Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

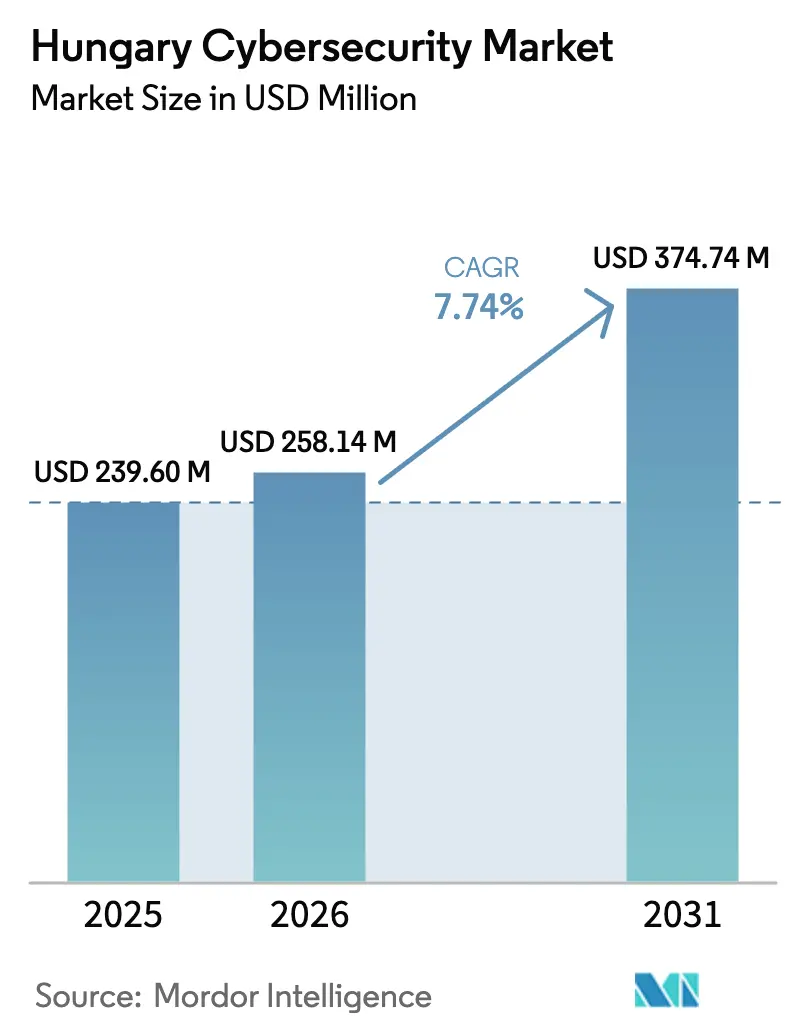

| Base Year Market Size (2025) | USD 239.6 Million |

| Market Size (2026) | USD 258.14 Million |

| Market Size (2031) | USD 374.74 Million |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Cybersecurity Market Analysis by Mordor Intelligence

The Hungary cybersecurity market size is expected to grow from USD 239.6 million in 2025 to USD 258.14 million in 2026 and is forecast to reach USD 374.74 million by 2031 at 7.74% CAGR over 2026-2031. The expansion reflects broad-based digitalisation, zero-trust mandates under the Digital Success Programme 2030, and Budapest’s ascent as a regional hyperscale data-centre hub. Growing ransomware activity, evolving EU regulations such as NIS2 and DORA, and rising instant-payments volumes are pushing organisations to replace legacy defences with cloud-native, AI-driven security stacks. Meanwhile, persistent skills shortages elevate demand for managed security services, and government funding via the National Research, Development and Innovation Fund (NRDI) sustains local innovation. Competitive intensity remains moderate because domestic specialists such as SEON and Tresorit coexist with multinationals like IBM and Microsoft, yet no single provider controls a dominant Hungary cybersecurity market share.

Key Report Takeaways

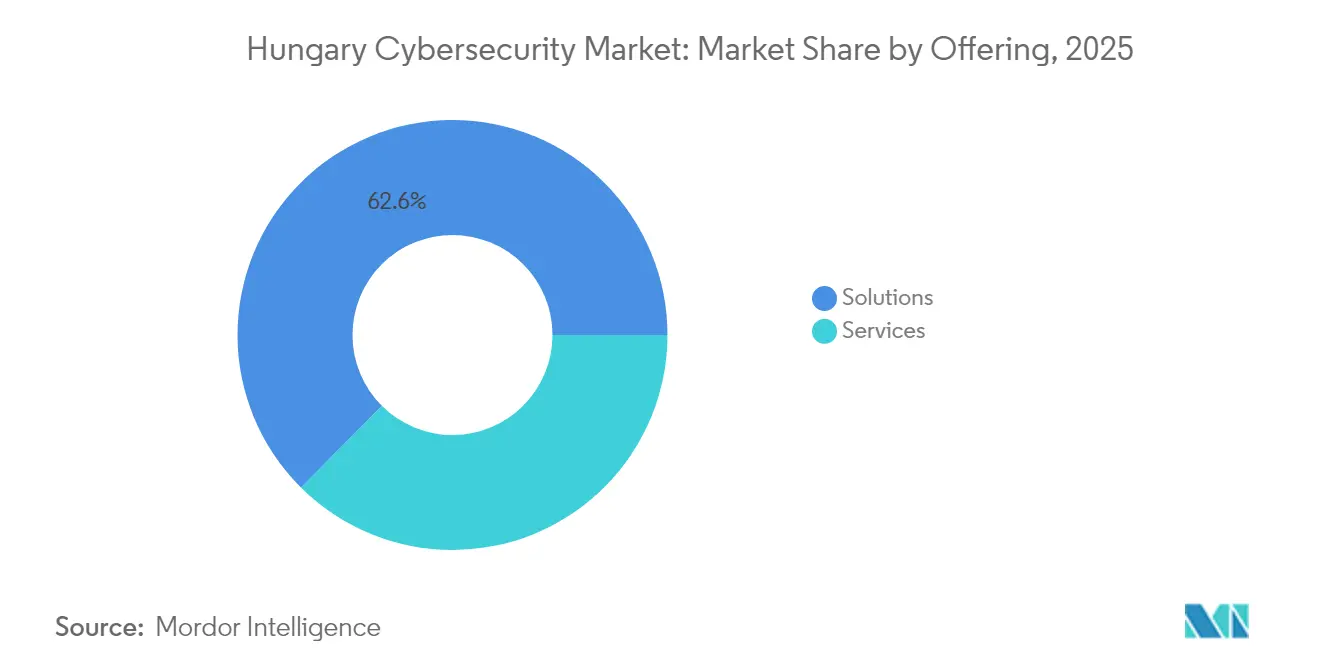

- By offering, Solutions led with 62.55% revenue share in 2025, while Services are projected to register the fastest 9.12% CAGR to 2031.

- By deployment mode, on-premise retained 58.95% of the Hungary cybersecurity market size in 2025; cloud implementations are set to record an 10.78% CAGR through 2031.

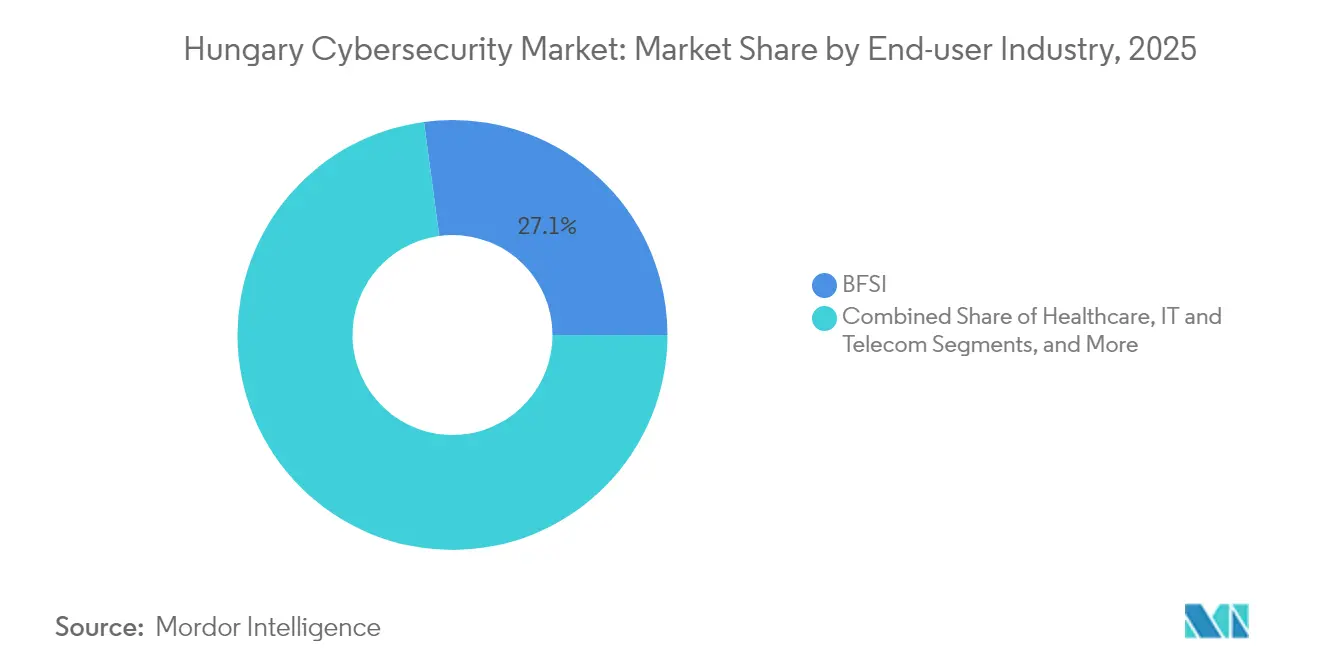

- By end-user industry, BFSI captured 27.12% of the Hungary cybersecurity market share in 2025; Healthcare is poised for a 10.15% CAGR, the quickest among all verticals.

- By end-user enterprise size, large enterprises held 67.74% of 2025 revenue, whereas the SME segment is forecast to expand at a 10.46% CAGR as mandatory audits drive uptake.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hungary Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budapest Hyperscale and Colocation Boom Accelerating Cloud-Native Security Demand | +2.1% | Budapest metropolitan area, spillover to Central Hungary | Medium term (2-4 years) |

| Surge in Phishing and Ransomware Attacks on Hungarian SMEs | +1.8% | National, with concentration in Budapest and industrial regions | Short term (≤ 2 years) |

| Digital Success Programme 2030 Driving e-Government Zero-Trust Adoption | +1.5% | National, with priority implementation in government sectors | Long term (≥ 4 years) |

| Instant Payments and E-commerce Growth Raising PSD2/SCA and PCI-DSS Compliance Spend | +1.2% | National, with emphasis on Budapest financial district | Medium term (2-4 years) |

| NIS2 Directive Implementation Mandating Cybersecurity Audits | +0.9% | National, affecting all qualifying enterprises | Short term (≤ 2 years) |

| DORA Regulation Enhancing Financial Sector IT Resilience Requirements | +0.7% | National, concentrated in BFSI sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budapest Hyperscale and Colocation Boom Accelerating Cloud-Native Security Demand

A stream of hyperscale builds around Budapest is reshaping buyer preferences toward cloud-centric architectures that require elastic identity, network and data-protection layers. Each new facility spawns an ecosystem of colocated tenants whose regulatory obligations and multi-cloud footprints translate into higher outlays for managed detection and response, security automation and zero-trust gateways. Deep fibre backbones and Magyar Telekom’s 80% gigabit coverage enable low-latency security controls that scale with workload bursts.

Surge in Phishing and Ransomware Attacks on Hungarian SMEs

Ransomware operators increasingly target Hungary’s 690,000 SMEs, exploiting limited budgets and uneven cyber-hygiene. A series of double-extortion incidents in manufacturing and municipal networks has heightened board-level focus, prompting accelerated roll-outs of endpoint detection, backup immutability and user-awareness programmes. Despite the urgency, resource constraints keep demand skewed toward pay-as-you-go managed services, sustaining a healthy pipeline for MSSPs.

Digital Success Programme 2030 Driving e-Government Zero-Trust Adoption

The state’s flagship programme requires ministries and regional offices to harden identity, privilege and data flows under a zero-trust blueprint. Budget streams earmarked within the Recovery and Resilience Plan finance upgrades ranging from multi-factor authentication to continuous monitoring. Private-sector suppliers must now align with these procurement baselines, effectively expanding the Hungary cybersecurity market beyond the public realm.

Instant Payments and E-commerce Growth Raising PSD2/SCA and PCI-DSS Compliance Spend

Online retail reached USD 2.75 billion in 2023, and merchants processing real-time transactions must satisfy PSD2 strong-customer-authentication and PCI-DSS rules. Fraud analytics, tokenisation and behavioural biometrics thus top investment agendas for banks and marketplaces, adding incremental tailwinds to the Hungary cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified SOC Analysts | -1.4% | National, acute in Budapest and regional centers | Long term (≥ 4 years) |

| Price Sensitivity among MSMEs Limiting Adoption of Enterprise-Grade Solutions | -1.1% | National, particularly affecting rural and smaller urban areas | Medium term (2-4 years) |

| Fragmented Regulation on Cross-border Data Flows Creating Procurement Delays | -0.8% | EU-wide, affecting multinational operations | Long term (≥ 4 years) |

| Limited Digital Skills Among Workforce Hampering Security Implementation | -0.6% | National, with regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified SOC Analysts

Hungary’s talent gap keeps salaries elevated and slows complex roll-outs, particularly for threat-hunting, forensics, and OT security. Enterprises respond by outsourcing monitoring and embracing AI-supported analytics that stretch scarce human bandwidth. Government-funded cyber-scholarships under the NRDI fund look helpful, yet will not plug the demand near term.

Price Sensitivity among MSMEs Limiting Adoption of Enterprise-Grade Solutions

Roughly 99% of Hungarian firms are SMEs; two-thirds still rely on freeware or consumer-grade tools. Capital constraints curb uptake of comprehensive suites, compelling vendors to strip feature sets or bundle offerings as subscription services. While cloud delivery lowers entry costs, concerns around data residency persist outside Budapest’s tech clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services gain momentum despite solutions dominance

Solutions commanded 62.55% of 2025 revenue, underpinned by network, application and cloud-security suites adopted by banks, telecom carriers and manufacturers. The Hungary cybersecurity market size for Services is, however, expanding faster at a 9.12% CAGR because enterprises struggling with labour shortages turn to consulting, integration and managed detection services. Vendors specialising in continuous compliance, penetration testing and incident response benefit most as NIS2 audit deadlines loom.

Growth pockets include identity-as-a-service and MDR subscriptions, which bundle 24×7 monitoring with automated containment. On the solutions side, workload-centric cloud firewalls and data-loss prevention tools outpace legacy perimeter defences. Demand for integrated-risk-management platforms is rising in financial services as firms prepare for DORA-mandated ICT controls.

By Deployment Mode: Cloud acceleration challenges on-premise dominance

On-premise systems retained 58.95% Hungary cybersecurity market share in 2025. Cloud-delivered controls are forecast to notch an 10.78% CAGR, aided by vendor commitments to local data centres that address sovereignty concerns and by Magyar Telekom’s network modernisation. The new cybersecurity law supplies certainty on cross-border processing, which compliance advisors previously flagged .

Many mid-tier manufacturers now keep sensitive OT data on-site but route analytics to SOC-as-a-service platforms hosted in Budapest hyperscale facilities. Financial institutions deploy cloud-based sandboxing and fraud analytics yet continue to run core transaction systems on domestic servers to satisfy Magyar Nemzeti Bank directives. This hybrid pattern is likely to define the Hungary cybersecurity market through 2031.

By End-user Industry: Healthcare digitisation drives fastest growth

BFSI generated 27.12% of 2025 outlays as card issuers and brokers invested in crypto-agility, transaction screening and DORA-aligned resilience testing. Healthcare, however, is poised for a 10.15% CAGR because the Electronic Health Service Space necessitates advanced identity governance and encryption. Budapest medical centres lead pilot deployments, while regional hospitals follow as connectivity improves.

Industrial firms are raising OT budgets following ransomware incidents that halted automotive lines. Energy utilities add anomaly-detection layers to meet critical-infrastructure norms. Retailers replatform for omnichannel fraud prevention as e-commerce expands. Government agencies remain steady adopters, driven by the zero-trust roadmap within Digital Success Programme 2030.

By End-user Enterprise Size: SMEs accelerate despite large-enterprise dominance

Large enterprises held 67.74% of 2025 revenue, whereas SMEs are forecast to grow at 10.46% CAGR thanks to NRDI-backed digitisation vouchers and mandatory NIS2 audits. The SME segment's growth is supported by the development of cost-effective security-as-a-service models that provide enterprise-level protection at accessible price points, addressing previous barriers related to budget constraints and technical complexity.

The enterprise size dynamic reflects broader market maturation, where large enterprises are transitioning from basic security implementations to advanced threat detection and response capabilities, while SMEs are moving from minimal protection to comprehensive security frameworks.

Geography Analysis

Budapest and its commuter belt generate roughly 40% of national spending, underpinned by dense BFSI clusters, tech start-ups and hyperscale data facilities. High fibre density enables SaaS adoption, while state ministries headquartered in the capital accelerate procurements tied to zero-trust rollouts. Colocation demand further broadens the Hungary cybersecurity market as resident cloud tenants require multi-layered defences.

Western border counties benefit from cross-border logistics and automotive plants, prompting investments in OT firewalls, industrial DMZs and IEC-62443 compliance frameworks. The Hungary cybersecurity market size for these regions is expected to edge up as tier-one suppliers tighten risk-sharing clauses. Central Hungary enjoys spill-over growth because of shared services centres that adopt cloud-first models aligned with Magyar Telekom’s 5G coverage.

Eastern and Southern regions still lag because SMEs cite budget and skill constraints; however, NRDI-funded accelerators in Debrecen and Szeged are catalysing cyber-start-up formation. Uniform NIS2 audit thresholds now oblige enterprises with 50+ staff to upgrade baseline controls, gradually harmonising demand curves nationwide.

Competitive Landscape

Magyar Telekom leverages its network footprint to bundle connectivity with DDoS scrubbing, SOC-as-a-service, and secure-access gateways, holding about 12% of the IT-services pool [2]Magyar Telekom, “Enterprise Security Services,” telekom.hu. Fraud-focused SEON has raised USD 107.7 million to expand AI-based risk APIs into regional neobanks. Tresorit secured USD 18 million to develop end-to-end encrypted collaboration tools tailored to GDPR-sensitive workflows[3]Tresorit, “Company Facts,” tresorit.com.

Global vendors IBM, Microsoft, Cisco, and Fortinet position AI-driven XDR and SASE portfolios for large-enterprise deals. Their partner ecosystems include SOC integrators Balasys and secure-coding platform Avatao, which supply niche training and code-assessment services. Proof of NIS2 and DORA conformity now acts as a procurement filter, granting early movers a measurable edge.

Consolidation is gradual; no merger has yet re-shaped the Hungary cybersecurity market in 2025, though managed-service specialists continue to acquire boutique pen-test firms to secure scarce talent. White-space opportunities persist in quantum-safe encryption, OT anomaly detection, and SME-oriented, pay-per-use security suites.

Hungary Cybersecurity Industry Leaders

IBM Corporation

Magyar Telekom / T-Systems Hungary

Seon Fraud Fighters

Cisco Systems, Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: HUB Cyber Security closed its share-swap acquisition of BlackSwan Technologies to expand AI-based secured data fabrics across EU financial institutions.

- January 2025: The Digital Operational Resilience Act (DORA) entered into force, assigning the Hungarian National Bank supervisory powers over ICT risk management.

- January 2025: Hungary’s new cybersecurity law, aligned with NIS2, mandated completion of external audits by 31 Dec 2025.

- November 2024: The national defence procurement agency suffered a USD 5 million ransom demand after an INC Ransomware breach.

Hungary Cybersecurity Market Report Scope

Cybersecurity solutions enable an organization to monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and phishing to maintain data confidentiality.

The Hungary cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Hungary cybersecurity market in 2026?

It is valued at USD 258.14 million and is projected to reach USD 374.74 million by 2031.

What CAGR is expected for Hungary’s cybersecurity spending through 2031?

The market is forecast to grow at a 7.74% CAGR over 2026-2031.

Which segment is expanding fastest within the Hungary cybersecurity market?

Services, especially managed security offerings, are set to post a 9.12% CAGR due to the national skills shortage.

Why is Healthcare a high-growth vertical for cybersecurity vendors in Hungary?

The Electronic Health Service Space digitisation requires advanced identity governance and data-protection controls, driving a 10.15% CAGR in healthcare spend.

Page last updated on: