Robotic Medical Imaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

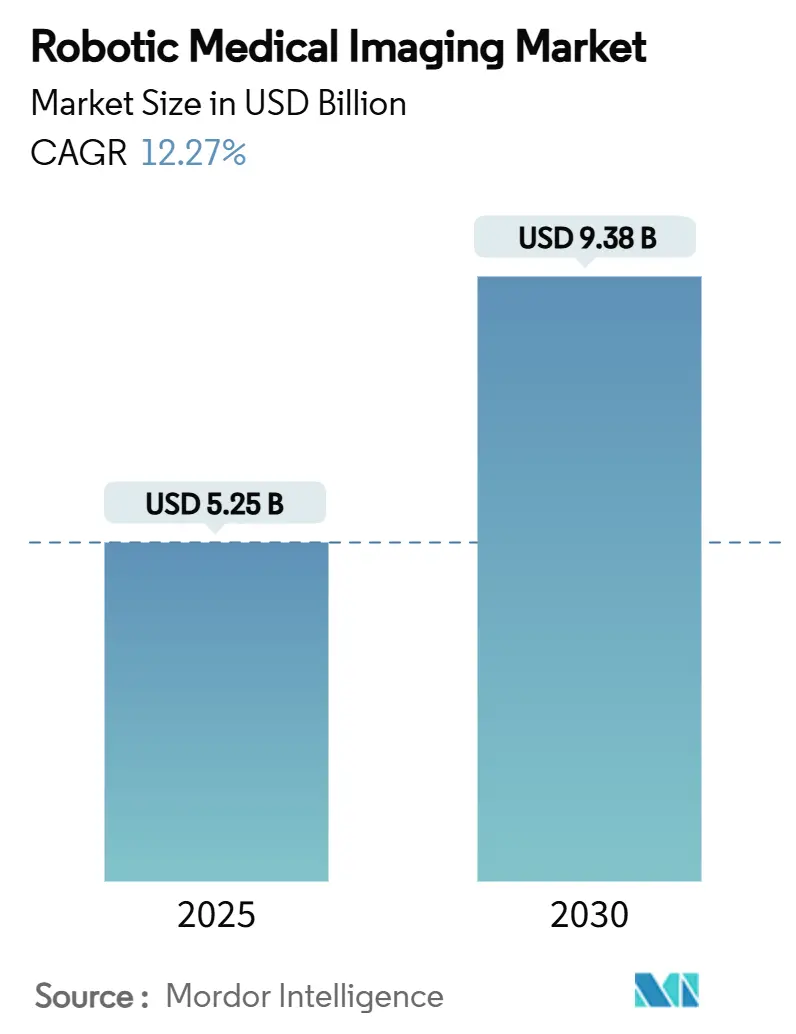

| Market Size (2025) | USD 5.25 Billion |

| Market Size (2030) | USD 9.38 Billion |

| Growth Rate (2025 - 2030) | 12.27% CAGR |

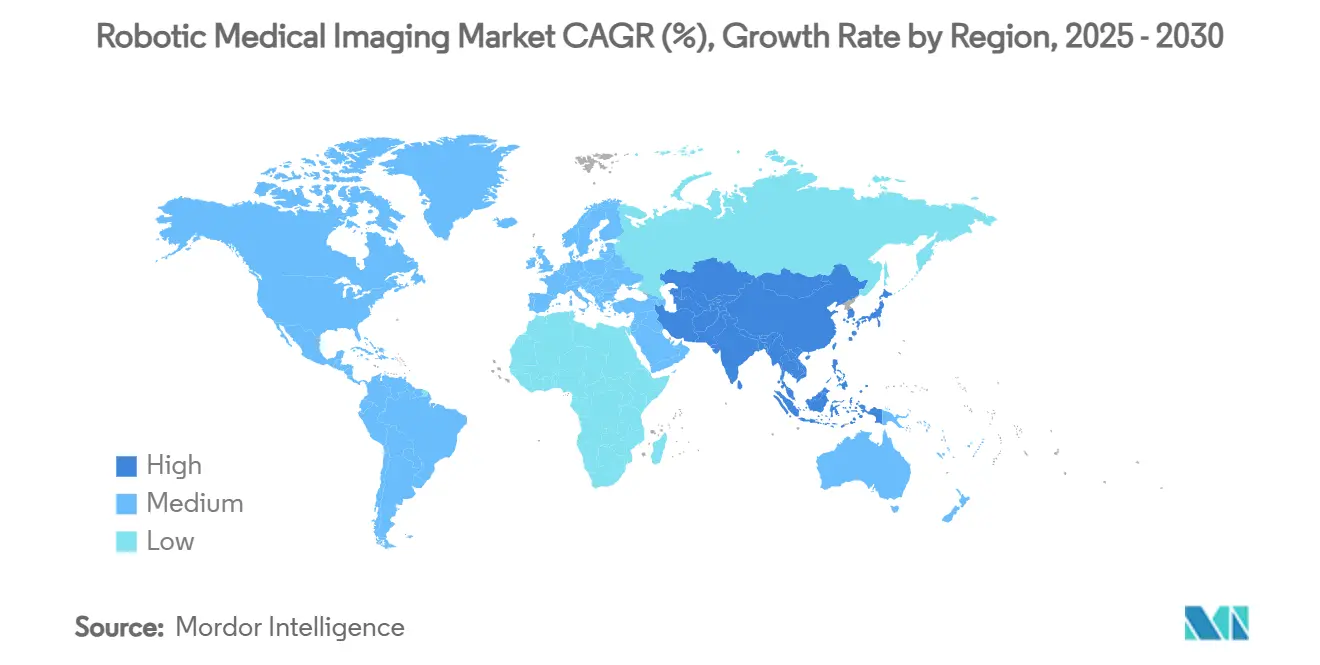

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

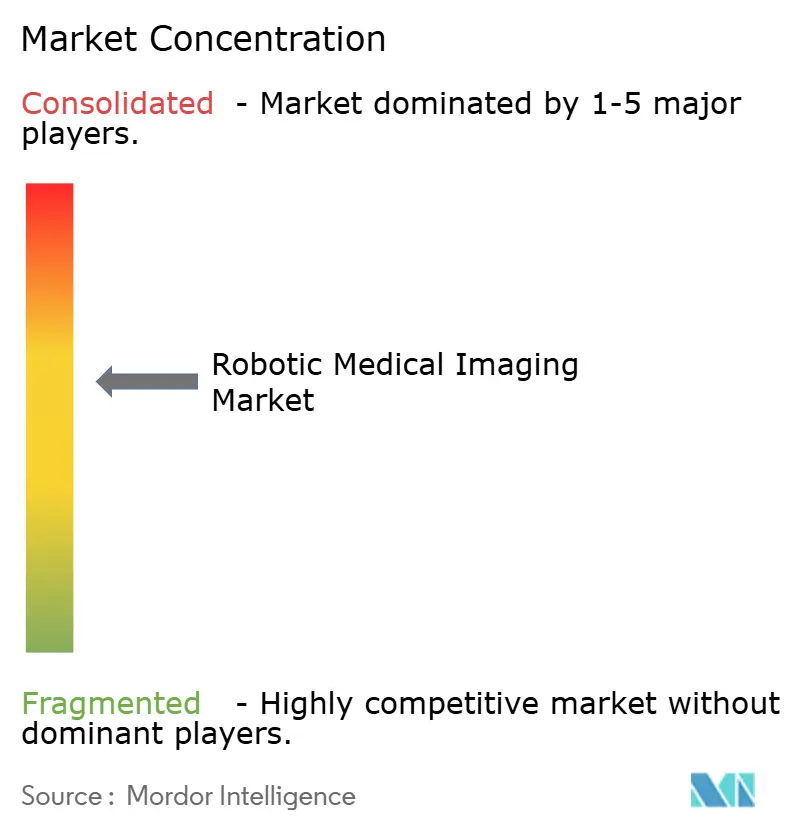

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Medical Imaging Market Analysis by Mordor Intelligence

The robotic medical imaging market size is valued at USD 5.25 billion in 2025 and is forecast to reach USD 9.38 billion by 2030, reflecting a 12.27% CAGR. Adoption accelerates as artificial intelligence merges with surgical robotics, enabling 40% fewer intra-operative imaging errors than conventional techniques.[1]Food and Drug Administration, “Marketing Submission Recommendations for a Predetermined Change Control Plan for Artificial Intelligence-Enabled Device Software Functions,” FDA.gov Miniaturized robotic arms now deliver bedside imaging and reshape workflow patterns in hybrid operating rooms and intensive-care units. Venture funding, favorable reimbursement, and the transition toward outpatient surgical settings keep commercial momentum strong. Established suppliers respond with continuous platform upgrades, while emerging players target cost-sensitive segments with collaborative robots. Capital-expenditure hurdles and component supply constraints temper the otherwise positive growth outlook.

Key Report Takeaways

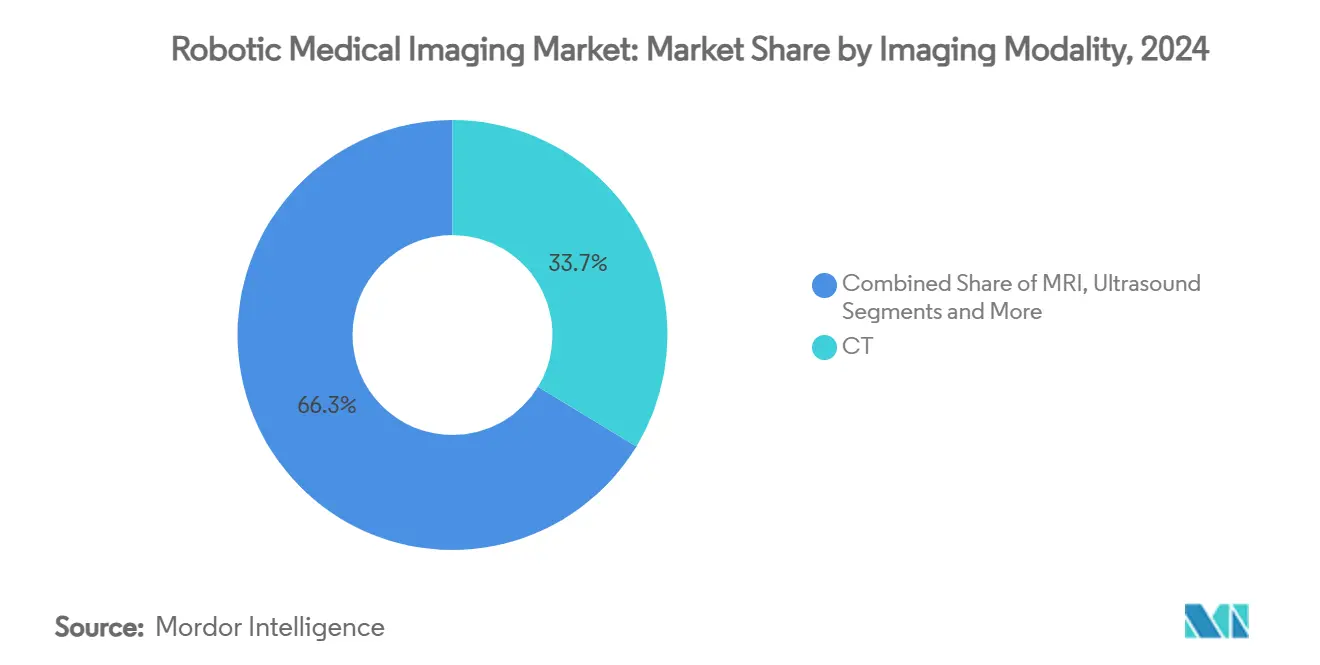

- By imaging modality, CT retained 33.67% of robotic medical imaging market share in 2024, whereas MRI applications are expanding at a 15.42% CAGR through 2030.

- By robot type, articulated platforms led with 39.68% share of the robotic medical imaging market size in 2024, while collaborative robots record the highest 16.34% CAGR to 2030.

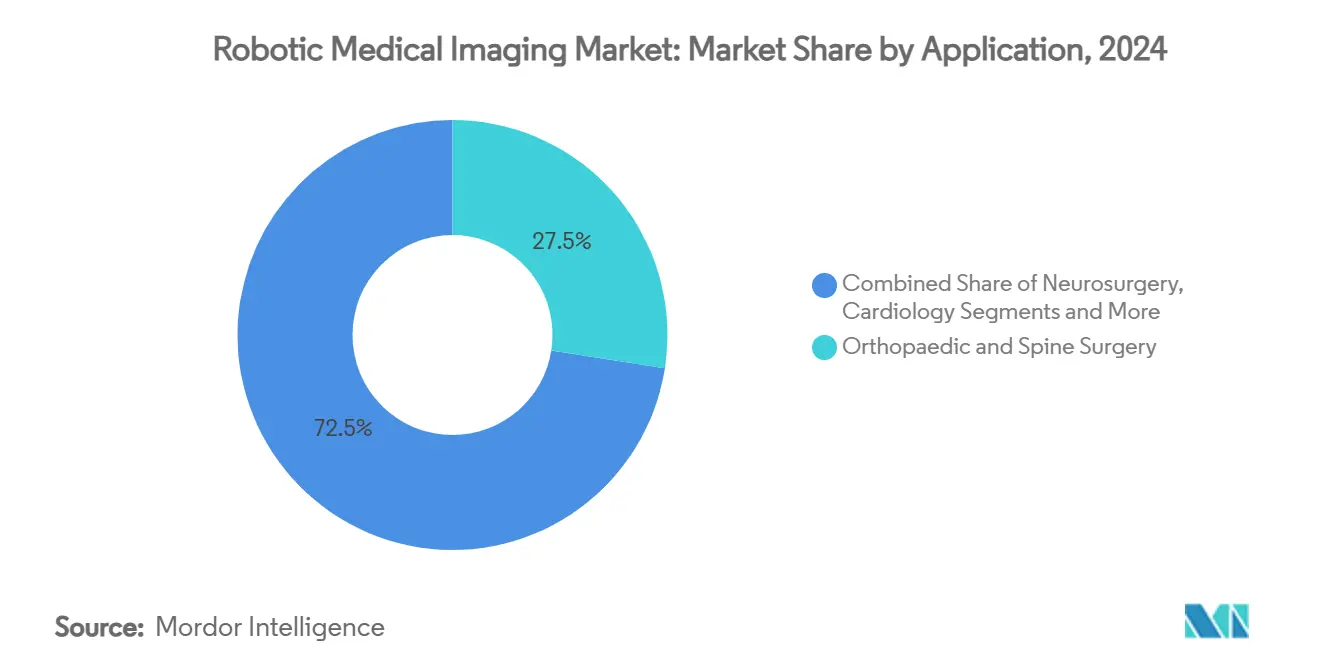

- By application, orthopedic and spine surgery captured 27.48% of robotic medical imaging market share in 2024; oncology biopsy and ablation is poised for the fastest 15.11% CAGR.

- By end user, tertiary hospitals held 44.77% share of the robotic medical imaging market size in 2024, whereas ambulatory surgical centers are projected to expand at a 14.77% CAGR.

- By geography, North America commanded 36.49% share of the robotic medical imaging market in 2024, and Asia-Pacific represents the fastest-growing region with a 14.83% CAGR.

Global Robotic Medical Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-powered image guidance reduces intra-operative errors | +2.1% | North America, Europe, global diffusion | Medium term (2–4 years) |

| Miniaturized robotic arms enable bedside imaging | +1.8% | Asia-Pacific core, spill-over to North America | Short term (≤2 years) |

| Rising hybrid OR installations in tier-2 hospitals | +1.4% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Shift to outpatient surgical centers demanding compact systems | +1.6% | North America primary, Europe secondary | Medium term (2–4 years) |

| Reimbursement expansion for robotic fluoroscopy in the United States | +1.2% | United States | Short term (≤2 years) |

| Venture-capital surge for MRI-compatible robots in China | +2.3% | China, wider Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Image Guidance Reduces Intra-Operative Errors

FDA-cleared platforms demonstrate a 40% decline in navigation errors during complex procedures.[2]Food and Drug Administration, “Clarification of Radiation Control Regulations for Manufacturers of Diagnostic X-Ray Equipment,” FDA.gov Siemens’ CIARTIC Move mobile C-arm, cleared in 2024, automatically positions itself using AI-driven anatomical recognition. Surgeons no longer perform repeated manual adjustments that once added 15–20 minutes per case. Multi-modal imaging is processed within milliseconds, giving sub-millimeter visual accuracy that is vital in neurosurgery and structural-heart interventions. The FDA’s predetermined change-control pathway allows software upgrades without lengthy resubmissions, shortening innovation cycles for vendors.

Miniaturized Robotic Arms Enable Bedside Imaging

Actuator advances shrink robotic footprints by 60% yet maintain 0.1 mm precision; WeMed’s ETcath robot, approved in China in 2025, weighs under 50 kg. Bedside ultrasound and CT units limit patient transport risks and cut infection exposure in critical-care wards. Carbon-fiber structures and brushless servo motors support mobility without compromising structural rigidity. The largest gains appear in pediatric and geriatric care, where patient mobility is restricted.

Rising Hybrid OR Installations in Tier-2 Hospitals

Hybrid operating rooms in secondary facilities climbed 35% in 2024. Integrating imaging and therapy lets surgeons switch seamlessly between diagnostic scans and interventions, lowering combined care costs up to 30%. Broader access enables communities to manage cardiovascular and neurovascular cases locally rather than referring to urban tertiary centers. Demand for robotic imaging inside these ORs grows as hospitals aim to maximize throughput.

Shift to Outpatient Surgical Centers Demanding Compact Systems

Ambulatory surgical centers process same-day procedures and value platforms setting up in under 10 minutes within 400–600 sq ft rooms. Medicare spent USD 6.1 billion on ASCs treating 3.3 million beneficiaries in 2022, underscoring economic relevance.[3]Maria X. Sanmartin, “Cost-Effectiveness of Remote Robotic Mechanical Thrombectomy in Acute Ischemic Stroke,” Journal of Neurosurgery, thejns.org Portable systems boost turnover and reduce nursing staff training burdens. Developers respond with modular architectures to fit tight floorplans without performance compromises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for small hospitals | –1.9% | Global, acute in developing regions | Long term (≥4 years) |

| Lack of standardized interoperability protocols | –1.1% | Global, variable by regulator | Medium term (2–4 years) |

| Radiologist–surgeon credentialing bottlenecks | –0.8% | North America, Europe | Short term (≤2 years) |

| Supply-chain fragility for specialized actuators | –1.4% | Global, Asia-Pacific manufacturing concentration | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Small Hospitals

Annual ownership reaches USD 2.5 million once training, service contracts, and facility retrofits are included. Volumes below 500 cases rarely recoup outlays, leaving rural and community hospitals unable to justify purchases. Shared-service and leasing models exist but hinge on administrative coordination many sites lack.

Lack of Standardized Interoperability Protocols

Multiple robotic brands coexist in large centers, each using proprietary data formats. Despite ISO/IEEE 11073 progress, full adoption is several years away. Manual data entry raises error rates and lengthens procedure timelines. Emergency deployments become cumbersome when systems cannot exchange imaging files seamlessly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Imaging Modality: MRI Drives Innovation Despite CT Dominance

CT retained 33.67% of robotic medical imaging market share in 2024 as health systems relied on its speed for trauma and routine diagnostics. MRI-guided platforms, however, outpace with a 15.42% CAGR as clinicians demand real-time image guidance for neurosurgical and cardiac interventions. Cloud-based MRI leveraging 6G bandwidth extends scans beyond hospital walls, while MRI-compatible robots overcome ferromagnetic restrictions. Ultrasound systems exploit portability and cost advantages in point-of-care environments. Fluoroscopy and traditional X-ray remain essential for cardiovascular and orthopedic guidance, yet advance through AI dose-optimization algorithms.

Emerging cloud MRI tools deliver sub-millimeter biopsy precision, and GE HealthCare’s Revolution Vibe CT shortens cardiac scan times. Multimodal platforms that fuse CT, MRI, and ultrasound into a single robotic interface promise holistic diagnostics but intensify interoperability challenges. Vendors that resolve these technical barriers stand to capture cross-modality opportunities within the robotic medical imaging market.

By Robot Type: Collaborative Systems Reshape Surgical Workflows

Articulated robots kept 39.68% of the robotic medical imaging market size in 2024, favored for six-axis dexterity during orthopedic and cranial work. Collaborative robots, or cobots, are advancing fastest at 16.34% CAGR. Their inherent safety allows human teammates to work inside the operating envelope without cages, making them ideal for space-constrained ambulatory centers. SCARA designs deliver repeatable linear pathways in radiology suites, while Cartesian robots target niche linear tracking tasks.

Cobots linked via 5G enable cross-border telesurgery; a 1,700 km remote gastrectomy in 2025 proved clinical feasibility. Force-feedback and haptics minimize tremor and surgeon fatigue, enhancing precision in lengthy ablation sessions. Future software updates will further automate positioning tasks, freeing staff for higher-value decision making.

By Application: Oncology Precision Drives Fastest Growth

Orthopedic and spine surgery dominated 2024 revenue at 27.48%, reflecting entrenched robotic adoption in joint replacements. Oncology biopsy and ablation leads growth at 15.11% CAGR, mirroring precision-medicine imperatives. Interventional radiology employs robotic navigation for complex vascular mapping, whereas neurosurgery requires the highest positional accuracy inside eloquent brain areas. Cardiology focuses on minimally invasive valve and electrophysiology work, where robotic stability improves electrode placement.

Robotic bronchoscopy now reaches peripheral lung nodules and delivers 99.1% lesion targeting accuracy. MRI-guided ablation of prostate and liver tumors provides exact thermal dosing, sparing adjacent tissue. The oncology pipeline therefore remains a primary innovation frontier inside the robotic medical imaging market.

By End User: ASCs Challenge Hospital Dominance

Tertiary hospitals accounted for the largest spend at 44.77% in 2024, justified by high case complexities and academic research mandates. Ambulatory surgical centers, though smaller, are expanding at 14.77% CAGR. These centers prize faster turnarounds and lower overhead, adopting compact robotic imaging that fits within modest floorplans. Specialty clinics in orthopedics and ophthalmology form a niche but high-throughput environment where single-purpose robots excel.

Value-based care incentives accelerate the shift as payers reward cost-effective outpatient options. Vizient data showed 13% growth in outpatient advanced imaging during 2024. Vendors tailoring price points and service packages for ASCs could unlock a sizeable share of the robotic medical imaging market.

Geography Analysis

North America held 36.49% of the robotic medical imaging market in 2024, supported by early FDA approvals and Medicare reimbursement. Asia-Pacific is the fastest climber at 14.83% CAGR, fueled by Chinese venture backing and national modernization programs. Europe advances steadily, emphasizing clinical-evidence generation and strict regulatory adherence. The Middle East and Africa emerge as opportunity zones tied to medical tourism and greenfield hospital construction.

Chinese financing rounds narrowed to nine in 2024 yet delivered larger ticket sizes, including Ruilong Surgery’s CNY 300 million raise. India counts 170 installed da Vinci systems and over 850 trained surgeons, highlighting regional appetite for advanced robotics. Future 6G networks promise ultra-low latency, further boosting remote surgical prospects.

Competitive Landscape

Leading suppliers maintain an innovation edge yet face rising cost-pressure from nimble entrants. Intuitive Surgical installed 147 da Vinci 5 units in Q1 2025, pushing quarterly revenue to USD 2.25 billion, a 19% gain. GE HealthCare purchased Intelligent Ultrasound’s AI diagnostics arm for USD 51 million, combining hardware with decision-support algorithms. Canon’s Adora DRFi adds robotic positioning to conventional radiography, streamlining technologist workload.

Competitors now differentiate through connectivity, AI integration, and modularity. Emerging Chinese firms leverage government grants to undercut on price while emphasizing MRI compatibility. Supply-chain diversification and predictive maintenance services become strategic must-haves in bids. Leasing and outcome-based contracts appear increasingly in ambulatory segments, lowering upfront barriers and shifting vendor revenue toward service annuities.

Robotic Medical Imaging Industry Leaders

Intuitive Surgical Inc.

Siemens Healthineers AG

Medtronic plc

Stryker Corp.

Canon Medical Systems Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare introduced Revolution Vibe CT featuring Unlimited One-Beat Cardiac imaging that completes a full cardiac view within a single heartbeat.

- March 2025: Canon Medical received FDA clearance for the Adora DRFi hybrid solution which merges robotic positioning with digital radiography to enhance imaging workflow.

Global Robotic Medical Imaging Market Report Scope

| CT |

| MRI |

| Ultrasound |

| Fluoroscopy & X-ray |

| Cartesian Robots |

| SCARA Robots |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Interventional Radiology |

| Orthopaedic & Spine Surgery |

| Neurosurgery |

| Cardiology |

| Oncology Biopsy & Ablation |

| Tertiary Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Imaging Modality | CT | |

| MRI | ||

| Ultrasound | ||

| Fluoroscopy & X-ray | ||

| By Robot Type | Cartesian Robots | |

| SCARA Robots | ||

| Articulated Robots | ||

| Collaborative Robots (Cobots) | ||

| By Application | Interventional Radiology | |

| Orthopaedic & Spine Surgery | ||

| Neurosurgery | ||

| Cardiology | ||

| Oncology Biopsy & Ablation | ||

| By End User | Tertiary Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the robotic medical imaging market?

The robotic medical imaging market size stands at USD 5.25 billion in 2025 with growth forecast to USD 9.38 billion by 2030.

Which imaging modality shows the highest growth potential?

MRI-guided robotic systems are projected to expand at a 15.42% CAGR due to real-time intra-operative guidance advantages.

Why are ambulatory surgical centers important for vendors?

ASCs offer the fastest 14.77% CAGR because they need compact, quick-setup robots that fit tight rooms and enhance same-day procedure throughput.

Which region is growing the fastest?

Asia-Pacific leads with a 14.83% CAGR, supported by Chinese venture funding and expanding smart-hospital infrastructure.

What is the primary cost barrier to broader adoption?

Total ownership costs average USD 2.5 million annually for small hospitals, covering equipment, service, and facility upgrades.

How do collaborative robots differ from traditional articulated robots?

Collaborative robots operate safely beside staff without barriers and currently log the highest 16.34% CAGR, whereas articulated robots still dominate installed base share.

Page last updated on: