Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

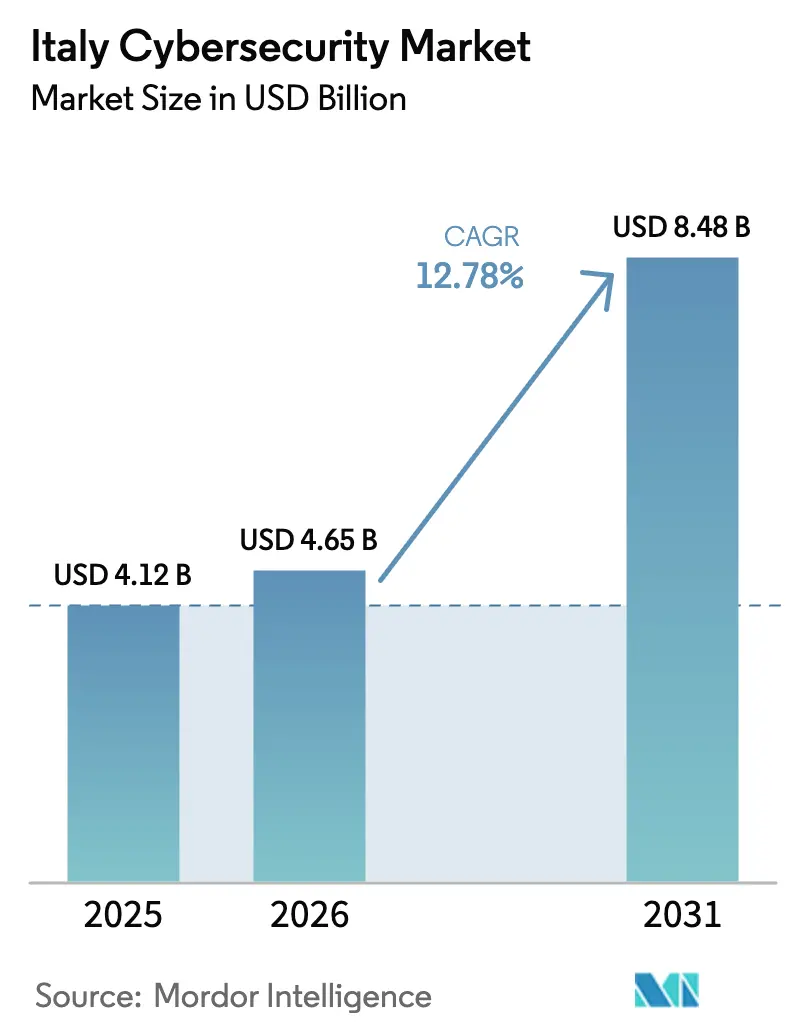

| Base Year Market Size (2025) | USD 4.12 Billion |

| Market Size (2026) | USD 4.65 Billion |

| Market Size (2031) | USD 8.48 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

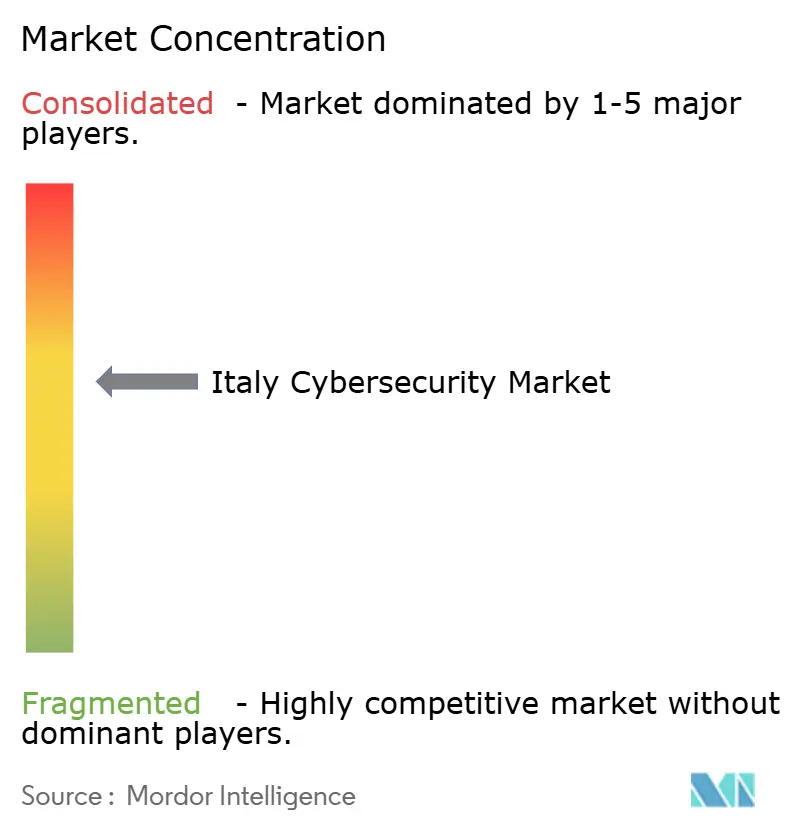

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Cybersecurity Market Analysis by Mordor Intelligence

The Italy cybersecurity market size was valued at USD 4.12 billion in 2025 and estimated to grow from USD 4.65 billion in 2026 to reach USD 8.48 billion by 2031, at a CAGR of 12.78% during the forecast period (2026-2031). Growth is led by compulsory compliance with EU laws such as the NIS2 Directive and the Digital Operational Resilience Act, together with USD 2.2 billion in public funding dedicated to national cyber-perimeter programs. [1]International Trade Administration, “Italy – Digital Economy,” trade.gov Rising ransomware attacks on operational technology, fast cloud adoption in Milan and Turin, and quantum-resistant encryption pilots are reshaping corporate investment road maps. Board-level attention has intensified as the manufacturing sector absorbed 70% of all industrial ransomware incidents in Q4 2024. Large enterprises still dominate spend, yet soaring SME demand, a deepening talent crunch, and state incentives for “Made-in-Italy” platforms are realigning the competitive field.

Key Report Takeaways

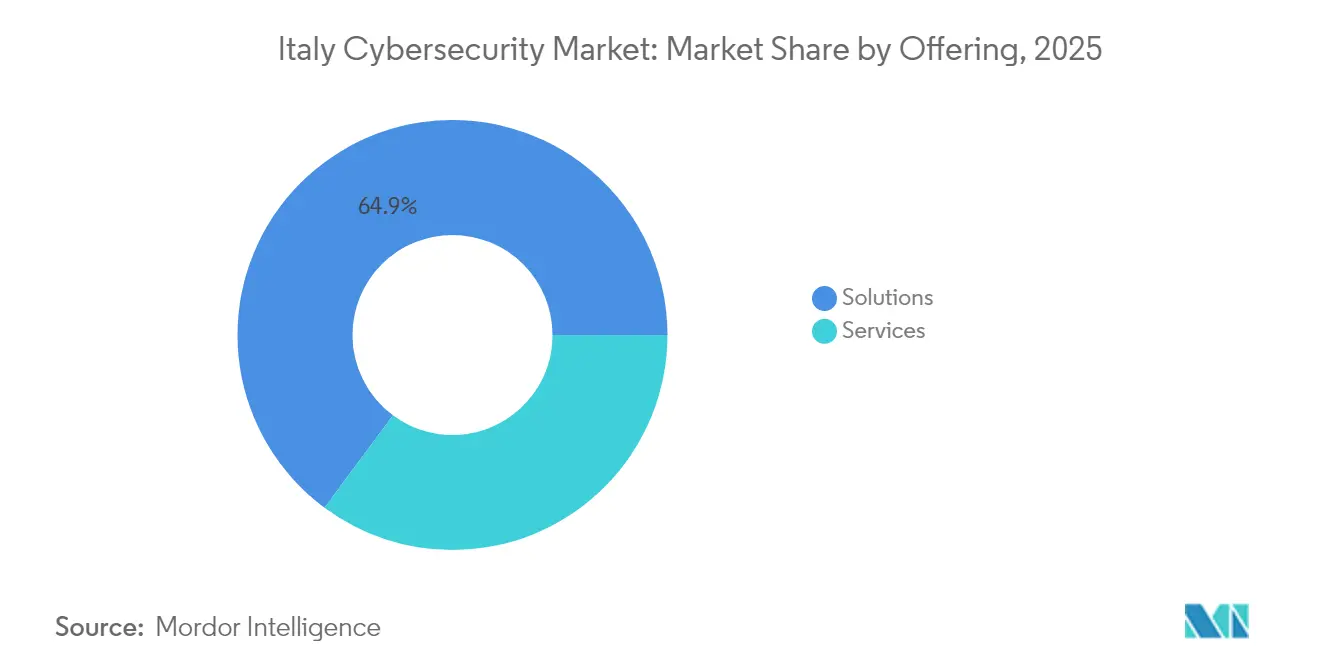

- By offering, solutions led with a 64.85% share in 2025, while services are forecast to grow at a 13.95% CAGR through 2031.

- By deployment mode, on-premise held 59.85% of Italy cybersecurity market share in 2025; cloud is projected to post an 17.55% CAGR to 2031.

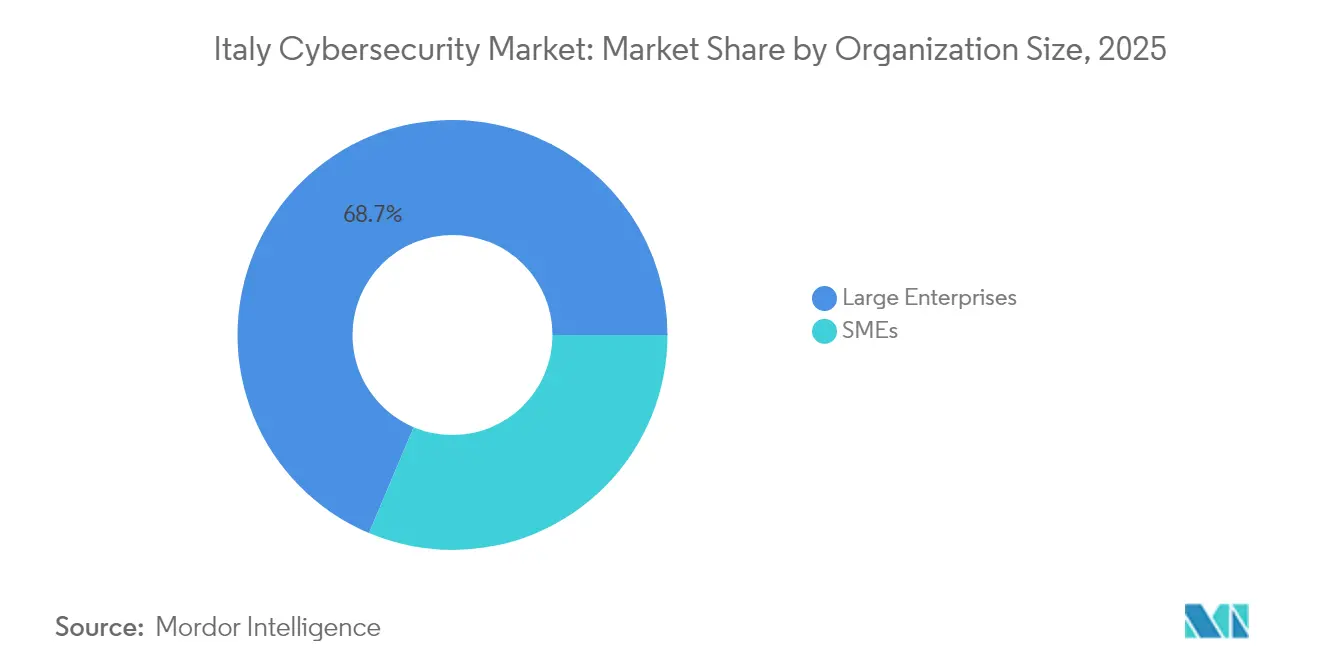

- By organization size, large enterprises commanded 68.65% of Italy cybersecurity market size in 2025; the SME segment is set to expand at 14.88% annually.

- By end user, BFSI led with 26.35% revenue share in 2025, while healthcare is advancing at a 15.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first public-service mandates accelerating national cyber-perimeter programs | +3.50% | Rome, Milan, Turin | Medium term (2-4 years) |

| Surge in ransomware attacks targeting industrial automation networks | +2.80% | Po Valley corridor | Short term (≤ 2 years) |

| EU NIS2 and DORA compliance deadlines driving budget re-allocation | +4.20% | Milan, Rome | Medium term (2-4 years) |

| Cloud-native start-up boom requiring SaaS security posture management | +1.80% | Milan, Turin | Medium term (2-4 years) |

| Growth of OT/ICS installations in the energy corridor | +1.20% | Po Valley | Long term (≥ 4 years) |

| Increased government incentives for “Made-in-Italy” cyber platforms | +1.40% | Rome, Milan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-First Public-Service Mandates Accelerating National Cyber-Perimeter Programs

Italy earmarked 27% of National Recovery and Resilience Plan resources for digital transition, including USD 2.2 billion for cybersecurity. The National Cybersecurity Agency now obliges essential service providers to meet strict perimeter controls, yet only 2% of public administrations currently comply. As municipal portals, welfare payments and national ID services move online, local authorities in Rome, Milan and Turin are upgrading identity management and zero-trust frameworks, often contracting managed security operators to compensate for in-house skill shortages.

Surge in Ransomware Attacks Targeting Italian Industrial Automation Networks

Manufacturing firms absorbed 70% of industrial ransomware incidents in Q4 2024, a shift from mere data theft to operational sabotage. During Q1 2025 alone, Europe logged 135 OT-focused breaches. Factories along the Po Valley are hardening PLCs, segmenting networks and rolling out AI-driven anomaly detection to avoid multi-day production shutdowns. Vendor demand for secure remote-maintenance gateways has reached record levels.

EU NIS2 and DORA Compliance Deadlines Driving Budget Re-allocation Toward Security Tooling

Legislative Decree 138/2024 extended NIS2 coverage to more than 100,000 Italian entities, with fines of up to EUR 10 million or 2% of turnover for gaps. DORA adds sector-specific controls for finance from January 2025. Boards are diverting technology budgets toward log retention, incident reporting automation and threat-intelligence feeds, and 89% of regulated firms expect to hire extra cyber staff. [2]European Union Agency for Cybersecurity, “ENISA Threat Landscape: Finance Sector,” enisa.europa.eu

Cloud-Native Start-up Boom in Milan and Turin Intensifying Demand for SaaS Security Posture Management

TIM’s 2024 alliance with Oracle sparked accelerated multicloud adoption. Venture-backed firms in Milan’s Porta Nuova district and Turin’s innovation precinct scale on Kubernetes yet face GDPR transfer hurdles, prompting uptake of CSPM and CNAPP solutions that map misconfigurations across regions. Cybersecurity vacancies in these hubs are expected to rise 25% in 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Italian-speaking Cyber-Talent Raising MSSP Costs | -1.2% | National, with acute impact in Milan and Rome | Medium term (2-4 years) |

| Prevailing 'Security - Cost Center' Mind-set Within Mid-Market Manufacturing SMEs | -1.8% | National, with concentration in industrial regions | Medium term (2-4 years) |

| Fragmented Legacy Telco Infrastructure Hindering Zero-Trust Roll-outs | -0.8% | National, with emphasis on southern regions and rural areas | Long term (≥ 4 years) |

| Slow Migration from On-Prem HSMs in Highly Regulated BFSI Segment | -0.6% | Milan, Rome, and other financial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Italian-Speaking Cyber-Talent Raising MSSP Costs

Cybersecurity job postings fell 10% between 2022 and 2024 even as demand climbed, leaving 90% of organisations with skills gaps. Local-language SOC analysts command premiums, pushing smaller firms to delegate monitoring to managed security service providers headquartered in Milan and Rome.

Prevailing ‘Security - Cost Center’ Mind-set Within Mid-Market Manufacturing SMEs

OECD surveys show 18% of Italian SMEs operate without any cybersecurity protocols and only 18% are aware of available state aid. [3]OECD, “SME Digitalisation to Manage Shocks and Transitions: 2024 Survey,” oecd.org Many family-owned factories reinsure lost production before they invest in threat prevention, stalling adoption of basic controls such as patching and MFA despite heightened exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Solutions Growth

Solutions held 64.85% of Italy cybersecurity market share in 2025, led by network firewalls and identity platforms. Budget reallocations tied to NIS2 and DORA sustain robust refresh cycles among large banks and utilities. However, services are projected to record a 13.95% CAGR to 2031, eclipsing product growth as enterprises outsource SOC, penetration testing and incident response to mitigate the talent deficit. Managed detection and response platforms now bundle threat-hunting and regulatory reporting, creating sticky multi-year contracts. Italy cybersecurity market size for services is set to surpass USD 3.18 billion by 2031, aided by demand for 24/7 monitoring anchored in Italian language.

Italy cybersecurity market expands as consulting teams guide compliance mapping, architecture redesign and quantum-resilience pilots. Professional services revenues are rising fastest in Rome’s public-sector cluster, while MSSP uptake is highest in Milan’s financial quarter where tier-one banks off-load log correlation and digital-forensics workloads during merger integrations. Identity-as-a-Service and zero-trust assessments also gain traction among healthcare networks preparing for electronic health-record rollouts.

By Deployment Mode: Cloud Adoption Accelerates

On-premise solutions retained 59.85% of Italy cybersecurity market share in 2025, reflecting strong data-sovereignty preferences among critical infrastructure operators. Yet cloud-delivered controls are climbing at an 17.55% CAGR, driven by SaaS productivity suites, remote work, and rising comfort with EU-hosted hyperscale regions. As the Italy cybersecurity market size for cloud deployment surpasses USD 4.36 billion in 2031, demand concentrates on cloud-native SIEM, container runtime defense and policy-as-code automation that streamlines GDPR audits.

Hybrid architectures dominate transitional road maps: threat-intelligence lakes remain on-premise, while vulnerability scanning and backup encryption shift to SaaS. Cross-border data-transfer clauses under GDPR fuel interest in confidential computing and customer-managed keys. Vendors now bundle data-residency dashboards to win cautious public authorities migrating citizen portals to private-cloud nodes in Turin and Bologna.

By Organization Size: SMEs Close the Security Gap

Large enterprises commanded 68.65% of Italy cybersecurity market size in 2025 as banks, telecoms and energy majors maintained layered defenses spanning OT and IT estates. These firms pilot quantum-key-distribution links between data centers and embed AI-based attack-path mapping across dispersed subsidiaries. Compliance with DORA further widens tooling depth, from immutable backups to insider-risk analytics.

The SME segment, forecast to grow 14.88% annually, is unlocking fresh volume for unified threat management appliances and cloud-delivered endpoint security. Tax credits for digital upgrades and lower-priced MDR subscriptions are lowering barriers. Despite progress, only 2% of local authorities and many mid-market manufacturers have reached full framework alignment, highlighting a still-wide protection gap.

By End User: Healthcare Emerges as Growth Leader

BFSI retained a 26.35% revenue share in 2025, with banks accounting for 46% of finance-sector incidents. DORA mandates continuous penetration testing, creating lucrative niches for red-team providers and secure code-review consultancies. Banks deploying quantum-safe encryption report higher return on tangible equity, underlining cyber resilience as a profitability lever.

Healthcare is projected to expand at a 15.92% CAGR as telemedicine adoption swells. Italy cybersecurity market share in electronic medical-record hosting is rising swiftly after a ransomware breach triggered a EUR 25,000 GDPR (USD 29443.75) fine on a university hospital. Hospitals now prioritise privileged-access controls, network segmentation and immutable backups. Cloud-hosted imaging archives further lift demand for HIPAA-aligned CSPM tools.

Geography Analysis

Milan anchors the nation’s fintech and start-up scene. Eighty-two percent of European chief risk officers deem cyber risk their principal concern, pushing Milanese banks to triple spending on threat-intelligence feeds. With cybersecurity roles commanding up to EUR 74,000, the talent squeeze is acute, spurring heavy reliance on MSSPs. Cloud regions launched by hyperscalers draw SaaS vendors, further fuelling the Italy cybersecurity market in Lombardy.

The Po Valley industrial corridor, stretching from Turin to Venice, concentrates OT security deployments. Manufacturers are hardening PLCs and deploying deception grids after repeated ransomware shutdowns. SMEs there still treat security as overhead, explaining slower penetration of EDR and IAM. Regional innovation funds now offer grants covering up to 50% of pilot project costs, nudging family-owned factories toward zero-trust gateways and secure remote monitoring.

Rome remains the policy nucleus. The National Cybersecurity Agency coordinates sector CSIRTs and oversees annual registration of NIS2 entities. Public tenders for SOC-as-a-Service and citizen-ID authentication solutions keep local integrators busy. Yet only a fraction of ministries meet basic protocol benchmarks, highlighting the need for accelerated procurement cycles. Southern regions lag on connectivity, but targeted broadband rollouts under PNRR are beginning to level the field, opening space for tele-health security and municipal e-payment encryption.

Competitive Landscape

The competitive arena blends global brands and specialist Italian firms, with the top ten vendors controlling roughly 60% of overall revenue. Leonardo S.p.A. increased Cyber and Security Solutions turnover by 21% in Q1 2025 to EUR 168 million (USD 197.86 million), aided by sovereign SOC projects. Tinexta has rolled up niche providers to form a national cyber hub, driving cybersecurity sales up 33.4% in the quarter. Reply S.p.A. leverages generative-AI analytics to automate detection, posting an 8.9% revenue rise.

Strategic alliances shape differentiation. TIM’s subsidiary Telsy piloted quantum-key-distribution over existing fibre links, giving early-mover advantage in post-quantum security. Almaviva’s USD 335 million acquisition of Iteris added smart-mobility telemetry that feeds city-wide SOC dashboards. International players such as Palo Alto Networks and CrowdStrike compete on next-gen firewall refreshes and endpoint XDR, but localisation and in-country support remain decisive.

Italy Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems Inc

Trend Micro Incorporated

Dell Technologies Inc.

Broadcom Inc. (Symantec)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tinexta approved FY 2024 accounts showing EUR 106.3 million cybersecurity turnover, projecting >20% growth for 2025.

- January 2025: Tinexta S.p.A. recorded 33.4% growth in cybersecurity sales to EUR 31.9 million, citing strong managed services demand.

- January 2025: Reply S.p.A. posted EUR 603.4 million (USD 710.65 million) Q1 revenues, up 8.9%, with cyber-AI solutions as a core driver.

- January 2025: Leonardo S.p.A. announced a 21% jump in Cyber and Security Solutions revenue to EUR 168 million (USD 197.86 million).

Italy Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and phishing to maintain data confidentiality. The study is structured to track the revenues accrued by cybersecurity vendors through sales of various solutions and allied services.

Italy cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries),. The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Organization Size

| SMEs |

| Large Enterprises |

By End User

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End User | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the current size of the Italy cybersecurity market?

The market is valued at USD 4.65 billion in 2026 and is projected to reach USD 8.48 billion by 2031.

Which segment is expanding fastest within the Italy cybersecurity market?

Services such as managed detection and response are growing at a 13.95% CAGR, the highest among all offerings.

How are EU regulations affecting Italian cybersecurity spending?

The NIS2 Directive and DORA impose mandatory controls and heavy fines, prompting many firms to reallocate budgets toward security tooling and staffing.

Why is healthcare the fastest-growing vertical?

Rapid digitalisation of patient records and a spike in ransomware incidents are pushing hospitals to scale cybersecurity budgets, resulting in a 15.92% forecast CAGR.

What challenges impede market growth?

A shortage of Italian-speaking cyber professionals and a persistent view of security as a cost among manufacturing SMEs are restraining the overall CAGR by nearly three percentage points.

Which regions in Italy show the strongest cybersecurity demand?

Milan leads with heavy BFSI investment, Po Valley focuses on OT security for manufacturing, and Rome drives public-sector procurement under national cyber-perimeter programs.

Page last updated on: