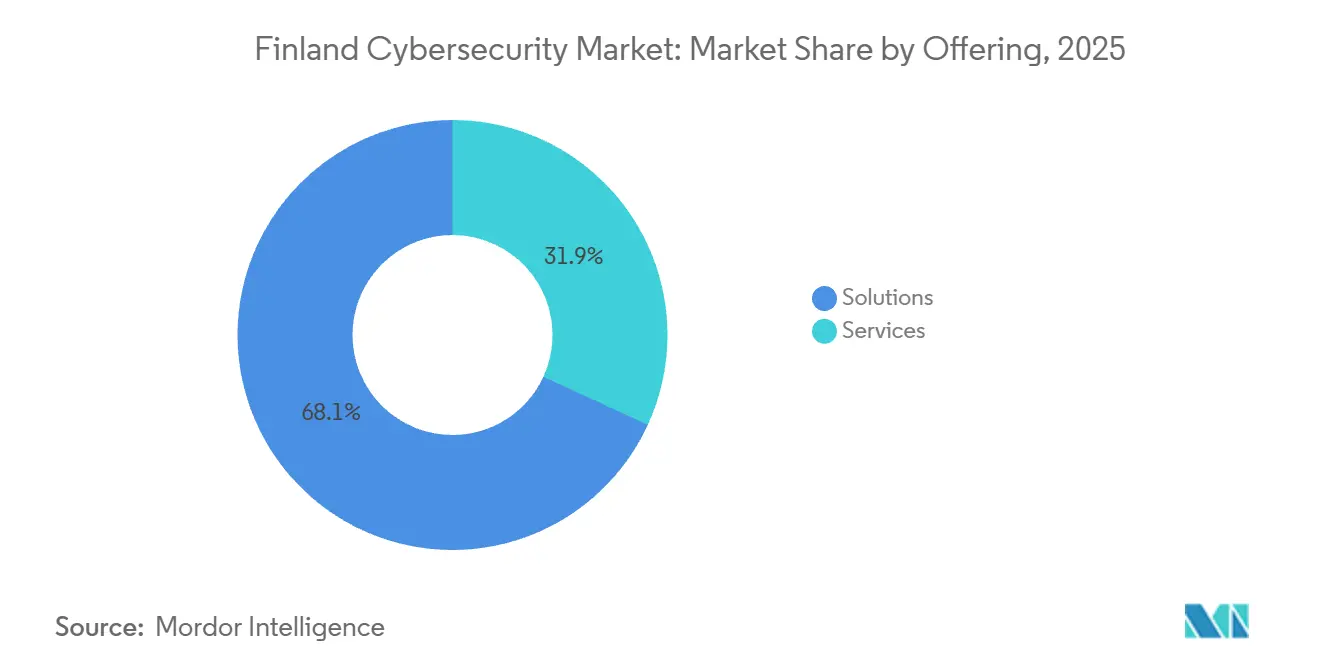

- By offering, solutions led with 68.14% market share in 2025, whereas services are advancing at a 7.54% CAGR through 2031, narrowing the gap as enterprises outsource threat hunting and incident response.

- By deployment mode, on-premises retained 55.73% of the Finland cybersecurity market share in 2025, yet cloud adoption is expanding at a 7.63% CAGR through 2031 as multi-cloud strategies gain favor.

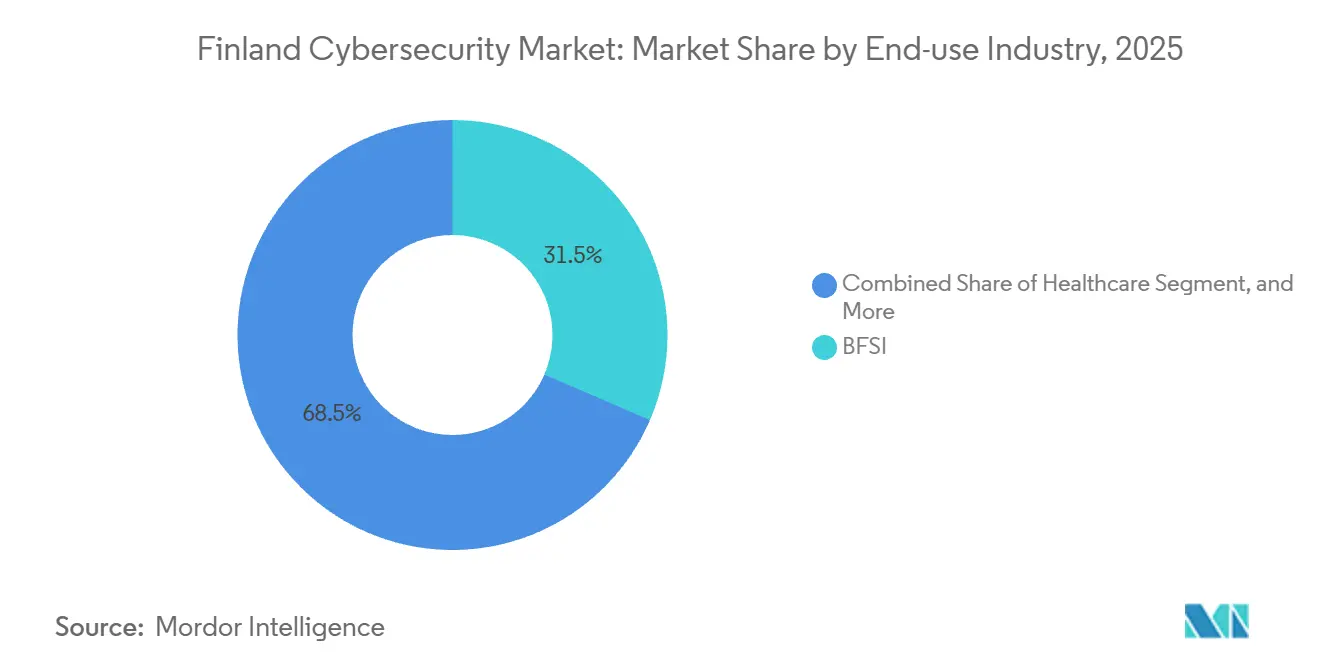

- By end-use industry, banking, financial services, and insurance captured 31.47% of the market share in 2025, while healthcare is projected to post the fastest 8.13% CAGR through 2031, driven by zero-trust and encryption upgrades.

- By enterprise size, large organizations accounted for 61.27% of the Finland cybersecurity market in 2025, but small and medium enterprises posted a higher 7.87% CAGR to 2031 after losing former regulatory exemptions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Finland Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Digitalization of Finnish Public Services Expanding Attack Surface | +1.8% | National, concentrated in Helsinki, Espoo, Tampere, Turku | Medium term (2-4 years) |

| Accelerated 5G and Industrial IoT Roll-outs in Manufacturing Clusters | +1.5% | National, industrial clusters in Oulu, Vaasa, Lahti | Medium term (2-4 years) |

| Enforcement of EU NIS2 and Finland Cyber Security Strategy 2024-2035 | +2.1% | National, all sectors under NIS2 scope | Short term (≤ 2 years) |

| Finland's NATO Accession Boosting Critical-Infrastructure Protection Budgets | +1.3% | National, emphasis on energy, telecom, transport | Long term (≥ 4 years) |

| High Online-Banking and Mobile-Payment Use Driving Advanced Fraud-Prevention Demand | +1.0% | National, urban banking centers | Short term (≤ 2 years) |

| Active Local Cyber-Innovation Ecosystem Catalyzing Early Adoption | +0.7% | National, startup hubs in Helsinki, Espoo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enforcement of EU NIS2 and Finland Cyber Security Strategy 2024-2035

Finland transposed NIS2 on 8 April 2025, placing roughly 5,000 entities under 24-hour incident-reporting rules and fines topping EUR 10 million, a catalyst for security-information and event-management procurement.[1]Traficom, “Finland’s New Cybersecurity Act Enters Force 8 April 2025,” traficom.fi Sustained EUR 4.7 million (USD 5.3 million) annual funding now supports national threat-sharing portals that reached 1,200 registrants by early 2025.[2]Bank of Finland, “Finnish Payment Habits 2024,” suomenpankki.fi Demand therefore skews toward integrated suites bundling vulnerability scanning, penetration testing, and compliance dashboards, especially for smaller operators lacking internal expertise.

Robust Digitalization of Finnish Public Services Expanding Attack Surface

Municipalities deliver 87% of tax filings and 92% of healthcare bookings online, exposing shared identity platforms to attack.[3]Statistics Finland, “Official Statistics of Finland,” stat.fi The 2024 breach that affected 300,000 Helsinki residents precipitated a surge in identity-and-access-management roll-outs and prompted EUR 2 million central funding for municipal defenses. Thousands of IoT sensors deployed for traffic and waste management extend risk to the network edge, further elevating managed detection and response demand among public agencies.

Accelerated 5G and Industrial IoT Roll-outs in Manufacturing Clusters

Finland reached 99.9% population 5G coverage in 2024. Private 5G networks on factory floors introduce software-defined radio elements that require continual firmware validation. Legacy controllers in pulp and paper mills lack the power for endpoint agents, steering procurement toward passive OT-network-monitoring tools that interpret industrial protocols without touching production systems.

Finland's NATO Accession Boosting Critical-Infrastructure Protection Budgets

NATO membership drove EUR 158 million (USD 178.5 million) in 2025 allocations for cyber-hardening energy, telecom, and transport infrastructure. Alliance standards accelerate deployment of orchestration platforms able to integrate with Cyber Rapid Reaction Teams, while energy operators add anomaly-detection modules that spot deviations in grid telemetry. Telecom carriers collaborate with the Finnish Defence Forces to fortify mobile networks, extending benefits to civilian resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Finnish-Speaking Cyber Talent Raising MSSP Labor Costs | -1.2% | National, most acute in Helsinki, Tampere, Oulu | Medium term (2-4 years) |

| Consolidated Telecom Market Limiting Network-Security Vendor Diversity | -0.8% | National, all sectors reliant on carrier infrastructure | Long term (≥ 4 years) |

| Legacy OT Systems in Pulp and Paper Plants Hindering Modern Security Roll-outs | -0.6% | Regional, Oulu, Vaasa, Lahti industrial zones | Long term (≥ 4 years) |

| Budget Constraints Among Municipalities Outside Helsinki Delaying Cloud-Security Moves | -0.5% | Regional, municipalities under 50,000 population | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Finnish-Speaking Cyber Talent Raising MSSP Labor Costs

A deficit of about 3,000 bilingual experts inflates managed-service payrolls 20-30%, compressing margins and prompting automation investments. Multinationals recruiting locally deepen the shortfall for indigenous MSSPs, while university graduates will not close the gap for several years. Elevated consulting fees push SMEs toward subscription-based platforms that incorporate machine-learning-driven detection and response.

Consolidated Telecom Market Limiting Network-Security Vendor Diversity

Three national carriers command 95% of subscribers, creating high integration hurdles for software-defined perimeter solutions. Vendor lock-in with Nokia-and-Ericsson bundles slows 5G standalone core features such as network slicing. Smaller security vendors, therefore, face protracted sales cycles and limited test-bed access, which restrains innovation in mobile-edge protections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Expand as Skills Remain Scarce

Solutions contributed 68.14% of the Finland cybersecurity market in 2025, reflecting historical reliance on perpetual software and on-premise appliances. Services, however, are on track to outgrow the overall Finland cybersecurity market at a 7.54% CAGR to 2031 as firms without internal analysts outsource 24/7 monitoring. Managed detection and response packages that bundle endpoint telemetry, threat intelligence, and incident handling appeal to mid-tier companies, while professional services peak during NIS2 audits. The combined weight of talent scarcity and regulatory deadlines is tilting procurement toward subscription models that shift capital outlays to operating expenses, positioning service-centric vendors for sustained expansion within the Finland cybersecurity market size.

Sustained demand for advisory engagements around zero-trust architecture, penetration testing, and cloud-migration security stretches the consultant pool, allowing qualified providers to command premium day rates. Simultaneously, commoditization of antivirus and traditional firewalls compresses standalone product margins, accelerating mergers that combine endpoint, network, and email defenses into unified consoles. This consolidation further supports services revenue because enterprises increasingly seek a single partner to integrate tools, run tabletop exercises, and supply continuous improvement roadmaps linked to board-level risk metrics within the Finland cybersecurity market.

By Deployment Mode: Cloud Gains Ground Despite Data-Residency Scrutiny

On-premise assets remained dominant in 2025, accounting for 55.73% of the Finland cybersecurity market share among highly regulated banks and hospitals. Cloud deployments, advancing at 7.63% CAGR to 2031, benefit from government cloud strategies that insist on EU-based data centers and from growing trust in vendor certifications such as ISO 27001. Multi-cloud estates drive demand for cloud-security posture-management dashboards that surface misconfigurations and excessive entitlements across AWS, Azure, and Google Cloud, ensuring consistent policies as workloads shift.

Hybrid patterns persist where latency or sovereignty dictates local processing, yet operational burdens hardware refreshes, patch cycles, and capacity planning, tilt total-cost-of-ownership calculations in favor of cloud-native controls. Because NIS2 now covers cloud providers directly, contracts increasingly codify incident-notification requirements, pushing hyperscalers to harden services and share forensics. As more Finnish entities adopt SaaS productivity suites, cloud access security brokers are becoming baseline defenses, accelerating the Finland cybersecurity market adoption curve for cloud-first security.

By End-Use Industry: Healthcare Leads in Growth After High-Profile Breach

Financial institutions absorbed 31.47% of market share in 2025, driven by DORA mandates for resilience testing and granular third-party oversight. Healthcare’s 8.13% forecast CAGR makes it the growth frontrunner as providers install encrypted repositories and zero-trust segmentation following the Vastaamo psychotherapy incident that drew a EUR 0.608 million (USD 0.69 million) penalty. New electronic-health-record roll-outs incorporate privileged-access controls and behavioral analytics that flag anomalous record pulls.

Telecom operators focus on defending 5G cores and signaling protocols from disruption, while industrial producers retrofit aging programmable logic controllers through passive monitoring of Modbus and Profinet traffic. Retail faces rising bot attacks and payment fraud, leading to expanded application-security budgets. Energy companies adopt anomaly detection to safeguard cross-border electricity flows aligned with NATO cyber-pledge requirements, underpinning specialized operational-technology spending within the Finland cybersecurity market size.

By Enterprise Size: SMEs Accelerate Under Regulatory Pressure

Large corporations held 61.27% of the market share in 2025, supported by mature security operations centers and threat intelligence teams. These teams correlate telemetry across on-premises, cloud, and OT domains. Small and medium enterprises are, however, projected to expand faster at 7.87% CAGR, their Finland cybersecurity market share rising as NIS2 obliges even micro-scale healthcare providers and digital platforms to meet strict controls.

SMEs gravitate toward integrated, subscription-based suites that offer endpoint, email, and vulnerability management via a single portal, easing administrative overhead. Managed security providers tailor tiered offerings that layer from basic log monitoring up to incident response, converting fragmented demand into predictable annuities. Automation alleviates the human resource deficit that particularly hampers SMEs, while vendor consolidation reduces licensing complexity, further narrowing the capability gap between firm sizes.

Geography Analysis

Helsinki, Espoo, and Vantaa constitute Finland’s economic hub and command nearly half of national cybersecurity expenditure. Concentrated headquarters of banks, telecom carriers, and government ministries drive premium demand for threat intelligence, security orchestration, and compliance management. The presence of Aalto University and VTT fosters research collaborations that pilot AI-driven anomaly detection and quantum-safe encryption before countrywide roll-outs. Following the 2024 municipal breach, identity governance and municipal security-operations outsourcing surged, reinforcing capital-region outlays.

Regional centers Tampere, Turku, and Oulu exhibit accelerating adoption. Oulu’s telecom legacy sustains network-security innovation for private 5G; Tampere’s machinery producers procure passive OT-monitoring appliances to secure robotic assembly lines; Turku’s maritime cluster implements vessel-navigation safeguards that align with global maritime cyber codes. Nevertheless, municipalities below 50,000 inhabitants defer cloud-security upgrades due to tight budgets, a gap the central government targets through shared situational-awareness platforms and pooled incident-response resources.

Nordic integration extends Finland’s cybersecurity posture beyond borders. Joint Nordic-Baltic exercises refine collective defense scenarios, and the cross-border Vipps MobilePay platform obliges harmonized incident-handling protocols. EU directives and NATO drill participation ensure that Finnish solutions carry interoperability features, compelling vendors to certify products against multiple supranational frameworks, a distinct procurement criterion across the Finland cybersecurity market.

Competitive Landscape

Finland’s cybersecurity arena remains moderately fragmented, with global giants such as Microsoft, Cisco, Palo Alto Networks, and Fortinet leveraging multi-layer portfolios and reseller channels with Elisa, Telia, and DNA. Indigenous specialists WithSecure, SSH Communications Security, and Hoxhunt succeed through Finnish-language interfaces, deep regulatory insight, and culturally tuned user-awareness programs. WithSecure’s Elements platform bundles endpoint detection, vulnerability management, and threat intelligence under a single license, appealing to mid-market customers seeking reduced supplier sprawl. Hoxhunt’s behavior-based phishing simulation targets the enduring human factor, while SSH Communications Security exploits its secure-shell heritage to promote zero-trust privileged-access controls.

Managed security services form a battleground where talent scarcity caps analyst growth and boosts churn risk. Providers differentiate on mean-time-to-detect, bespoke threat hunting, and integration depth with Traficom portals. Rising demand for operational-technology security opens white space, with few players mastering industrial protocols and safety-critical uptime requirements. Startups that apply machine learning to automate correlation and response lower analyst workloads, positioning themselves as enablers for both SMEs and resource-strained MSSPs. Conservative Finnish buyers favor proven suppliers, slowing but not blocking adoption of confidential computing and homomorphic encryption as those technologies mature inside the Finland cybersecurity market.

The market’s pricing dynamics reinforce this balance. Basic antivirus and perimeter firewalls are increasingly bundled into broader endpoint or network platforms, limiting margin growth and prompting vendors to differentiate through value-added services such as automated incident response or sector-specific threat intelligence. Channel alliances with Elisa, Telia, and DNA remain decisive because most Finnish enterprises purchase cyber solutions as part of integrated connectivity or cloud packages, giving carriers disproportionate influence over shortlists. Global suppliers are stepping up local investments—Microsoft opened a Helsinki security co-innovation hub in 2025, while Palo Alto Networks expanded Finnish-language support in 2026 to secure government and regulated-industry contracts that stipulate domestic service desks. Looking ahead, consolidation is poised to accelerate; OT-security specialists, phishing-awareness startups, and compliance-automation vendors represent attractive acquisition targets for larger players eager to deepen domain coverage and secure scarce bilingual talent without lengthy recruitment cycles.

Finland Cybersecurity Industry Leaders

IBM Corporation

Microsoft Corporation

Fortinet Inc.

Check Point Software Technologies

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Finnish government’s permanent EUR 4.7 million (USD 5.3 million) annual cyber-budget uplift became effective, extending Hyöky and Havaro coverage to thousands of NIS2-regulated entities.

- April 2025: Finland’s updated Cybersecurity Act enforcing NIS2 obligations took effect, imposing 24-hour incident reporting and large monetary penalties.

- March 2025: A supplementary allocation of EUR 158 million (USD 178.5 million) was approved to meet NATO cyber-resilience requirements across energy, telecom, and transport infrastructure.

- February 2025: Traficom received an earmarked EUR 2 million (USD 2.3 million) to bolster municipal digital-service defenses via centralized threat-sharing portals.

Finland Cybersecurity Market Report Scope

The Finland cybersecurity market's scope encompasses the revenues derived from solutions and services utilized across end-user industries. The analysis draws from a blend of secondary research and primary sources, providing a comprehensive view of the market. The market also covers the major factors impacting its growth in terms of drivers and restraints.

The Finland Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace Military and Defense, and Other End-use Industries), and End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| Endpoint Security | |

| Services | Professional Services |

| Managed Services |

| On-Premise |

| Cloud |

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| Endpoint Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is Finland’s cybersecurity spending expected to be by 2031?

Spending is projected to reach USD 0.52 billion by 2031, reflecting a 6.92% CAGR from 2026 to 2031.

Which user group is expanding fastest in adopting cyber defenses across Finland?

Small and medium enterprises show the highest growth, advancing at a 7.87% CAGR through 2031 as NIS2 removes earlier exemptions.

Why is healthcare investing heavily in new cyber controls in Finland?

The 2020 Vastaamo breach that exposed 33,000 patient records prompted zero-trust segmentation, encrypted repositories, and privileged-access management, driving an 8.13% CAGR in healthcare security budgets.

What main factor drives organizations to outsource security operations in Finland?

A shortage of about 3,000 Finnish-speaking analysts inflates labor costs and compels firms to rely on managed detection and response services.

How does NATO membership influence Finland’s cyber priorities?

Alliance obligations spurred a EUR 158 million (USD 178.5 million) allocation in 2025 for hardening energy, telecom, and transport networks and integrating with NATO cyber-defense exercises.

Which deployment approach is gaining momentum despite data-residency concerns?

Cloud-based security is expanding at 7.63% CAGR to 2031 as multi-cloud strategies spread and EU data-center options satisfy sovereignty requirements.

Page last updated on: