Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

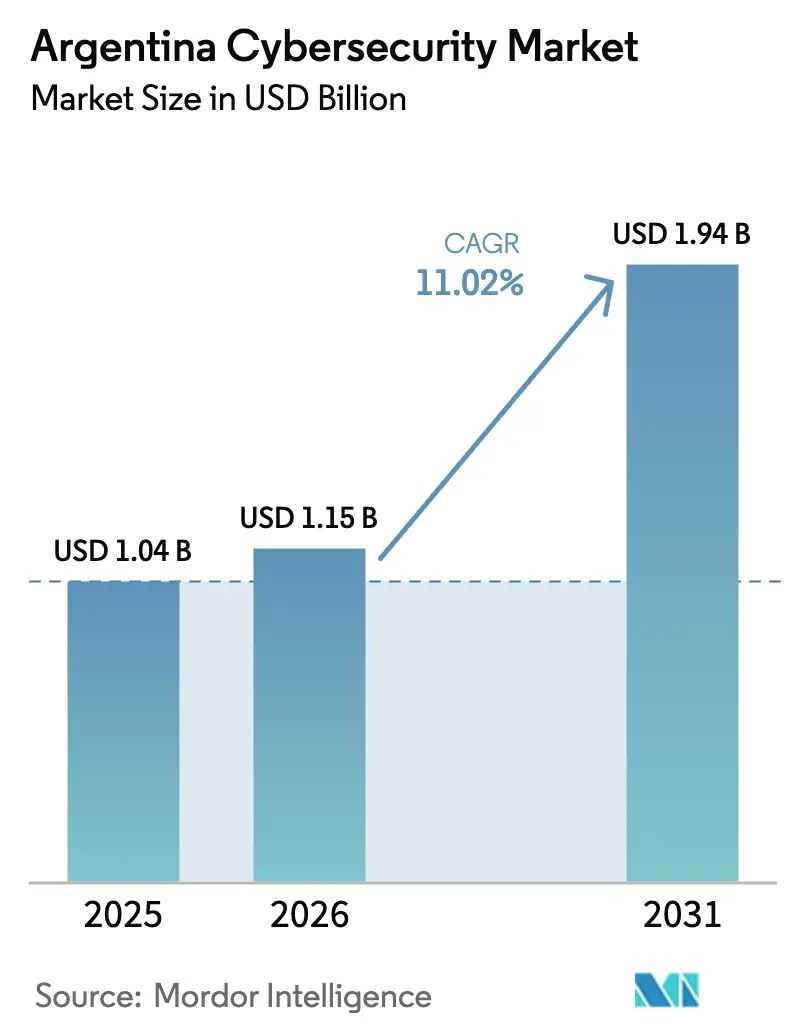

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

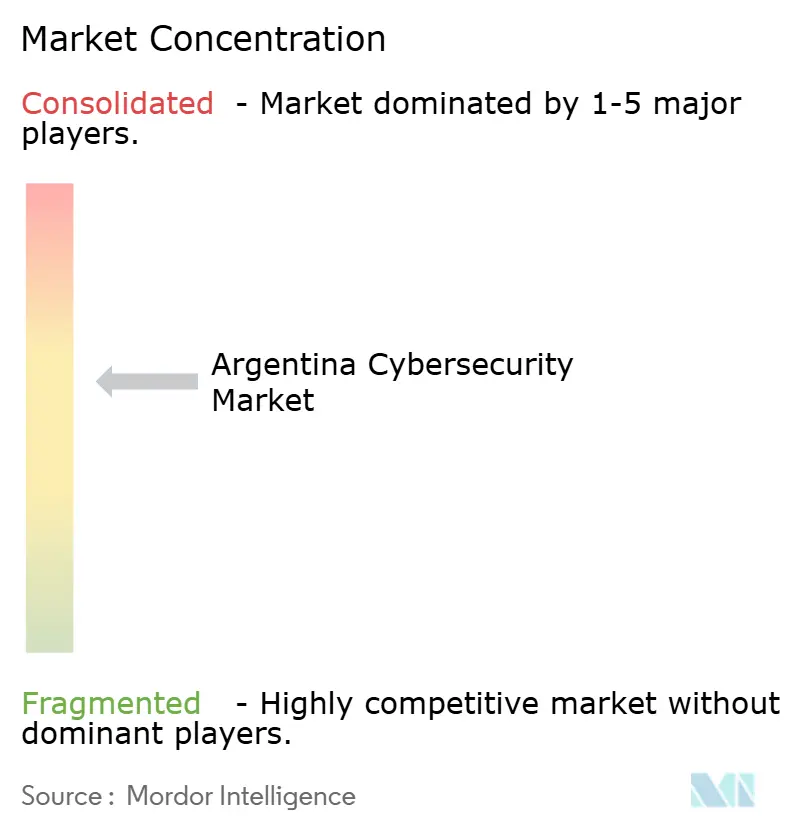

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Cybersecurity Market Analysis by Mordor Intelligence

The Argentina cybersecurity market size is expected to increase from USD 1.04 billion in 2025 to USD 1.15 billion in 2026 and reach USD 1.94 billion by 2031, growing at a CAGR of 11.02% over 2026-2031. The upward curve mirrors the country’s ranking as Latin America’s third-most-attacked economy, the 260 million intrusion attempts recorded by Fortinet in Q1 2024, and the rapid capacity build-out triggered by the National Cybersecurity Centre that became operational in January 2026. Digital-first banking, booming e-commerce activity, and cloud mandates for regulated sectors keep the Argentina cybersecurity market on a double-digit growth path despite inflation pressures that temper discretionary IT spending. The solutions segment still dominates but the managed-services wave is accelerating as enterprises outsource threat hunting, while cloud deployment retains its lead because Central Bank Communication A 7724 effectively obliges banks to adopt cloud-native controls. Rising attack sophistication, Spanish-language phishing, and a 329,000-person regional talent gap further elevate demand for identity, endpoint, and SIEM products that embed automation and analytics.

Key Report Takeaways

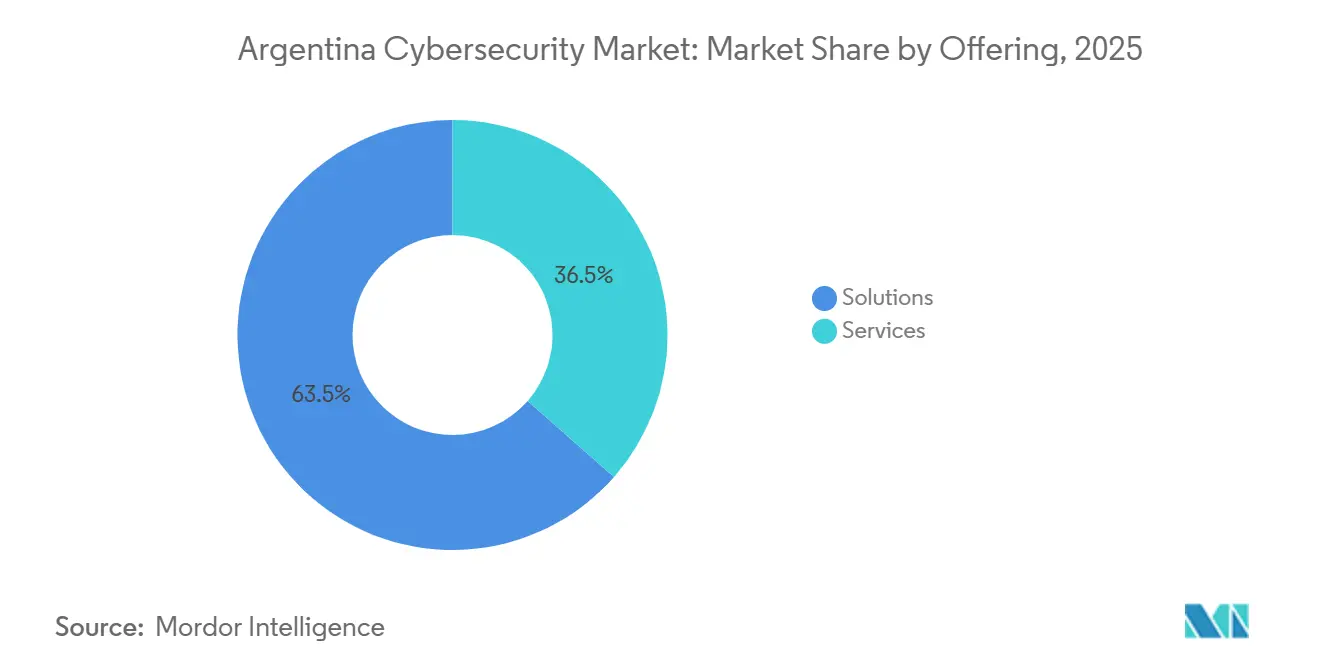

- By offering, solutions led with 63.53% revenue share in 2025; services are advancing at an 11.82% CAGR through 2031.

- By deployment mode, cloud deployment captured 57.27% of the Argentina cybersecurity market share in 2025, while the same mode is projected to expand at a 12.06% CAGR to 2031.

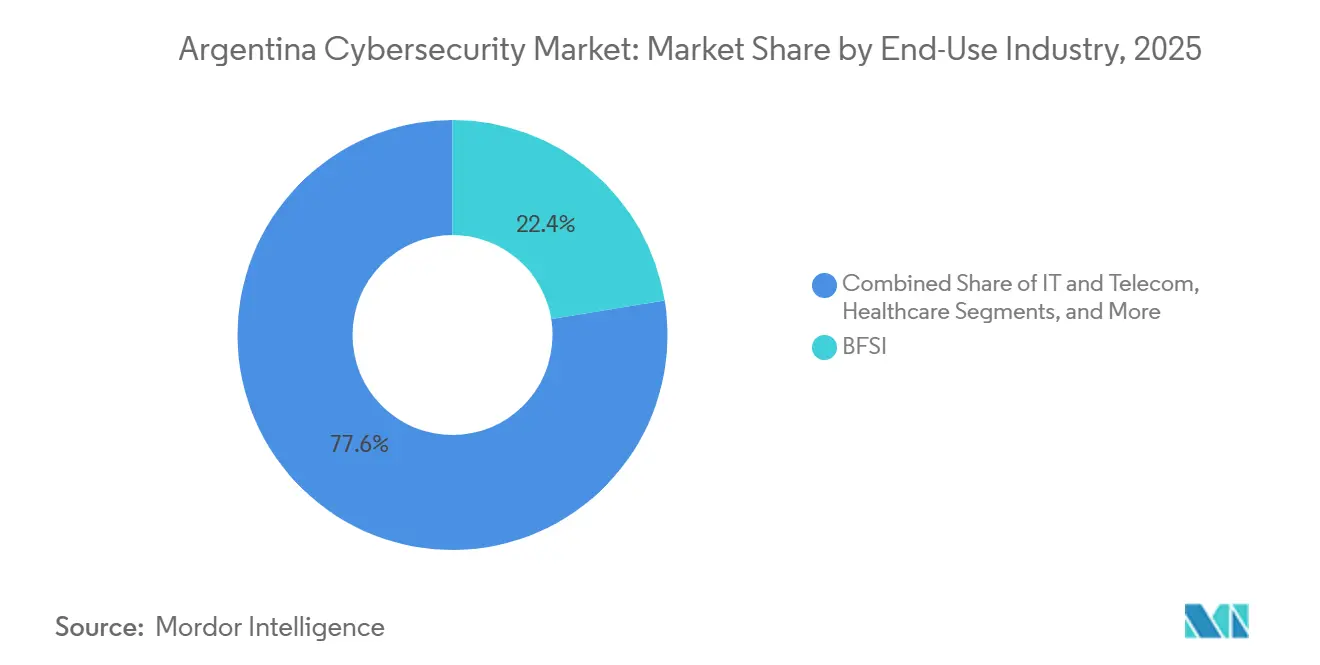

- By end-use industry, BFSI commanded 22.43% of 2025 spending and retail is set to grow at a 12.92% CAGR between 2026-2031.

- By enterprise size, large enterprises accounted for 68.31% of outlay in 2025 and small and medium enterprises are pacing ahead at a 12.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital Transformation Among Argentine Enterprises | +2.3% | National, with early gains in Buenos Aires, Córdoba, Rosario | Medium term (2-4 years) |

| Uptake of Cloud-Native Workloads in Regulated Sectors | +2.1% | National, concentrated in BFSI and Healthcare hubs | Medium term (2-4 years) |

| Mandatory Zero-Trust Architecture Guidelines From National Cybersecurity Directorate | +1.8% | National, phased rollout across federal agencies and critical infrastructure | Long term (≥ 4 years) |

| Surge in Sophisticated Spanish-Language Phishing Campaigns | +1.6% | National, highest impact in Buenos Aires metropolitan area | Short term (≤ 2 years) |

| Expansion of 5G Private Networks in Industrial Hubs | +1.4% | Regional, focused on mining, oil, ports, agroforestry zones | Long term (≥ 4 years) |

| Emergence of Buenos Aires as a Regional FinTech Hub | +1.2% | Buenos Aires and Greater Buenos Aires metropolitan region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital Transformation Among Argentine Enterprises

Improving security now tops the digital-transformation agenda, according to GSMA’s 2025 Mobile Economy report.[1]GSMA, “Mobile Economy 2025,” gsma.com Financing from the World Bank and the Inter-American Development Bank earmarked for data-center and broadband upgrades has expanded the potential surface for cyberattacks. Telecom Argentina lifted its data-center count to 16 in September 2025, each engineered for 10 MW loads that support AI-heavy traffic, and deployed micro-segmentation to isolate assets. The ITU Global Cybersecurity Index ranks Argentina in the “Evolving” tier, indicating large headroom for maturity and governance improvements. Smartphone tax reductions announced in 2025 are forecast to add 4 million users, widening the mobile attack surface and sustaining demand for SASE solutions.

Uptake of Cloud-Native Workloads in Regulated Sectors

Communication A 7724 from the Central Bank compels financial institutions to embed monitoring, logging, and playbooks directly into cloud stacks, pushing the Argentina cybersecurity market toward SaaS-delivered controls. Google Cloud advertises out-of-the-box compliance to fast-track core banking migration. Healthcare follows suit after ANMAT released prescriptive cybersecurity requirements for telemedicine and Software as a Medical Device, with standards N70 and N73 taking full effect in 2026. The National Securities Commission’s Resolution 1058/2025 extends similar mandates to crypto platforms. Vendors such as BioCatch demonstrated scalability by rolling out a behavioral-biometrics platform across multiple Argentine banks in three months.

Mandatory Zero-Trust Architecture Guidelines From National Cybersecurity Directorate

Argentina’s Second National Cybersecurity Strategy outlines a phased zero-trust roadmap. The National Cybersecurity Centre, live since January 2026, now centralizes audits, incident response, and threat-intelligence feeds. Telefónica Tech reported that its Security Edge with ZTNA Next 360 trimmed customer incidents by 60% and boosted performance by 45%, proving real-world payoffs. A July 2024 budget injection of 100 billion pesos (USD 80 million) accelerates zero-trust pilots across ministries handling citizen data. Procurement rules that favor identity federation, continuous authentication, and micro-segmentation are already influencing vendor shortlists.

Surge in Sophisticated Spanish-Language Phishing Campaigns

UFECI logged 34,468 cybercrime complaints in 2024, with phishing in the lead. CERT.ar observed seasonal spikes when actors impersonated the tax authority, while Check Point documented a December 2025 wave targeting e-signature portals. ZULA Ciberseguridad revealed a 47% phishing success rate within finance departments at SMEs. The Mi Argentina identity portal breach that compromised 13,000 accounts prompted mandatory multi-factor authentication across government websites. Phishing awareness services, DMARC adoption, and secure e-signature workflows now feature prominently in enterprise RFPs, adding momentum to the Argentina cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Cybersecurity Talent With Spanish and Portuguese Fluency | -1.4% | National, acute in provinces outside Buenos Aires | Long term (≥ 4 years) |

| Persistent Macroeconomic Volatility Affecting IT Budgets | -1.8% | National, disproportionate impact on SMEs | Short term (≤ 2 years) |

| High Informality Rate Limiting Security Spending by SMEs | -1.1% | National, concentrated in retail, hospitality, construction | Medium term (2-4 years) |

| Delayed Enforcement of National Data-Protection Bill | -0.9% | National, regulatory uncertainty affecting compliance investments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Cybersecurity Talent With Spanish and Portuguese Fluency

ISC2’s workforce study pegs the region’s gap at 329,000 professionals, and bilingual analysts remain scarce. The OECD SME Policy Index scores Argentina under the regional average on digital skills, and even leaders such as Globant compete fiercely for talent.[2]OECD, “SME Policy Index for Latin America 2025,” oecd.org The Knowledge Economy Law eases payroll taxes for technology firms yet has not solved the pipeline deficit. As a result, managed service providers pitch 24/7 monitoring staffed from regional SOCs, a trend that increases service penetration in the Argentina cybersecurity market.

Persistent Macroeconomic Volatility Affecting IT Budgets

Inflation and peso depreciation elevate the cost of imported security appliances and subscriptions. Telecom Argentina’s mid-2025 capex expanded by 53.7% year-over-year when expressed in pesos, illustrating currency drag on procurement. SMEs feel the squeeze acutely and often restrict spending to essential endpoint and network tools. Until inflation stabilizes and the new data-protection bill is enforced, complex GRC platforms and AI-enabled analytics will see staggered uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Enterprises Outsource Threat Hunting

Services spending in the Argentina cybersecurity market size for this category is projected to outpace solutions at an 11.82% CAGR across 2026-2031. Telecom Argentina’s multitenant SOC launched in October 2025 exemplifies the trend, consolidating monitoring across four Southern Cone economies. Managed detection and response, vulnerability assessments, and compliance audits resonate with firms that lack in-house skills. The solutions basket still held 63.53% of 2025 revenue, anchored by cloud security and identity suites aligned with zero-trust mandates. ANMAT’s enforcement of secure SDLC for Software as a Medical Device pushes application-security uptake, while Central Bank communication requirements keep IAM and data-loss prevention high on the shopping list. Professional services wrap consulting and training around these stacks, appealing to BFSI and healthcare operators navigating layered local regulations.

In 2025, application security, cloud security, and IAM ruled procurement cycles, each mapping to either regulatory diktats or rapid SaaS adoption. Cloud-native SIEM and SOAR tools are now bundled with MSSP retainers. Meanwhile, network and endpoint security remain foundational because Fortinet’s telemetry showed 260 million attempted attacks in a single quarter. The Argentina cybersecurity market share for managed services is set to expand steadily as SOC build-outs by Claro, Metrotel, and regional ISPs intensify competition and lower price points.

By Deployment Mode: Cloud Dominance Reinforced by Regulatory Mandates

Cloud captured 57.27% of Argentina cybersecurity market share in 2025 and is forecast to grow at a 12.06% CAGR through 2031. Central Bank Communication A 7724, CNV Resolution 1058/2025, and ANMAT’s healthcare standards collectively nudge enterprises to migrate workloads or adopt cloud-based controls. Google Cloud advertises pre-certified controls, while BioCatch’s Trust Argentina rollout illustrates elastic scale.

On-premises solutions persist where air-gapped operational-technology or data-residency rules apply. Hybrid models, blended by Cisco’s network modernization push, allow sensitive workloads to stay on-premises while offloading log analytics or backup to the cloud. ENACOM’s low-cost spectrum allocation expedites private-5G pilots, creating fresh demand for containerized firewalls and micro-segmentation in edge locations. The Argentina cybersecurity market continues to tilt cloudward, yet integration middleware and secure gateways are crucial for hybrid continuity.

By End-Use Industry: Retail Surges on E-Commerce Fraud Prevention

BFSI dominated spend with 22.43% in 2025 as instant transfers and QR payments soared. Retail and e-commerce, however, is the fastest mover with a 12.92% CAGR expected, propelled by Mercado Libre’s 647 million live listings and 99% proactive fraud filtering. IT and telecom players upgrade perimeter and data-center defenses to support AI traffic, while healthcare sees budget shifts toward secure telemedicine. Manufacturing adopts 5G private networks in mining and ports, necessitating operational-technology firewalls and anomaly detection. The Argentina cybersecurity market size for OT security will rise as energy and utilities confront ransomware incidents documented by Entel Digital.

B2B marketplaces and logistics providers are now embedding application programming interface level security to protect the rising flow of instant-transfer settlement instructions that reached 603.4 million transactions in December 2024. BioCatch reports that account-takeover attempts spike during seasonal sales, prompting large retailers to pair behavioral biometrics with AI-based chargeback scoring. Meanwhile, healthcare networks are allocating part of their 2026 telemedicine budgets to micro-segmentation and privileged-access management so that Software as a Medical Device deployments comply with standards N70 and N73. Energy producers experimenting with private-5G rigs in Patagonia now request ruggedized next-generation firewalls that operate in temperatures below -10 °C, a niche that regional vendors are starting to fill. Collectively, these vertical-specific moves reinforce double-digit growth in the Argentina cybersecurity market by broadening demand beyond traditional BFSI strongholds.

By Enterprise Size: SMEs Accelerate on Tax Incentives

Large enterprises own 68.31% of 2025 spending, but SMEs will log the fastest expansion at 12.43% CAGR. Knowledge Economy Law tax credits trim cost barriers, and the Federal Cybercrime Prevention Plan subsidizes assessments. SMEs remain high-risk targets, with a 47% phishing success rate in administrative departments. Managed services tailored for Spanish-language awareness training and cloud-hosted mail filters lower entry hurdles, deepening Argentina cybersecurity market penetration outside Buenos Aires.

Cloud-delivered endpoint suites priced on a per-device basis are gaining traction after Claro’s Southern Cone SOC began offering a bundled plan that starts at 50 seats, an entry point aligned with the median Argentine SME headcount. ZULA Ciberseguridad’s 2025 field tests show that phishing-click rates fall below 12% when SMEs adopt quarterly micro-training instead of annual sessions, encouraging insurers to discount cyber-premiums for participants. The Ministry of Security is piloting a voucher scheme that reimburses up to 40% of first-year MSSP subscriptions for firms outside Buenos Aires, channeling Federal Cybercrime Prevention Plan funds toward regional inclusion. As these incentives stack up, the Argentina cybersecurity market sees a virtuous cycle in which lower upfront costs expand the protected footprint, and a wider customer base in turn attracts new local managed-service entrants.

Geography Analysis

Buenos Aires and its metropolitan ring absorb most budgets, courtesy of dense BFSI, fintech, and telecom headquarters. BYMA Ventures’ 2025 investment in cybersecurity startups reinforces the city’s position as a regional innovation hub. Córdoba and Rosario form secondary corridors across automotive and agribusiness, yet talent scarcity outside the capital means many firms rely on remote SOCs or cloud-resident defenses. Inflationary stress has a sharper bite in the provinces, pressing CISOs to favor incremental upgrades over platform swaps.

The National Cybersecurity Centre now supplies nationwide threat intelligence and coordinates with provincial CERTs, a move expected to harmonize maturity levels. An IDB-financed USD 30 million program continues to harden energy grids and water systems across non-metropolitan zones. ENACOM’s spectrum policy lowers connectivity costs for private networks, incentivizing industrial players in Patagonia and the Northwest to trial edge security stacks. As smartphone adoption rises by 4 million new users countrywide, mobile-threat defense demand expands beyond urban cores, spreading the Argentina cybersecurity market footprint.[3]Telecom Argentina, "Annual Report 2024 and Investor Presentations 2025," telecom.com.ar

Argentina’s Tier 4 ranking in the ITU index signals that legal and organizational pillars still lag regional leaders. Nevertheless, accession to the International Counter Ransomware Initiative injects global best practices into local playbooks, elevating readiness even in resource-strained provinces. Financial incentives, regulatory nudges, and national coordination are laying the groundwork for more balanced growth of the Argentina cybersecurity market across geographies.

Competitive Landscape

The Argentina cybersecurity market displays moderate fragmentation, with the top five vendors controlling about 40% of revenue. Palo Alto Networks, Fortinet, Cisco, CrowdStrike, and IBM lean on global threat-intelligence networks, bolstering appeal to multinationals. Telefónica Tech rides Spanish-language support and regional cloud nodes to win mid-market accounts. Local integrators BGH Tech Partner and Snoop Consulting turn regulatory fluency into turnkey compliance suites, assisting banks and virtual-asset service providers with A 7724 or Resolution 1058 adherence.

Strategy themes include regional SOC rollouts, as Claro’s October 2025 facility and Metrotel’s USD 14 million hub illustrate. Vendors also chase the SME opportunity with subscription bundles that pair endpoint agents with phishing simulation localized for Argentina. BioCatch exemplifies disruptive moves, scaling behavioral biometrics via cloud APIs in under a quarter, while Telecom Argentina’s Akamai Guardicore deployment proves domestic appetite for micro-segmentation. Cisco’s Country Digital Accelerator commitment to training 200,000 professionals by 2028 underscores ecosystem investment. Price competition remains intense, yet niche providers offering OT firewalls or Spanish-language threat feeds carve defensible positions.

Private-equity interest is rising, illustrated by BYMA Ventures’ seed investments in three Buenos Aires start-ups that develop Spanish-language phishing emulation engines and low-code compliance-automation bots. International vendors respond by deepening channel alliances; CrowdStrike signed a 2025 distribution deal with BGH Tech Partner to target provincial industrial clients that require on-premises data retention. At the same time, Metrotel’s new SOC intends to white-label its telemetry platform for smaller regional ISPs, potentially fragmenting market share even further. Skill development also features in competitive positioning, with Cisco pledging to train 10,000 Argentine cybersecurity specialists by 2028 under its Country Digital Accelerator roadmap. These capital infusions, channel expansions, and workforce programs indicate that rivalry will intensify, yet they also broaden solution availability, ultimately supporting sustained growth of the Argentina cybersecurity market.

Argentina Cybersecurity Industry Leaders

-

Palo Alto Networks Inc.

-

Fortinet Inc.

-

Cisco Systems Inc.

-

Check Point Software Technologies Ltd.

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Argentine government established the National Cybersecurity Centre, a federal coordination body responsible for incident response, threat intelligence, and compliance audits.

- December 2025: Metrotel announced a USD 14 million investment to build a Cybersecurity Hub in Argentina, expanding its managed-services portfolio.

- November 2025: Cisco added Argentina to its Country Digital Accelerator program, earmarking resources for network modernization and cybersecurity capacity building.

- October 2025: Claro Argentina launched a Southern Cone Security Operations Center, consolidating monitoring for Argentina, Chile, Uruguay, and Paraguay.

Argentina Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Argentina Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the projected value of the Argentina cybersecurity market in 2031?

Forecasts place the market at USD 1.94 billion by 2031, advancing at an 11.02% CAGR over 2026–2031.

Which deployment mode is growing fastest among Argentine buyers?

Cloud deployment is expanding at a 12.06% CAGR as Central Bank rules and healthcare mandates favor cloud-native controls.

Why are services outpacing solutions in spending growth?

Enterprises facing a 329,000-person talent gap prefer managed detection, response, and compliance audits delivered by external SOCs.

Which end-use vertical shows the highest growth momentum?

Retail and e-commerce leads with a projected 12.92% CAGR thanks to proactive fraud-prevention investments by platforms such as Mercado Libre.

How does macroeconomic volatility influence security budgets?

Inflation and peso depreciation raise the cost of imported tools, pushing SMEs to focus on essential endpoint and network defenses and delaying adoption of advanced analytics.

Are there regional differences in cyber maturity within Argentina?

Buenos Aires enjoys higher investment and talent density, while provinces rely more on cloud services and IDB-funded critical-infrastructure hardening.

Page last updated on: