Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

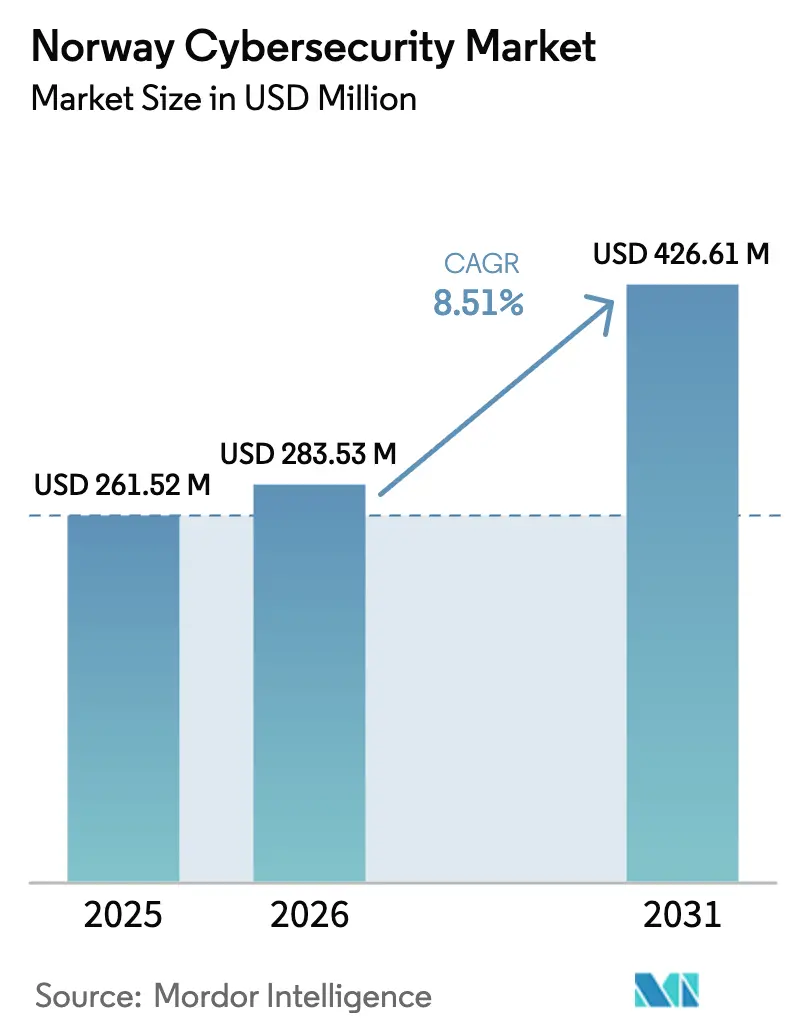

| Base Year Market Size (2025) | USD 261.52 Million |

| Market Size (2026) | USD 283.53 Million |

| Market Size (2031) | USD 426.61 Million |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Cybersecurity Market Analysis by Mordor Intelligence

The Norway cybersecurity market size is projected to be USD 261.52 million in 2025, USD 283.53 million in 2026, and reach USD 426.61 million by 2031, growing at a CAGR of 8.51% from 2026 to 2031. Norway’s shift toward sovereign cloud regions, the modernization of Arctic and offshore energy infrastructure, and the steady cadence of state-sponsored intrusions sustain double-digit annual spending increments. The Digital Security Act, effective since October 2025, continues to pull security investments forward as enterprises adopt compliance automation while escalating threat activity from Chinese and Russian APT groups elevates demand for managed detection and response. Intensifying workload migration to Azure, AWS, and Google Cloud drives uptake of cloud workload protection, and the fusion of operational technology and information technology inside substations, drilling rigs, and maritime fleets widens the Norway cybersecurity market addressable base. At the same time, workforce scarcity and SME price sensitivity temper near-term upside, compelling vendors to refine automation and flexible consumption options.

Key Report Takeaways

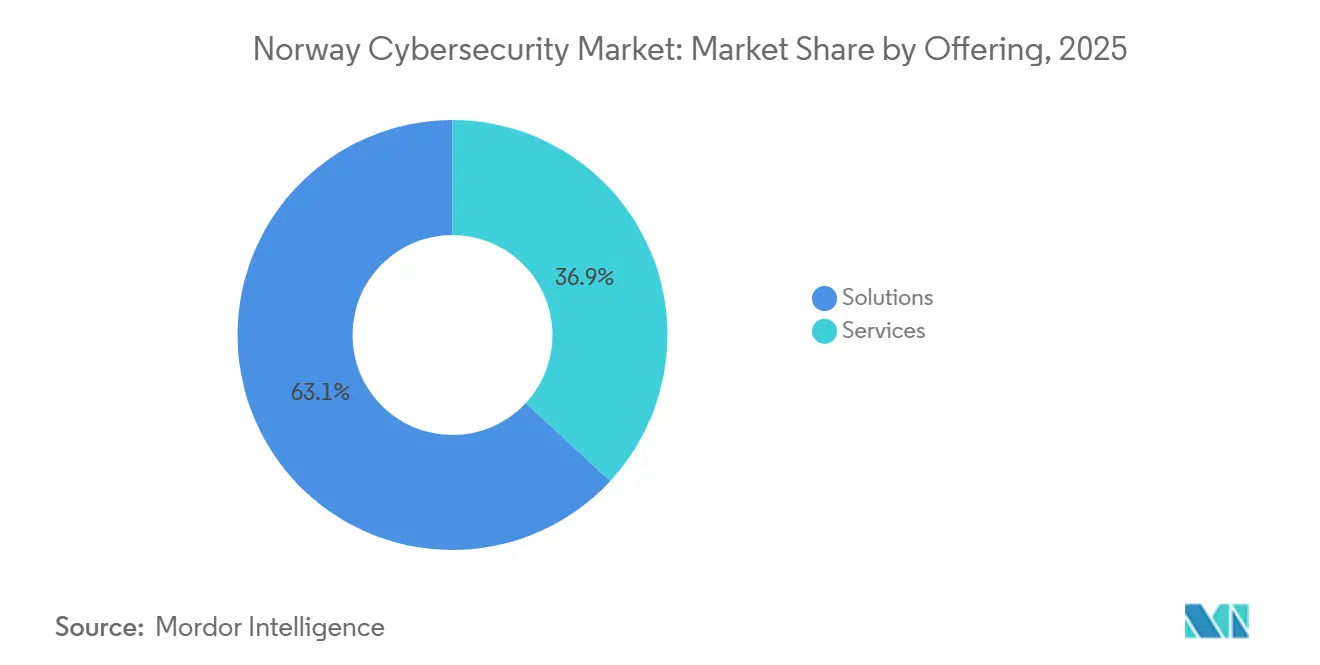

- By offering, Solutions led with 63.11% of Norway cybersecurity market share in 2025, whereas Services are forecast to post the fastest 8.82% CAGR through 2031.

- By deployment mode, cloud captured 57.43% of the Norway cybersecurity market size in 2025 and is expected to advance at a 9.26% CAGR between 2026 and 2031.

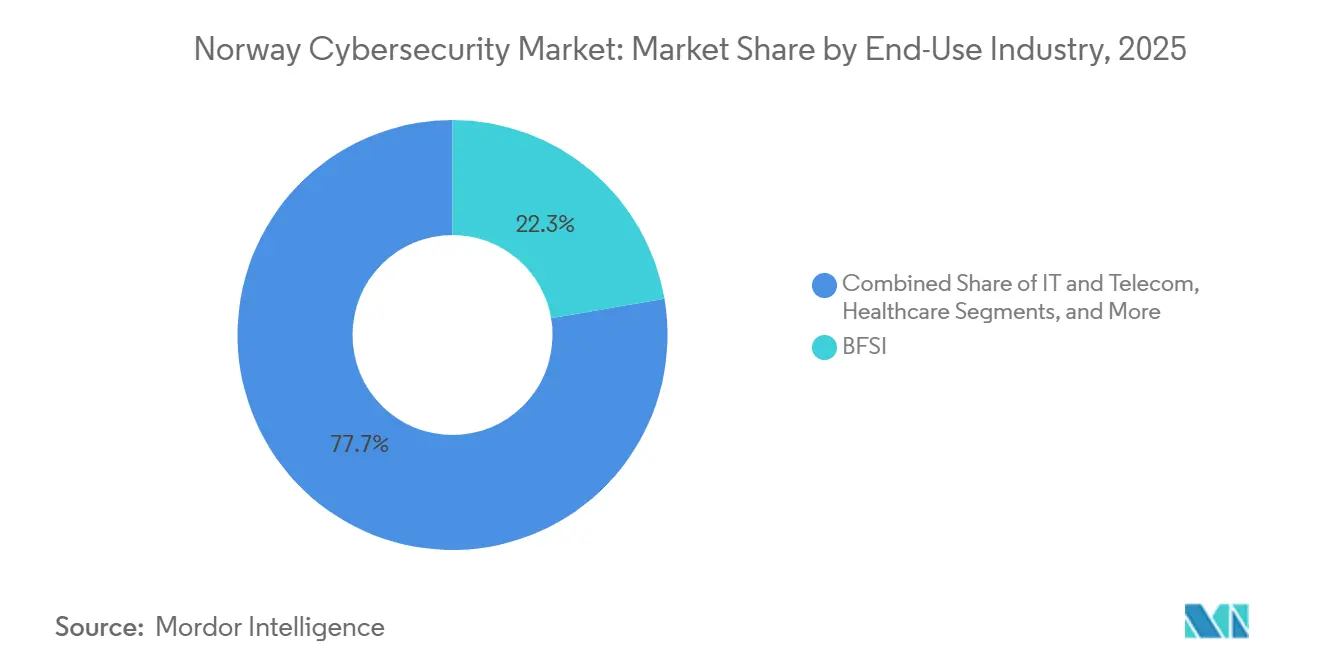

- By end-use industry, Banking, Financial Services, and Insurance held 22.31% revenue share in 2025, while Healthcare is set to expand at the strongest 10.26% CAGR to 2031.

- By enterprise size, Large Enterprises represented 68.36% spending in 2025, yet Small and Medium Enterprises are projected to grow the fastest at 9.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Norway Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Sophistication of Cyber Threat Landscape | +1.9% | National with emphasis on Oslo, Bergen, Stavanger | Short term (≤ 2 years) |

| Accelerated Cloud Adoption Among Norwegian Enterprises | +2.1% | Oslo, Trondheim, Bergen metropolitan areas | Medium term (2-4 years) |

| Stringent National Cybersecurity Regulations and Directives | +1.6% | Compliance-driven across all sectors | Medium term (2-4 years) |

| Rapid Digital Transformation in Critical Infrastructure Sectors | +1.8% | Energy hubs in Stavanger, Trondheim and maritime clusters | Long term (≥ 4 years) |

| Government Funding for Arctic Digital Resilience Initiatives | +1.0% | Northern Norway including Tromsø, Bodø, Kirkenes | Long term (≥ 4 years) |

| Growing Adoption of Offshore Wind Farm SCADA Security Solutions | +0.8% | Coastal North Sea and Norwegian Sea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication Of Cyber Threat Landscape

Salt Typhoon compromised telecom links to siphon government and defense data in early 2026, underscoring how organized state groups now probe Norway’s core infrastructure. APT28’s 2025 e-mail spear-phishing against logistics operators raised ransomware counts in the maritime vertical to 72 incidents, pushing NORMA Cyber to impose vessel-level EDR by 2027. BankBot strains that bypass MFA on Norwegian mobile banking apps have moved lenders toward adaptive authentication. Together, these incursions compel continuous monitoring services, zero-trust frameworks, and threat intelligence subscriptions, enlarging the Norway cybersecurity market.

Accelerated Cloud Adoption Among Norwegian Enterprises

Public and hybrid cloud workloads reached 68% penetration by end-2025 as CIOs chased scalability and cost relief.[1]Norwegian Digitalisation Agency, “Cybersecurity Workforce Shortage Projection,” DIGDIR.NO DNB routed NOK 1.3 billion (USD 120 million) into cloud-native application security, mirroring Nordea’s EUR 1.5 billion (USD 1.7 billion) technology spend that targets full data-center exit by 2028. Aker ASA’s 230-megawatt Narvik data center furnishes Azure sovereign regions, satisfying GDPR residency mandates. Multi-cloud complexity propels uptake of cloud security posture management and workload protection suites, feeding the Norway cybersecurity market growth pipeline.

Stringent National Cybersecurity Regulations And Directives

The Digital Security Act enforces 72-hour breach reporting and ISO/IEC 27001 alignment, with fines capping at 2% of global turnover.[2]Norwegian Government, “Digital Security Act,” REGJERINGEN.NO Healthcare now follows Normen Code 7.0, obligating encryption and annual pen-testing across e-health estates. Anticipated NIS2 transposition by late 2026 broadens compliance to mid-sized suppliers in energy and transport, accelerating demand for governance, risk, and compliance automation. Mandatory registration for >1 MW data centers brings physical and cyber resiliency oversight, anchoring fresh investment cycles.

Rapid Digital Transformation In Critical Infrastructure Sectors

Statnett set aside NOK 150-200 billion (USD 13.9-18.5 billion) for smart grid rollouts through 2034, inserting IP-enabled assets that require industrial firewalls and anomaly detection. SecurEL’s consortium, led by SINTEF, scales IEC 61850-aware intrusion detection for 40+ DSOs until 2033. Offshore operators Equinor and Aker BP test AI-driven analytics on drilling rigs via Cognite’s USD 164 million platform, deepening IT-OT convergence. These projects lift security budgets throughout the energy value chain, reinforcing the Norway cybersecurity market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Cybersecurity Professionals | -1.3% | National, pronounced in rural and Northern Norway | Short term (≤ 2 years) |

| High Cost of Advanced Security Solutions for SMEs | -0.9% | SMEs outside Oslo and Bergen | Medium term (2-4 years) |

| Latency Issues in Rural Northern Norway Affecting Cloud Security Effectiveness | -0.3% | Finnmark, Troms, Nordland | Long term (≥ 4 years) |

| Fragmented Incident Reporting Culture Among Norwegian SMEs | -0.2% | Retail, hospitality, light manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Skilled Cybersecurity Professionals

Norway faces a projected 3,500 deficit in cyber roles by 2030, with universities graduating fewer than 400 specialists in 2025. Telenor formed vocational pipelines after reporting hiring hurdles for its Cyberdefence wing. Rural municipalities rely on part-time consultants, delaying patch cycles and compliance audits. Although a national cyber reserve is under study, implementation drifts beyond 2027, so automation and managed services must bridge the resource gap near term, lightly constraining the Norway cybersecurity market.

High Cost Of Advanced Security Solutions For SMEs

Average SME spend stands near NOK 500,000 (USD 46,300) yearly, equal to 3-5% of IT budgets.[3]Norwegian Digitalisation Agency, “Cybersecurity Workforce Shortage Projection,” DIGDIR.NO XDR subscriptions often exceed NOK 1,200 (USD 111) per seat each month, pushing retail and hospitality owners toward basic antivirus. KommuneCERT subsidizes MDR across only 120 of 356 municipalities, leaving many micro-firms uncovered. Cost friction, together with underreported incidents, limits threat-intel sharing and slows Norway cybersecurity market penetration among the long-tail of businesses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain As Outsourcing Accelerates

Services revenue is projected to compound at 8.82% annually through 2031 as firms pivot toward round-the-clock monitoring instead of running proprietary SOCs. Orange Cyberdefense Norway’s Oslo CyberSOC now processes 3.5 billion daily events for 200 clients, illustrating how outsourced detection meets surge demand from ransomware-plagued energy and public bodies. Professional services flourish under the 72-hour reporting clause, with auditors rushing to map control gaps. Solutions, however, still delivered 63.11% of 2025 spending because endpoint, network, and identity stacks remain foundational cornerstones of the Norway cybersecurity market.

Cloud security solutions outpace legacy tools, policing policy drift across Azure, AWS, and Google Cloud realms and satisfying boards’ appetite for visibility. Data-centric security spans encryption and DLP to align with GDPR, while risk quantification dashboards bring ISO 31000 narratives to senior leadership. Network and endpoint layers guard a mobile workforce, and ruggedized appliances from Fortinet protect harsh offshore rigs. Together, the blended stack cements recurring revenue within the Norway cybersecurity market.

By Deployment Mode: Cloud Leads On Sovereignty And Scalability

Cloud claimed 57.43% Norway cybersecurity market share in 2025, then registered the segment’s fastest 9.26% CAGR outlook. The National Digitalisation Strategy steers government workloads to sovereign regions, aided by Aker ASA’s Narvik megacenter that anchors local Azure zones. Finance and healthcare migrate sandbox and analytics clusters first, maintaining sensitive payment or patient records in country yet benefiting from cloud elasticity. Security posture management platforms therefore become default guardrails, ensuring encryption key ownership and drift remediation.

On-premises continues to serve low-latency SCADA control rooms inside substations and drilling rigs, where air-gapped designs still dominate. Payment card core processing likewise retains hardware security modules behind vault doors. Hybrid blueprints now prevail, splitting regulated data between secure private racks and cloud AI sandboxes. The Norwegian Communications Authority’s 1 MW registration rule also standardizes on-prem and colocation resiliency thresholds, tightening baseline expectations across the Norway cybersecurity market.

By End-Use Industry: Healthcare Surges On Digitalization Mandates

Healthcare revenues will escalate at 10.26% CAGR to 2031, spurred by Normen Code 7.0 that prescribes encryption of every electronic health record field and annual red-team drills. Regional health trusts have started to ring-fence imaging repositories behind zero-trust gates after observing European hospital ransomware shutdowns. BFSI still commanded 22.31% of 2025 turnover because DNB and Nordea each funneled nine-figure budgets into behavioral analytics and cloud-native defenses to stymie BankBot.

Energy and utilities allocate part of Statnett’s NOK 150-200 billion smart-grid war chest to OT firewalls and intrusion monitoring, while Telenor prioritizes 5G signaling protection. Industrial manufacturing integrates segmentation at robotic workcells, and retail chains layer fraud analytics over e-commerce stacks. Defense programs in the Arctic, funded through NOK 50 billion allocations, further widen TAM for ruggedized solutions, collectively expanding the Norway cybersecurity market size.

By End-User Enterprise Size: SMEs Accelerate Despite Cost Barriers

SMEs are forecast to add 9.74% CAGR as KommuneCERT subsidies and cyber insurance clauses force security adoption. Cloud-based security-as-a-service bundles reduce startup costs, letting a 20-person fishing exporter in Bodø tap MDR dashboards once reserved for banks. The Norway cybersecurity market size for SMEs therefore rises from a low base, even though licensing sticker shock remains palpable.

Large Enterprises, still 68.36% of 2025 spend, deploy advanced SOAR playbooks and threat-intel fusion. Equinor, Aker BP, and Telenor collectively exceed NOK 5 billion outlays, pulling ecosystem partners into vendor certifications. These blue-chip accounts drive roadmap influence and early AI-based analytics rollouts, anchoring the high end of the Norway cybersecurity market.

Geography Analysis

Oslo, Bergen, Stavanger, and Trondheim concentrate over 70% of cyber spending as headquarters clusters for finance, energy, and telecom. Oslo hosts Mnemonic, Netsecurity, and Watchcom SOCs, giving enterprises local data residency plus Norwegian-language incident response. Stavanger’s offshore energy majors equip drilling rigs with ruggedized next-gen firewalls and machine-learning anomaly sensors, channeling sizeable slices of the Norway cybersecurity market.

Northern Norway benefits from NOK 50 billion defense injections and the Arctic Broadband Network operational since December 2024, yet fiber penetration still lags 60% in Finnmark and Troms, creating latency gaps for real-time cloud defenses.[4]Norwegian Communications Authority, “Data Center Registration Mandate,” NKOM.NO Aker ASA’s Narvik data center supplies sovereign Azure zones, bolstering local compute while drawing heat reuse into greenhouses. As broadband coverage climbs toward 90% by 2030, SMEs in Kirkenes and Hammerfest can shift workloads cloudward, broadening regional slices of the Norway cybersecurity market.

Coastal North Sea wind projects deploy encrypted SCADA tunnels and segmented turbine controllers, attracting niche vendors versed in maritime OT. Trondheim’s university and SINTEF labs test IEC 61850 firmware hardening, feeding SecurEL prototypes into DSOs nationwide. These academic-industry linkages reinforce innovation density and sustain the Norway cybersecurity industry flywheel.

Competitive Landscape

The field is moderately fragmented. Mnemonic leverages its Argus platform to parse 10 billion events daily and integrates Nordic government intel feeds for regional actor specificity. Netsecurity capitalizes on tight partnerships with municipal councils, bundling compliance dashboards that map each clause of the Digital Security Act. Watchcom spots opportunity in continuous red-teaming against maritime fleets, referencing 72 live vessel honeypots in the Norwegian Sea.

Global majors anchor cloud and endpoint layers, Microsoft’s long-term Azure contract at Narvik locks sovereign workloads, Cisco ruggedizes industrial firewalls for Statnett’s substations, while Palo Alto Networks pilots AI-operated policy engines on Equinor rigs. Fortinet and CrowdStrike push zero-trust suites through Telenor’s 5G slices, and Orange Cyberdefense scales incident response headcount locally by 40% to cover SLA upticks.

White-space niches include offshore wind OT security, where turbine-vendor ecosystems lack uniform segmentation. Arctic Security introduces Nordic-tuned threat-intel feeds, and Cognite embeds data operations plus anomaly models directly in Aker BP’s drilling digital twins. Vendor differentiation now orbits around compliance automation, Norwegian-language SOC analysts, and local data residency, all prerequisites for sustainable Norway cybersecurity market share gains.

Norway Cybersecurity Industry Leaders

Mnemonic AS

Netsecurity AS

Watchcom Security Group AS

Visma Group Holding AS

Telenor ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Norwegian Police Security Service confirmed Salt Typhoon breaches in telecom infrastructure, triggering NSM monitoring directives.

- January 2026: Aker ASA valued its Nscale Narvik data center at NOK 6.7 billion (USD 620 million) following Azure sovereign region uptake.

- October 2025: Directorate of eHealth enforced Normen Code 7.0, compelling encryption and annual penetration tests across health IT estates.

- October 2025: Digital Security Act became effective, mandating 72-hour incident reporting and ISO/IEC 27001 alignment.

Norway Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Norway Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Norway cybersecurity market in 2026?

Norway cybersecurity market size is estimated at USD 283.53 million in 2026 with an 8.51% CAGR outlook to 2031.

Which deployment model grows the fastest?

Cloud solutions lead, expanding at a 9.26% CAGR as sovereign regions and multi-cloud adoption accelerate.

What sector shows the highest growth?

Healthcare is projected to post a 10.26% CAGR through 2031 after encryption and zero-trust mandates took effect in 2025.

Why are SMEs investing more in security?

The Digital Security Act’s extended scope and KommuneCERT subsidies lower entry costs, pushing SME cybersecurity spend up 9.74% CAGR.

Which regulation most impacts spending?

The Digital Security Act, effective Oct 2025, enforces 72-hour breach reporting and ISO/IEC 27001 alignment, compelling rapid controls deployment.

Who are the key Norwegian vendors?

Mnemonic, Netsecurity, and Watchcom Security Group headline local expertise, supplemented by Microsoft, Cisco, and Palo Alto Networks.

Page last updated on: